NCERT Solutions - Sources of Business Finance

Short Answer Questions

Q1: What is business finance? Why do businesses need funds? Explain.

Ans: Business finance is the capital or funds required to set up, run and expand a business. It includes money needed to acquire fixed assets, meet day-to-day expenses and finance growth. Business finance covers funds for starting operations, running regular activities and for future expansion or diversification.

The following are the main reasons why a business needs funds.

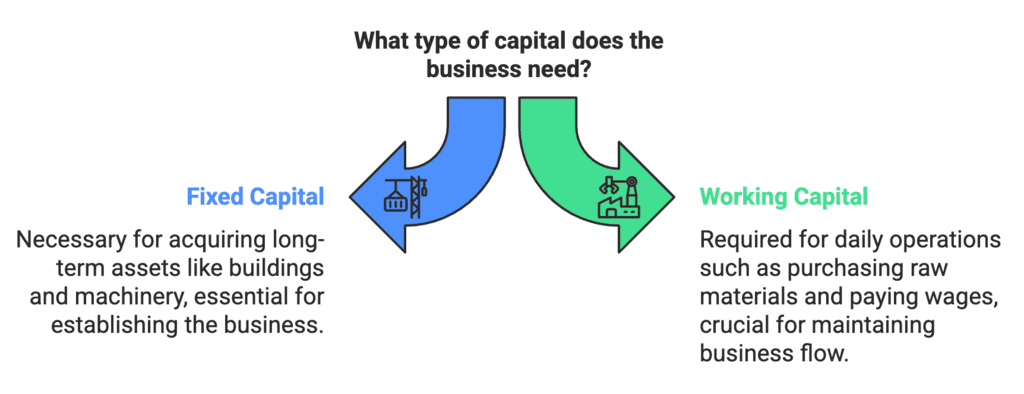

- Fixed capital requirements: Funds are needed to acquire long-term assets such as land, buildings, machinery, furniture and fixtures. The amount of fixed capital depends on the size, nature and scale of the business. Without adequate fixed capital, a business cannot start or operate efficiently.

- Working capital requirements: Businesses need funds to finance routine, short-term operations - for example, buying raw materials, paying wages and meeting other day-to-day expenses. Sufficient working capital ensures smooth production and timely delivery of goods and services.

Q2: List sources of raising long-term and short-term finance.

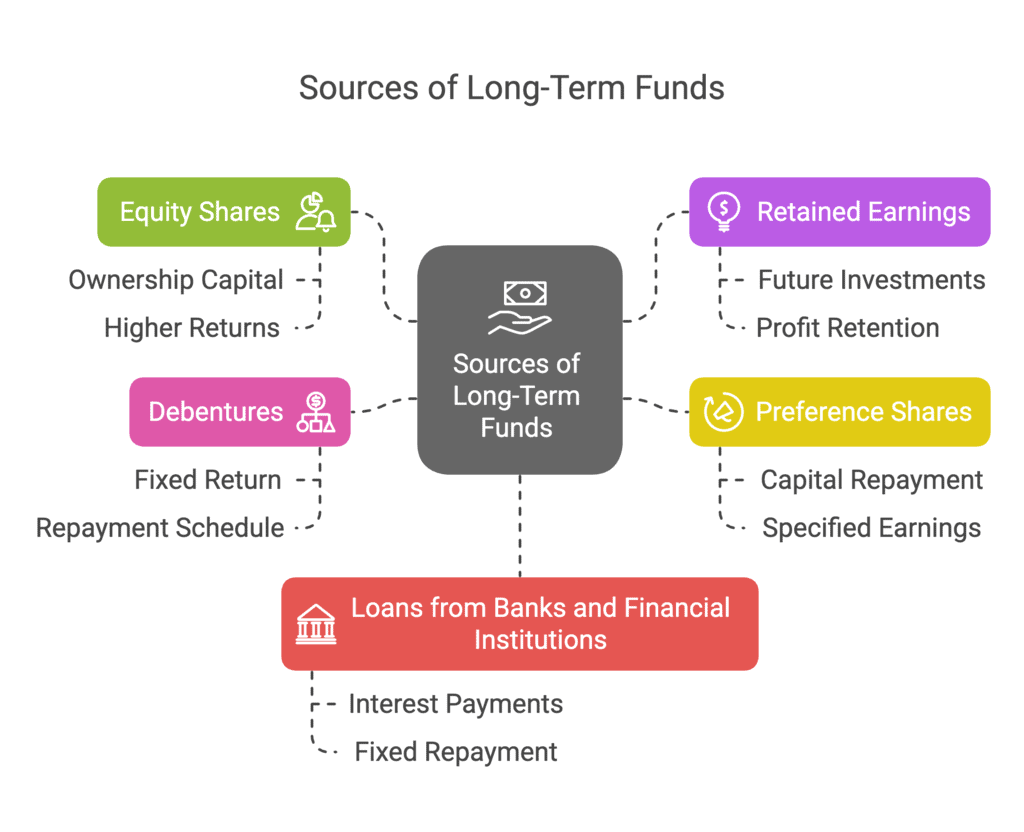

Ans: The following are some of the sources of long-term funds.

- Equity shares: Capital raised by issuing equity shares represents ownership in the company. Equity shareholders share in the profits through dividends and usually have voting rights. Equity is suitable for long-term expansion and does not require fixed repayments.

- Retained earnings: These are profits that a company retains instead of distributing as dividends. Retained earnings are an internal long-term source of finance and can be used for expansion, modernisation or meeting unforeseen needs.

- Debentures: Debentures are long-term debt instruments issued by companies. They carry a fixed rate of interest and have a stipulated date for repayment. Debenture holders are creditors and do not have ownership rights.

The following are some of the sources of short-term funds.

- Trade credit: Credit extended by suppliers to the buyer for the purchase of goods without immediate payment. It helps firms manage short-term cash flow.

- Banks: Banks provide short-term finance in the form of cash credits, overdrafts and short-term loans to meet working capital needs.

- Commercial paper: Short-term, unsecured promissory notes issued by creditworthy firms to raise funds for a short period. They are cost-effective for well-rated companies.

Q3: What is the difference between the internal and external sources of raising funds? Explain.

Ans: Internal sources of funds are generated from within the business. Examples include:

- Selling surplus inventories

- Collecting receivables

- Reinvesting profits

These funds usually have low explicit cost and are immediately available, but they are often limited in amount. External sources of funds come from outside the organisation, such as:

- Suppliers

- Creditors

- Investors

- Banks and financial institutions

External funds can meet larger and long-term requirements, but they may involve explicit costs (interest, fees) and conditions. In summary:

- Internal sources: limited, generated within the business and usually less costly.

- External sources: larger in amount, obtained from outside and may carry more conditions or costs.

Q4: What preferential rights are enjoyed by preference shareholders? Explain.

Ans: Preference shares give holders certain priority rights over equity shareholders. The main preferential rights are:

- Priority in dividend: Preference shareholders receive dividends at a fixed rate before any dividend is paid to equity shareholders. If dividends cannot be paid in a year, certain types allow accumulation for future payment.

- Priority in capital repayment: In the event of winding up or liquidation, preference shareholders are entitled to repayment of their capital before equity shareholders.

Preference shares combine features of both equity and debt: they often carry a fixed return like debt but do not create a legal liability to repay the capital until liquidation. Preference shareholders generally do not have voting rights at ordinary general meetings, except in certain special circumstances. Common types include:

- Cumulative: Unpaid dividends accumulate and must be paid later.

- Participating: After fixed dividends, holders may share in extra profits.

- Convertible: Can be converted into equity shares at a specified time or ratio.

Overall, preference shares suit investors seeking stable income with lower risk than equity, while companies use them to raise funds without diluting control.

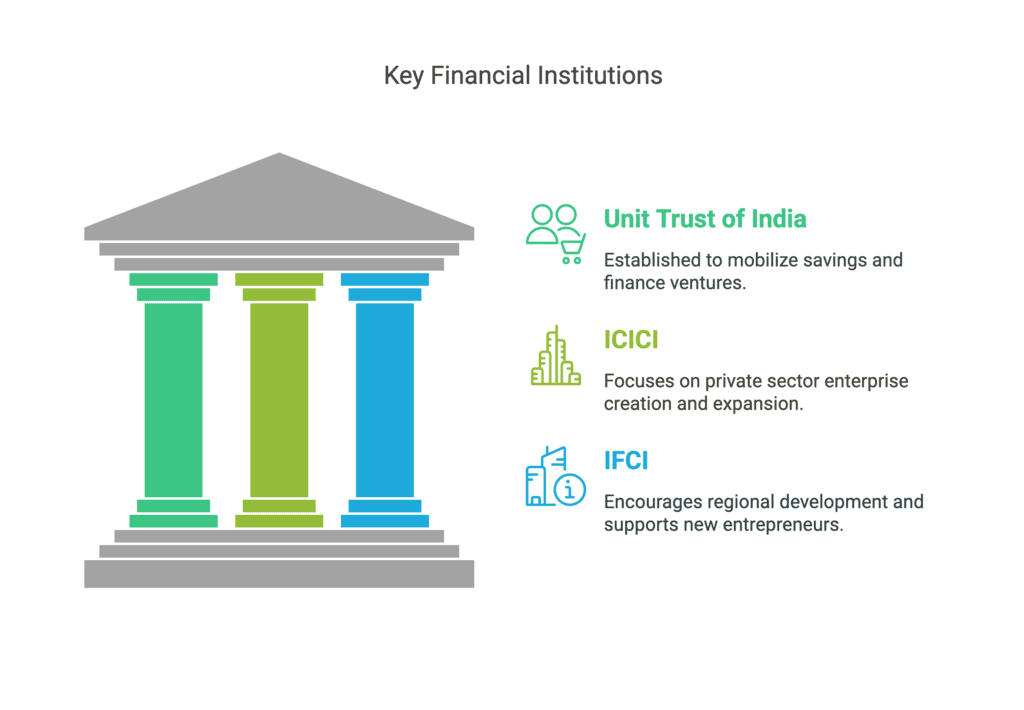

Q5: Name any three special financial institutions and state their objectives.

Ans: Financial institutions are organisations that provide long-term and specialised finance to industry and business. Three important institutions are:

- Unit Trust of India (UTI): Established in 1964 under the Unit Trust of India Act, 1963, UTI was created to mobilise small savings from the public and invest them in profitable ventures, thereby promoting wider participation in capital markets.

- Industrial Credit and Investment Corporation of India (ICICI): Formed in 1955 as a development finance institution, ICICI's objective was to provide long-term finance and technical assistance to promote industrial development and modernisation in the private sector.

- Industrial Finance Corporation of India (IFCI): Established in 1948 under the Industrial Finance Corporation Act, 1948, IFCI was set up to provide long-term finance to industrial enterprises, support regional development and encourage new entrepreneurs in priority sectors.

Q6: What is the difference between GDR and ADR? Explain.

Ans: Global Depository Receipts (GDRs) and American Depository Receipts (ADRs) are instruments that allow investors to buy shares of foreign companies in local markets. The key differences are:

- Market: ADRs are issued for foreign companies to be traded in the United States markets. GDRs are issued to be traded in international markets outside the issuing company's home country, commonly in Europe and other financial centres.

- Issuing bank and trading currency: Both are issued by a depository bank against underlying shares. ADRs are usually denominated in US dollars; GDRs are commonly denominated in US dollars or euros.

- Investor base: ADRs are designed primarily for US investors to access foreign equities on US exchanges. GDRs target a broader international investor base and are freely tradable in multiple markets.

- Accessibility and regulation: ADRs must comply with US regulatory requirements and reporting standards. GDRs are governed by the regulations of the markets where they are listed and by the terms set by the depository bank.

Both GDRs and ADRs facilitate foreign investment, increase liquidity for the issuing company and provide investors with easier access to international stocks without dealing directly with foreign exchanges.

Long Answer Questions

Q1: Explain trade credit and bank credit as sources of short-term finance for business enterprises.

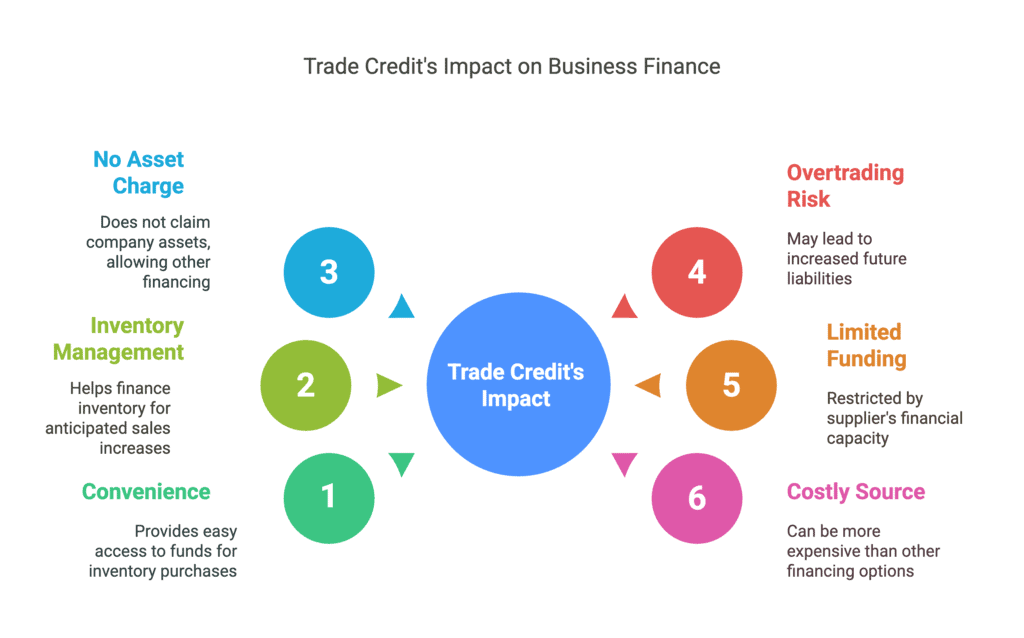

Ans: Trade credit: Trade credit is credit extended by suppliers to buyers, allowing goods to be purchased and paid for at a later date. It is an informal short-term source of finance widely used by businesses to manage working capital.

Merits of Trade Credit:

- Convenience: Easy and quick to obtain as part of normal business transactions.

- Helps inventory management: Firms can purchase inventory in advance of sales without immediate cash outflow.

- No collateral: Usually does not require pledging assets, so it keeps borrowing capacity open for other sources.

Demerits of Trade Credit:

- Risk of overtrading: Excessive reliance may lead a firm to overextend itself and face liquidity problems later.

- Limited availability: The amount depends on the supplier's financial strength and business relationship.

- Costly if discounts are foregone: If early payment discounts are available but not taken, the effective cost of trade credit can be high.

Bank credit: Bank credit consists of loans, overdrafts, cash credit and other facilities provided by banks to meet short-term working capital needs. Banks normally assess creditworthiness and may require security or collateral.

Merits of Bank Credit:

- Flexibility: Various tailored products (overdrafts, cash credit) suit different needs and seasonal requirements.

- Confidentiality and reliability: Banks maintain confidentiality and provide a stable source of funds backed by formal agreements.

Demerits of Bank Credit:

- Security and conditions: Banks often require collateral and impose covenants that can restrict business decisions.

- Cost and procedures: Interest and processing charges increase the cost; obtaining large limits may be time-consuming.

Q2: Discuss the sources from which a large industrial enterprise can raise capital for financing modernisation and expansion.

Ans: The following are common long-term sources suitable for large industrial enterprises:

- Equity shares: Provide permanent capital without fixed repayment obligations. Equity is suitable for financing long-term projects but may dilute existing ownership and control.

- Retained earnings: Using undistributed profits avoids external borrowing and interest costs. Retained earnings are a safe internal source but depend on the firm's profitability and may be limited.

- Preference shares: Offer fixed dividends and priority over equity at liquidation. They do not usually carry voting rights, so owners retain control better than with equity issues.

- Debentures: Long-term debt instruments with fixed interest payments. Debentures do not dilute ownership, and interest payments are tax-deductible, but they create fixed financial obligations.

- Loans from banks and financial institutions: Term loans and specialised finance from financial institutions can fund expensive modernisation projects. These often come with technical guidance and structured repayment schedules.

Q3: What advantages does the issue of debentures provide over the issue of equity shares?

Ans: Debentures offer several advantages compared with issuing equity shares:

- No dilution of ownership: Debenture holders are creditors, not owners. Issuing debentures does not reduce existing shareholders' control or voting power.

- Tax advantage / lower cost: Interest paid on debentures is tax-deductible for the company, which can reduce the overall cost of capital compared with dividends on equity, which are not tax-deductible.

- Fixed obligation: Debentures carry a fixed rate of interest and a predetermined redemption schedule. This predictability helps in financial planning. Equity dividends are variable and depend on profitability.

Q4: State the merits and demerits of public deposits and retained earnings as methods of business finance.

Ans: Public deposits: Companies can accept deposits from the public for short- to medium-term finance. Depositors receive a receipt and periodic interest.

Merits of Public Deposits:

- Simple procedure: Raising funds through public deposits is relatively straightforward and involves fewer formalities than some other sources.

- Lower cost than some borrowings: Interest on public deposits is often lower than the cost of some bank loans or overdrafts.

- No dilution of ownership: Depositors are creditors and do not gain management or voting rights.

Demerits of Public Deposits:

- Limited amount: The total funds available depend on public willingness to invest and the firm's reputation.

- Unsuitable for new firms: New or unknown companies may find it difficult to attract depositors.

- Repayment obligation: Deposits are repayable and may create liquidity pressure at maturity if not managed well.

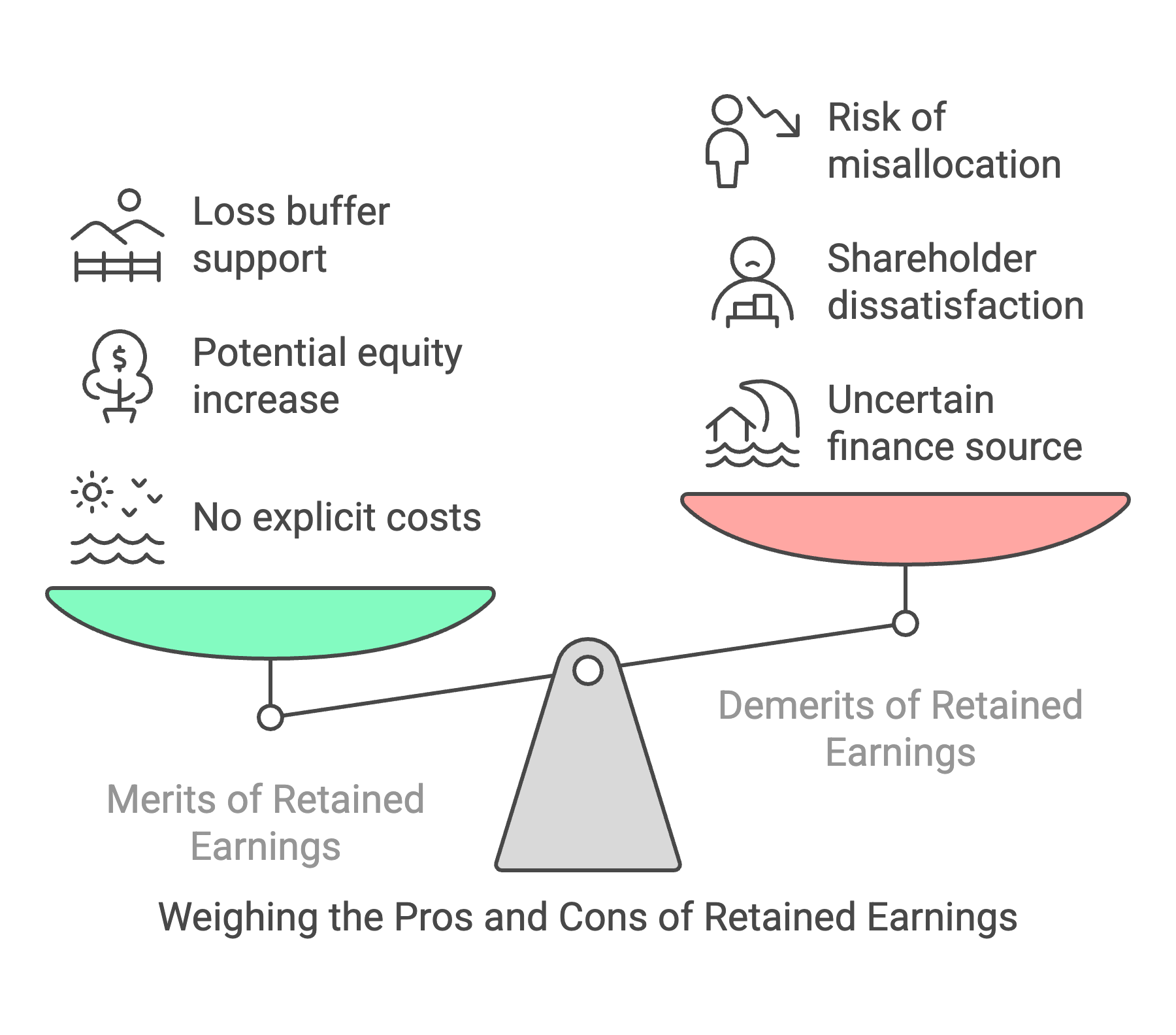

Retained Earnings: These are profits kept in the business for reinvestment rather than distributed as dividends.

Merits of Retained Earnings:

- No explicit cost: Retained earnings do not incur flotation costs, interest or dilution of control.

- Reduces external dependence: Using internal funds lessens reliance on external lenders and their conditions.

- Supports stability: Retained earnings can cushion against future downturns or unexpected losses.

Demerits of Retained Earnings:

- Uncertain availability: They depend on the firm's profitability and may not be sufficient for large projects.

- Shareholder dissatisfaction: Excessive retention may upset shareholders who expect dividends.

- Opportunity cost: Retaining earnings means those funds are not available for shareholders to invest elsewhere; poor internal allocation may lead to sub-optimal use.

FAQs on NCERT Solutions - Sources of Business Finance

| 1. What are the different sources of business finance? |  |

| 2. How can a company raise funds through equity shares? | |

| 3. What are the advantages of raising funds through debentures? | |

| 4. How can a company obtain loans from financial institutions? | |

| 5. What is trade credit and how does it serve as a source of business finance? | |