NCERT Solution - Introduction to Accounting

Short Question Answers

Q1: Define accounting.

Ans: Accounting is the organised process of identifying financial events, recording them in the journal, classifying them into their respective ledger accounts, summarising the results in the Profit and Loss Account and the Balance Sheet, and communicating the outcomes to users such as owners, government, creditors and investors. According to the American Institute of Certified Accountants (1941), "Accounting is an art of recording, classifying and summarising in a significant manner and in terms of money transactions and events that are, in part at least, of a financial character and interpreting the results thereof."

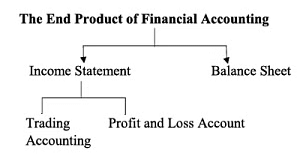

Q2: State what is end product of financial accounting?

Ans:

- Income statements (Trading and/or Profit and Loss Account) - These statements show the results of operations for an accounting period by presenting revenues and expenses and thereby ascertaining gross and net profit or loss. They help users to judge operating performance and profitability.

- Balance Sheet - This shows the financial position of the business at a given date by listing assets and liabilities. It helps users to assess solvency, liquidity and the overall financial stability of the enterprise.

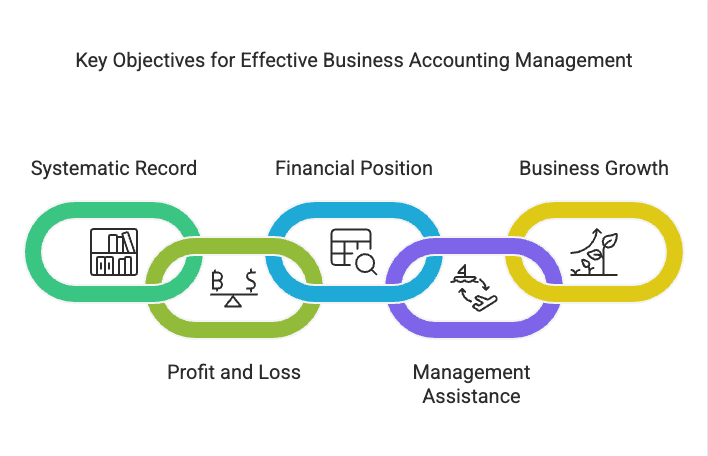

Q3: Enumerate main objectives of accounting.

Ans: The main objectives of accounting are given below.

- To keep a systematic record of all business transactions so that every event can be traced and verified.

- To determine the profit earned or loss incurred during an accounting period by preparing a Profit and Loss Account.

- To ascertain the financial position of the business at the end of each accounting period by preparing a Balance Sheet showing assets and liabilities.

- To assist management in decision-making, control, budgeting and forecasting by providing relevant financial data.

- To assess the progress and growth of the business from year to year through the comparison of results.

- To detect and prevent fraud and errors by maintaining verifiable records and internal controls.

- To communicate useful information to various users, including owners, creditors and investors.

Q4: Who are the users of accounting information?

Ans: Users of accounting information are divided into two categories: internal users and external users.

Internal Users- These are persons within an organisation who have direct access to accounting information and use it for operational and strategic purposes. Examples include:

- Owners - to evaluate business performance and changes in capital.

- Management - to plan, control and make decisions about operations and resources.

- Employees and workers - to assess job security, wage negotiations and company stability.

External Users- These are outsiders who rely on published accounting information for decision-making. They do not have direct access to internal records. Examples include:

- Banks and financial institutions - to assess creditworthiness before granting loans.

- Investors and potential investors - to evaluate profitability and growth prospects before investing.

- Creditors - to judge the firm's ability to meet its obligations.

- Tax authorities - to determine taxable income and ensure compliance.

- Government - to monitor industry performance and formulate policy.

- Consumers - to check the stability of suppliers and product continuity.

- Researchers - to study trends and perform economic analysis.

- Public - to understand an organisation's economic contribution and accountability.

Q5: State the nature of accounting information required by long-term lenders.

Ans: Long-term lenders require information that helps them judge a borrower's ability to meet long-term obligations. This includes the firm's repaying capacity, profitability, liquidity, operational efficiency and future growth prospects. Lenders look for stable earnings, adequate cash flows, strong asset backing and prudent financial policies.

Q6: Who are the external users of information?

Ans: External users are individuals or organisations outside the firm who have an interest in its financial affairs but do not manage the business. They rely on published reports such as financial statements and annual reports. Typical external users are the government, tax authorities, banks, creditors, investors, labour unions, researchers and the general public. Each needs accounting information for decisions like lending, investing, taxation and policy formulation.

Q7: Enumerate the informational needs of management.

Ans: The informational needs of management include:

- Assisting in short-term and long-term decision-making and business planning by providing timely financial data.

- Preparing reports on funds, costs and profits to check financial soundness and control expenditures.

- Comparing current financial results with past performance and with competitors to assess operational efficiency and identify areas for improvement.

Q8: Give three examples of revenues.

Ans: Three examples of revenue are given below.

- Sales revenue

- Interest received

- Dividends received

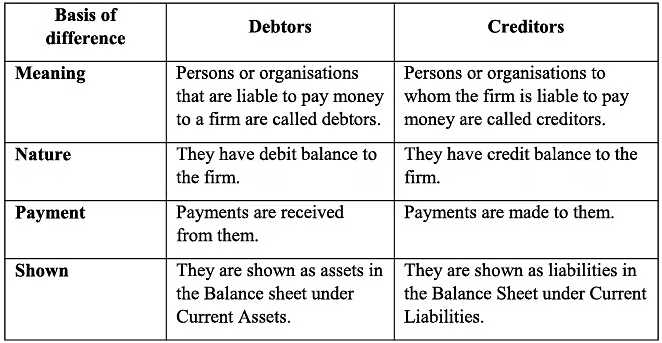

Q9: Distinguish between debtors and creditors; Profit and Gain.

Ans:

Difference between Debtors and Creditors is given below.

The difference between Profit and Gain is given below.

- Gain - Gain arises from incidental or non-recurring transactions that are not part of ordinary business operations, for example, profit on sale of fixed assets or appreciation in the value of an asset.

- Profit - Profit is the excess of revenue over expenses from regular business activities. It may be gross or net profit and is normally added to the owner's capital at the end of the accounting period.

Q10: 'Accounting information should be comparable'. Do you agree with this statement? Give two reasons.

Ans: I agree. Comparable accounting information is important because:

- It enables inter-firm comparisons, allowing users to evaluate the relative performance and policies of different companies operating in the same industry.

- It facilitates intra-firm comparisons across different accounting periods, helping management to identify trends, measure growth and judge the effectiveness of policies over time.

Q11: If the accounting information is not clearly presented, which of the qualitative characteristics of the accounting information is violated?

Ans: If accounting information is not clearly presented, the qualitative characteristics of understandability, reliability and comparability are violated. Lack of clarity makes information hard to interpret, reduces confidence in its accuracy and prevents meaningful comparisons across periods or with other firms.

Q12: "The role of accounting has changed over the period of time" - Do you agree? Explain.

Ans: Yes, the role of accounting has changed. Earlier, accounting was mainly concerned with record-keeping. Today it provides a comprehensive information system that not only records transactions but also supplies relevant data for decision-making, planning, forecasting and performance evaluation. This change has been driven by a more complex and competitive business environment, which requires managers and external users to rely on accounting information for strategic and operational choices.

Q13: Giving examples, explain each of the following accounting terms:

- Fixed assets

- Revenue

- Expenses

- Short-term liability

- Capital

Ans:

- Fixed assets: Assets held for long-term use in the business that increase its earning capacity and are not intended for sale, for example, land, buildings and machinery.

- Revenue: Income arising from the ordinary activities of the business, such as sales of goods or services; also includes regular receipts like rent, commission and interest.

- Capital: The amount invested by the owner in the business, either in cash or in kind; it is a liability of the business to the owner.

- Expenses: Costs incurred in earning revenue, such as wages, rent, depreciation and interest; these reduce profit and are shown on the debit side of the trading or profit and loss account.

- Short-term liabilities: Obligations payable within one year, for example, creditors, bills payable, outstanding wages and short-term bank loans.

Q14: Define revenues and expenses.

Ans:

Revenues: Revenues are amounts earned from the day-to-day operations of the business, such as proceeds from sales and fees for services. Regular receipts like rent, commission, royalties and interest are treated as revenue and are shown on the credit side of the income statement.

Expenses: Expenses are the costs incurred to earn revenue and to run the business, such as wages, rent and utilities. They are shown on the debit side of the income statement and reduce the profit of the period.

Q15: What is the primary reason for business students and others to familiarise themselves with the accounting discipline?

Ans: Business students and others should familiarise themselves with accounting because it provides a systematic way to record, summarise and interpret economic transactions so all users can understand financial results. Specifically:

- It helps in studying various aspects of accounting theory and practice.

- It enables learning how to maintain books of accounts accurately.

- It facilitates summarising accounting data into meaningful reports.

- It aids in interpreting financial information to support decision-making.

Long Question Answers

Q1: Define accounting.

Ans: Accounting is the systematic process of identifying financial events, recording them in the journal, classifying them in appropriate accounts, summarising the results in the Profit and Loss Account and the Balance Sheet, and communicating the information to users such as owners, creditors, investors and government. According to the American Institute of Certified Accountants (1941), "Accounting is the art of recording, classifying and summarising in a significant manner and in terms of money, transactions and events that are, in part at least, of financial character and interpreting the results thereof." In 1970, the definition was refined to state that accounting provides quantitative information, primarily financial in nature, about economic entities intended to be useful in making economic decisions.

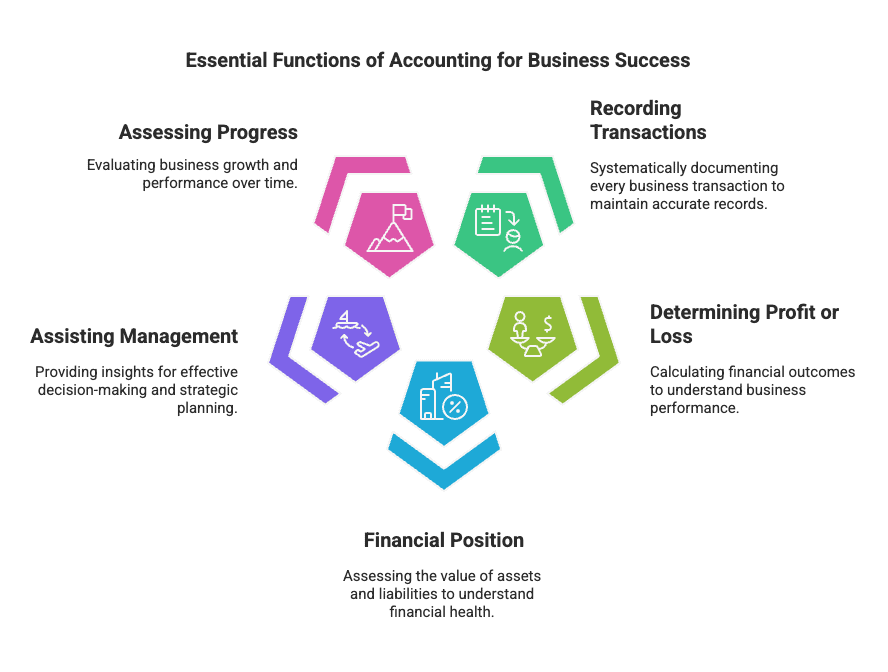

Objectives of Accounting:

- Recording business transactions systematically - Maintain complete and orderly records of each transaction so that details can be verified and audited when required.

- Determining profit earned or loss incurred - Prepare Trading and Profit and Loss Accounts to find gross and net profit or loss for the accounting period, showing revenue, costs and expenses.

- Ascertaining the financial position of the firm - Prepare the Balance Sheet to show assets, liabilities and owner's equity so the owner can see the net worth of the business.

- Assisting management - Supply timely and relevant data to help management make decisions, control operations, prepare budgets and forecast future needs.

- Assessing the progress of the business - Enable inter-period and inter-firm comparisons to judge growth, efficiency and the success of policies.

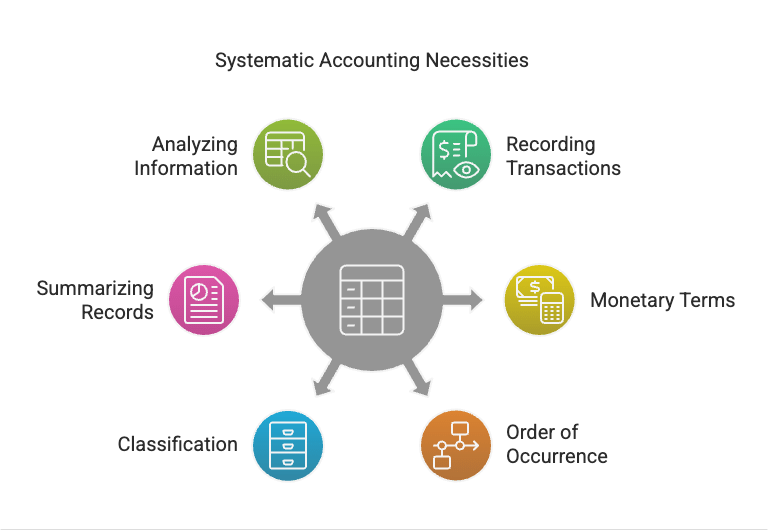

Q2: Explain the factors that necessitated systematic accounting.

Ans: The need for systematic accounting arises from several factors:

- Recording only financial transactions - Only monetary events are recorded; non-monetary facts such as a person's qualifications are not included.

- Transactions recorded in monetary terms - Only those transactions that can be expressed in monetary terms are recorded in the books. For example, if a business has two buildings and four machines, then their economic values are recorded in the books, i.e., buildings costing Rs 2,00,000, four machines costing Rs 8,00,000. Therefore, the total value of assets is Rs 10,00,000.

- The art of recording - Transactions are recorded in chronological order to maintain an accurate history of business events.

- Classification of transactions - Similar transactions are grouped together in accounts (e.g., all machinery transactions in a Machinery Account) to provide clarity.

- Summarising records - Records are summarised in the Trial Balance, Trading Account, Profit and Loss Account and Balance Sheet to present concise information to users.

- Analysing and interpreting information - Systematic accounting enables analysis and interpretation using ratios, trends and charts to support decision-making and forecasting.

Q3: Describe the informational needs of external users.

Ans: External users require accounting information for different purposes:

- Banks and other financial institutions - Need information on liquidity, profitability and solvency to decide whether to grant loans and on what terms.

- Lenders (creditors) - Require details about the firm's short-term liquidity and cash flows to judge ability to repay trade credit.

- Investors and potential investors - Seek information on profitability, dividends and growth prospects to make investment decisions.

- Tax authorities - Use accounting records to determine taxable income and ensure correct tax compliance.

- Government - Relies on aggregate accounting data for policy-making, estimating national income and monitoring industrial growth.

- Researchers - Use accounting data for economic and market research, credit ratings and industry studies.

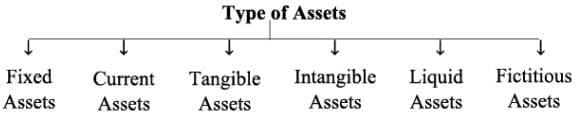

Q4: What do you mean by an asset, and what are the different types of assets?

Ans: An asset is any resource owned by a business that has economic value and from which future benefits are expected. Types of assets include:

- Fixed assets - Long-term assets used in operations and not held for sale, e.g., land, buildings and machinery.

- Current assets - Assets convertible into cash within a year, e.g., cash, debtors and inventory.

- Tangible assets - Physical assets that can be seen and touched, e.g., vehicles and furniture.

- Intangible assets - Non-physical assets such as goodwill, patents and trademarks.

- Liquid assets - Highly convertible assets like cash, bank balances and marketable securities.

- Fictitious assets - These are the heavy revenue expenses, the benefit of which can be derived over multiple years. They represent losses or expenses that are written off over a period of time, e.g., if the promotional expenditure is Rs 1,00,000 for five years, then every year Rs. 20,000 will be written off.

Q5: Explain the meaning of gain and profit. Distinguish between these two terms.

Ans:

Profit: Profit is the excess of revenue over expenses arising from ordinary business activities. It is typically classified as gross profit or net profit and increases the owner's capital when retained. Example: selling goods for Rs. 1,20,000 that cost Rs. 1,00,000 yields a profit of Rs. 20,000.

Gain: Gain arises from incidental or non-recurring transactions that are not part of usual operations, such as selling old machinery above its book value. Example: selling old machinery with a book value of Rs. 20,000 for Rs. 25,000 gives a gain of Rs. 5,000. In short, profit relates to operating results; gain arises from peripheral or extraordinary events.

Q6: Explain the qualitative characteristics of accounting information.

Ans:  The following are the qualitative characteristics of accounting information:

The following are the qualitative characteristics of accounting information:

- Reliability: Information should be free from material error and bias and should be verifiable from source documents like invoices and receipts, so users can depend on it.

- Relevance: Information must be useful for decision-making; it should have predictive and confirmatory value and avoid immaterial details.

- Understandability: Financial information should be presented clearly so users with reasonable knowledge can comprehend it without undue effort.

- Comparability: Information should be prepared consistently so users can compare financial data across periods and between firms to assess performance and trends.

Q7: Describe the role of accounting in the modern world.

Ans: Accounting today performs several vital roles beyond record keeping:

- Supporting management: Provides data for planning, budgeting, forecasting and control to help managers make informed decisions.

- Comparative analysis: Enables comparison of current performance with past periods and with competitors to assess strengths and weaknesses.

- Memory substitute: Serves as a reliable record of past transactions that cannot be remembered in detail by individuals.

- Information to end users: Supplies relevant and reliable financial information to owners, investors, creditors, regulators and other stakeholders for decision-making.

FAQs on NCERT Solution - Introduction to Accounting

| 1. What are the main principles of accounting and why do they matter for SSC CGL exams? |  |

| 2. How do debit and credit rules work differently for assets, liabilities, and capital? | |

| 3. What's the difference between capital and revenue expenditure, and why do examiners ask about this? | |

| 4. Can you explain the accounting equation and how it stays balanced in every transaction? | |

| 5. What are the key differences between NCERT accounting concepts and what actually appears in SSC CGL Tier 2 papers? | |