Compensation and Revenue Models

This topic covers how broker-dealers earn money and compensate their representatives, focusing on the structural differences between commission-based and fee-based models, markups and markdowns, spreads, and advisory compensation. Understanding these models is critical for the SIE exam because questions test your ability to identify appropriate compensation structures, calculate transaction costs, and distinguish between agent and principal transactions.

Core Concepts

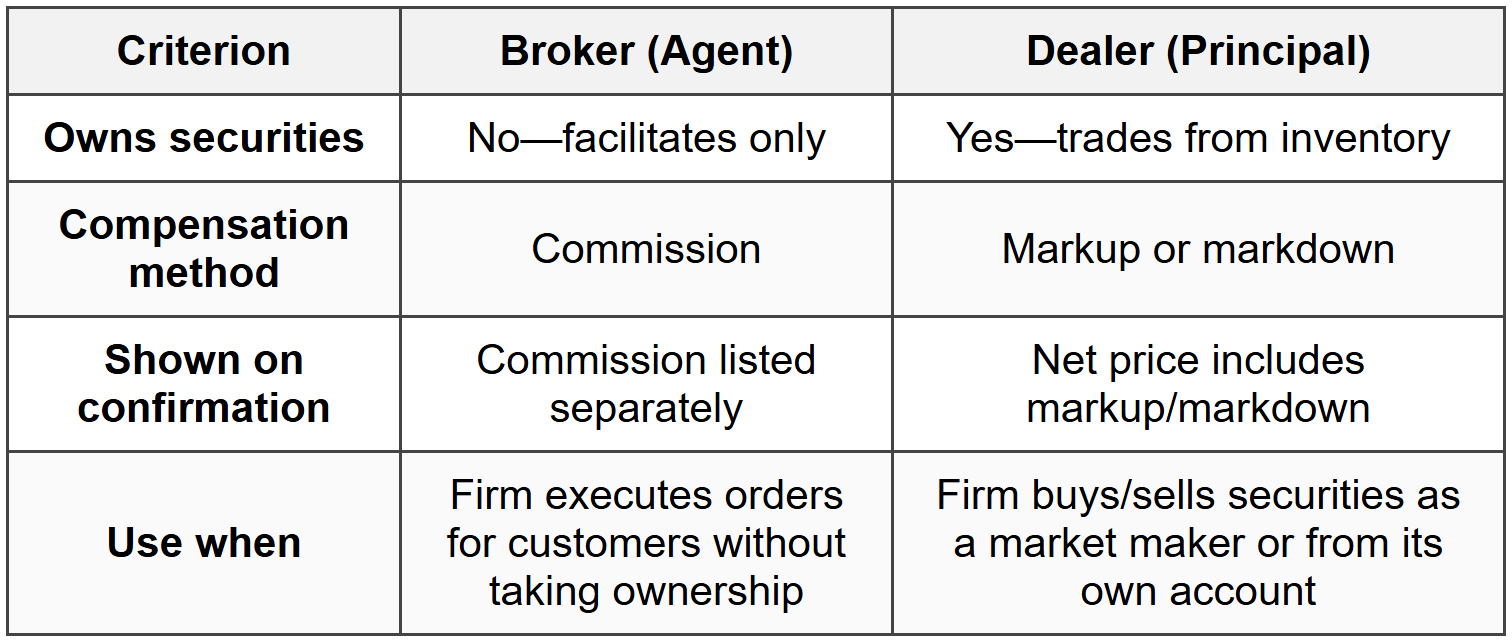

Broker vs. Dealer Functions

A broker acts as an agent for a customer, executing trades on behalf of the client and earning a commission for the service. The broker does not own the securities being traded and simply facilitates the transaction between buyer and seller.

A dealer acts as a principal, buying and selling securities from its own inventory. The dealer profits from the spread-the difference between what it pays to buy securities (the bid) and what it charges to sell them (the ask). No commission is charged in a principal transaction; instead, the dealer's compensation is embedded in the price through a markup (when selling to a customer) or markdown (when buying from a customer).

Example: If you buy 100 shares through your broker-dealer acting as an agent, you pay the market price plus a commission. If the same firm acts as principal and sells you shares from its own inventory, you pay a price that includes the firm's markup, but no separate commission.

- Agent transaction: Commission charged separately; firm does not own the securities

- Principal transaction: Markup/markdown embedded in price; firm owns the securities

- Firms must disclose on the confirmation whether they acted as agent or principal

- A firm cannot charge both a commission and a markup/markdown on the same transaction

When to Use This

- When an exam question describes a transaction and asks how the firm is compensated-look for whether the firm bought or sold from inventory (principal/markup) or facilitated a trade (agent/commission)

- If a confirmation shows both commission and markup, recognize this as a violation

- Choose "agent" when the question emphasizes execution services; choose "principal" when the firm holds inventory or acts as a market maker

Markups and Markdowns

A markup is the amount added to the dealer's cost when selling a security to a customer from inventory. A markdown is the amount subtracted from the market price when the dealer buys a security from a customer for its own inventory.

The FINRA 5% Policy (also called the 5% Markup Policy) serves as a guideline-not a hard rule-for determining whether a markup, markdown, or commission is fair and reasonable. The 5% figure is a guide; actual fairness depends on multiple factors.

- Applies to markups, markdowns, and commissions in non-exempt securities

- Does not apply to mutual funds, new issues, or securities sold by prospectus

- Factors considered: type of security, size of transaction, dollar amount, disclosure, market conditions, nature of the broker-dealer's business, and services provided

- 5% is a starting point; higher or lower percentages may be justified based on circumstances

- Markups and markdowns are calculated from the prevailing market price, not the dealer's acquisition cost

When to Use This

- When a question asks whether a 7% markup is automatically unfair-answer that it depends on the factors above, not a strict 5% cap

- If the exam presents a low-priced, illiquid security with a 10% markup, recognize that higher markups may be reasonable for such securities

- Exclude mutual fund transactions when applying the 5% Policy-they are governed by prospectus rules instead

Spreads

The spread is the difference between the bid price (what a dealer will pay to buy a security) and the ask price (what a dealer will charge to sell the same security). The spread represents the dealer's gross profit on a round-turn transaction.

Example: A dealer quotes a stock at 50.00 bid, 50.10 ask. The spread is \(50.10 - 50.00 = 0.10\) per share. If a customer buys 100 shares at the ask (50.10), the dealer earns \(0.10 \times 100 = 10.00\) in gross revenue.

- Wider spreads typically occur in illiquid or thinly traded securities

- Narrower spreads are common in highly liquid, actively traded stocks

- Market makers are required to quote both bid and ask prices

- The spread compensates the dealer for risk and inventory holding costs

When to Use This

- When a question gives bid and ask prices and asks for the dealer's profit per share, calculate the spread

- If asked why a dealer's spread is wide, associate this with low liquidity or higher risk

- Distinguish spread from markup-spread is between bid and ask; markup is added above the dealer's cost or prevailing market

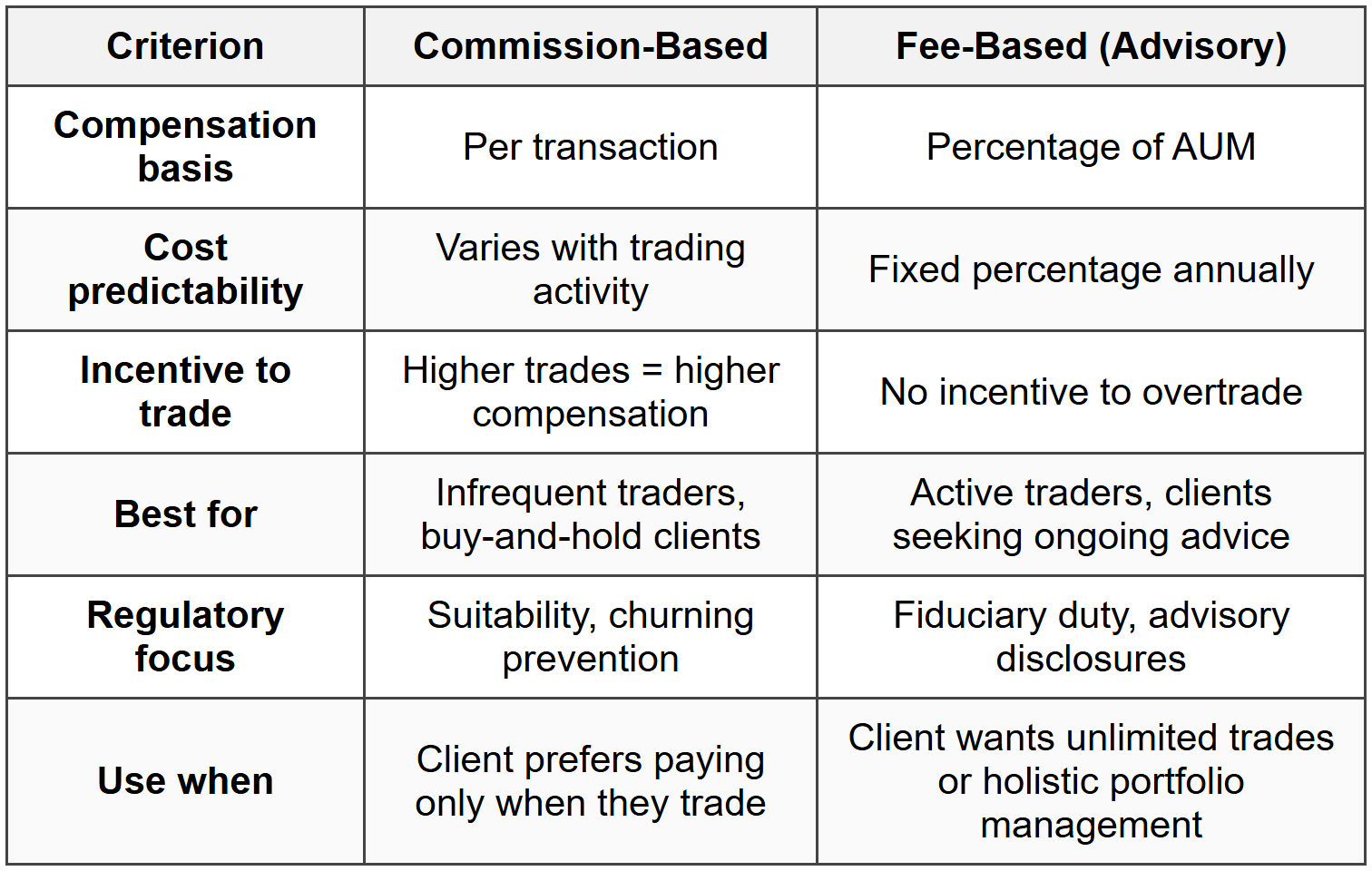

Commission-Based Compensation

Registered representatives (RRs) typically earn commissions based on the volume and type of securities transactions they execute for clients. Commissions vary by product: stocks, bonds, mutual funds, options, and annuities each have different payout structures.

- Commissions are transaction-based-more trades generally mean higher compensation

- Firms may offer tiered payout grids, where higher production earns a higher percentage payout

- RRs cannot share commissions with non-registered individuals

- Commissions must be disclosed on customer confirmations

- Churning-excessive trading to generate commissions-is prohibited

When to Use This

- When a question describes frequent trading in a customer account with no apparent investment objective, identify this as potential churning

- If asked who may receive commission payments, exclude anyone not registered with the firm

- Choose commission-based over fee-based models when the question emphasizes transactional activity rather than ongoing advice

Fee-Based Compensation (Advisory Accounts)

In a fee-based account, the client pays a percentage of assets under management (AUM) rather than commissions per transaction. This model aligns the representative's compensation with the growth of the client's portfolio, not the number of trades.

- Typical fees range from 1% to 2% of AUM annually, billed quarterly

- No commissions charged on individual trades within the account

- Suitable for clients who trade frequently or seek ongoing investment advice

- Registered Investment Advisers (RIAs) commonly use this model

- Fee-based accounts are regulated under the Investment Advisers Act of 1940 if advisory services are provided

When to Use This

- When a question presents a client who trades actively and wants predictable costs, recommend a fee-based account over commission-based

- If asked about compensation alignment with client interests, recognize fee-based models reduce incentive to churn

- Distinguish between fee-based and commission-based when the question asks about regulatory structure-advisory accounts fall under different rules

Sharing in Customer Accounts

Registered representatives are generally prohibited from sharing in profits or losses in a customer's account unless specific conditions are met.

- RR must obtain written authorization from both the customer and the firm

- Sharing must be proportional to the RR's financial contribution to the account

- Exception: If the customer is an immediate family member (spouse, parent, child, sibling, in-law), sharing does not need to be proportional

- Immediate family includes: parents, mother-in-law, father-in-law, husband, wife, children, siblings

When to Use This

- When a question asks if an RR can share profits with a customer, check for written authorization and proportional sharing

- If the customer is the RR's mother, recognize that proportional sharing is not required

- Exclude friends, cousins, or non-immediate family from the exception-these require proportional sharing

Riskless Principal Transactions

A riskless principal transaction occurs when a broker-dealer receives a customer order, immediately buys or sells the security as principal to fill that order, then sells or buys the security to or from the customer at a markup or markdown.

Example: A customer places an order to buy 500 shares of XYZ. The firm simultaneously buys 500 shares in the market as principal and sells them to the customer at a markup. The firm held the securities for only seconds and took minimal risk.

- The firm acts as principal but assumes virtually no market risk

- Markup or markdown is allowed, but the transaction must still comply with the 5% Policy

- The confirmation must show the firm acted as principal

- The firm cannot charge both a markup and a commission

When to Use This

- When a question describes a firm buying securities to fill a specific customer order with no inventory held beforehand, identify this as a riskless principal transaction

- If asked about compensation in such trades, confirm the firm earns a markup/markdown, not a commission

- Recognize that the 5% Policy still applies even though the transaction is riskless

Soft Dollar Arrangements

Soft dollars refer to brokerage commissions paid by investment advisers or broker-dealers in exchange for research, analytical tools, or other services that benefit clients. These arrangements are permitted but must meet strict criteria.

- Services received must provide lawful and appropriate assistance in investment decision-making

- Soft dollars cannot be used for rent, office supplies, travel, or other overhead expenses

- Advisers must disclose soft dollar arrangements to clients

- Commonly used to pay for third-party research, market data, and portfolio analysis tools

When to Use This

- When a question asks if soft dollars can pay for office furniture or computers, recognize these are not permissible uses

- If the exam describes an adviser using commissions to purchase research reports, identify this as an acceptable soft dollar use

- Choose disclosure requirements when asked about adviser obligations in soft dollar arrangements

Commonly Tested Scenarios / Pitfalls

1. Scenario: A customer buys 200 shares of a stock from a broker-dealer's inventory at $52 per share. The prevailing market price is $50. The confirmation shows a $100 commission. Is this permissible?

Correct Approach: No. The firm acted as principal (selling from inventory), so it cannot charge a separate commission. The firm's compensation is the markup embedded in the $52 price. Charging both a markup and a commission on the same transaction violates FINRA rules.

Check first: Determine whether the firm acted as agent or principal. If the firm sold from inventory, it acted as principal and can only charge a markup.

Do NOT do first: Do not assume that because a commission appears on the confirmation, the charge is legitimate. Always verify the capacity in which the firm acted.

Why other options are wrong: Allowing both a markup and commission would result in double compensation, which is prohibited. A markdown applies when buying from a customer, not selling to one. A spread applies to quoted bid-ask differences, not individual transactions.

2. Scenario: An RR wants to share in the profits of a wealthy client's account. The client agrees verbally, and the RR contributes 10% of the account's capital. The firm has not been notified. Is this allowed?

Correct Approach: No. The RR must obtain written authorization from both the customer and the firm. Verbal agreement is insufficient, and the firm must approve the arrangement even if sharing is proportional.

Check first: Confirm that written authorization from both the customer and the firm has been obtained before any sharing occurs.

Do NOT do first: Do not assume verbal agreement suffices. Written documentation is mandatory for account sharing.

Why other options are wrong: Proportional contribution alone does not satisfy the requirement-firm and customer authorization are always required. Immediate family exception applies only to sharing arrangements with family members, not all clients. Oral consent does not meet regulatory standards.

3. Scenario: A dealer quotes a municipal bond at 98 bid, 99 ask. A customer buys the bond from the dealer at 99.50. What is the dealer's compensation?

Correct Approach: The dealer's compensation is the markup of 0.50 points (or $5 per $1,000 bond) above the ask price of 99. The spread (98 to 99) is not the dealer's compensation in this transaction; it's the difference between bid and ask quotes. The markup is the difference between the ask and the price charged to the customer.

Check first: Identify the ask price and the price charged to the customer. The markup is the difference between these two figures.

Do NOT do first: Do not confuse the spread (bid to ask) with the markup. The spread is what the dealer would earn on a round-turn transaction at quoted prices; the markup is what the dealer adds above the ask when selling to a customer.

Why other options are wrong: The bid price is irrelevant when the customer is buying-only the ask and sale price matter. The spread does not directly measure the dealer's compensation on this specific sale. Calculating from the dealer's cost without considering the prevailing ask violates the 5% Policy framework.

4. Scenario: An investment adviser manages $10 million for a client and charges a 1.5% annual fee. The adviser uses $15,000 in soft dollars from brokerage commissions to pay for office rent. Is this permissible?

Correct Approach: No. Soft dollars can only be used for services that assist in investment decision-making, such as research or analytical tools. Office rent is an overhead expense and does not qualify.

Check first: Determine whether the expense directly benefits clients' investment decisions. If it's overhead or personal benefit, it's not a permissible soft dollar use.

Do NOT do first: Do not assume all adviser expenses can be paid with soft dollars. Only research and decision-making tools are allowed.

Why other options are wrong: Payment for rent benefits the firm, not client portfolios. Travel, furniture, and administrative costs are similarly excluded. Only research, data, and analysis tools that aid investment decisions are acceptable soft dollar uses.

5. Scenario: A client trades very infrequently-perhaps once every six months-and wants the lowest cost structure. Should the RR recommend a commission-based or fee-based account?

Correct Approach: Commission-based. The client will pay only when they trade, which is rare. A fee-based account charging 1-2% annually would cost more given the low trading frequency.

Check first: Assess the client's trading frequency and compare the annual fee (percentage of AUM) to expected commission costs.

Do NOT do first: Do not default to recommending fee-based accounts for all clients. Fee-based accounts are cost-effective only for active traders or those needing ongoing advice.

Why other options are wrong: A fee-based account would charge the client annually regardless of trading activity, resulting in higher costs. Wrap accounts and advisory fees are unsuitable for infrequent traders. Commission-based pricing aligns cost with usage.

Step-by-Step Procedures or Methods

Task: Calculating a markup or markdown in a principal transaction

- Identify the prevailing market price (the current bid or ask, depending on the transaction direction).

- Determine the price charged or paid to the customer.

- If the dealer is selling to the customer, subtract the prevailing ask price from the customer's purchase price. This is the markup.

- If the dealer is buying from the customer, subtract the customer's sale price from the prevailing bid price. This is the markdown.

- Calculate the percentage markup or markdown by dividing the dollar difference by the prevailing market price and multiplying by 100.

- Compare the percentage to the 5% guideline and consider factors such as security type, liquidity, and transaction size to determine fairness.

Example:

A dealer's prevailing ask price for a stock is $40. The dealer sells the stock to a customer at $41.

Markup = \(41 - 40 = 1\) dollar per share.

Percentage markup = \(\frac{1}{40} \times 100 = 2.5\%\).

This is within the 5% guideline and likely reasonable, depending on other factors.

Task: Determining whether sharing in a customer account is permissible

- Confirm the RR has obtained written authorization from the customer.

- Confirm the RR has obtained written approval from the employing broker-dealer.

- Check if the customer is an immediate family member (spouse, parent, child, sibling, in-law).

- If the customer is not immediate family, verify that sharing is proportional to the RR's financial contribution.

- If the customer is immediate family, proportional sharing is not required.

- If all conditions are met, sharing is permissible; if any condition is missing, sharing is prohibited.

Practice Questions

Q1: A broker-dealer buys 500 shares of stock from a customer at $48 per share when the current market bid is $50. What is this transaction called, and what is the broker-dealer's compensation?

(a) Agency transaction; commission of $2 per share

(b) Principal transaction; markdown of $2 per share

(c) Principal transaction; markup of $2 per share

(d) Riskless principal transaction; spread of $2 per share

Ans: (b)

The broker-dealer bought from the customer at a price below the market bid, acting as principal. The $2 difference between the market bid ($50) and the customer's sale price ($48) is a markdown. Option (a) is incorrect because commissions apply to agency transactions, not principal transactions. Option (c) is wrong because markups apply when selling to a customer, not buying from one. Option (d) is incorrect because this is not a riskless principal transaction-it's a straightforward purchase from the customer-and spread refers to bid-ask differences, not compensation on a single transaction.

Q2: An RR wishes to share in the profits of a customer's account. The customer is the RR's brother. Which of the following is required?

(a) Written authorization from the customer and the firm; proportional sharing based on the RR's contribution

(b) Written authorization from the customer and the firm; no proportional sharing required

(c) Written authorization from the customer only; proportional sharing based on the RR's contribution

(d) No authorization required for immediate family members

Ans: (b)

When the customer is an immediate family member (including a sibling), written authorization from both the customer and the firm is still required, but proportional sharing is not necessary. Option (a) is incorrect because proportional sharing is not required for immediate family. Option (c) omits firm approval, which is always mandatory. Option (d) is wrong because written authorization from both parties is required even for family members.

Q3: A dealer quotes a corporate bond at 102 bid, 103 ask. A customer sells the bond to the dealer at 101. What is the dealer's compensation?

(a) 1 point markup

(b) 1 point markdown

(c) 1 point spread

(d) 2 point markup

Ans: (b)

The dealer bought the bond from the customer at 101, which is 1 point below the prevailing bid of 102. This is a markdown of 1 point. Option (a) is incorrect because markups apply when selling to a customer. Option (c) is wrong because the spread is the difference between bid and ask (102 to 103), not the dealer's compensation on this transaction. Option (d) incorrectly calculates the markdown and mislabels it as a markup.

Q4: Which of the following is NOT a permissible use of soft dollars by an investment adviser?

(a) Paying for third-party research reports

(b) Subscribing to a financial data service

(c) Purchasing computer hardware for the adviser's office

(d) Obtaining portfolio analysis software

Ans: (c)

Soft dollars must be used for services that assist in investment decision-making. Computer hardware is an overhead expense and does not directly aid investment decisions. Options (a), (b), and (d) are all acceptable soft dollar uses because they provide research, data, or analytical tools that benefit clients' portfolios.

Q5: A client trades actively, executing 30-40 transactions per month. The client's account value is $500,000. Which compensation model is likely most cost-effective for this client?

(a) Commission-based account charging $10 per trade

(b) Fee-based account charging 1.5% of AUM annually

(c) Principal transactions with markups averaging 3%

(d) Riskless principal transactions with commissions

Ans: (b)

With 30-40 trades per month, commission-based costs would range from $3,600 to $4,800 annually ($10 × 30 to 40 trades × 12 months), or potentially higher. A fee-based account at 1.5% of $500,000 = $7,500 annually, but includes unlimited trades and advisory services, making it more cost-effective and aligned with the client's active trading. Option (a) might seem lower cost, but only if commissions are exactly $10 per trade with no other fees; in practice, active traders benefit from fee-based accounts. Option (c) would result in high cumulative costs due to markups on every trade. Option (d) is nonsensical-riskless principal transactions involve markups, not commissions.

Q6: A confirmation shows that a broker-dealer sold 1,000 shares of stock to a customer as principal at $25 per share. The confirmation also lists a $50 commission. What is the issue?

(a) The markup is excessive under the 5% Policy

(b) The firm cannot charge both a markup and a commission on the same transaction

(c) The firm should have acted as agent, not principal

(d) The commission is too low for 1,000 shares

Ans: (b)

When a firm acts as principal, it cannot charge a separate commission; its compensation is embedded in the price as a markup. Charging both violates FINRA rules. Option (a) is incorrect because we don't know the prevailing market price, so we can't determine if the markup is excessive. Option (c) is wrong because firms may act as principal or agent depending on circumstances-neither is inherently incorrect. Option (d) is irrelevant; the real issue is the dual charge.

Quick Review

- Agent transactions: Broker facilitates trades for a commission; firm does not own securities

- Principal transactions: Dealer buys/sells from inventory; compensation is markup (selling) or markdown (buying)

- A firm cannot charge both a commission and a markup/markdown on the same trade

- 5% Policy: Guideline for fair markups, markdowns, and commissions; not a hard cap; factors include security type, size, and liquidity

- Markups and markdowns are calculated from the prevailing market price, not the dealer's cost

- Spread: Difference between bid and ask; represents dealer's gross profit on quoted prices

- Sharing in customer accounts requires written authorization from customer and firm; proportional sharing unless customer is immediate family

- Immediate family for sharing purposes: spouse, parents, children, siblings, in-laws

- Fee-based accounts charge a percentage of AUM annually; best for active traders or clients seeking ongoing advice

- Commission-based accounts charge per transaction; best for infrequent traders

- Soft dollars may only pay for research, data, and analytical tools-not overhead like rent or furniture

- Riskless principal transactions: Firm buys security to fill a customer order, then sells to customer at a markup; minimal risk

- Confirmations must disclose whether the firm acted as agent or principal

- Churning-excessive trading to generate commissions-is prohibited and a red flag in commission-based accounts