Risks and Benefits of ETFs

ETFs (Exchange-Traded Funds) are pooled investment vehicles that combine features of mutual funds and stocks, traded on exchanges throughout the day at market prices. The FINRA SIE Exam tests your understanding of the specific advantages ETFs offer investors, the unique risks they present, and how they compare to mutual funds and other investment products.

Core Concepts

What ETFs Are and How They Trade

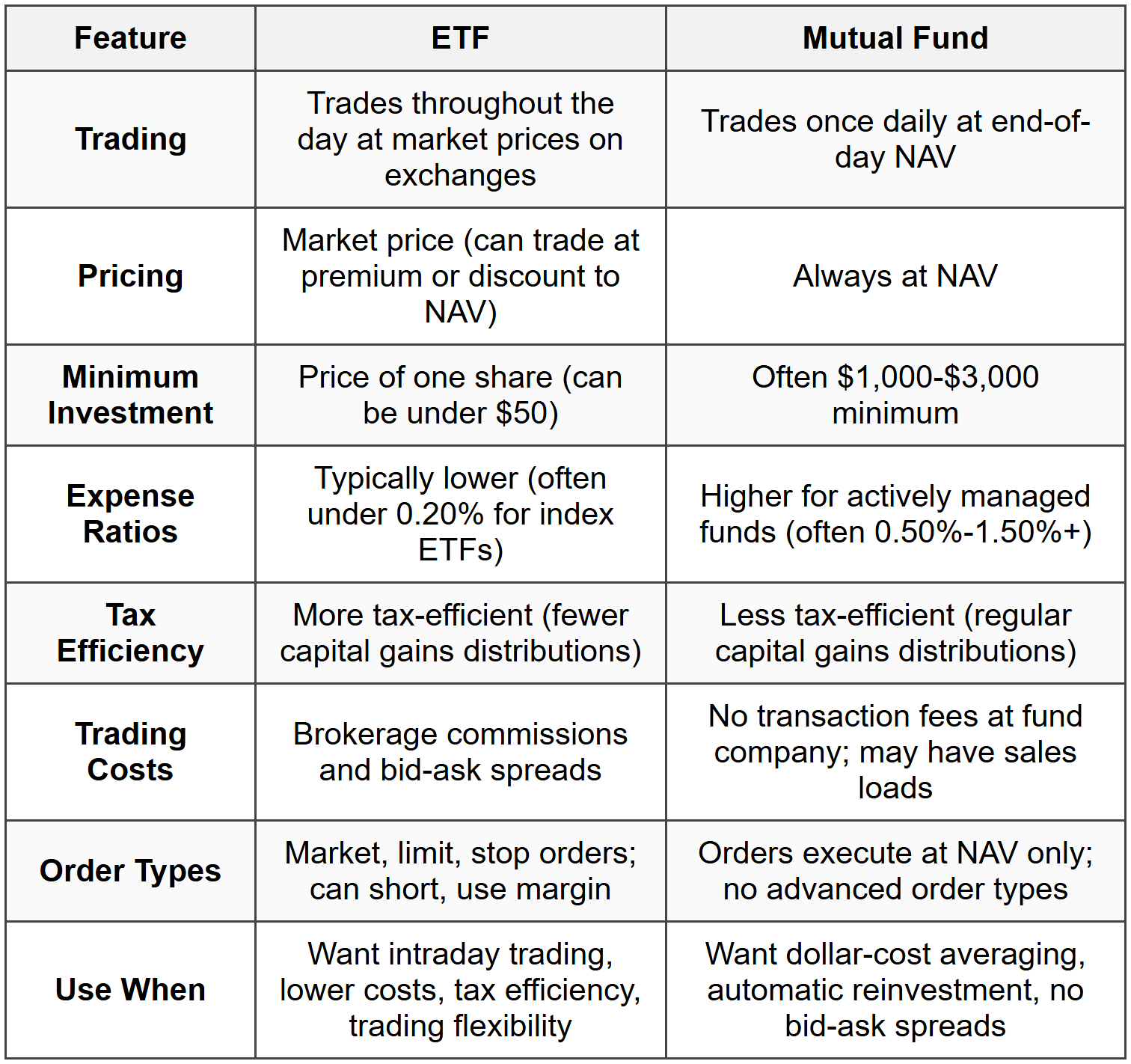

An ETF is an investment company that holds a portfolio of securities (stocks, bonds, commodities, or other assets) and issues shares that trade on exchanges like individual stocks. Unlike mutual funds that price once daily at NAV, ETFs trade continuously during market hours at prices determined by supply and demand. The market price of an ETF may differ slightly from its NAV (Net Asset Value), creating either a premium (trading above NAV) or discount (trading below NAV).

ETFs use an authorized participant (AP) mechanism where large institutional investors can create or redeem shares directly with the fund in large blocks called creation units (typically 50,000 shares). This process helps keep the market price close to NAV through arbitrage.

When to Use This

- When the exam asks how ETF pricing differs from mutual fund pricing-remember ETFs trade at market prices throughout the day, not once at NAV

- When comparing liquidity between investment products-ETFs provide intraday liquidity like stocks

- When asked about the mechanism that keeps ETF prices near NAV-the creation/redemption process with authorized participants

- When distinguishing between price and value-market price vs. NAV can differ in ETFs

Key Benefits of ETFs

Intraday Trading: Investors can buy and sell ETF shares at any time during market hours at current market prices. This provides flexibility that mutual funds cannot offer, as mutual funds only execute trades at the end-of-day NAV.

Lower Expense Ratios: ETFs typically have lower annual expense ratios than actively managed mutual funds because most ETFs are passively managed (tracking an index). Lower expenses mean more of the investment returns stay with the investor.

Tax Efficiency: ETFs generally generate fewer capital gains distributions than mutual funds due to their unique structure. The in-kind creation and redemption process allows ETFs to remove low-cost-basis securities from the fund without triggering taxable events. When an AP redeems shares, the ETF can deliver securities in-kind rather than selling them, avoiding capital gains taxes that would otherwise be passed to shareholders.

Transparency: Most ETFs disclose their holdings daily, allowing investors to see exactly what securities the fund owns at any time. This contrasts with mutual funds, which typically disclose holdings quarterly.

Diversification: A single ETF share provides exposure to dozens, hundreds, or even thousands of securities, spreading risk across multiple investments. For example, an S&P 500 ETF gives exposure to 500 large-cap U.S. stocks with one transaction.

No Minimum Investment: Unlike many mutual funds that require minimum initial investments (often $1,000 to $3,000), investors can purchase ETFs for the cost of a single share plus commission (which may be zero at many brokers).

Trading Flexibility: Because ETFs trade like stocks, investors can use various trading strategies including limit orders, stop orders, short selling, buying on margin, and options strategies (if options are available on that ETF).

When to Use This

- When comparing costs between investment products-ETFs typically have lower expense ratios than actively managed mutual funds

- When tax efficiency is the focus-ETFs generate fewer capital gains distributions due to in-kind transactions

- When asked about trading flexibility-ETFs allow limit orders, stop orders, margin purchases, and short selling

- When distinguishing disclosure practices-ETFs show holdings daily; mutual funds quarterly

Key Risks of ETFs

Market Risk: ETF share prices fluctuate with the underlying securities. If the stocks, bonds, or other assets in the ETF decline in value, the ETF's value declines. This is the fundamental risk of all equity and fixed-income investments.

Trading at Premium or Discount: While the creation/redemption mechanism generally keeps ETF market prices close to NAV, during periods of market stress or for less liquid ETFs, the market price can diverge significantly from NAV. Investors buying at a premium pay more than the underlying securities are worth; those selling at a discount receive less.

Liquidity Risk: While popular ETFs (like those tracking the S&P 500) have high trading volume and tight bid-ask spreads, specialized or sector-specific ETFs may have lower volume. Lower liquidity means wider bid-ask spreads, increasing transaction costs. The liquidity of an ETF depends both on its own trading volume and the liquidity of its underlying holdings.

Tracking Error: ETFs that follow an index may not perfectly replicate the index's performance due to management fees, transaction costs, or sampling strategies. The difference between the ETF's return and the index's return is tracking error. Even index ETFs rarely match their benchmarks exactly.

Leveraged and Inverse ETF Risk: Some ETFs use derivatives to amplify returns (leveraged ETFs seeking 2× or 3× daily returns) or profit from declines (inverse ETFs). These products reset daily, causing compounding effects that make them unsuitable for holding periods longer than one day. Over multiple days, returns can diverge dramatically from the underlying index due to volatility decay.

Sector and Concentration Risk: ETFs focusing on specific sectors, industries, or geographic regions lack diversification across the broader market. A sector ETF (like technology or energy) can experience greater volatility than a broad-market ETF.

Trading Costs: Unlike no-transaction-fee mutual funds, buying or selling ETFs typically involves brokerage commissions (though many brokers now offer commission-free ETF trading). The bid-ask spread also represents a cost-the difference between what you pay to buy and what you receive when selling.

Closing Risk: ETFs can close if they don't attract sufficient assets or investor interest. While shareholders receive the NAV value of their investment, this forced liquidation may trigger unexpected capital gains taxes and disrupt investment plans.

When to Use This

- When asked about risks unique to ETFs-premium/discount trading and bid-ask spread costs distinguish ETFs from mutual funds

- When leveraged or inverse ETFs appear-flag them as suitable only for single-day trading due to daily reset and compounding effects

- When tracking error is mentioned-it's the difference between ETF performance and the index it follows

- When comparing liquidity-ETF liquidity depends on both share trading volume and underlying security liquidity

ETF vs. Mutual Fund Comparison

When to Use This Comparison

- When the exam presents a scenario where an investor wants intraday trading-choose ETF

- When tax efficiency is a priority and the investor is in a taxable account-ETF is better

- When the investor wants to invest a specific dollar amount regularly-mutual funds accommodate fractional shares more easily

- When asked about pricing certainty-mutual funds always trade at NAV, removing premium/discount risk

Leveraged and Inverse ETFs

Leveraged ETFs use derivatives (futures, swaps, options) to amplify the daily return of an underlying index. A 2× leveraged ETF seeks to deliver twice the daily return of its benchmark; a 3× leveraged ETF seeks triple the daily return. These are daily reset products, meaning the leverage applies only to each single day's performance.

Inverse ETFs profit when the underlying index declines. A standard inverse ETF seeks to deliver the opposite of the index's daily return (if the index drops 1%, the ETF rises 1%). Leveraged inverse ETFs combine both features, seeking to deliver a multiple of the opposite daily return (a -2× ETF seeks twice the inverse return).

Critical Risk-Compounding and Volatility Decay: Because these ETFs reset daily, holding them for more than one day exposes investors to compounding effects. In volatile markets, even if the underlying index ends a multi-day period unchanged, the leveraged or inverse ETF will likely lose value due to the mathematical impact of daily rebalancing. For example:

Day 1: Index up 5%, 2× ETF up 10%

Day 2: Index down 5%, 2× ETF down 10%

Index: 100 → 105 → 99.75 (down 0.25%)

2× ETF: 100 → 110 → 99 (down 1%)

The index lost only 0.25% over two days, but the 2× ETF lost 1% due to compounding. This effect worsens with higher volatility and longer holding periods.

When to Use This

- When the exam asks about holding periods for leveraged or inverse ETFs-suitable only for single-day trading

- When volatility decay or compounding effects appear-these explain why leveraged ETFs diverge from expected returns over time

- When identifying appropriate investors-these products suit only sophisticated traders with daily monitoring capability, not buy-and-hold investors

- When asked about suitability-leveraged and inverse ETFs are generally unsuitable for retail investors with long-term goals

Costs Associated with ETFs

Expense Ratio: The annual fee charged by the ETF, expressed as a percentage of assets. This is deducted from the fund's returns and covers management fees, administrative costs, and other operational expenses.

Bid-Ask Spread: The difference between the highest price a buyer will pay (bid) and the lowest price a seller will accept (ask). This represents an implicit transaction cost every time you trade. Highly liquid ETFs have tight spreads (pennies), while less liquid ETFs may have spreads of several cents or more.

Brokerage Commissions: Some brokers charge a commission to buy or sell ETFs, though many now offer commission-free trading on select or all ETFs. This cost is incurred with each transaction.

Premium/Discount: When an ETF trades above NAV, buyers pay a premium; when it trades below NAV, sellers receive a discount. This is a cost or benefit depending on transaction timing and market conditions.

When to Use This

- When comparing total costs-consider expense ratio, bid-ask spread, and commissions together

- When asked what makes one ETF more expensive to trade than another despite similar expense ratios-wider bid-ask spreads increase trading costs

- When identifying costs that don't appear in expense ratios-bid-ask spreads and premiums/discounts are implicit costs

Commonly Tested Scenarios / Pitfalls

1. Scenario: An investor wants to know why an ETF that tracks the S&P 500 index has returned 9.8% this year while the S&P 500 index itself returned 10.0%. The exam asks what explains this difference.

Correct Approach: The difference is tracking error caused by the ETF's expense ratio and transaction costs. Even passively managed index ETFs cannot perfectly replicate their benchmark due to these costs.

Check first: Look at the expense ratio-this is the most common cause of tracking error. A 0.20% expense ratio means the ETF will underperform the index by approximately that amount annually.

Do NOT do first: Don't assume the ETF is poorly managed or buying the wrong securities. Index ETFs use algorithms to track their benchmarks closely; small tracking error is expected and normal.

Why other options are wrong: Market volatility affects both the index and the ETF equally, so it doesn't explain the difference. The premium/discount to NAV affects the purchase/sale price but not the calculated return over time.

2. Scenario: A client purchased shares of a 2× leveraged ETF tracking the technology sector one month ago, expecting to hold it for several months. The technology index is up 5% over the month, but the client's ETF is only up 8%. The client expected 10% (2× the 5% gain) and asks what went wrong.

Correct Approach: Leveraged ETFs reset daily, so multi-day holding periods create compounding effects that cause returns to diverge from the simple multiple of the index return. These products are designed only for single-day trading, not multi-week or multi-month holding.

Check first: Identify that this is a leveraged ETF (2×, 3×, or inverse) and determine the holding period. If longer than one day, compounding effects explain the unexpected return.

Do NOT do first: Don't calculate expected returns by simply multiplying the index return by the leverage factor over multi-day periods. This ignores daily reset and compounding, which are the defining characteristics of these products.

Why other options are wrong: This isn't a tracking error issue (which is minor for leveraged ETFs), nor is it about expense ratios (which don't explain an 8% vs. 10% difference). The premium/discount to NAV also doesn't explain performance divergence over a holding period.

3. Scenario: An investor wants maximum tax efficiency in a taxable account and is choosing between an actively managed mutual fund and an index-tracking ETF, both investing in large-cap U.S. stocks. Both have similar long-term performance. Which is more tax-efficient and why?

Correct Approach: The ETF is more tax-efficient because its structure allows in-kind creation and redemption, which avoids triggering capital gains distributions that would be taxable to shareholders. Mutual funds must sell securities to meet redemptions, often generating capital gains passed to all shareholders.

Check first: Confirm the account is taxable (not an IRA or 401(k)), because tax efficiency only matters in taxable accounts. In retirement accounts, both are equally tax-efficient since gains aren't taxed until withdrawal.

Do NOT do first: Don't focus on expense ratios or performance when the question asks specifically about tax efficiency. These are separate considerations.

Why other options are wrong: Lower expense ratios improve after-tax returns but aren't the same as tax efficiency. The ETF's intraday trading doesn't affect tax efficiency; it's the creation/redemption mechanism that matters.

4. Scenario: A client places a market order to buy shares of a thinly traded sector ETF at 2:00 PM when the market is open. The ETF's NAV is $50.00, but the client's order executes at $50.40. The client asks why they paid more than the ETF is worth.

Correct Approach: The client paid the market price, which can differ from NAV due to supply and demand. The ETF was trading at a premium of $0.40 (0.8%) above NAV. Additionally, because this is a thinly traded ETF, the bid-ask spread was likely wide, and the market order executed at the ask price (the higher price sellers demand).

Check first: Identify whether the ETF is highly liquid or thinly traded. Thinly traded ETFs have wider bid-ask spreads and are more prone to trading at premiums or discounts to NAV.

Do NOT do first: Don't assume an error occurred or that the client was overcharged illegally. Trading at premiums and discounts is a normal feature of ETFs, especially those with lower liquidity.

Why other options are wrong: This isn't about expense ratios (which don't affect the purchase price) or tracking error (which is about performance, not trade execution price). The creation/redemption process helps minimize but doesn't eliminate premiums/discounts, especially in real-time trading.

5. Scenario: An investor wants to make regular monthly investments of $500 into a broad market index. The exam asks whether an ETF or mutual fund is more suitable for this strategy.

Correct Approach: A no-load mutual fund is more suitable because it allows fractional share purchases, meaning the entire $500 can be invested each month. ETFs require whole share purchases, so unless the ETF price divides evenly into $500, there will be uninvested cash each month.

Check first: Identify that this is a regular, fixed-dollar investment strategy (dollar-cost averaging). Mutual funds accommodate this better than ETFs due to fractional shares.

Do NOT do first: Don't immediately choose the ETF based on lower expense ratios or tax efficiency. While these are ETF advantages, they don't outweigh the operational difficulty of whole-share-only purchases for systematic fixed-dollar investing.

Why other options are wrong: Intraday trading isn't relevant for a long-term monthly investment plan. Tax efficiency matters but is secondary to the practical issue of deploying the full $500 each month. Brokerage commissions (even if zero) don't address the fractional share problem.

Step-by-Step Procedures or Methods

Task: Determining whether an ETF or mutual fund is more appropriate for a specific investor scenario

- Identify the investor's primary need: Is it intraday trading, tax efficiency, low costs, regular fixed-dollar investing, or advanced trading strategies?

- Check the account type: If it's a retirement account (IRA, 401(k)), tax efficiency doesn't matter-focus on costs and trading needs.

- Determine investment frequency and amount: Regular fixed-dollar amounts favor mutual funds (fractional shares); lump sums or flexible amounts favor ETFs (lower costs).

- Assess trading strategy: If the investor wants to use limit orders, stop orders, short selling, or margin, only ETFs work.

- Evaluate liquidity needs: If the investor needs to enter/exit positions during the day or wants price certainty at specific times, choose ETFs.

- Compare total costs: Add expense ratio + bid-ask spread + commissions for ETFs; compare to mutual fund expense ratio + any sales loads.

- Consider tax situation: For taxable accounts with long holding periods, ETFs typically generate fewer capital gains distributions.

- Review any specific product risks: If it's a leveraged, inverse, sector-specific, or international ETF, ensure the investor understands and can tolerate those risks.

Task: Calculating the effective cost of trading an ETF

- Identify the bid price (what you receive if selling) and ask price (what you pay if buying).

- Calculate the bid-ask spread: Ask price - Bid price.

- Express the spread as a percentage: \(\frac{\text{Bid-Ask Spread}}{\text{Midpoint Price}} \times 100\)

- Add any brokerage commission per trade (may be $0 for commission-free ETFs).

- Check if the ETF is trading at a premium or discount to NAV: Market price - NAV.

- Sum all costs: Spread cost + Commission + Premium (if buying) or Discount (if selling).

- Annualize for comparison: If you plan to trade frequently, multiply by expected number of trades per year.

Practice Questions

Q1: An investor holds a 3× leveraged ETF that tracks the Nasdaq 100 index. Over the past month, the Nasdaq 100 is up 6%, but the investor's ETF is only up 15% instead of the expected 18% (3 × 6%). What best explains this discrepancy?

(a) The ETF has a high expense ratio that reduced returns

(b) The ETF experienced tracking error due to the fund manager's security selection

(c) Daily rebalancing and compounding effects caused returns to diverge from the simple multiple of the index return

(d) The ETF was trading at a discount to NAV when the investor purchased it

Ans: (c)

Leveraged ETFs reset daily, meaning the leverage applies only to each single day's return. Over multi-day periods, compounding effects (especially in volatile markets) cause returns to diverge from the simple arithmetic multiple of the index return. (a) is incorrect because expense ratios are typically small and don't explain a 3% difference. (b) is incorrect because leveraged ETFs are passively managed and use derivatives to track the index, not active security selection. (d) is incorrect because premiums/discounts affect purchase price, not the calculated return over a holding period.

Q2: Which of the following is the primary reason ETFs are generally more tax-efficient than mutual funds?

(a) ETFs have lower expense ratios, reducing taxable income

(b) ETFs use an in-kind creation and redemption process that avoids triggering capital gains

(c) ETFs trade on exchanges, allowing investors to control the timing of capital gains

(d) ETFs are only available in retirement accounts where taxes are deferred

Ans: (b)

The in-kind creation and redemption mechanism allows ETFs to transfer securities to authorized participants without selling them, avoiding capital gains that would otherwise be distributed to shareholders. (a) is incorrect because expense ratios affect returns, not tax efficiency. (c) is incorrect; while investors control when they sell, this doesn't explain why ETFs generate fewer distributions than mutual funds. (d) is factually wrong-ETFs are available in both taxable and retirement accounts.

Q3: An investor wants to invest $1,000 per month in a broad market index. The investor's primary goal is long-term growth in a taxable account. Which of the following is the most significant advantage a no-load mutual fund offers over an ETF for this specific situation?

(a) Mutual funds have lower expense ratios than ETFs

(b) Mutual funds allow fractional share purchases, ensuring the full $1,000 is invested each month

(c) Mutual funds provide better diversification than ETFs

(d) Mutual funds generate fewer capital gains distributions than ETFs

Ans: (b)

Mutual funds allow fractional shares, so the entire $1,000 investment is deployed each month. ETFs require whole share purchases, so unless the share price divides evenly into $1,000, there will be uninvested cash. (a) is incorrect-ETFs typically have lower expense ratios. (c) is incorrect; both can provide similar diversification if tracking the same index. (d) is incorrect; ETFs are generally more tax-efficient, not less.

Q4: A thinly traded ETF has a bid price of $48.50 and an ask price of $49.00. The ETF's NAV is $48.75. An investor places a market order to buy 100 shares. What is the most likely outcome?

(a) The order executes at $48.75, the NAV

(b) The order executes at $48.50, the bid price

(c) The order executes at $49.00, the ask price

(d) The order is rejected because the ETF is trading above its NAV

Ans: (c)

A market buy order executes at the ask price, which is the lowest price at which sellers are willing to sell ($49.00). (a) is incorrect because ETFs trade at market prices, not NAV. (b) is incorrect because the bid is the price for sellers, not buyers. (d) is incorrect; trading above NAV (at a premium) is normal and doesn't prevent order execution.

Q5: Which of the following statements about leveraged and inverse ETFs is correct?

(a) They are suitable for long-term buy-and-hold investors seeking enhanced returns

(b) They reset quarterly, so returns should be evaluated over 90-day periods

(c) They are designed for single-day trading and are generally unsuitable for holding longer than one day

(d) They eliminate market risk by hedging the underlying index exposure

Ans: (c)

Leveraged and inverse ETFs reset daily, meaning their performance objectives apply only to single-day periods. Compounding effects over longer periods cause returns to diverge significantly from expectations, making them unsuitable for multi-day holding. (a) is incorrect; these products are inappropriate for long-term holding. (b) is incorrect; they reset daily, not quarterly. (d) is incorrect; they amplify or inverse market risk but don't eliminate it.

Q6: An investor is comparing two ETFs that track the same index. ETF A has an expense ratio of 0.10% and a typical bid-ask spread of $0.02. ETF B has an expense ratio of 0.05% and a typical bid-ask spread of $0.15. Both ETFs have a share price around $100. If the investor plans to buy and hold for 10 years with no interim trading, which factor should be weighted most heavily?

(a) The bid-ask spread, because it represents a recurring annual cost

(b) The expense ratio, because it is charged annually over the entire holding period

(c) The bid-ask spread, because it will compound over 10 years

(d) Both factors equally, because they both impact long-term returns

Ans: (b)

For a buy-and-hold investor, the expense ratio is charged every year over the 10-year holding period, compounding its impact on returns. The bid-ask spread is a one-time cost paid at purchase (and again at sale), so it's less significant over a long holding period. ETF A's slightly higher expense ratio (0.10% vs. 0.05%, or 0.05% difference = 5 basis points annually for 10 years) costs more than the one-time wider spread of ETF B. (a) is incorrect because bid-ask spreads are not recurring costs. (c) is incorrect; spreads don't compound-they're incurred only during transactions. (d) is incorrect because the annual expense ratio has much greater impact over a 10-year hold than a one-time spread.

Quick Review

- ETFs trade continuously during market hours at market prices; mutual funds trade once daily at NAV

- ETF market prices can differ from NAV, creating premiums (above NAV) or discounts (below NAV)

- Authorized participants create and redeem ETF shares in large blocks (creation units), keeping prices near NAV through arbitrage

- In-kind creation/redemption makes ETFs more tax-efficient than mutual funds by avoiding capital gains distributions

- Leveraged and inverse ETFs reset daily and are suitable only for single-day trading due to compounding effects

- Tracking error is the difference between ETF performance and its benchmark, caused by expense ratios and transaction costs

- Bid-ask spread is an implicit cost of trading ETFs; wider spreads mean higher transaction costs

- ETFs require whole share purchases; mutual funds allow fractional shares, making them better for regular fixed-dollar investing

- ETFs allow advanced trading strategies like limit orders, stop orders, short selling, and margin purchases

- Total ETF costs include expense ratio + bid-ask spread + brokerage commissions