NCERT Solutions - Introduction (Macroeconomics)

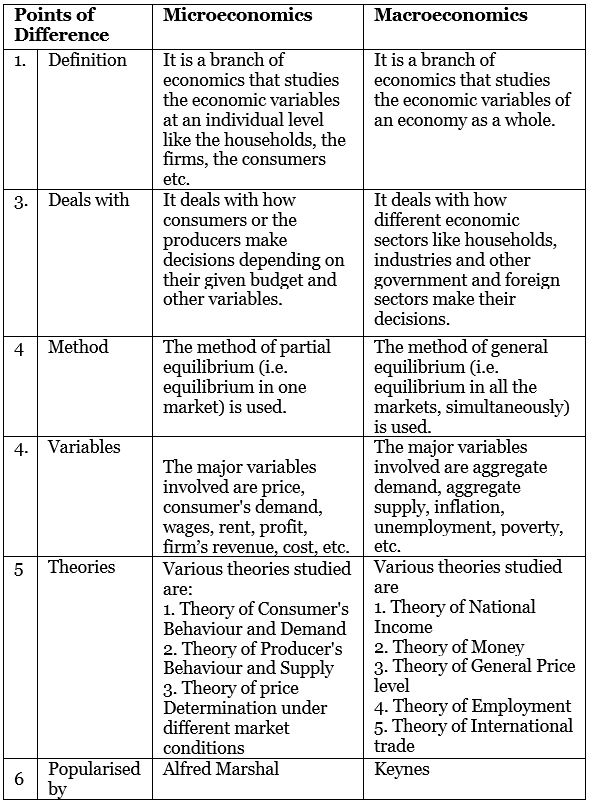

Q1: What is the difference between microeconomics and macroeconomics?

Ans:

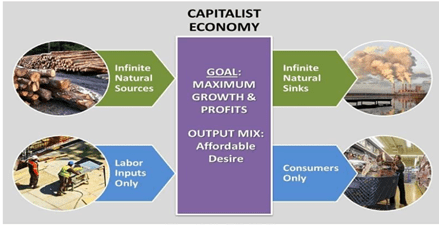

Q2: What are the important features of a capitalist economy?

Ans: The capitalist economy is an economic system where the means of production are privately owned. These means of production are driven by the motive of profit-making. This economic structure is also known as a free market economy or laissez-faire.

The following are the features of a capitalist economy:

- Role of the government: The government provides the legal and institutional framework needed for markets to function. It maintains law and order, enforces contracts and protects property rights. Its role is usually limited to creating conditions for markets rather than directly organising production.

- Profit motive: Economic agents-owners, firms and entrepreneurs-are mainly motivated by profit. This motive encourages efficiency, innovation and investment as firms seek to reduce costs and increase returns.

- Central problems: In a capitalist economy, the basic economic problems of what to produce, how to produce and for whom to produce are largely resolved by market forces of demand and supply. Prices act as signals that guide producers and consumers.

- Role of the private sector: Private individuals and firms own and operate the means of production. They decide what to produce, how much to invest and how to employ resources. The private sector plays the dominant role in producing goods and services.

- Laissez-faire: The system is often called laissez-faire, meaning minimal government interference. Markets are allowed to operate freely, although in practice some regulation exists to correct market failures and protect consumers.

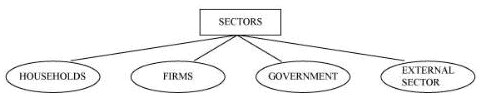

Q3: Describe the four major sectors in an economy according to the macroeconomic point of view.

Ans: The four major sectors of an economy according to the macroeconomic point of view are:

(i) Households: Households buy goods and services for consumption and also supply factors of production such as land, labour, capital and entrepreneurship. They earn income by supplying these factors and use that income to consume goods and services.

(ii) Firms: Firms are the production units that combine factors of production to produce goods and services. They employ labour and capital, make production decisions and sell output in markets with the aim of earning profit.

(iii) Government: The government provides public goods and services, enforces laws, and undertakes developmental projects such as infrastructure, education and health. Its objective is social welfare and economic stability rather than profit. It also influences aggregate demand through taxation and public expenditure.

(iv) External sector: The external sector deals with trade and financial transactions with the rest of the world. Exports are domestic goods and services sold abroad; imports are goods and services bought from other countries. The external sector affects domestic output, income and employment.

Q4: Describe the Great Depression of 1929.

Ans: The Great Depression was a severe worldwide economic downturn that began in 1929, triggered by the stock market crash in the United States. It spread rapidly to other countries and lasted through the 1930s. Key points include:

- Primary causes: A sharp fall in aggregate demand because of underconsumption by households and excessive investment in speculative activities. Overproduction in some industries meant unsold goods accumulated, which pushed prices down.

- Impact on prices and profits: Falling prices (deflation) reduced business profits, forcing firms to cut production and postpone investment.

- Employment and income: Unemployment rose dramatically; in the United States it rose from about 3% before the crash to nearly 25% at its peak. Falling incomes further reduced demand, creating a vicious cycle.

- Global effects: World trade declined, international lending and investment fell, and many countries experienced severe economic contraction.

The Great Depression had important implications for economic thought and policy:

- It exposed limitations of classical economics that relied on self-correcting markets and full employment assumptions.

- It led to the development and acceptance of the Keynesian approach, which argued that active government intervention-especially fiscal stimulus-was necessary to restore demand and employment.

- It helped establish macroeconomics as a distinct field, focusing on aggregates like national income, unemployment and inflation, and on the role of government policy.

In short, the sequence can be summarised as: Low demand → Falling prices and profits → Reduced output → Rising unemployment → Falling income → Further fall in demand. The lessons of 1929 emphasised the need for policy measures to stabilise aggregate demand during downturns.

FAQs on NCERT Solutions - Introduction (Macroeconomics)

| 1. What is macroeconomics and how is it different from microeconomics? |  |

| 2. Why do we need to study macroeconomics to understand the Indian economy? | |

| 3. What are the main objectives of macroeconomic policy that UPSC asks about? | |

| 4. How do circular flow of income and national accounting concepts relate to real Indian economy problems? | |

| 5. What key macroeconomic indicators should I focus on for UPSC preparation on the Indian economy? | |