NCERT Numerical Questions Answers - Analysis of Financial Statements | Accountancy Class 12 - Commerce PDF Download

Q1 :

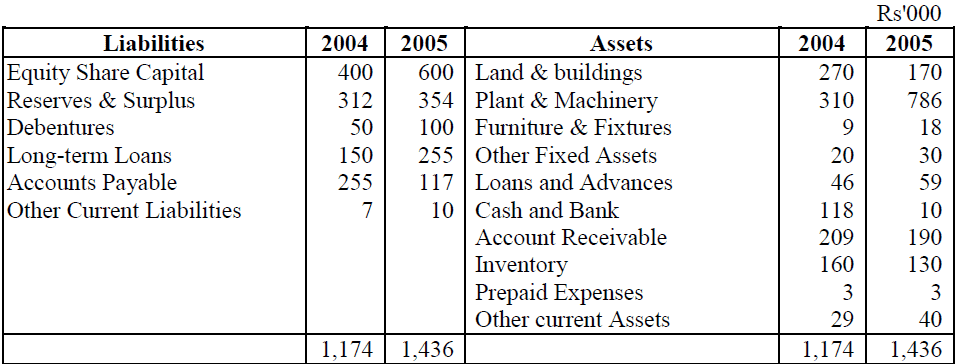

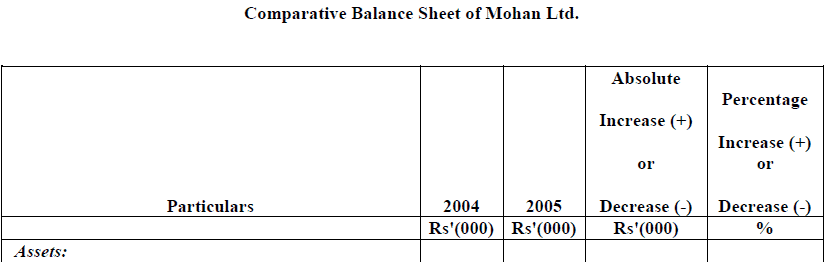

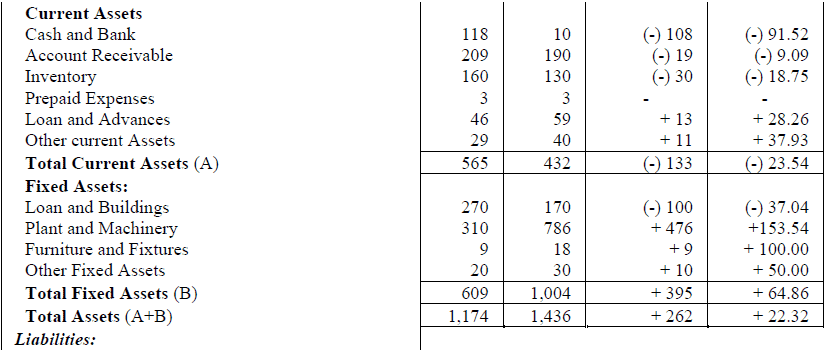

The following are the Balance Sheets of Mohan Ltd., at the end of 2004 and 2005.

Prepare a Comparative Balance Sheet and study the financial position of the company.

Answer :

Q2 :

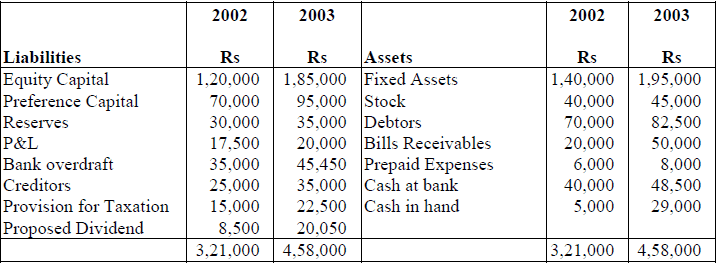

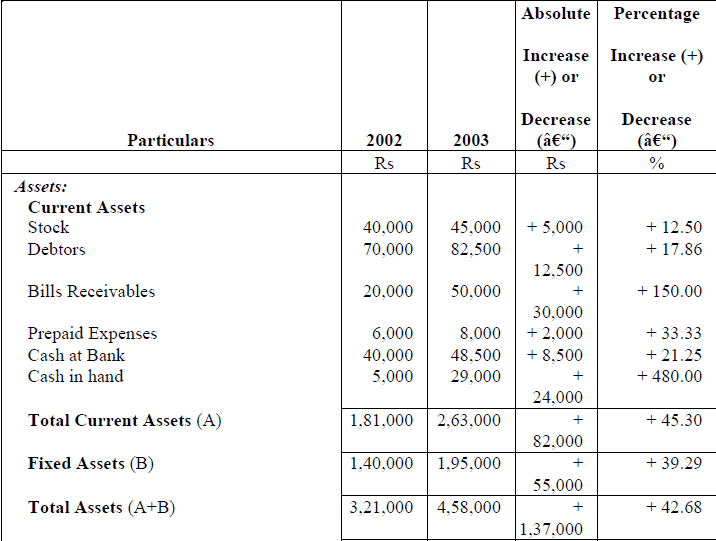

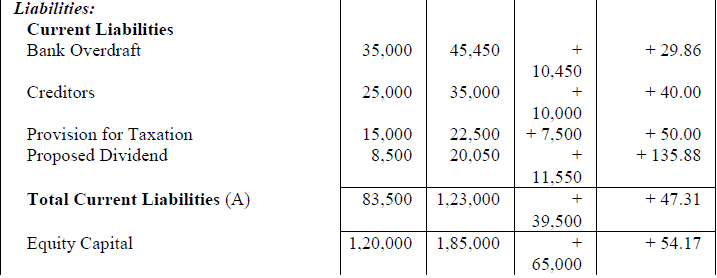

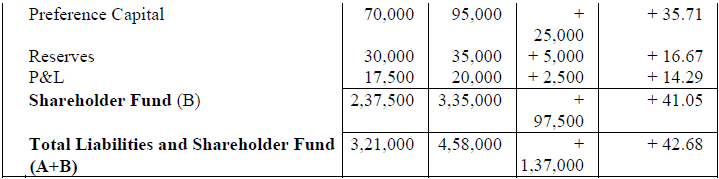

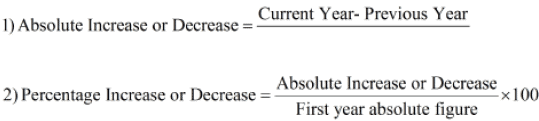

The following are the balance sheets of Devi Co. Ltd at the end of 2002 and 2003. Prepare a Comparative Balance Sheet and study the financial position of the concern.

Answer :

Comparative Balance Sheet of Devi Co Ltd.

Interpretation

1) The comparative balance sheet of a company reveals that during the year 2003, there has been an increase in fixed asset by 55,000 i.e. 39.29% while equity Capital increase by 65,000 i.e. 54.17 and preference capital increase by 25,000 i.e. 35.71. It shows that company purchase fixed assets from long term source of finance, which does not affect the working capital.

2) The current assets have increased by 82,000 i.e. 42.30% and current liabilities have increased by 39,500 i.e. 47.31. It shows ratio between current assets and current liabilities more or less should be same compare to previous year.

3) The overall financial position of a company is satisfactory.

Working Notes

Q3 :

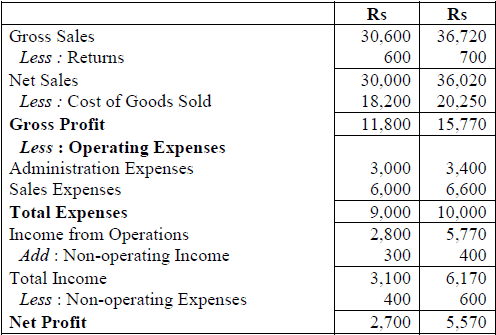

Convert the following Income Statement into Common Size Statement and interpret the changes in 2005 in the light of the conditions in 2004.

Answer :

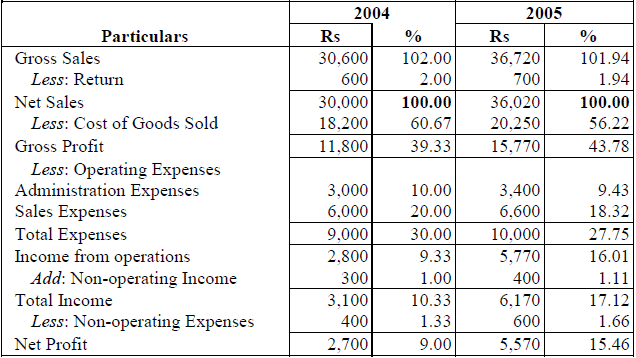

Common Size Income Statement

Interpretation:

1) The Net Profit of the company increased from 9% to 15.46 % as the income from operations has increased from 9.15% to 15.71%.

2) Simultaneously the company has tried to reduce its costs to improve its profit margin.

3) Profitability of the company has improved over the year.

Q4 :

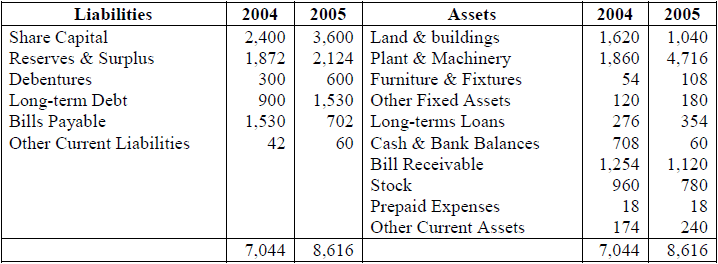

Following are the balance sheets of Reddy Ltd. as on 31 March 2003 and 2004.

Analyse the financial position of the company with the help of the Common Size Balance Sheet.

Answer :

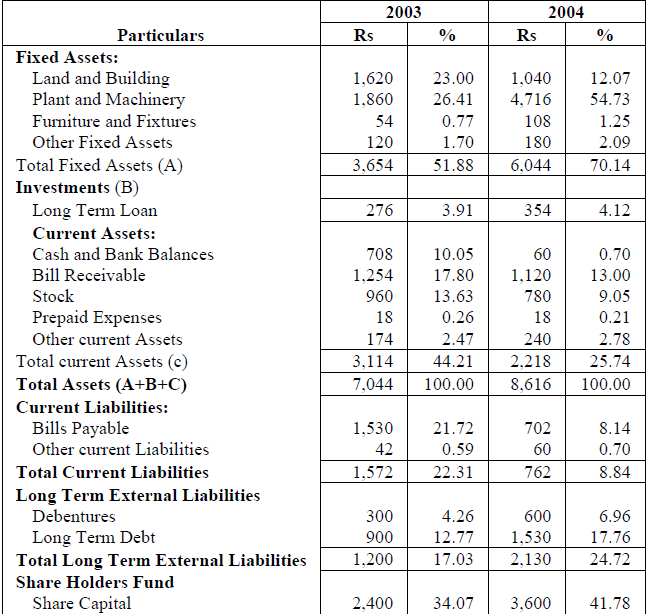

Common Size Balance Sheet of Reddy Ltd. as on March 31, 2003 and 2004

Interpretation:

1) The Current Assets has decreased from 44.21% to 25.74% i.e. by 18.47% and the Current Liabilities has reduced from 22.31% to 8.84% i.e. by 13.47%. Despite the decrease in the Current Assets and the decrease in the Current Liabilities, the Current Ratio has improved.

2) Fixed Assets, Long term External Debts and the Share Capital have increased from 51.88% to 70.14%, 17.03% to 24.72%, 34.07% to 41.78% respectively. Thus from this, it can be inferred that the company had purchased fixed assets from long-term source of finance. As the fixed assets were financed through the long-term debts, so the company's working capital remained unaffected.

3) Analysing the reducing figures of the Cash and Bank Balances, it can be inferred that the company has a poor cash management policy. Thus we can predict that the company may face an acute liquidity problem.

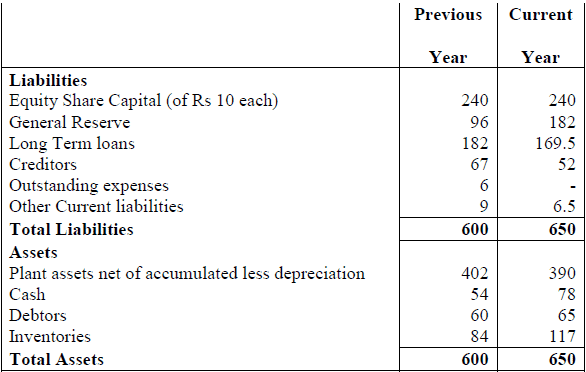

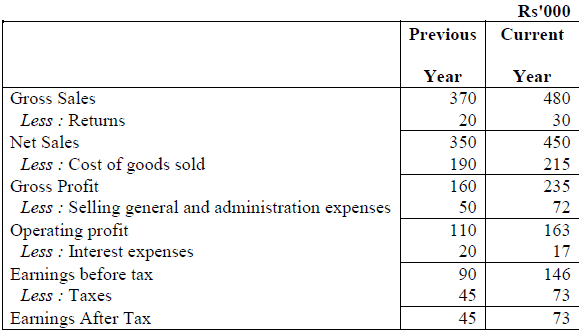

Q5 :

The accompanying balance sheet and profit and loss account related to SUMO Logistics Pvt. Ltd. Convert these into Common Size Statements.

Previous Year = 2005, Current Year = 2006

Income Statement for the year ended

Answer :

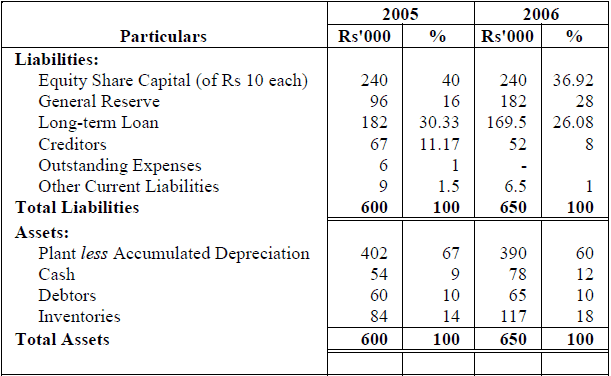

Common Size Balance Sheet of SUMO Logistics Pvt. Ltd. As on 2005 and 2006

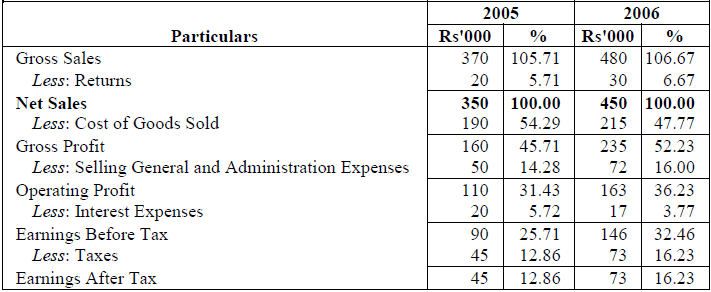

Common Size Income Statement of SUMO Logistics Pvt. Ltd.

For the year ended 2005 and 2006

|

42 videos|199 docs|43 tests

|

FAQs on NCERT Numerical Questions Answers - Analysis of Financial Statements - Accountancy Class 12 - Commerce

| 1. What is the importance of analyzing financial statements in commerce? |  |

| 2. What are the different types of financial statements that are analyzed in commerce? | |

| 3. How can ratio analysis be used to analyze financial statements in commerce? | |

| 4. What are the limitations of financial statement analysis in commerce? | |

| 5. How can a company improve its financial position through financial statement analysis in commerce? | |

Important questions

,ppt

,shortcuts and tricks

,Free

,Extra Questions

,NCERT Numerical Questions Answers - Analysis of Financial Statements | Accountancy Class 12 - Commerce

,practice quizzes

,past year papers

,Objective type Questions

,Semester Notes

,Summary

,Exam

,NCERT Numerical Questions Answers - Analysis of Financial Statements | Accountancy Class 12 - Commerce

,study material

,MCQs

,video lectures

,Sample Paper

,NCERT Numerical Questions Answers - Analysis of Financial Statements | Accountancy Class 12 - Commerce

,Previous Year Questions with Solutions

,mock tests for examination

,Viva Questions

;

NCERT Numerical Questions Answers - Analysis of Financial Statements Free PDF Download

Importance of NCERT Numerical Questions Answers - Analysis of Financial Statements

NCERT Numerical Questions Answers - Analysis of Financial Statements Notes

NCERT Numerical Questions Answers - Analysis of Financial Statements Commerce

Study NCERT Numerical Questions Answers - Analysis of Financial Statements on the App

|

© EduRev

|

Education Revolution

|

|