Key Concepts: Money & Credit

Money as a Medium of Exchange

Money is anything that is commonly accepted as a medium of exchange and in the discharge of debts.

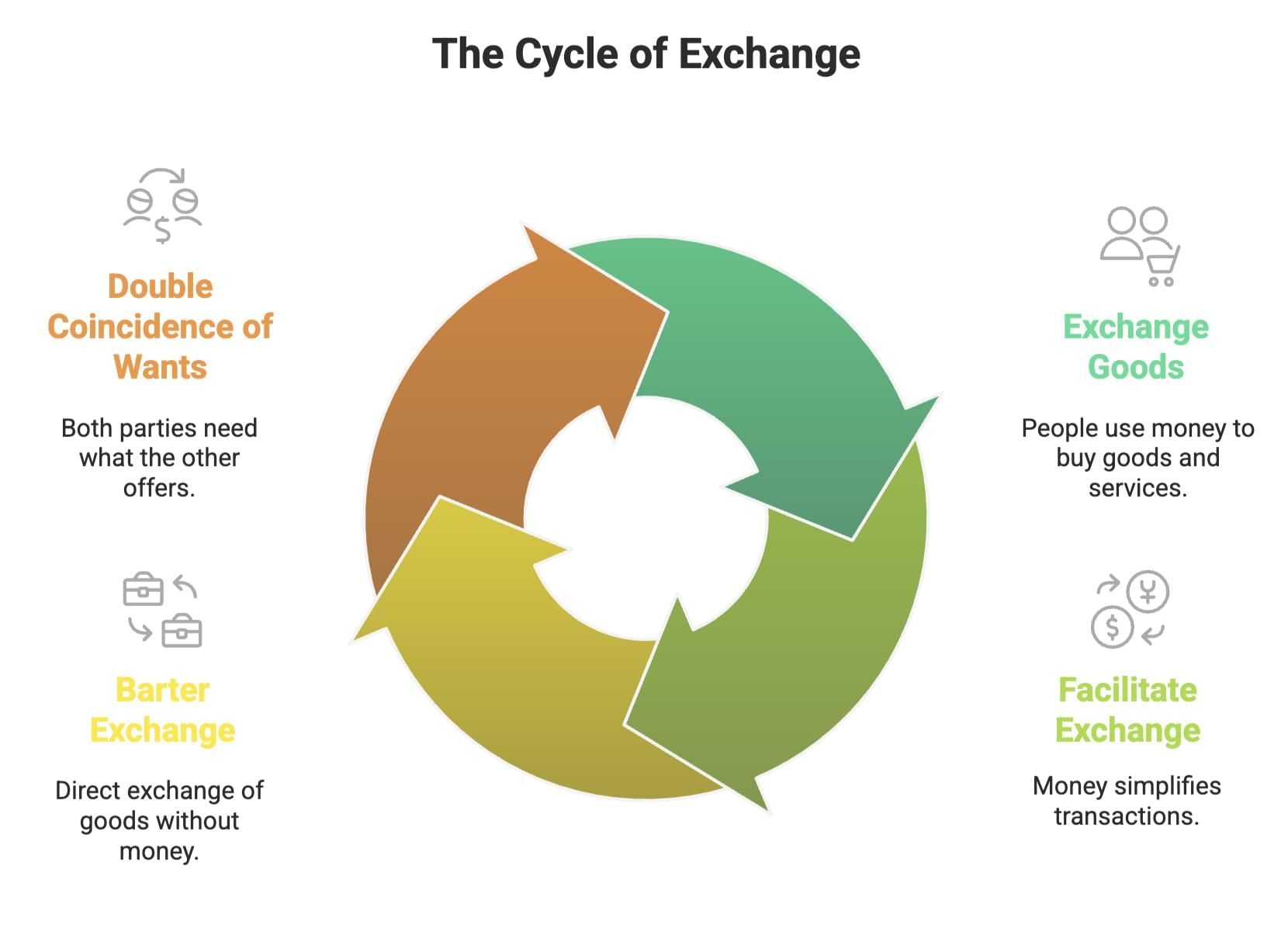

- People exchange goods and services through the medium of money. Money by itself has no physical utility like food or clothing; it acts as an intermediary that facilitates exchange by overcoming the limitations of direct barter.

- Barter exchange is the direct exchange of goods for goods (commodity for commodity), without the use of money.

- Barter requires the double coincidence of wants, that is, each party must have what the other wants and be willing to exchange at the same time.

Example: A shoe manufacturer wants to sell his shoes in the market and buy wheat. Now he has to exchange shoes for wheat without the use of money directly. He would have to look for a wheat-growing farmer who not only wants to sell wheat but also wants to buy shoes in exchange. - Because the double coincidence of wants is difficult to achieve widely and consistently, societies moved from barter to the use of commonly accepted objects as money to simplify transactions.

Forms of Money

Money has taken several forms through history as societies evolved and trade expanded. Each form improved the ease and safety of transactions.

- In early times many societies used commodity money such as grains and cattle.

- Later people began to use metallic coins made of gold, silver and copper. Coins brought uniformity and portability compared with commodity money.

- With growing trade, paper money (currency notes) was introduced. Paper notes are lighter and easier to carry than coins for large-value transactions.

- As transaction volumes expanded further, paper money also began to be inconvenient for large or frequent transactions. This led to the development of bank money represented by cheques, demand drafts, debit and credit cards, and electronic transfers.

- Today, electronic payments and digital banking (for example, mobile banking, online transfers and payment systems) are important forms of bank money that allow direct settlement without physical cash.

Characteristics and Functions of Money

For a commodity or object to serve as money it must have certain characteristics and perform important functions in the economy.

- Acceptability: People must be willing to accept it in exchange for goods and services.

- Durability: It should not perish easily so it can be used repeatedly.

- Portability: It should be easy to carry for transactions.

- Divisibility: It must be divisible into smaller units to facilitate transactions of different sizes.

- Limited supply: Its supply should be controlled to maintain value.

- Uniformity: Units of money should be identical so they are accepted at the same value.

- Primary functions of money are: medium of exchange, unit of account (a common measure for valuing goods and services), store of value (preserving purchasing power over time).

Banks and their Main Functions

Banks play a central role in the modern economy by accepting deposits, offering payment facilities and providing credit.

- The major function of a bank is to give loans, particularly to businessmen and entrepreneurs, and thereby earn interest.

- Banks obtain funds to provide loans by accepting deposits from the public. Deposits are the lifeline of a bank.

- There are two main kinds of deposits: demand deposits and time deposits.

Demand deposits can be withdrawn at any time (for example, by issuing a cheque). Time deposits can be withdrawn only after a specified period. - The facility of cheques and other payment instruments against demand deposits makes it possible to settle payments directly without using cash.

- Other important functions of banks include: accepting savings and fixed deposits, providing services to transfer money, acting as agents for collection and payment, and creating credit in the economy through lending.

- The Reserve Bank of India (RBI) supervises and regulates the functioning of banks in order to maintain financial stability and protect depositors.

Credit

Credit refers to an agreement in which the lender supplies the borrower with money, goods or services in return for the promise of future payments, usually with interest. Credit makes it possible for production and consumption to continue even when current funds are insufficient.

- Credit helps businesses and individuals meet ongoing expenses, complete production, purchase inputs and expand activities.

Example: Saleem obtains loans to meet the needs of production. The credit helps him to meet the need of ongoing expenses of production, complete production in time, and thereby increase his earnings. - However, credit can also push borrowers into a debt trap when they are unable to repay loans.

Example: Swapana, a farmer, could not repay loans because of crop failure; this made recovery painful and created hardship. - Terms of credit include the interest rate, collateral requirements, documentation requirements and the mode and schedule of repayment. These terms vary with the nature of the lender and borrower.

- Collateral is an asset that the borrower owns (such as land, buildings, vehicles or livestock) which is offered as security to the lender until the loan is repaid. If the borrower fails to repay, the lender can seize the collateral according to agreed terms.

Sources of Credit: Formal and Informal

Borrowers in India obtain credit from a mix of formal and informal sources. The choice affects the cost of borrowing, the security of the borrower and legal protections.

- Formal sources include banks and cooperative societies. These institutions generally charge lower rates of interest and follow regulated procedures. They are supervised by the Reserve Bank of India (RBI).

- Informal sources include moneylenders, traders, employers, relatives and friends. Informal lenders often charge much higher interest rates and there is no formal regulator to prevent unfair or coercive recovery methods.

- Because formal sources offer lower interest rates and legal protection, policies and programmes often aim to expand formal credit to poorer sections of society and to small producers.

Self-Help Groups

Self-Help Groups (SHGs) are an important institutional response to provide small savings and credit facilities to the rural poor.

- The idea is to organise the rural poor into small groups that pool their savings. Typical saving per member varies from around Rs 25 to Rs 100 or more, depending on the member's ability to save.

- Members can take small loans from the group itself at lower interest rates to meet household or production needs.

- If an SHG keeps regular savings and maintains discipline, it becomes eligible to obtain loans from banks, thereby linking group members to formal credit sources.

- SHGs also encourage financial discipline, mutual support and collective decision-making, reducing dependence on high-cost informal lenders.

FAQs on Key Concepts: Money & Credit

| 1. What is the difference between money and credit? |  |

| 2. How does credit affect the economy? | |

| 3. What are the advantages of using credit? | |

| 4. What are the risks associated with borrowing on credit? | |

| 5. How can individuals manage their credit effectively? | |