Shareholder Rights

Shareholder rights are the legal powers and privileges granted to individuals who own common stock in a corporation. For the FINRA SIE exam, you must know the specific rights that come with equity ownership, how these rights function in practice, and what distinguishes different types of shareholders. This content tests your understanding of corporate governance, voting procedures, and the financial benefits available to stockholders.

Core Concepts

Voting Rights

Common stockholders have the right to vote on major corporate matters. This is the fundamental difference between equity ownership and debt ownership-stockholders participate in corporate governance while bondholders do not.

Stockholders vote on:

- Election of the board of directors-the individuals who oversee management and make strategic decisions

- Approval of major corporate actions-including mergers, acquisitions, stock splits, and amendments to the corporate charter

- Selection of independent auditors-the accounting firm that reviews the company's financial statements

- Approval of stock option plans-compensation programs that grant shares or options to employees

Stockholders typically receive one vote per share owned. If you own 500 shares, you get 500 votes. The voting takes place at the annual meeting or at special meetings called for specific purposes.

When stockholders cannot attend meetings in person, they vote by proxy-a legal document that authorizes someone else to vote on their behalf. Companies mail proxy materials to all shareholders of record before the meeting date.

When to Use This

- When a question asks what rights common stockholders possess versus preferred stockholders or bondholders

- When identifying which corporate decisions require shareholder approval

- When determining how many votes a stockholder controls based on share ownership

- When a scenario describes a shareholder who cannot attend a meeting and needs to exercise their voting power

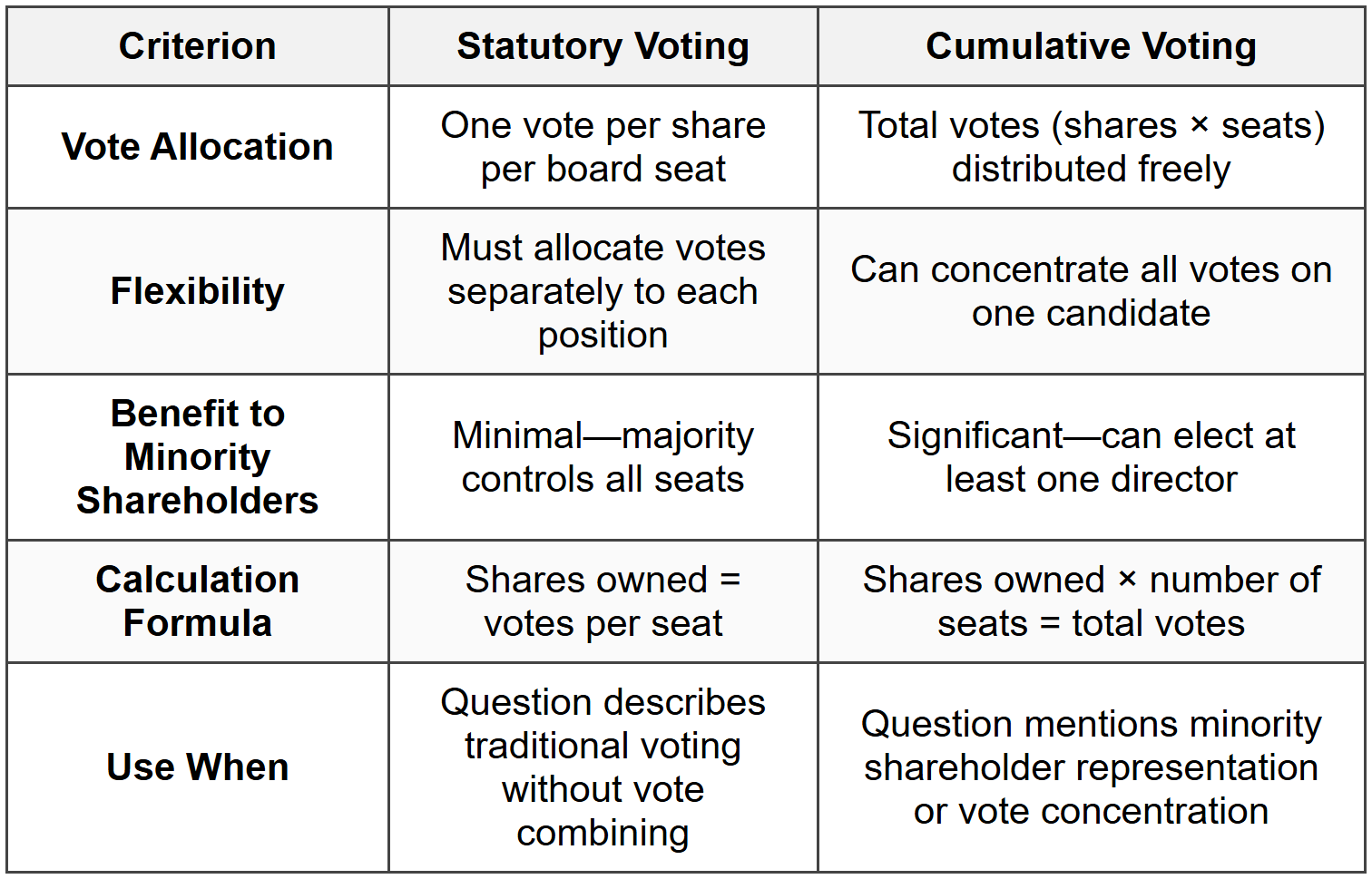

Statutory Voting vs. Cumulative Voting

There are two methods for electing directors, and the SIE exam tests your ability to distinguish them and calculate voting power.

Statutory voting (also called regular voting) means each shareholder can cast one vote per share for each director position. If there are three board seats open and you own 100 shares, you cast 100 votes for the first seat, 100 votes for the second seat, and 100 votes for the third seat-but you cannot combine them.

Cumulative voting allows shareholders to multiply their shares by the number of positions being filled, then distribute all those votes however they choose. With 100 shares and three open seats, you have 300 total votes. You could put all 300 votes on one candidate or split them any way you prefer.

Cumulative voting benefits minority shareholders because they can concentrate their voting power to elect at least one representative to the board. With statutory voting, majority shareholders control every seat.

Calculation example:

You own 200 shares. There are 4 board seats open.

Statutory voting: 200 votes per seat × 4 seats = 800 total votes, but you must allocate 200 to each position

Cumulative voting: 200 shares × 4 positions = 800 total votes that you can distribute freely (e.g., 800 votes for one candidate, or 400 for one and 200 each for two others)

When to Use This

- When a question asks which voting method gives minority shareholders better representation

- When calculating total voting power based on share ownership and number of board seats

- When comparing how different voting methods affect election outcomes

- When determining whether a shareholder can concentrate votes on a single candidate

Preemptive Rights

Preemptive rights give existing shareholders the right to maintain their proportionate ownership when the company issues new shares. If you own 5% of the company, preemptive rights allow you to purchase 5% of any new offering before shares are sold to the public.

Without preemptive rights, new stock issuances dilute existing shareholders' ownership percentage and voting power. If the company issues millions of new shares, your 5% ownership might drop to 3% or less.

Important: Preemptive rights are not automatic. They must be explicitly granted in the corporate charter. Many modern corporations do not include preemptive rights.

Example:

You own 1,000 shares of a company with 100,000 shares outstanding (1% ownership).

The company plans to issue 50,000 new shares.

With preemptive rights: You can purchase 500 shares (1% of the new issue) to maintain your 1% stake.

Without preemptive rights: Your ownership drops to approximately 0.67% (1,000 ÷ 150,000).

When to Use This

- When a question asks how existing shareholders can prevent ownership dilution

- When identifying which right protects proportionate ownership in new offerings

- When determining whether a shareholder can automatically purchase new shares before the public

- When comparing rights that all shareholders possess versus rights that must be granted in the charter

Right to Transfer Ownership

Common stockholders have the right to freely transfer ownership by selling, gifting, or bequeathing their shares. This is called negotiability-shares can be traded without restriction (unless otherwise specified in a shareholders' agreement or for restricted securities).

This right distinguishes publicly traded securities from private investments. You can sell your shares of a public company on an exchange without needing company approval. The company maintains a transfer agent who handles the administrative process of updating ownership records.

When to Use This

- When a question asks what makes common stock a liquid investment

- When identifying characteristics that distinguish equity ownership from partnership interests

- When determining what rights shareholders have without company permission

Right to Inspect Corporate Books and Records

Shareholders have the right to inspect certain corporate records, including:

- Financial statements and annual reports

- Minutes from shareholder meetings

- List of shareholders (the stock ledger)

- Corporate bylaws and charter documents

This right is limited and must be exercised for proper purposes. Shareholders cannot demand proprietary business information or trade secrets. The purpose typically must relate to evaluating their investment or exercising their voting rights.

The company must provide:

- Quarterly and annual financial reports

- Proxy materials before shareholder meetings

- Notice of dividend declarations

- Information about material corporate events

When to Use This

- When a question asks what information shareholders can legally access

- When distinguishing between public disclosure documents and proprietary information

- When identifying shareholder rights that relate to monitoring company performance

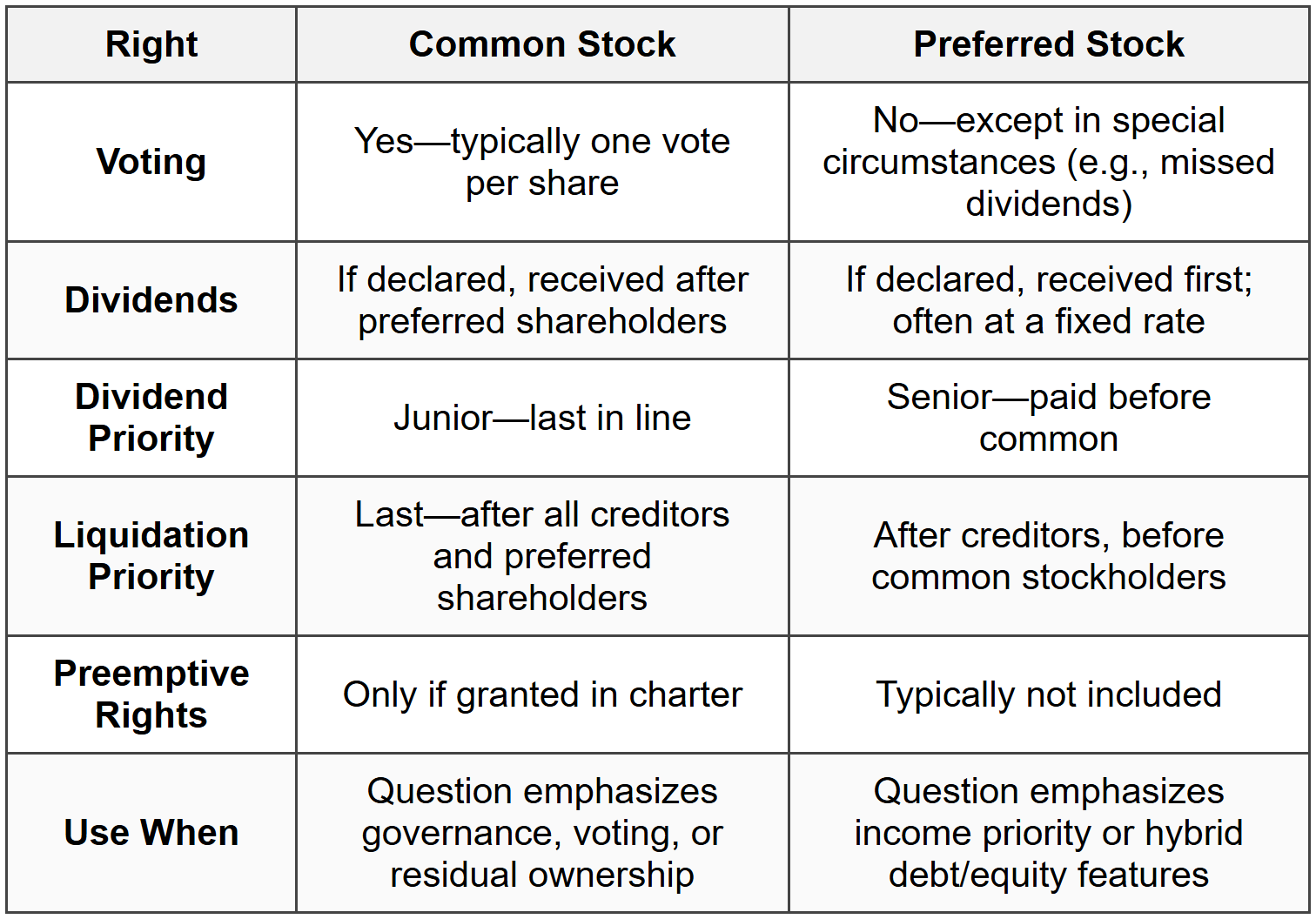

Right to Receive Dividends (If Declared)

Common stockholders have the right to receive dividends if and when declared by the board of directors. This is not a guaranteed right-the board has full discretion over whether to pay dividends, how much to pay, and when to pay them.

Key point: Common stockholders receive dividends after preferred stockholders. Preferred stock has priority in dividend payments.

Dividends are typically paid in cash, but companies can also distribute stock dividends (additional shares) or property dividends (other assets).

Important dates:

- Declaration date-the board announces the dividend and sets the record date

- Ex-dividend date-the first day the stock trades without the dividend; set by the exchange at one business day before the record date

- Record date-shareholders on the company's books as of this date receive the dividend

- Payment date-the company distributes the dividend

To receive the dividend, you must own the stock before the ex-dividend date. If you buy on or after the ex-dividend date, you do not receive the upcoming dividend-the seller keeps it.

When to Use This

- When a question asks whether common stockholders have a guaranteed right to dividends

- When determining which shareholder class gets paid first when dividends are declared

- When identifying what date determines dividend eligibility

- When comparing common stock dividend rights to preferred stock dividend rights

Residual Claim in Liquidation

Common stockholders have a residual claim on corporate assets if the company liquidates. This means they are paid last-after all creditors, bondholders, and preferred stockholders receive their claims.

Liquidation priority (highest to lowest):

- Secured creditors (e.g., mortgage holders, collateralized lenders)

- Unsecured creditors (e.g., bondholders, suppliers, employees)

- Preferred stockholders

- Common stockholders

In most bankruptcies, common stockholders receive nothing because senior claims exhaust the company's assets. This is why common stock is considered the riskiest form of corporate investment in terms of liquidation.

When to Use This

- When a question asks who gets paid last in a corporate liquidation

- When comparing common stockholders' claims to bondholders' or preferred stockholders' claims

- When identifying why common stock is riskier than bonds or preferred stock

- When determining what common stockholders receive if a company goes bankrupt

Limited Liability

Shareholders have limited liability-they can only lose the amount they invested. If the company goes bankrupt or faces lawsuits, shareholders are not personally liable for corporate debts or legal judgments.

This distinguishes corporate ownership from sole proprietorships or general partnerships, where owners have unlimited personal liability.

Example:

You purchase 100 shares of XYZ Corp at $50 per share ($5,000 total investment).

XYZ Corp loses a $10 million lawsuit.

Your maximum loss: $5,000 (your investment in the stock).

You cannot be sued for any portion of the $10 million judgment.

When to Use This

- When a question asks what shareholders can lose if a company fails

- When comparing corporate equity ownership to partnership or sole proprietorship structures

- When determining whether shareholders have personal liability for corporate actions

Commonly Tested Scenarios / Pitfalls

1. Scenario: A question asks whether common stockholders have a guaranteed right to receive dividends.

Correct Approach: State that common stockholders have the right to receive dividends if and when declared by the board of directors, but there is no guarantee. The board has full discretion over dividend policy.

Check first: Whether the question asks about common stock or preferred stock. Preferred stockholders have priority in dividend payments, but even they do not have an absolute guarantee unless they own cumulative preferred stock and dividends are in arrears.

Do NOT do first: Assume that owning stock automatically entitles you to dividends. This is a fundamental misunderstanding-dividend declarations are discretionary corporate actions, not contractual obligations.

Why other options are wrong: Any answer suggesting that dividends are mandatory or that shareholders can force the board to declare dividends is incorrect. Only the board of directors can declare dividends, and they may choose to retain earnings for reinvestment.

2. Scenario: A question presents a shareholder who owns 500 shares and asks how many votes they have in an election with four board seats open. The company uses cumulative voting.

Correct Approach: Multiply the number of shares by the number of board seats: 500 shares × 4 seats = 2,000 total votes. The shareholder can distribute these 2,000 votes freely across the four candidates.

Check first: Whether the voting method is statutory or cumulative. The calculation differs dramatically. With statutory voting, the shareholder would have 500 votes per seat but could not combine them.

Do NOT do first: Calculate 500 votes per seat without checking the voting method. This leads to the wrong answer if the question specifies cumulative voting, because you would miss the multiplication step.

Why other options are wrong: Options that give 500 votes total or 500 votes per seat without allowing combination reflect statutory voting rules. Options that ignore the number of board seats or multiply incorrectly misunderstand the cumulative voting formula.

3. Scenario: A question asks which type of shareholder has the best chance to elect a representative to the board: a minority shareholder in a company with statutory voting or a minority shareholder in a company with cumulative voting.

Correct Approach: Choose cumulative voting. Minority shareholders can concentrate all their votes on one candidate, increasing the likelihood of electing at least one board member. With statutory voting, the majority shareholders control every seat.

Check first: Whether the question is asking about minority or majority shareholders. Cumulative voting benefits minority shareholders specifically, while majority shareholders maintain control under either method.

Do NOT do first: Assume that all voting methods treat shareholders equally. The exam tests your understanding that cumulative voting is designed to give minority shareholders representation, which is impossible under statutory voting when the majority holds significantly more shares.

Why other options are wrong: Options favoring statutory voting ignore the mathematical reality that minority shareholders cannot win any seats when votes must be allocated separately to each position. Options suggesting that voting method does not matter miss the purpose of cumulative voting systems.

4. Scenario: A question asks what happens to a shareholder's percentage ownership when the company issues new shares and the shareholder does not purchase any of the new offering. The company does not have preemptive rights.

Correct Approach: State that the shareholder's percentage ownership decreases (is diluted) because the total number of outstanding shares increases while their share count remains the same. Without preemptive rights, they have no right to purchase new shares before the public offering.

Check first: Whether the company has preemptive rights in its charter. If preemptive rights exist, the shareholder would have the opportunity to maintain their proportionate ownership by purchasing new shares. Without them, dilution is automatic.

Do NOT do first: Assume that shareholders automatically receive new shares or can automatically prevent dilution. Dilution occurs unless the shareholder participates in the offering, and without preemptive rights, they have no priority access to new shares.

Why other options are wrong: Options stating that ownership percentage stays the same ignore basic math-if the denominator (total shares outstanding) increases and the numerator (shares owned) does not, the fraction decreases. Options suggesting the shareholder must be compensated or consulted misunderstand corporate authority to issue shares.

5. Scenario: A question asks which investor gets paid first if a company liquidates: a common stockholder, a preferred stockholder, a bondholder, or a general creditor.

Correct Approach: Choose the bondholder or general creditor (both are creditors and rank ahead of equity holders). Among creditors, secured creditors are first, then unsecured creditors. Preferred stockholders come before common stockholders, but both equity classes are paid after all creditors.

Check first: Whether the question distinguishes between secured and unsecured creditors or simply asks about creditors versus stockholders. The key concept is that creditors always rank ahead of stockholders in liquidation.

Do NOT do first: Choose any equity class (common or preferred stock) before checking if creditors are listed. Creditors are senior to all stockholders in liquidation priority, regardless of stock class.

Why other options are wrong: Options placing common or preferred stockholders ahead of bondholders or creditors reverse the liquidation priority structure. Equity holders have residual claims, meaning they are paid only after all debt obligations are satisfied. In most bankruptcies, equity holders receive nothing.

Step-by-Step Procedures or Methods

Task: Calculate total voting power under cumulative voting

- Identify the number of shares the investor owns

- Identify the number of board positions being filled in the election

- Multiply shares owned by the number of board positions: \(\text{Total votes} = \text{Shares owned} \times \text{Number of board seats}\)

- Recognize that the investor can distribute all votes freely-they can place all votes on one candidate or split them across multiple candidates

- If calculating votes needed to guarantee one board seat, use the formula: \(\text{Votes needed} = \frac{\text{Total shares outstanding} \times \text{Number of seats}}{(\text{Number of seats} + 1)} + 1\)

Example:

An investor owns 1,000 shares. There are 3 board seats open and 50,000 shares outstanding total.

Step 1: Shares owned = 1,000

Step 2: Board seats = 3

Step 3: Total votes = 1,000 × 3 = 3,000 votes

Step 4: The investor can allocate all 3,000 votes to one candidate or split them (e.g., 1,500 to one, 1,000 to another, 500 to a third)

Step 5 (bonus): To guarantee one seat:

\(\text{Votes needed} = \frac{50{,}000 \times 3}{3 + 1} + 1 = \frac{150{,}000}{4} + 1 = 37{,}500 + 1 = 37{,}501\) votes

The investor has 3,000 votes, which is not enough to guarantee a seat but could elect a director if votes are split among many candidates.

Task: Determine dividend eligibility based on purchase date

- Identify the record date-the date the company checks its books to see who owns the stock

- Determine the ex-dividend date-one business day before the record date (set by the exchange)

- If the investor purchases shares before the ex-dividend date, they receive the dividend

- If the investor purchases shares on or after the ex-dividend date, the seller receives the dividend (the stock trades "ex-dividend")

- Remember regular way settlement is T+2 (trade date plus two business days), but the ex-dividend date determines eligibility, not the settlement date

Example:

Record date: Friday, June 10

Ex-dividend date: Thursday, June 9 (one business day before record date)

Scenario A: Investor buys shares on Wednesday, June 8 → Receives dividend (purchased before ex-dividend date)

Scenario B: Investor buys shares on Thursday, June 9 → Does NOT receive dividend (purchased on ex-dividend date)

Scenario C: Investor buys shares on Friday, June 10 → Does NOT receive dividend (purchased after ex-dividend date)

Practice Questions

Q1: A company with 100,000 shares outstanding is electing 5 directors. An investor owns 2,000 shares. If the company uses cumulative voting, how many total votes does this investor control?

(a) 2,000 votes

(b) 5,000 votes

(c) 10,000 votes

(d) 400 votes

Ans: (c)

Under cumulative voting, multiply shares owned by the number of board seats: 2,000 shares × 5 seats = 10,000 total votes. The investor can distribute these votes freely across the five candidates. Option (a) reflects statutory voting where the investor would have 2,000 votes per seat but could not combine them. Option (b) incorrectly adds shares and seats. Option (d) divides instead of multiplies.

Q2: Which of the following rights is NOT automatic for common stockholders?

(a) Right to vote for the board of directors

(b) Right to receive dividends when declared

(c) Right to maintain proportionate ownership in new offerings

(d) Right to transfer shares freely

Ans: (c)

Preemptive rights-the right to maintain proportionate ownership when new shares are issued-must be explicitly granted in the corporate charter and are not automatic. Options (a), (b), and (d) are standard rights that come with common stock ownership without requiring special charter provisions. Note that (b) is the right to receive dividends if declared, not a guarantee of dividends.

Q3: An investor buys common stock on the ex-dividend date. The record date is the next business day. Who receives the dividend?

(a) The buyer, because they own the stock on the record date

(b) The seller, because the stock trades without the dividend on the ex-dividend date

(c) Both parties split the dividend equally

(d) Neither party receives the dividend

Ans: (b)

On the ex-dividend date, the stock begins trading without the dividend. Anyone who purchases on or after the ex-dividend date does not receive the upcoming dividend-it belongs to the seller. Option (a) is wrong because ownership on the record date does not determine eligibility; the ex-dividend date does. Options (c) and (d) are incorrect because the dividend is paid in full to one party (the seller), not split or forfeited.

Q4: In a corporate liquidation, which of the following has the lowest priority claim on assets?

(a) Preferred stockholders

(b) General creditors

(c) Common stockholders

(d) Secured bondholders

Ans: (c)

Common stockholders have a residual claim, meaning they are paid last after all creditors and preferred stockholders. The liquidation priority is: secured creditors first (d), then unsecured creditors/general creditors (b), then preferred stockholders (a), and finally common stockholders (c). In most bankruptcies, common stockholders receive nothing because senior claims exhaust available assets.

Q5: Which voting method provides the greatest benefit to minority shareholders seeking board representation?

(a) Statutory voting

(b) Cumulative voting

(c) Proxy voting

(d) Discretionary voting

Ans: (b)

Cumulative voting allows shareholders to multiply shares by the number of board seats and then concentrate all votes on one or a few candidates, giving minority shareholders the best chance to elect at least one director. Statutory voting (a) requires votes to be allocated separately to each position, allowing majority shareholders to control all seats. Proxy voting (c) is simply the mechanism for voting when you cannot attend meetings and does not favor minority or majority shareholders. Discretionary voting (d) is not a recognized method for board elections.

Q6: A shareholder owns 500 shares out of 100,000 shares outstanding (0.5% ownership). The company issues 50,000 new shares. The company does NOT have preemptive rights in its charter. What happens to the shareholder's percentage ownership if they do not purchase any new shares?

(a) Ownership increases to 0.75%

(b) Ownership remains at 0.5%

(c) Ownership decreases to approximately 0.33%

(d) Ownership decreases to 0%

Ans: (c)

The shareholder now owns 500 shares out of 150,000 total outstanding shares (100,000 original + 50,000 new). \(\frac{500}{150{,}000} = 0.00333 = 0.33\%\). This is dilution-the shareholder's proportionate ownership decreases because total shares outstanding increased while their share count stayed the same. Without preemptive rights, they had no priority access to purchase new shares. Option (a) incorrectly suggests ownership increases. Option (b) ignores the dilutive effect of new shares. Option (d) is extreme-the shareholder still owns shares, just a smaller percentage of the total.

Quick Review

- Common stockholders have voting rights-typically one vote per share for board elections and major corporate actions

- Cumulative voting = shares × board seats = total votes distributed freely; benefits minority shareholders

- Statutory voting = one vote per share per seat, allocated separately; majority controls all seats

- Preemptive rights allow shareholders to maintain proportionate ownership in new offerings; must be granted in charter, not automatic

- Shareholders can receive dividends if declared by the board, but dividends are not guaranteed

- To receive a dividend, you must own shares before the ex-dividend date (one business day before record date)

- Common stockholders are paid last in liquidation-after secured creditors, unsecured creditors, and preferred stockholders

- Limited liability means shareholders can only lose their investment amount; they are not personally liable for corporate debts

- Shareholders have the right to inspect corporate books and records for proper purposes (e.g., financial statements, shareholder lists)

- Common stockholders have residual claims-they receive what is left after all senior claims are satisfied, which is often nothing in bankruptcy