NCERT Solutions - Money and Banking

Q1: What is a barter system? What are its drawbacks?

Ans: Barter system was the method of exchange used in ancient times in which goods were traded directly for other goods without the use of money. For example, a person who had rice and wanted tea would seek someone who had tea and wanted rice. An economy operating on barter was called a 'C-C economy' (commodity for commodity).

The main drawbacks of the barter system are as follows:

- Problem of double coincidence of wants: Exchange can occur only when two parties each have what the other wants. For example, a person with tea can exchange it for rice only if they find someone who wants tea and has rice to offer.

- Lack of common unit of value: There was no standard measure to compare the values of different goods. It was difficult to state how many units of one commodity equalled a unit of another - for example, how many sacks of rice equal one horse.

- Difficulty in storing wealth: Many commodities are perishable or bulky, so they cannot be stored easily for future use. This made saving and deferred payments difficult; storing value in the form of goods (like food or livestock) was inefficient and risky.

- Lack of standard of deferred payments: Contracts or loans were hard to enforce because future payments in goods were uncertain in value and difficult to store. Repayment in specific commodities was often impractical.

Q2: What are the main functions of money? How does money overcome the shortcomings of a barter system?

Ans: The main functions of money are:

- Medium of exchange: Money serves as a commonly accepted medium through which goods and services are bought and sold. This removes the need for a double coincidence of wants: sellers accept money and buyers pay money, so direct barter is unnecessary.

- Unit of value: Money provides a single standard for measuring and comparing the value of different goods and services. Prices express value in terms of money, making exchange and valuation simple and uniform.

- Store of value: Money can be saved and used in the future without significant loss of value (subject to inflation). It is easier to store wealth in money than in perishable or bulky commodities.

- Standard of deferred payments: Money provides a standard for settling debts and future obligations. Loans, wages and interest can be contracted and repaid in money, which is more convenient than repayment in goods.

How money overcomes the shortcomings of barter:

- Money removes the need for double coincidence of wants because goods are exchanged for money rather than for other commodities.

- By acting as a common unit of value, money makes comparison of prices and exchange easy and consistent.

- Money provides a convenient way to store value for future use, avoiding the problems of storing perishable or bulky goods.

- Money enables clear and enforceable deferred payments, making contracts, loans and savings practical in an economy.

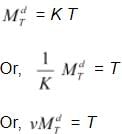

Q3: What is transaction demand for money? How is it related to the value of transactions over a specified period of time?

Ans: Transaction demand for money is the demand to hold money for everyday purchases and regular payments - that is, to meet routine transactions. Because incomes are received at particular times while spending takes place continuously, people and firms hold some money balances to carry out transactions.

The relationship between the total value of transactions and the transaction demand for money can be expressed using the following identity:

The transaction demand for money in an economy  can be written as

can be written as

Where,

,

,represents velocity of circulation of money

T = Total value of transactions in the economy over a period of time

K is a positive fraction

= Stock of money people are willing to hold at a particular point of time.

= Stock of money people are willing to hold at a particular point of time.The key points are:

- Transaction demand for money is positively related to the total value of transactions (T): more transactions require larger money balances.

- It is negatively related to the velocity of circulation (V): if each unit of money changes hands more frequently, less money is needed to support the same volume of transactions.

- In simple terms, the transaction demand can be written as MT = k × T, where k is the proportion of the total transactions that people prefer to hold as money (k is the reciprocal of velocity).

Q4: What are the alternative definitions of money supply in India?

Ans: Money supply in India is measured by four broad aggregates, commonly denoted as M1, M2, M3 and M4. They are defined as follows:

Measures of M1 include:

- Currency notes and coins with the public (excluding cash in hand of all commercial banks) [C]

- Demand deposits of all commercial and co-operative banks excluding inter-bank deposits (DD). Demand deposits are withdrawable at any time, often by cheque.

- Other deposits with the Reserve Bank of India [O.D.]. These are deposits held by RBI on behalf of units other than government and banks.

- M1 = C + DD + O.D.

Measures of M2

- M1 (C + DD + O.D.)

- Post office savings deposits (small savings deposited with post office saving schemes)

Measures of M3

- M1

- Time deposits of all commercial and co-operative banks (these cannot be withdrawn before a specified period; fixed deposits are an example)

Measures of M4

- M3

- Total deposits with the post office saving organisation (excluding National Savings Certificates)

These aggregates move from narrow to broad measures of money: M1 is the narrowest and M4 the broadest measure of money supply.

Q5: What is a 'legal tender'? What is 'fiat money'?

Ans: Legal tender is currency - notes and coins - that the monetary authorities (the Reserve Bank of India and the Government of India) have declared acceptable as a legal medium of payment for settling debts and obligations. Creditors are obliged to accept legal tender as payment.

Fiat money is money that has value because the government declares it to be legal tender. It is not backed by a physical commodity such as gold or silver; its acceptability rests on trust in the issuing authority and on the legal status given by government. Fiat money therefore has no intrinsic value equal to its face value; its value is derived from legal decree and collective acceptance.

Q6: What is High Powered Money?

Ans: High powered money, also called the monetary base or reserve money, is the total liability of the central bank (RBI) and is created by the RBI. It includes:

- Currency (notes and coins) in circulation with the public,

- Deposits of the government with the RBI, and

- Reserves of commercial banks maintained with the RBI (cash reserves).

In simplified form, high powered money is written as:

H = C + R

Where:

H = High powered money

C = Currency in circulation

R = Cash reserves of commercial banks with the RBI

High powered money forms the base from which commercial banks create additional money via credit creation.

Q7: Explain the functions of a commercial bank.

Ans: Commercial banks perform several important functions. The main ones are:

Accepting deposits

Commercial banks accept various types of deposits from the public:

- Savings accounts: For individuals wishing to save and earn interest. These accounts allow deposits and limited withdrawals; cheque facilities are usually limited.

- Fixed deposit accounts: Deposits kept for a fixed period that earn a higher rate of interest. Funds cannot normally be withdrawn before the agreed period without penalty.

- Current (or demand) accounts: Primarily used by businesses. Funds can be withdrawn at any time by cheque; these accounts typically do not earn interest but allow many transactions.

Granting loans and advances

- Commercial banks lend money to individuals and businesses. Loans are usually long-term and granted against security, while advances are short-term facilities. The interest rate on loans is higher than the interest paid on deposits.

Agency functions

As agents, banks perform services on behalf of their customers:

- Transfer of funds via cheques, demand drafts and electronic transfers.

- Collection of cheques, bills of exchange, dividends and interest on securities.

- Payment of insurance premiums, taxes and utility bills on behalf of customers.

- Acting as trustees, executors and agents for investment and estate management.

Discounting bills of exchange

- Banks buy bills of exchange before their maturity by discounting them (deducting interest). This provides short-term finance to firms.

Credit creation

- By receiving deposits and making loans, commercial banks create credit and expand the supply of money in the economy. This credit creation supports investment and economic growth.

Other functions

- Providing safe custody facilities (lockers).

- Buying and selling foreign exchange.

- Issuing travellers' cheques and gift cheques.

- Underwriting issues of shares and debentures.

- Supplying information and data useful to customers and the public.

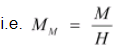

Q8: What is money multiplier? How will you determine its value? What ratios play an important role in the determination of the value of the money multiplier?

Ans: The money multiplier is the ratio of the stock of money (M) to the stock of high powered money (H) in the economy:

That is, MM = M/H.

The money multiplier is always greater than 1 because commercial banks create additional deposits by lending a portion of their deposits.

The value of the money multiplier can be derived as follows (outline as in the text):

We know that M = C + DD = (1 + cdr) × DD

Where:

M = Money supply

C = Currency held by the public

cdr = Currency-deposit ratio (currency held relative to deposits)

DD = Demand deposits

Let total deposits be D.

High powered money H = C + R

= cdr × D + rdr × D

= D × (cdr + rdr) (taking D common)

Thus MM = M/H = (1 + cdr) / (cdr + rdr)

Since rdr (reserve-deposit ratio) is less than 1, the multiplier is a function of the currency-deposit ratio (cdr) and the reserve-deposit ratio (rdr).

The roles of the ratios:

- Currency-deposit ratio (cdr): Higher cdr means people hold more currency relative to deposits, reducing the portion of deposits that can be re-lent by banks, and thus lowering the multiplier.

- Reserve-deposit ratio (rdr): Higher rdr means banks keep a larger fraction of deposits as reserves, leaving less for lending and lowering the multiplier.

Therefore, both a higher cdr and a higher rdr reduce the money multiplier, while lower values increase it.

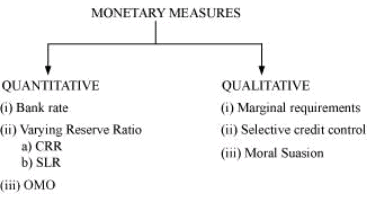

Q9: What are the instruments of monetary policy of RBI?

Ans: The Reserve Bank of India uses both quantitative and qualitative instruments to regulate money supply and credit. The flow chart in the book summarises these instruments:

Quantitative measures

Quantitative measures influence the overall quantity of money and credit in the economy. Major instruments include:

1. Bank rate: The interest rate at which the central bank lends to commercial banks. An increase in the bank rate raises borrowing costs for banks and tends to reduce lending and money supply; a decrease has the opposite effect.

2. Varying reserve ratios: The central bank can change reserve requirements for commercial banks. The main ratios are:

(i) Cash Reserve Ratio (CRR): CRR is the minimum percentage of deposits that banks must keep with the RBI in cash. Raising the CRR reduces funds available for lending and thereby reduces money supply; lowering CRR increases lending capacity.

(ii) Statutory Liquidity Ratio (SLR): SLR is the minimum percentage of net demand and time liabilities that banks must maintain in specified liquid assets (such as government securities). Increasing SLR reduces the funds available for lending and curbs money supply; decreasing SLR releases funds for credit expansion.

3. Open Market Operations (OMO): OMO are purchases and sales of government securities by the RBI in the open market. Selling securities absorbs liquidity from the system and reduces money supply; buying securities injects liquidity and increases money supply.

Qualitative measures: Qualitative measures affect the direction and quality of credit rather than its overall quantity. Key instruments include:

1. Margin requirements: Banks insist on a margin between the market value of security and the loan amount. Raising margin requirements reduces bank lending against securities and restricts credit to certain activities.

2. Selective Credit Controls (SCC): These are measures to encourage or restrict lending to certain sectors. For example, directed lending to priority sectors or restrictions on credit for speculative activities.

3. Moral suasion: The RBI uses persuasion, consultations and guidance to influence banks' behaviour. It is an informal tool - discussions, guidelines and public statements aimed at encouraging banks to follow policy objectives.

Q10: Do you consider a commercial bank 'creator of money' in the economy'?

Ans: Yes. Commercial banks are money creators because they accept deposits and lend a portion of those deposits. When banks grant loans, the loan proceeds are typically deposited in bank accounts, creating new demand deposits and thereby increasing the money supply.

Example (as given):

A depositor places Rs.10,000 in a savings account. If the bank keeps a cash reserve of 10% (CRR = 10%), it retains Rs.1,000 and lends out Rs.9,000. The Rs.9,000 when spent becomes income for others and is redeposited in banks, creating further deposits and further lending in successive rounds. This process multiplies the initial deposit.

Credit multiplier = 1 / CRR = 1 / 0.10 = 10

Thus, with a CRR of 10%, the initial deposit can support up to ten times that amount in total money supply through successive rounds of deposit and lending.

Q11: What role of RBI is known as 'lender of last resort'?

Ans: When a commercial bank experiences a sudden shortage of funds or faces liquidity problems and is unable to obtain finance from other sources, the Reserve Bank of India acts as the lender of last resort. The RBI provides emergency credit to the troubled bank to prevent its collapse and to safeguard the stability of the banking system. This role helps prevent bank failures, protects depositors and maintains public confidence in the financial system.

Old NCERT Questions

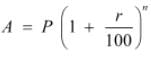

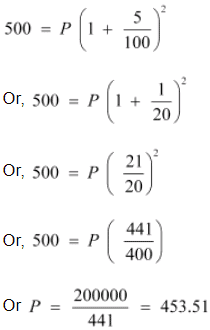

Q1: Suppose a bond promises Rs.500 at the end of two years with no intermediate return. If the rate of interest is 5 per cent per annum what is the price of the bond?

Ans: Let the price of the bond be Rs. P.

The present value formula for a single payment is:

Given:

A = Rs.500 (amount to be received after 2 years)

r = 5% = 0.05 per annum

n = 2 years

Using the present value formula:

Substituting the values:

Therefore, the price of the bond is Rs.453.51.

Q2: Why is speculative demand for money inversely related to the rate of interest?

Ans: Speculative demand for money arises because people may prefer holding money instead of bonds when they expect capital losses on bonds. The interest rate represents the opportunity cost of holding money rather than bonds. When interest rates are high, people expect them to fall in the future; lower future rates mean higher future bond prices and potential capital gains for those who buy bonds now. Hence, at high current interest rates, people convert money into bonds to gain from expected capital gains, so speculative demand for money is low. Conversely, when interest rates are low, people expect them to rise in the future, which would lower bond prices and cause capital losses for bondholders. To avoid such losses, people prefer to hold money, raising speculative demand. Thus speculative demand for money is inversely related to the rate of interest.

Q3: What is `liquidity trap'?

Ans: Liquidity trap is the situation in which the speculative demand for money becomes infinitely elastic with respect to the interest rate. In this case, the interest rate is so low (near a minimum, rmin) that everyone expects rates to rise in the future. As a result, people prefer to hold money rather than bonds to avoid capital losses from falling bond prices. Even if the central bank increases the money supply, people simply hold the extra money balances and do not buy bonds or increase spending. Therefore, monetary policy becomes ineffective in stimulating demand.

The relationship between speculative demand for money and the rate of interest is shown in the diagram:

At r = rmin the speculative demand curve is horizontal (infinitely elastic), indicating a liquidity trap.

FAQs on NCERT Solutions - Money and Banking

| 1. What is the role of money in the banking system? |  |

| 2. How do banks create money through the process of credit creation? | |

| 3. What are the functions of a central bank in the economy? | |

| 4. How do commercial banks differ from central banks in terms of their functions? | |

| 5. What are the different types of banking services offered to customers by commercial banks? | |