NCERT Solutions - Nature and Purpose of Business

Short Answer Questions

Q1: Why is business considered an economic activity?Ans: Businesses are economic activities because:

- Resource allocation: Businesses combine and use scarce resources - land, labour, capital and enterprise - to produce goods and services that satisfy people's needs, thereby allocating resources in the economy.

- Profit motive: The aim to earn profit motivates efficiency, innovation and risk-taking, which in turn promote production, employment and overall economic growth.

Q2: How does business contribute to the economic development of a country?

Ans: Businesses grow economies by:

- Jobs and Income: Businesses generate employment, providing individuals with income, thereby boosting consumption and economic growth.

- Goods and Services: They produce goods and services, improving living standards.

- Innovation: Businesses foster advancements and introduce new technologies, enhancing productivity and development.

Q3: State the different types of economic activities.

Ans: Economic activities are activities undertaken to earn a living. Examples include working in factories, practising medicine, managing offices, and teaching in schools. These activities are classified into three categories:

- Business - regular activities involving the production, purchase or sale of goods and services with the objective of earning profit.

- Profession - occupations requiring specialised knowledge and qualifications, for example, doctors, lawyers and chartered accountants, who work for fees.

- Employment - working under an employer for a salary or wages, where the employee performs specified duties.

Q4: State the meaning of business.

Ans: The term "business" derives from being "busy." Business refers to a regular occupation that involves the production, purchase or sale of goods and services with the objective of earning money. It includes manufacturing, buying for resale and providing services to meet consumer needs.

Q5: How would you classify business activities?

Ans: Business activities can be classified into:

- Economic activities: Activities undertaken to earn a living, for example, business, profession and employment; these are motivated by monetary reward.

- Non-economic activities: Activities done for personal satisfaction, social service or emotional reasons without the intention of earning money, for example, household chores, voluntary work and acts of charity.

Q6: What are the various types of industries?

Ans: Industries are categorised as:

- Primary industries: These involve the extraction and reproduction of natural resources, for example, farming, fishing, forestry and mining.

- Secondary industries: These use raw materials to manufacture goods for consumers or for further processing, for example, textile factories, steel plants and construction work.

- Tertiary industries: These provide services that support production and consumption, for example, transport, banking, insurance and advertising.

Q7: Explain any two business activities which auxiliaries to trade are.

Ans: The following are two business activities that are related to trade:

1. Transport and Communication: Production of goods is often region-specific. For instance:

- Tea is primarily produced in Assam.

- Cotton is grown in Gujarat and Maharashtra.

- Jute is cultivated in West Bengal and Odisha.

- Sugar is produced in Uttar Pradesh, Bihar, and Maharashtra.

However, these goods are required for consumption across the country. Transportation systems, such as roads, railways and coastal shipping, remove geographical barriers by moving raw materials to manufacturing centres and finished products to consumers. Effective communication systems - for example postal services, telephones and digital channels - enable producers, traders and buyers to exchange information quickly. Together, transport and communication are essential auxiliaries that make trade possible and efficient.

2. Banking and Finance: Financial resources are critical for business operations, including acquiring assets, purchasing raw materials, and covering operational expenses. Banks provide funds to businesses through facilities such as overdrafts, cash credit, loans, and advances, enabling businesses to overcome financial constraints.

Additionally, banks handle:

- Collection of cheques.

- Payment transfers to various locations.

- Bill discounting for traders.

In international trade, commercial banks assist exporters in collecting payments from importers. They also help promoters raise funds from the public, making banking and finance indispensable for supporting trade activities.

Q8: What is the role of profit in business?

Ans: A business's foundation is its objective, which defines the goals it aims to achieve. While it is widely believed that businesses exist solely for profit, this is not entirely true. Profit, which is the surplus of revenue over cost, is a critical objective but not the only one. Businesses strive to earn more than they invest, and profit plays a vital role for several reasons:

- Source of Revenue for Entrepreneurs: Profit provides income to entrepreneurs, rewarding their efforts and investments.

- Funding for Expansion: It serves as a financial resource to support the growth and diversification of a business.

- Indicator of Smooth Operations: A profitable business reflects efficient management and operational success.

- Validation of Utility: Profit signals society's approval of the business's goods or services, affirming its relevance and value.

- Reputation Building: Sustained profitability enhances a company's credibility and builds its reputation in the market. Although profit cannot be the sole purpose, its importance for sustainability and growth cannot be underestimated.

Q9: What is meant by business risk?

Ans: Business risk refers to the probability of reduced profits or losses due to unforeseen events. For instance:

- Changes in consumer preferences may lower product demand.

- Scarcity of raw materials can increase costs and reduce profit margins.

Risks are classified as:

- Speculative Risks: Arise from market conditions and can result in profit or loss (e.g., price changes, competition).

- Pure Risks: Only lead to loss or no loss (e.g., fire, theft, strikes).

Q10: State the causes of risks involved in business?

Ans: Business risks arise from internal and external factors:

Internal Causes:

- Poor management decisions

- Inefficient operations

- Lack of innovation

- Financial mismanagement

External Causes:

- Economic recessions

- Regulatory changes

- Raw material price fluctuations

- Consumer preference shifts

- Competitive advancements in technology

- Natural disasters and unforeseen events

Long Answer Questions

Q1: Discuss the development of the indigenous banking system in the Indian subcontinent.Ans: In ancient India, trade and commerce played a pivotal role in establishing the country as an economic powerhouse. The establishment of commercial hubs like Harappa and Mohenjodaro during the third millennium B.C. marked the beginning of organised economic activities. Trade relations with Mesopotamia facilitated the exchange of goods such as gold, silver, copper, gemstones, beads, pearls, terracotta pots, and seashells. Metals gradually became a medium of exchange due to their durability and divisibility, fostering economic growth.

The introduction of metallic money further enhanced economic activities by serving as a convenient exchange medium. Instruments like Hundi and Chitti were used for monetary transactions, enabling the transfer of money between parties. The Hundi, a widely recognized financial instrument in the subcontinent, was a contractual document that:

- Guaranteed unconditional payment of money.

- Facilitated monetary commitments or orders.

As banking practices evolved, individuals began depositing precious metals with lenders, known as Seths, who acted as early bankers. This system transformed money into a tool for increasing production, simplifying business operations through credit facilities, loans, and advances. The indigenous banking system supported a favorable trade balance by providing capital to manufacturers, traders, and merchants. Agricultural banks offered short- and long-term loans to farmers, while commercial and industrial banks emerged to support trade and commerce.

Q2: Define business. Describe its important characteristics.

Ans: The term "business" originates from the concept of being "busy." In essence, business refers to any occupation involving activities such as the production, purchase, or sale of goods and services with the intent to earn profit. The scope of activities includes manufacturing, purchasing for resale, and service provision to fulfill consumer needs.

Key characteristics of business:

Production or procurement of goods and services: A business must produce or acquire goods and services before offering them for sale; goods may be consumer items (such as sugar or notebooks) or capital goods (such as machinery).

Sale or exchange of goods and services: Business involves exchanging goods or services for money; personal consumption is not business unless it is undertaken for sale.

Regular dealings: Business implies continuity of transactions; occasional sales (for example, selling an old personal radio) do not amount to business.

Profit earning: Earning profit is a principal objective, necessary for the survival and growth of the enterprise.

Uncertainty of return: Business income is not guaranteed and can fluctuate despite effort and planning.

Element of risk: Business faces risks from competition, market changes and unforeseen events such as accidents or theft.

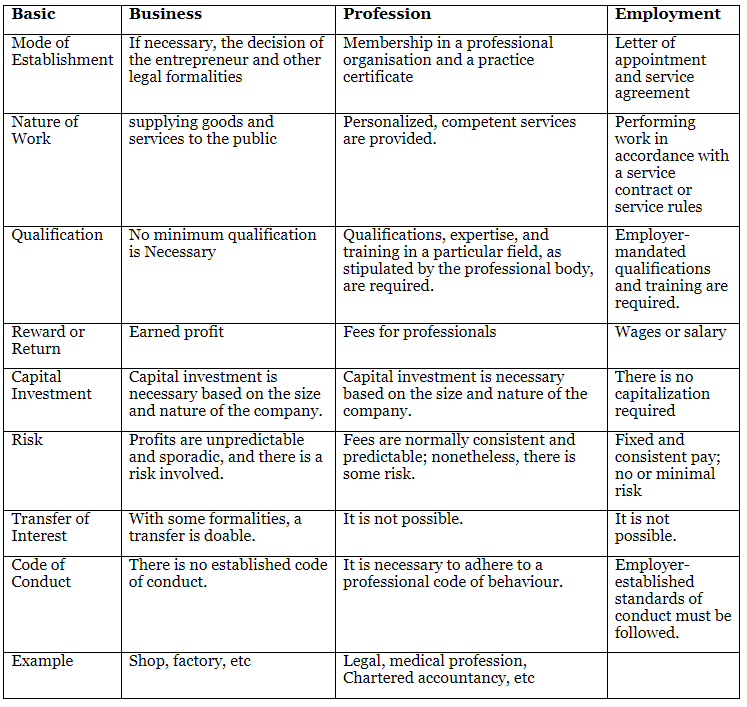

Q3: Compare business with profession and employment.

Ans: The comparison between business, profession, and employment is summarised below:

Q4: Define Industry. Explain various types of industries, giving examples.

Ans: Industry refers to economic activities that transform raw materials into finished products or that reproduce living organisms for human use. It includes manufacturing, processing and related operations. Industries are categorised as follows:

1. Primary industries:

These involve the extraction and production of natural resources or the reproduction of living organisms. Examples include farming, fishing, mining and forestry.

- Extractive industries: mining, fishing and farming.

- Genetic industries: breeding of plants and animals, for example, poultry farms and seed nurseries.

2. Secondary industries:

These use primary inputs to produce finished goods for consumers or for further processing.

- Manufacturing industries: for example, textile mills and automobile plants.

- Construction industries: building roads, bridges and dams.

3. Tertiary industries: These provide services and support to primary and secondary industries, such as transportation, banking, insurance and advertising.

Q5: Describe the activities relating to commerce.

Ans:

Trade is a key part of commerce. It involves selling, transferring, or exchanging goods and services. It helps to deliver products made by producers to customers and users.

Trade can be split into two types:

- Internal trade: buying and selling within the borders of a country.

- External trade: exchange of goods and services between businesses or individuals in different countries.

Auxiliaries to trade: Auxiliaries to trade are activities that support trade and help overcome the difficulties of making and distributing goods. They are essential for smooth commercial operations.

Here are some key auxiliaries to trade:

- Transport and communication: Transport moves raw materials and finished goods; communication connects producers, traders and consumers.

- Banking and finance: Provide funds and payment services required for production and trade, such as loans, bill discounting and remittances.

- Insurance: Protects businesses against losses from fire, theft, accidents and other risks.

- Warehousing: Stores goods until they are required, preventing loss and ensuring supply continuity.

- Advertising: Informs potential buyers about products, their features and prices and helps stimulate demand.

Q6: Explain any five objectives of business.

Ans: The following are important objectives of business:

Market position: To secure and strengthen a favourable position relative to competitors by offering reliable products and services that meet customer needs.

Innovation: To introduce new products, services or processes - both product/service innovation and supply-chain innovation - so as to remain competitive and improve efficiency.

- Product or Service innovation

- Supply Chain innovation

Innovation is essential for survival in a competitive market.

- Productivity: To make best use of resources and increase output per unit of input, thus lowering costs and improving competitiveness.

- Physical and financial resources: To acquire and use plants, machinery, buildings and finance efficiently according to business needs.

- Profit earning: To obtain reasonable returns on investment; profit is necessary for survival, expansion and rewarding stakeholders.

Q7: Explain the concept of business risk and its causes.

Ans:

The term "business risks" refers to the likelihood of reduced profits or losses due to unforeseen events. For example, a fall in demand because of changing consumer tastes or stronger competition can reduce sales and profits. Similarly, scarcity or price rise in raw materials increases production costs and lowers margins.

Types of business risks:

- Speculative risks: Arise from market conditions and may lead to gain or loss (for example, price changes or fashion risks).

- Pure risks: Result only in loss or no loss, for example, fire, theft or accidents.

Causes of business risks:

- Natural causes: floods, earthquakes and other disasters that disrupt production and supply chains.

- Human causes: employee dishonesty, strikes, managerial inefficiency or accidents.

- Economic causes: demand fluctuations, competition, price changes and changes in interest rates or taxes.

- Other causes: political instability, technical failures (for example, machinery breakdown) or exchange rate variations.

Q8: What factors are to be considered while starting a business? Explain.

Ans:

The following are some important factors to consider while starting a business:

Line-of-business selection: Decide the product or service and the field of activity, considering market demand, profitability and your skills or interests.

Size of the firm: Choose the appropriate scale of operations - small or large - based on demand stability, available finance and risk appetite.

Choice of ownership structure: Select a legal form - sole proprietorship, partnership, or company - keeping in mind capital needs, liability, control and continuity.

Business location: Choose a location that offers proximity to raw materials, labour, markets and essential services such as transport, banking and warehousing.

Funding the proposal: Estimate the required capital, identify sources of finance (own funds, loans, investors) and plan for efficient use of funds.

- assess required capital;

- identify funding sources; and

- plan for efficient capital utilisation.

Physical facilities: Arrange for suitable plant, machinery, buildings and utilities according to the nature and scale of business.

Plant layout: Prepare a layout that organises machinery and workflows to ensure efficient production and safety.

Workforce: Recruit and train the required skilled and unskilled staff and put in place measures for motivation and supervision.

Tax preparation: Carry out tax planning to understand obligations under relevant laws and to factor tax effects into financial planning.

Starting the business: After these decisions, mobilise resources, complete legal formalities, start production and implement a marketing plan to launch operations.

FAQs on NCERT Solutions - Nature and Purpose of Business

| 1. What is the main purpose of business and how does it differ from profit-making? |  |

| 2. What are the key characteristics that define the nature of business activities? | |

| 3. How does business differ from profession and employment in practical terms? | |

| 4. What role does risk play in business activities and why is it unavoidable? | |

| 5. Why is understanding business objectives important for Class 11 students preparing for exams? | |