Cheat Sheet: Yield Concepts

Understanding yield concepts is crucial for evaluating fixed-income securities and making informed investment decisions. Yield measures the return an investor receives from a bond or debt instrument. Different yield calculations serve different purposes and provide varying perspectives on investment returns. This cheat sheet consolidates the essential yield formulas, their applications, and key distinctions necessary for mastering bond analysis.

1. Current Yield (CY)

1.1 Definition and Formula

- Current Yield: Measures the annual interest income relative to the bond's current market price. It ignores capital gains/losses and time to maturity.

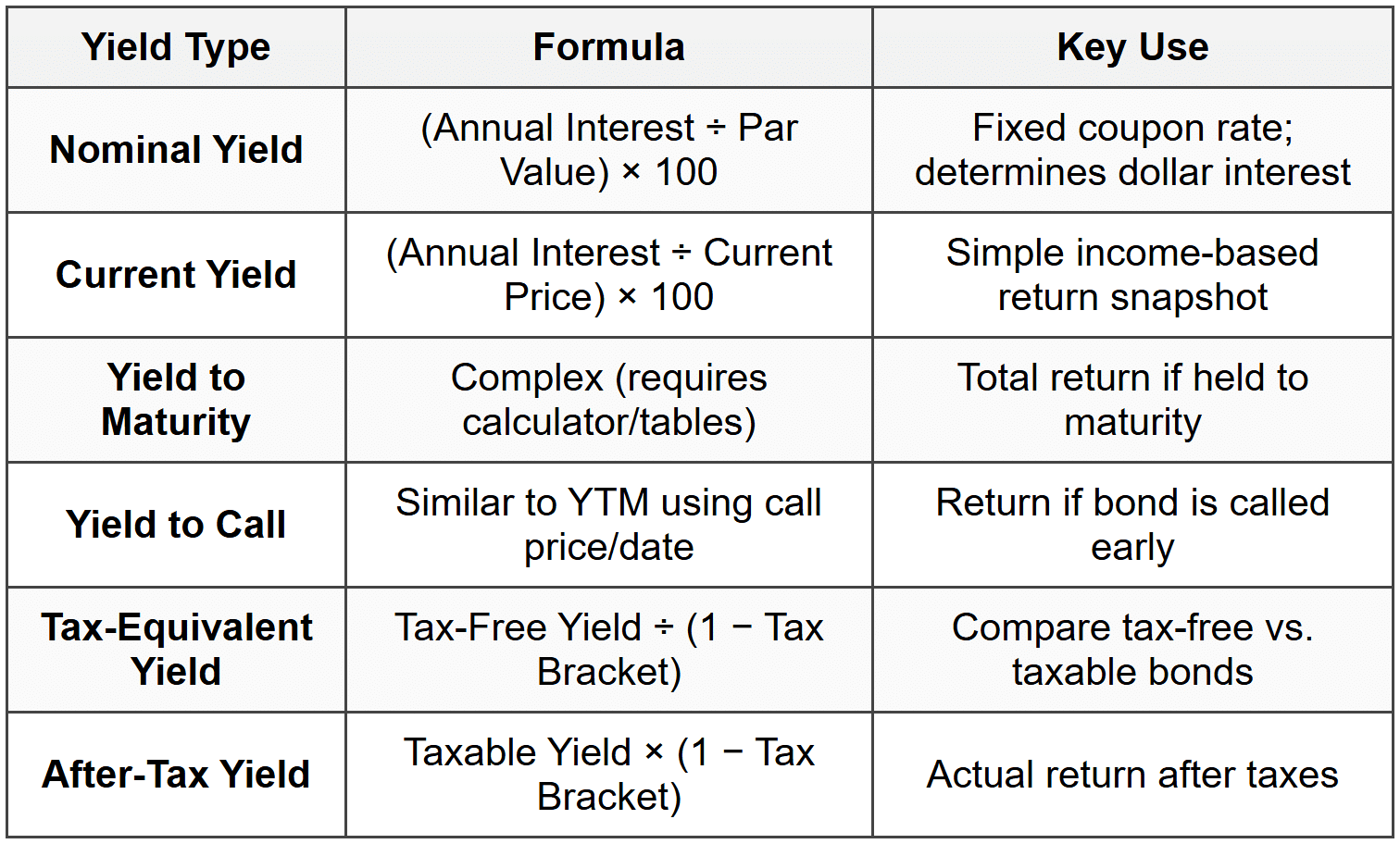

- Formula: Current Yield = (Annual Interest Payment ÷ Current Market Price) × 100

- Annual Interest Payment: Coupon Rate × Par Value (usually $1,000)

- Current Market Price: The price at which the bond is currently trading in the market

1.2 Key Characteristics

- Does not account for capital appreciation or depreciation at maturity

- Does not consider reinvestment of interest payments

- Most useful for comparing bonds with similar maturities and credit quality

- Always falls between Nominal Yield and Yield to Maturity for premium and discount bonds

1.3 Trap Alert

Common Mistake: Students often confuse Current Yield with Yield to Maturity. Remember: Current Yield is a simple snapshot calculation that only considers annual income and current price. It does NOT factor in what happens at maturity.

2. Nominal Yield (Coupon Rate)

2.1 Definition and Formula

- Nominal Yield: The stated annual interest rate on a bond's face value. Also called the Coupon Rate.

- Formula: Nominal Yield = (Annual Interest Payment ÷ Par Value) × 100

- Par Value: The face value of the bond, typically $1,000

- This rate is fixed at issuance and never changes throughout the bond's life

2.2 Key Characteristics

- Always calculated based on par value ($1,000), regardless of market price

- Determines the actual dollar amount of interest paid annually

- Does not reflect the investor's actual return if purchased at a premium or discount

- Lowest yield measure for bonds trading at a premium (above par)

- Highest yield measure for bonds trading at a discount (below par)

3. Yield to Maturity (YTM)

3.1 Definition and Formula

- Yield to Maturity: The total return anticipated on a bond if held until maturity. It considers all interest payments plus any capital gain or loss.

- Most comprehensive yield measure for bonds

- Assumption: All coupon payments are reinvested at the same YTM rate

- Calculation is complex and typically requires a financial calculator or bond table

3.2 Key Characteristics

- Accounts for annual interest income, time to maturity, and difference between purchase price and par value

- Represents the internal rate of return (IRR) of the bond investment

- For bonds purchased at a discount: YTM > Current Yield > Nominal Yield

- For bonds purchased at a premium: YTM < current="" yield="">< nominal="">

- For bonds purchased at par: YTM = Current Yield = Nominal Yield

3.3 Relationship with Price

- Inverse Relationship: When market interest rates rise, bond prices fall, causing YTM to increase

- When market interest rates fall, bond prices rise, causing YTM to decrease

- The longer the maturity, the more sensitive the bond price is to interest rate changes

4. Yield to Call (YTC)

4.1 Definition and Formula

- Yield to Call: The yield calculation assuming the bond is called (redeemed early) by the issuer at the first call date

- Relevant only for callable bonds, which give issuers the right to redeem before maturity

- Uses the call price instead of par value and call date instead of maturity date

- Calculation method is similar to YTM but with adjusted parameters

4.2 Key Characteristics

- Important for premium bonds, as issuers are more likely to call bonds when interest rates fall

- Typically lower than YTM for premium bonds because the investor receives the call price (often close to par) sooner

- Yield to Worst (YTW): The lowest yield among YTM and all possible YTC scenarios; conservative measure for callable bonds

4.3 Trap Alert

Common Mistake: Assuming YTC is always lower than YTM. For discount bonds, YTC can be higher than YTM if the call price exceeds the purchase price significantly. Always compare both yields for callable bonds.

5. Comparative Analysis: Yield Hierarchy

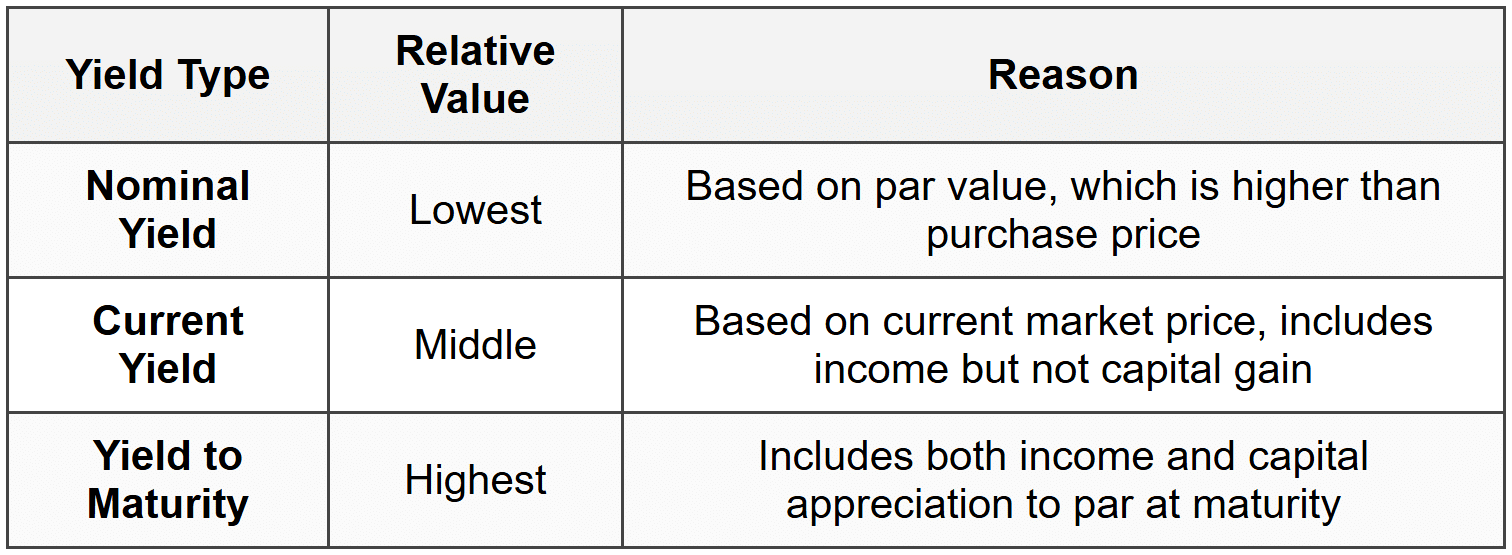

5.1 Bond Trading at a Discount (Below Par)

Hierarchy: Nominal Yield < current="" yield="">< yield="" to="">

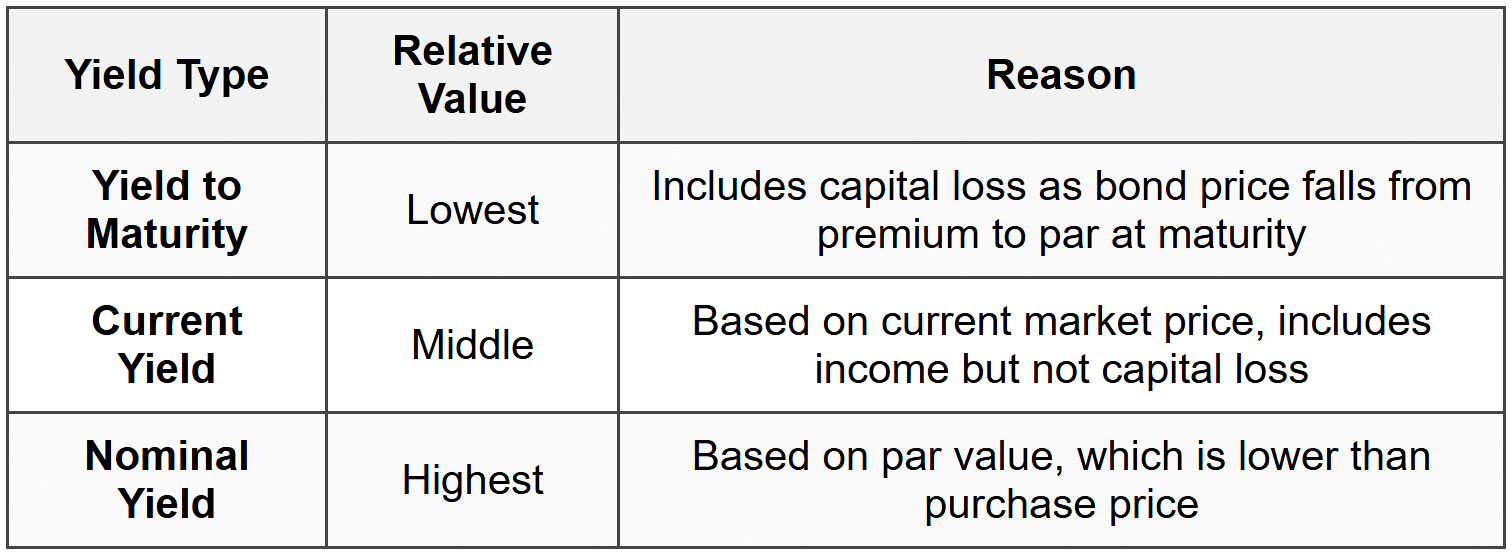

5.2 Bond Trading at a Premium (Above Par)

Hierarchy: Yield to Maturity < current="" yield="">< nominal="">

5.3 Bond Trading at Par

- All three yields are equal: Nominal Yield = Current Yield = Yield to Maturity

- No capital gain or loss at maturity since purchase price equals redemption value

6. Tax-Equivalent Yield (TEY)

6.1 Definition and Formula

- Tax-Equivalent Yield: The yield a taxable bond must offer to equal the after-tax yield of a tax-exempt bond (e.g., municipal bond)

- Formula: Tax-Equivalent Yield = Tax-Free Yield ÷ (1 - Tax Bracket)

- Tax-Free Yield: The stated yield on a municipal or tax-exempt bond

- Tax Bracket: The investor's marginal federal income tax rate (expressed as a decimal)

6.2 Key Characteristics

- Used to compare municipal bonds (tax-exempt) with corporate or Treasury bonds (taxable)

- Higher tax brackets benefit more from tax-exempt bonds

- Helps investors determine whether a tax-free bond is more advantageous than a taxable alternative

6.3 Example Calculation

If a municipal bond yields 3% and an investor is in the 25% tax bracket:

- Tax-Equivalent Yield = 3% ÷ (1 - 0.25) = 3% ÷ 0.75 = 4%

- A taxable bond must yield at least 4% to provide the same after-tax return as the 3% municipal bond

7. After-Tax Yield

7.1 Definition and Formula

- After-Tax Yield: The actual yield an investor retains after paying taxes on interest income from a taxable bond

- Formula: After-Tax Yield = Taxable Yield × (1 - Tax Bracket)

- Taxable Yield: The stated yield on a corporate, Treasury, or other taxable bond

- Tax Bracket: The investor's marginal federal income tax rate (expressed as a decimal)

7.2 Key Characteristics

- Inverse of Tax-Equivalent Yield; converts taxable yield to its after-tax equivalent

- Allows direct comparison with tax-exempt bond yields

- Important for evaluating the true return on taxable fixed-income investments

7.3 Example Calculation

If a corporate bond yields 5% and an investor is in the 30% tax bracket:

- After-Tax Yield = 5% × (1 - 0.30) = 5% × 0.70 = 3.5%

- The investor effectively earns 3.5% after paying federal income taxes

8. Yield Spread

8.1 Definition

- Yield Spread: The difference in yield between two bonds, typically used to compare risk levels

- Expressed in basis points (1 basis point = 0.01%)

- Common comparisons: Corporate bond yield vs. Treasury bond yield of similar maturity

8.2 Key Characteristics

- Credit Spread: Difference in yield due to differences in credit quality (default risk)

- Wider spreads indicate higher perceived risk or lower credit quality

- Used by investors to assess additional compensation for taking on credit risk

- Spreads widen during economic uncertainty and narrow during stable periods

9. Key Formulas Summary

10. Important Relationships and Concepts

10.1 Price-Yield Inverse Relationship

- Bond prices and yields move in opposite directions

- When interest rates rise → bond prices fall → yields increase

- When interest rates fall → bond prices rise → yields decrease

10.2 Reinvestment Assumption

- YTM assumes all coupon payments are reinvested at the same YTM rate

- Reinvestment Risk: The risk that future cash flows cannot be reinvested at the same rate

- Higher for bonds with higher coupon rates and longer maturities

10.3 Basis Points

- Basis Point (bp): 1/100th of 1%, or 0.01%

- 100 basis points = 1%

- Used to describe small changes in yields or interest rates

- Example: A yield increase from 3.5% to 3.75% is a 25 basis point increase

11. Trap Alerts and Common Mistakes

11.1 Confusing Yield Types

- Trap: Using Current Yield when YTM is needed for total return analysis

- Remember: Current Yield ignores capital gains/losses; YTM includes them

11.2 Tax Calculations

- Trap: Multiplying tax-free yield by tax bracket instead of dividing by (1 - Tax Bracket)

- Correct Formula: TEY = Tax-Free Yield ÷ (1 - Tax Bracket), NOT × Tax Bracket

11.3 Premium vs. Discount Yield Hierarchy

- Trap: Reversing the yield hierarchy for premium and discount bonds

- Remember: For discounts: NY < cy="">< ytm;="" for="" premiums:="" ytm="">< cy=""><>

11.4 Callable Bond Yields

- Trap: Ignoring call features when evaluating premium bonds

- Remember: Always consider YTC for callable bonds trading at a premium, as call risk is significant

Mastering these yield concepts enables accurate bond valuation, effective comparison of fixed-income securities, and informed investment decision-making. Understanding the distinctions between yield types, their appropriate applications, and their interrelationships is essential for success in securities analysis and portfolio management. Always verify which yield measure is most relevant for the specific investment scenario and investor objectives.