NCERT Solutions - Business Services

Short Answer Question

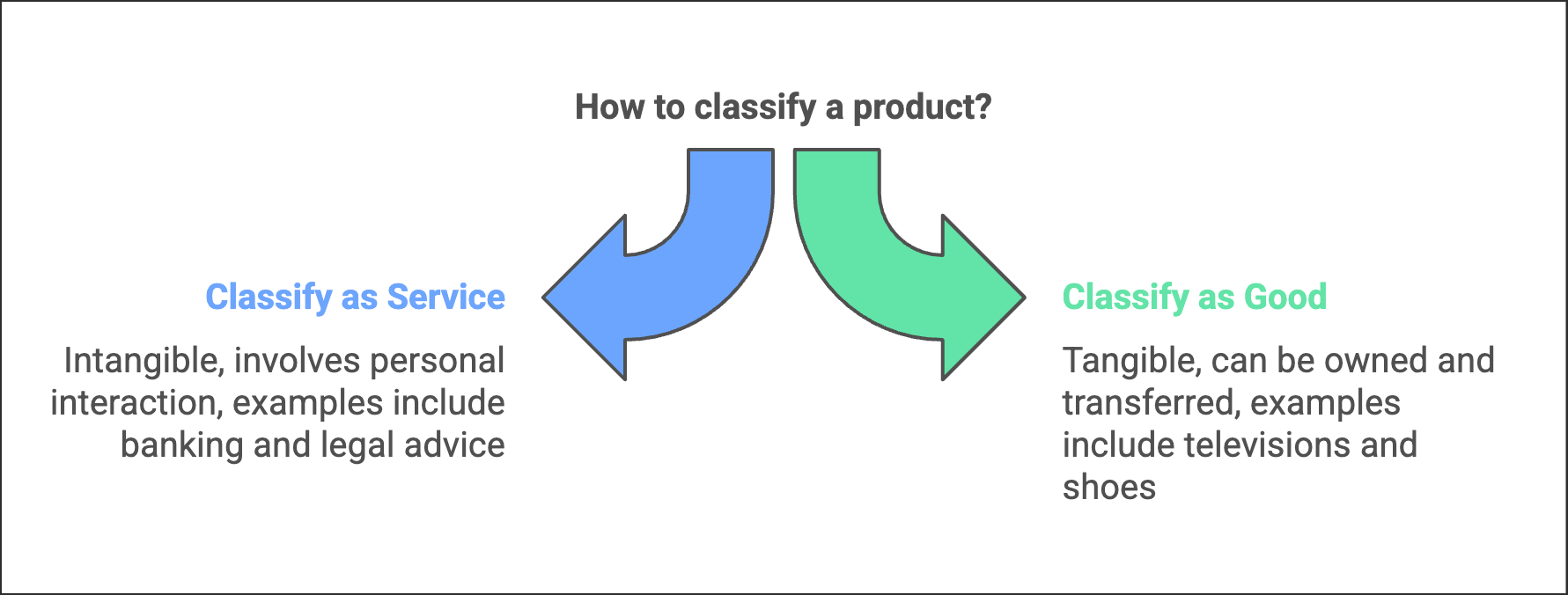

Q1. Define services and goods.

Ans: Services are activities or performances offered by one party to another that provide satisfaction or utility. They are intangible, cannot be owned and generally involve interaction between the provider and the consumer at the time of delivery. Services are often consumed as they are produced. They can be classified broadly into:

- Business services: Examples include banking, insurance and warehousing; these support business operations.

- Professional services: Examples include legal advice, medical consultations and tax consultancy; these require specialised skills or qualifications.

In contrast, goods are tangible items that can be seen, touched and stored. Ownership transfers on purchase. Examples include televisions, radios and shoes. Goods can be inventoried, transported and resold, while services are experienced and cannot be physically possessed.

Q2. What is e-banking. What are the advantages of e-banking?

Ans: E-banking refers to the delivery of banking services and transactions through electronic channels such as internet banking, mobile banking apps, ATMs and electronic fund transfer systems. It allows customers to perform routine banking tasks without visiting a branch. Common e-banking services include:

- transferring money between accounts or to other persons;

- checking account balances and transaction history;

- applying for loans, fixed deposits or other products online.

Key advantages of e-banking are:

- 24/7 availability: Customers can access services at any time, including outside normal branch hours, which adds convenience for those with busy schedules.

- Easy access: Banking is available via mobile phones or computers, reducing the need to visit a branch and saving travel time.

- Reduced branch workload: Routine transactions are handled electronically, allowing branch staff to focus on more complex customer needs.

- Better record keeping: Electronic statements and transaction logs help customers track spending and plan finances more effectively.

- Improved safety: Minimises the need to carry cash, lowering the risk of theft and loss; electronic authentication also helps secure transactions.

- Cost and time efficiency: Electronic transfers and payments are typically faster and cheaper than manual methods such as cheques or money orders.

Q3. Write a note on various telecom services available for enhancing business.

Ans: The following are the major telecom services that help businesses communicate and operate efficiently:

- Cellular mobile service: Provides voice calls, SMS and mobile data. It enables staff to communicate and access internet-based business applications while on the move.

- Radio paging service: A one-way service that sends short alerts or numeric messages to recipients. It is useful for urgent notifications where immediate acknowledgement is not required.

- Fixed-line service: Uses copper or fibre optic cables to carry voice and data. It provides reliable, high-speed connectivity for offices and data centres.

- Cable service: Transmits media and data to a defined area, typically for television and broadband services. Useful for marketing and information distribution in a region.

- VSAT service: Short for 'very small aperture terminal', this satellite-based service connects remote or rural locations where terrestrial networks are unavailable, extending business reach.

- DTH service: Direct-to-home TV service transmits channels by satellite. Businesses use DTH for broadcasting training, corporate messages or advertising to customers.

Together, these telecom services improve communication speed, support remote working and broaden a firm's ability to reach customers and suppliers.

Q4. Explain briefly the principles of insurance with suitable examples?

Ans:

- Utmost good faith: Both parties must be honest and disclose all material facts when entering into a policy. Example: Rahul must declare any existing heart condition when buying a life policy; failure to do so may lead to rejection of a claim.

- Insurable interest: The insured must stand to suffer financially from the loss of the insured item. Example: A business owner has insurable interest in their factory building and machinery because their loss would cause financial harm.

- Indemnity: The insurer compensates the insured to restore them to the same financial position as before the loss, but does not allow profit from the claim. Example: If stock worth Rs. 1 lakh is destroyed by fire, compensation is limited to that actual loss.

- Proximate cause: The loss must arise from a cause that is covered under the policy. Example: Damage caused by an insured peril such as fire is payable; if the loss results from an excluded peril, it may not be covered.

- Subrogation: After paying a claim, the insurer may take over the insured's right to recover the loss from a third party. Example: If a third party caused the damage, the insurer may pursue that party to recover costs.

- Contribution: If the same interest is insured with more than one insurer, each insurer shares the loss proportionately. Example: Two policies covering the same house will contribute to a claim in proportion to their sums insured.

- Mitigation: The insured must take reasonable steps to reduce or prevent further loss after an incident. Example: After a fire, the owner should arrange temporary repairs to limit additional damage and preserve eligibility for a claim.

Q5. Explain warehousing and its functions.

Ans: Warehousing is the organised storage of goods in a safe location to protect their quality and value until they are needed. Modern warehouses also provide services that support distribution and inventory management. Main functions include:

- Storage: Keeping raw materials and finished goods safe from damage, theft and spoilage until required.

- Value-added services: Activities such as grading, packaging, labelling and light assembly that increase the marketability of goods.

- Financing: Warehouse receipts can be used as collateral to obtain loans, helping businesses with working capital.

Long Answer Question

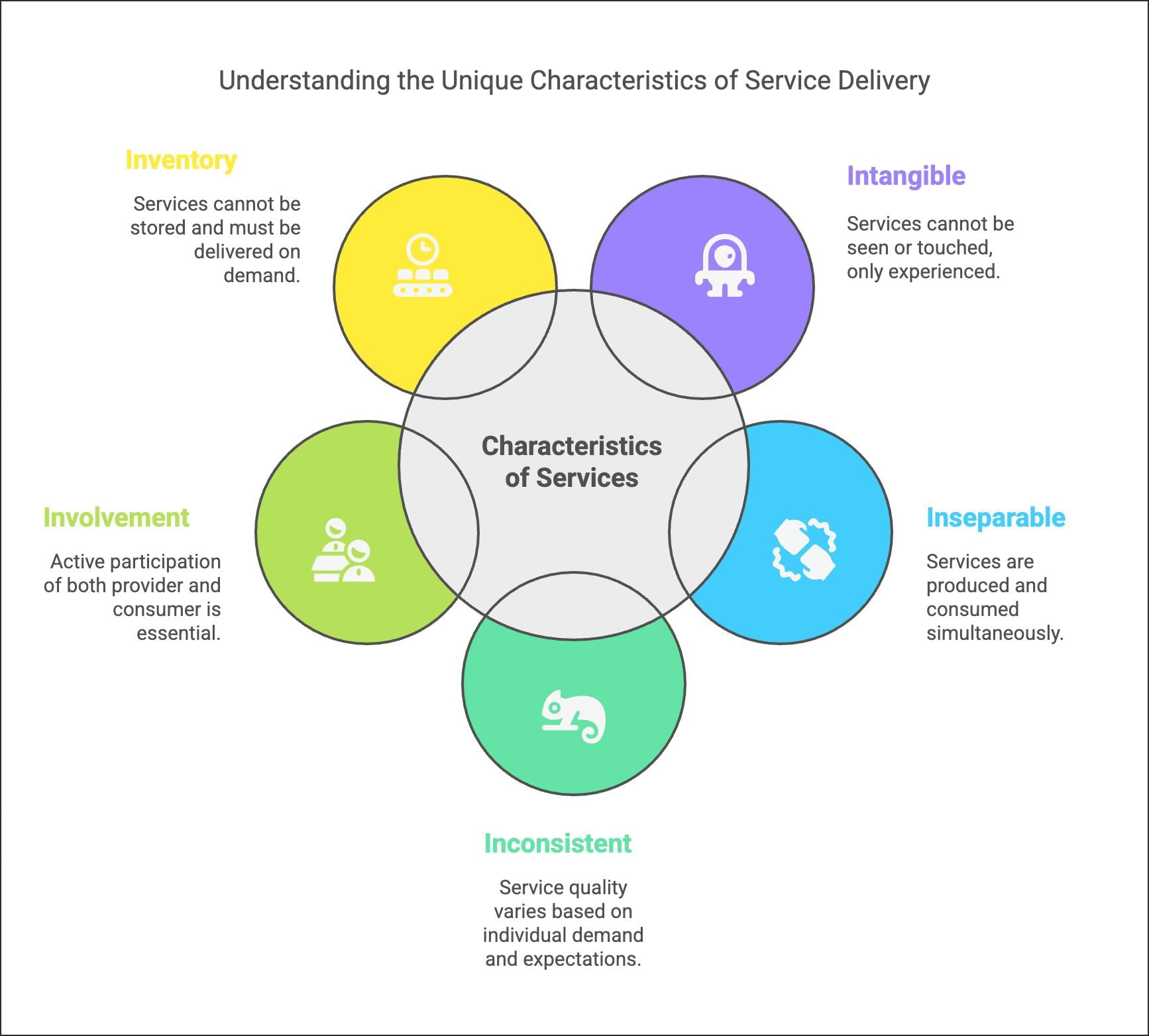

Q1. What are services? Explain their distinct characteristics.

Ans: Services are intangible economic activities provided to satisfy the needs of individuals or organisations. They normally involve direct interaction between the service provider and the consumer and do not result in ownership of any physical product. Services are commonly classified into business services (for example, banking, insurance and warehousing) and professional services (for example, legal advice, medical care and consultancy).

Distinct features of services are:

- Intangible: Services cannot be touched or held. Customers judge service quality from experience, reputation and interaction with the provider.

- Inseparable: Production and consumption often occur together; for example, a medical consultation is produced and consumed at the same time.

- Heterogeneous (inconsistent): Service quality may vary from provider to provider and from one occasion to another because human involvement causes variation.

- Involvement: Both the service provider and the customer participate in the service delivery process; their interaction affects the outcome.

- Perishability (no inventory): Services cannot be stored for later use; unused service capacity is lost (for example, an empty seat on a flight cannot be re-sold later).

Q2. Explain the functions of commercial banks with an example of each.

Ans: The main functions of commercial banks are:

- Collection of deposits: Banks accept deposits such as savings accounts, current accounts and fixed deposits. Example: A salaried person keeps monthly savings in a bank savings account and earns interest.

- Lending of funds: Banks advance loans and credit facilities like overdrafts, cash credits and term loans. Example: A business takes a bank loan to expand its factory; interest received is a major source of bank income.

- Cheque facility: Banks facilitate payments through cheques and operate clearing mechanisms. Example: A customer deposits a crossed cheque; it is routed through clearing and funds are credited to the payee's account.

- Remittance of funds: Banks enable safe transfer of money across locations using instruments such as bank drafts, pay orders and electronic transfers. Example: A person in Mumbai sends money to family in a different city using NEFT or RTGS.

- Provision of allied services: Banks offer services beyond core banking such as locker facilities, foreign exchange, underwriting and investment services. Example: A customer uses a bank locker to store valuable documents and jewellery.

Q3. Write a detailed note on various facilities offered by the Indian Postal Department.

Ans: The Indian Postal Department provides a wide range of services under three broad heads: financial facilities, mail facilities and allied services.

Financial Facilities:

- Public Provident Fund (PPF): A long-term small-savings scheme that offers tax benefits and a secure return for individuals.

- Kisan Vikas Patra (KVP): A savings certificate scheme that doubles the investment over a specified period if kept till maturity.

- National Savings Certificate (NSC): A fixed-income investment scheme suitable for small savers with guaranteed returns and tax benefits.

- Recurring Deposit Scheme: Allows customers to deposit a fixed sum every month and earn interest at a fixed rate.

- Fixed Deposit Scheme: Term deposits for a fixed period offering higher interest than savings accounts.

- Money Order Facility: Safe transfer of small sums of money to any part of the country, useful where banking services are limited.

Mail Facilities:

Mail services include:

- (i) Parcel facilities: Transport of goods and articles from one place to another with tracking options.

- (ii) Registration facilities: Registered post offers added security and a legal record of delivery.

- (iii) Insurance facilities: Insurance of valuable articles sent through post to cover loss or damage during transit.

Common mail items include:

- Postcards: The cheapest form of postal communication for short messages.

- Letters: Placed in envelopes and used where privacy of communication is required.

- Registered post: Ensures recorded delivery to the addressee or return to sender if undelivered.

Allied Facilities:

- Passport Service: Post offices act as authorised centres for accepting passport applications on behalf of the Ministry of External Affairs.

- Media Post: Offers corporate advertising through postal items like postcards and brochures.

- Direct Post: Delivers promotional material such as brochures and pamphlets to targeted areas.

- Speed Post: A fast delivery service for parcels and documents within a guaranteed time frame.

Q4. Describe various types of insurance and examine the nature of risks protected by each type of insurance.

Ans: Insurance may be classified into several types. The main types discussed here are life insurance, fire insurance and marine insurance. Each covers particular risks:

1. Life insurance

- Life insurance is a contract in which the insurer promises to pay a specified sum on the death of the insured or on maturity of the policy. The insured pays a periodic premium for this protection.

- It protects two principal risks:

- Risk of premature death: Provides financial support to dependants if the insured dies early, for example paying a lump sum to the family.

- Risk of living too long: Ensures retirement income or maturity benefits for the insured who survives the policy term, providing financial security in old age.

2. Fire insurance:

- Fire insurance covers loss or damage to property caused by fire and related perils such as lightning, explosion and sometimes malicious damage. The insurer pays compensation up to the sum insured, subject to terms and conditions. The insured must take reasonable steps to prevent or reduce damage to remain eligible for a claim.

3. Marine insurance:

- Marine insurance protects goods, ships and freight against losses during transit by sea (and often by other means). It covers perils such as sinking, collision, piracy, bad weather and theft during the voyage. Marine insurance helps traders manage the uncertainty and financial exposure associated with transporting goods.

Each insurance type addresses specific uncertainties and helps individuals and businesses manage financial consequences arising from those risks by transferring potential loss to the insurer.

Q5. Explain in detail the warehousing services.

Ans: Warehousing provides storage and associated services that support production, distribution and trade. Detailed warehousing services include:

- Consolidation: Collecting goods from different suppliers and grouping them for efficient dispatch to customers, reducing transport costs and simplifying logistics.

- Bulk breaking: Receiving goods in large consignments and dividing them into smaller lots for distribution to retailers or consumers.

- Stockpiling: Storing goods to meet seasonal demand or to stabilise supply, helping firms manage production and sales cycles.

- Price stabilisation: By storing surplus goods during periods of excess supply and releasing them during shortages, warehouses help moderate price fluctuations in the market.

- Value-added services: Activities such as grading, packaging, labelling and light assembly that improve product readiness for sale and reduce handling time downstream.

- Financing: Warehouse receipts act as documents of title and can be used as security to obtain credit from financial institutions, aiding working capital requirements for traders and producers.

FAQs on NCERT Solutions - Business Services

| 1. What are business services? |  |

| 2. What is the importance of business services? | |

| 3. How can businesses benefit from outsourcing business services? | |

| 4. What factors should businesses consider when selecting a business services provider? | |

| 5. How can businesses ensure the quality of business services received? | |