NCERT Solution - Recording of Transactions-II

Short Question Answers

Q1: Briefly state how the cash book is both a journal and a ledger.

Ans: A cash book is a journal because it records cash receipts and cash payments in chronological order directly from source documents. It is also a ledger because it contains separate columns (for example, cash and bank) whose balances are final and need not be posted again to separate cash and bank ledger accounts. Thus, the cash book performs the functions of both a journal and a ledger.

Q2: What is the purpose of contra entry?

Ans: A contra entry is made when cash and bank accounts are involved in the same transaction, for example when cash is deposited into the bank or when cash is withdrawn from the bank. In a double-column cash book, contra entries are marked by the letter "C" in the Ledger Folio (L.F.) column and are recorded on both the cash and bank sides. Contra entries transfer funds between cash and bank but do not affect the overall cash-plus-bank position of the business.

Q3: What are special purpose books?

Ans: Special purpose books (or subsidiary books) are books of prime entry used to record frequently occurring transactions of a similar nature directly, instead of recording them first in the journal. Examples include the purchases book, sales book, purchases return book, sales return book, cash book and bills book. They save time, reduce repetition and make the later posting to ledger accounts simpler and faster.

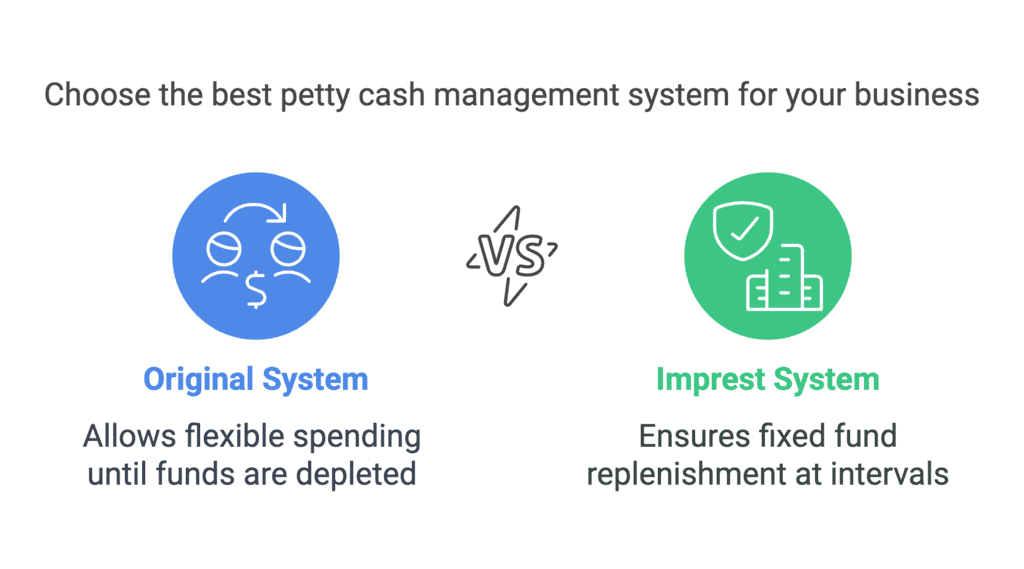

Q4: What is petty cash book? How is it prepared?

Ans: A petty cash book is a subsidiary book used to record small day-to-day expenses such as postage, stationery, conveyance, and telephone charges. It is maintained by a petty cashier who makes payments from a small cash fund kept for this purpose. There are two common systems for maintaining a petty cash book:

i. Original System: A fixed sum is given to the petty cashier. The petty cashier pays small expenses from this sum and records each payment. When the cash is exhausted, the petty cashier submits the petty cash book and is reimbursed for the amount spent.

ii. Imprest System: A fixed amount (the imprest) is given to the petty cashier at the start of the accounting period. At regular intervals, the petty cash book is checked, and the petty cashier is reimbursed only for the amount spent, so that the petty cashier always holds the fixed imprest amount. Q5: Explain the meaning of posting of journal entries?

Q5: Explain the meaning of posting of journal entries?

Ans: Posting is the process of transferring the information recorded in the journal (or subsidiary books) to the respective ledger accounts. Posting organises transactions by account so that the balance of each ledger account can be ascertained. This step is necessary to prepare the trial balance and final accounts.

Q6: Define the purpose of maintaining a subsidiary journal.

Ans: The main purposes of maintaining subsidiary (special purpose) journals are to simplify and speed up recording and to allocate responsibility. Benefits include:

- They allow specific persons to be made responsible for particular books, improving accuracy and internal control.

- They save time by recording recurring transactions (such as credit sales and credit purchases) directly in their respective books rather than recording each in the general journal.

- They improve efficiency because clerks become specialised in handling a particular type of transaction.

- They make it easier to locate and verify transactions of a particular type without searching through the general journal.

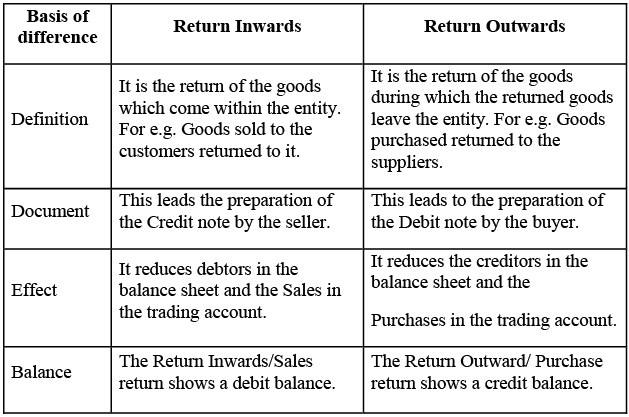

Q7: Write the difference between return inwards and return outwards.

Ans: The difference between return inwards and return outwards are as follows:

Q8: What do you understand about ledger folio?

Ans: Ledger folio (L.F.) is the reference number or page number of the ledger where a particular ledger account appears. Recording the L.F. in the journal or subsidiary book helps in easy cross-reference and quick tracing of the related ledger account entry.

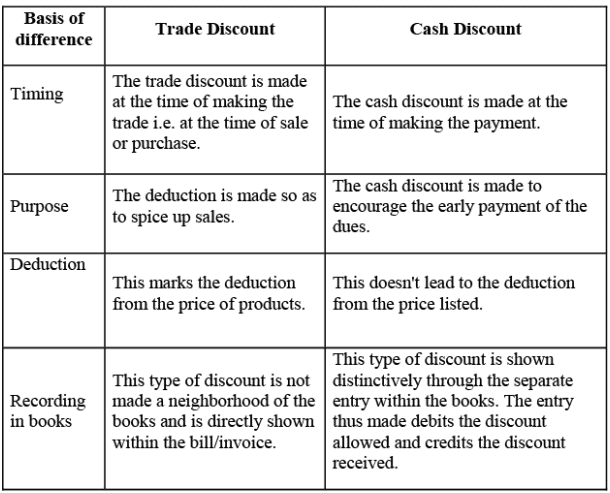

Q9: What is the difference between a trade discount and a cash discount?

Ans: The difference between trade discount and cash discount are as follows:

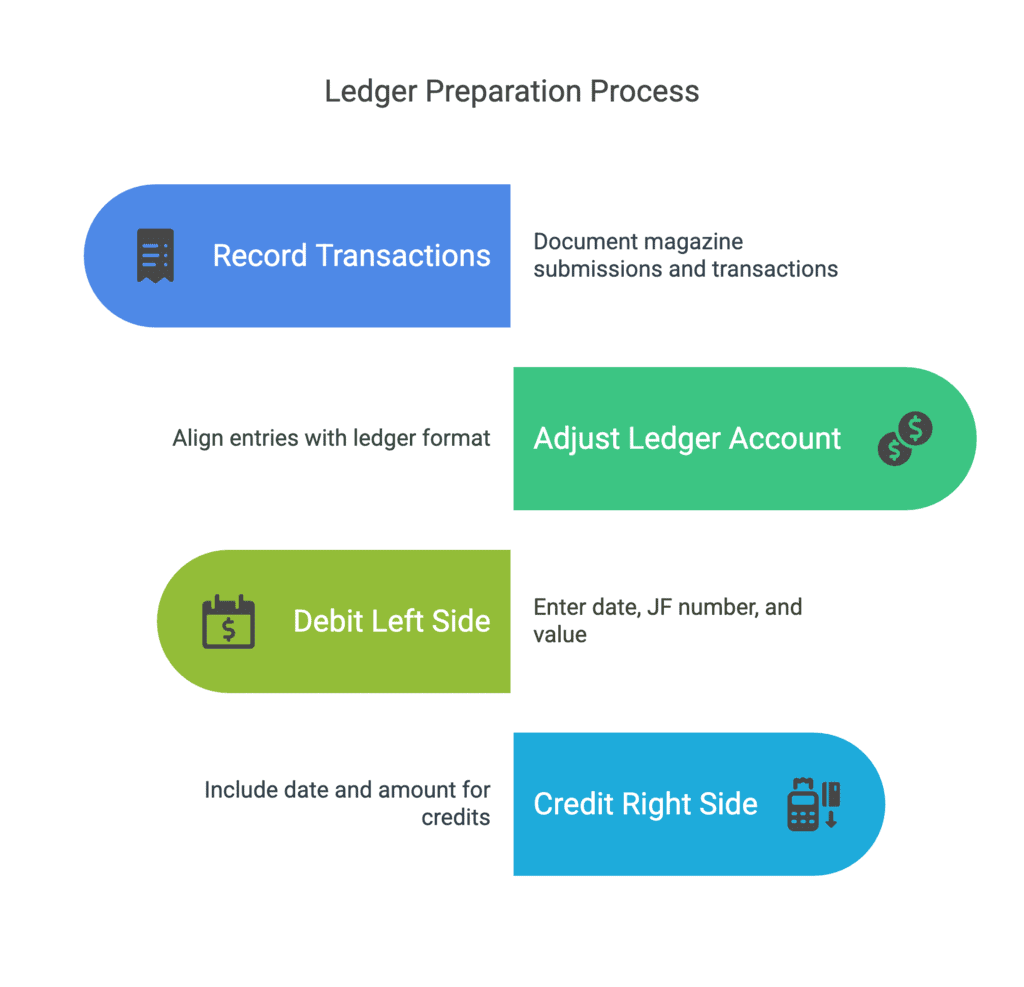

Q10: Write the process of preparing ledger from a journal.

Ans: The process of preparing ledger accounts from the journal is as follows:

- Identify each journal entry and determine which accounts are debited and credited.

- Open ledger accounts in the prescribed format showing date, particulars, JF (Journal Folio) and amount on both debit and credit sides.

- Post each debit from the journal to the debit side of the appropriate ledger account with the date, particulars (name of the other account) and amount. Enter the journal page or folio number in the JF column.

- Post each credit from the journal to the credit side of the appropriate ledger account in a similar manner.

- After all entries are posted, total and balance the ledger accounts at the end of the period.

Q11: What do you understand by the Imprest amount in a petty cash book?

Ans: The imprest amount is the fixed sum handed to the petty cashier at the start of the period under the imprest system. The petty cashier spends from this amount and is reimbursed periodically for the amount spent so that the petty cashier always holds the fixed imprest balance.

Long Question Answers

Q1: Explain the need for drawing up the special purpose books.

Ans: The following is a requirement for keeping books for a specific purpose:

- They allocate responsibility by assigning specific books to particular employees, which promotes accuracy and accountability.

- They speed up recording because repetitive transactions (such as credit sales and purchases) are recorded directly in appropriate subsidiary books.

- They increase efficiency by allowing staff to specialise in particular tasks, reducing clerical errors and saving time.

- They make it easier to extract information - for example, to find all credit purchases for a given date, one can simply consult the purchases book instead of searching the general journal.

- They simplify posting to ledgers because totals from subsidiary books can often be posted as single summary figures, reducing work.

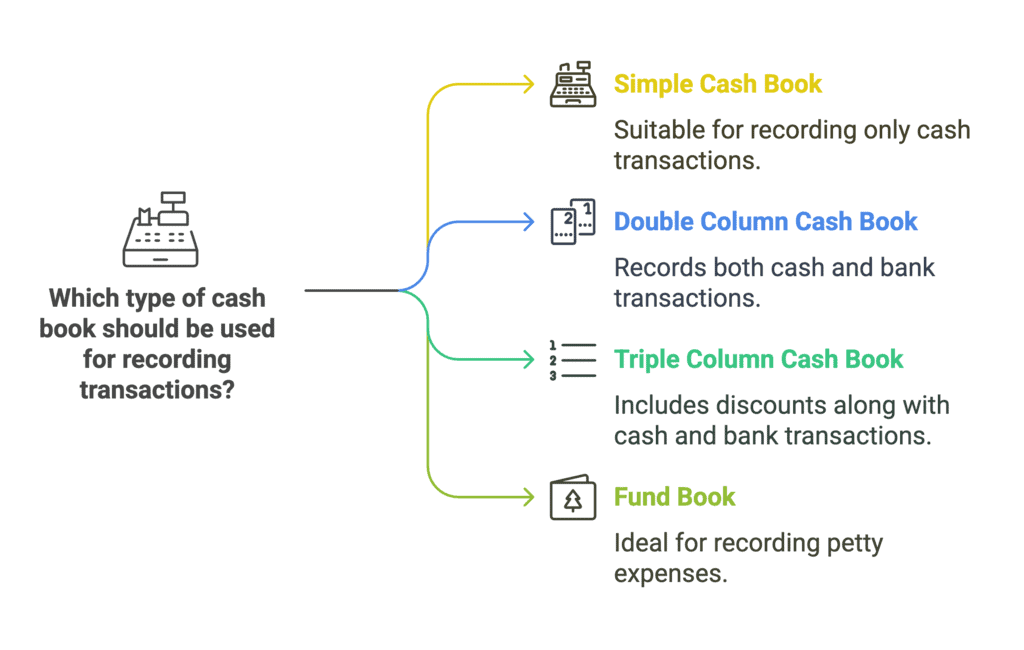

Q2: What is a cash book? Explain the types of cash book.

Ans:

A cash book is a special book of prime entry used to record all cash and bank transactions of a business. It functions both as a journal and as a ledger for cash and bank balances. The common types of cash book are:

- Simple Cash Book: Records only cash receipts and cash payments. It has a receipts side (debit) and a payments side (credit).

- Double-column Cash Book: Contains two columns on each side - usually Cash and Bank - and records transactions affecting cash and bank. It records contra entries when transfers occur between cash and bank.

- Triple-column Cash Book: Has three columns on each side - typically Cash, Bank and Discount. It records discounts allowed and received along with cash and bank transactions.

- Petty Cash Book: Used for recording small day-to-day expenses. It may be maintained under the original system or the imprest system.

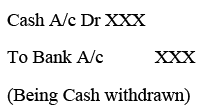

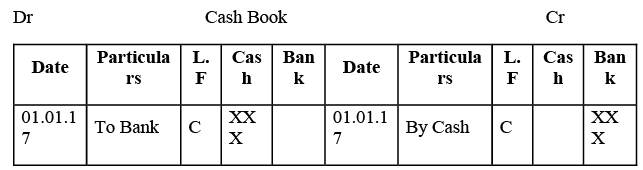

Q3: What is contra entry? How can you deal with this entry while preparing the double column cash book?

Ans: A contra entry arises when cash and bank are affected in the same transaction, for example, when cash is deposited into the bank or when cash is withdrawn from the bank. In a double-column cash book:

- A contra entry is recorded on both the cash and bank columns - once as a debit and once as a credit.

- It is indicated by the letter "C" in the Ledger Folio (L.F.) column.

- Contra entries do not change the combined cash and bank position of the business; they simply move funds between cash and bank.

The following is an example when cash is withdrawn from Bank:

This entry is illustrated in the cash book below:

Q4: What is a petty cash book? Write the advantages of a petty cash book?

Ans: A petty cash book records small expenses such as postage, stationery, conveyance and other miscellaneous payments made by a business. The petty cashier keeps this book and makes payments from the petty cash fund.

Methods of maintenance:

Original System: The petty cashier is given a sum of money and records payments until the money is exhausted; the cashier then reports and is reimbursed.

Imprest System: The petty cashier is given a fixed sum (imprest) at the start of the period. Periodically, the petty cash book is checked, and the cashier is reimbursed for the amount spent so that the imprest amount is restored.

Advantages:

- It saves time by avoiding recording numerous small transactions in the general journal.

- It exercises control over petty expenses by limiting the cash available and assigning responsibility to the petty cashier.

- It allows the chief cashier or accountant to focus on larger transactions while small expenses are handled separately.

This system thus ensures efficient and economical handling of minor payments.

Q5: Describe the advantages of subdividing the Journal.

Ans: The advantages of subdividing the journal (i.e. using subsidiary books) are:

- It creates clear responsibility by allocating specific books to different employees, which helps prevent errors and fraud.

- It saves time because recurring transactions are recorded directly in the appropriate subsidiary book instead of the general journal.

- It improves accuracy since specialised clerks become proficient in recording particular types of transactions.

- It simplifies the retrieval of information - for example, credit sales can be reviewed directly in the sales book.

Q6: What do you understand by the balancing of accounts?

Ans: Balancing an account means finding the difference between the total of the debit side and the total of the credit side and bringing forward the resulting balance to the next period. The usual steps are:

Step 1: Total the debit and credit sides of the account and identify which side has the larger total.

Step 2: Write the larger total as the grand total on the other side as well so that both sides show the same total.

Step 3: Calculate the difference between the grand total and the smaller side; write this difference as Balance c/d (carried down) on the smaller side.

Step 4: On the next accounting period, bring this down as Balance b/d (brought down) on the side that previously had the balance c/d.

Step 5: Continue posting subsequent entries below the balance b/d as the period progresses.

Numerical Question Answers

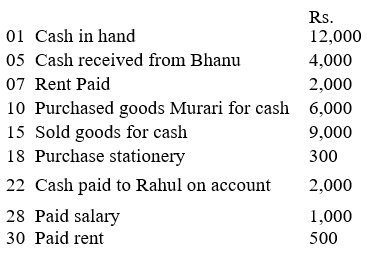

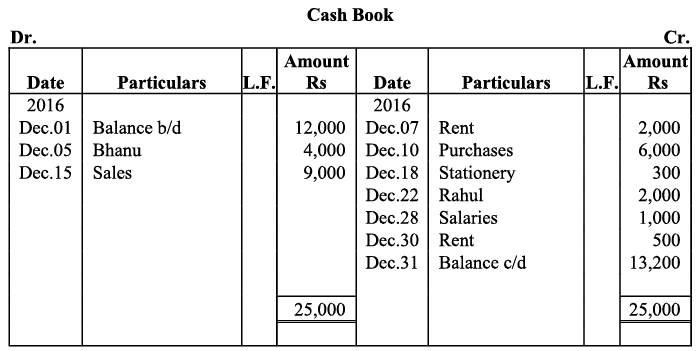

Q1: Enter the following transactions in a simple cash book for December 2016:

Ans:

Ans:

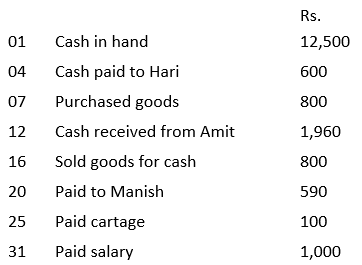

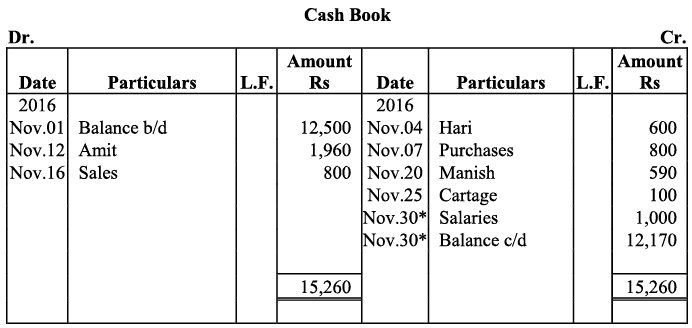

Q2: Record the following transaction in simple cash book for November 2016.

Ans:

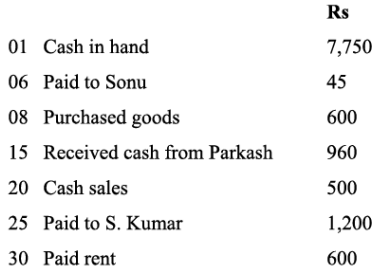

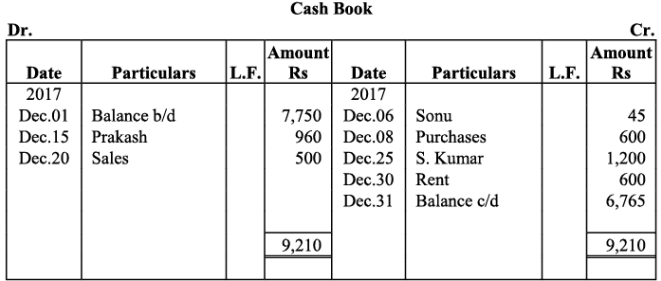

Q3: Enter the following transaction in Simple cash book for December 2017

Ans:

Ans:

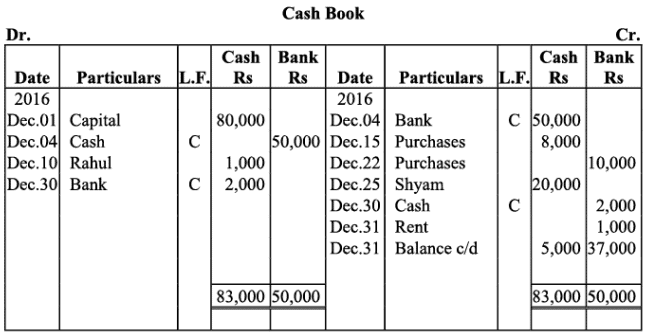

Q4: Record the following transactions in a bank column cash book for December 2016:

Ans:

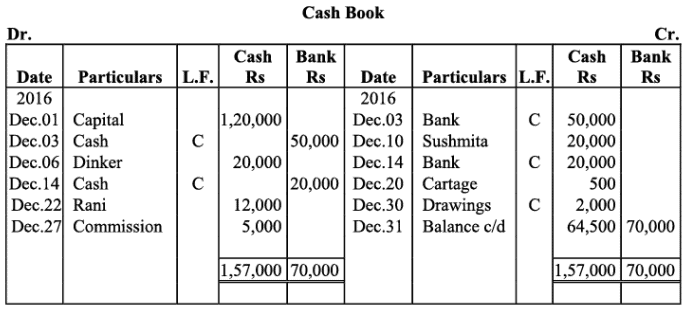

Q5: Prepare a double column cash book with the help of following information for December 2016:

Ans:

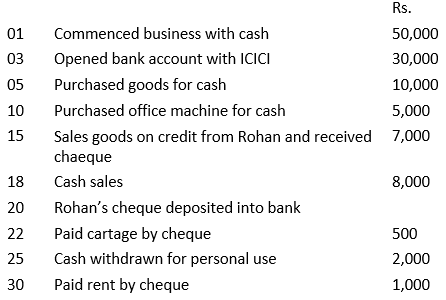

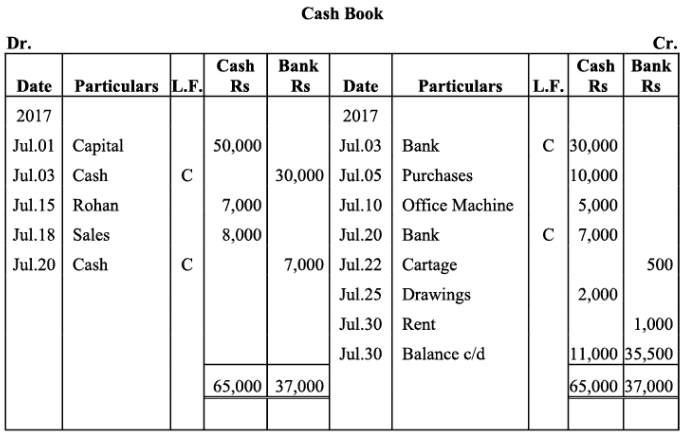

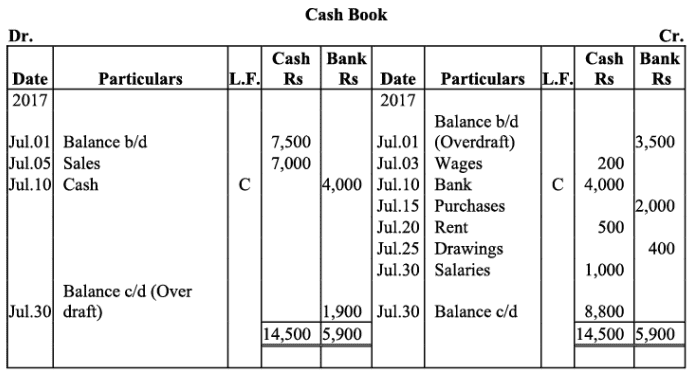

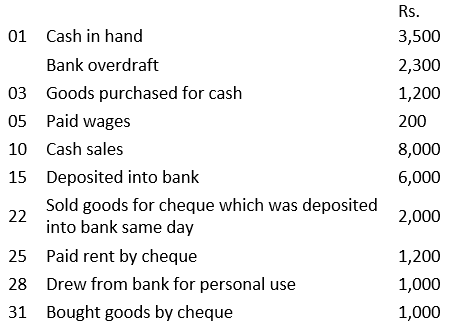

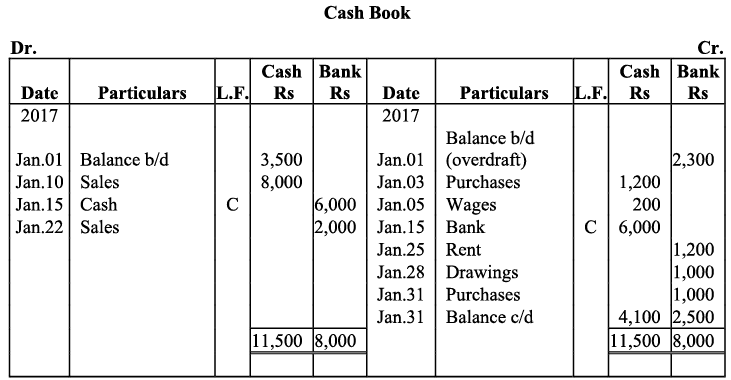

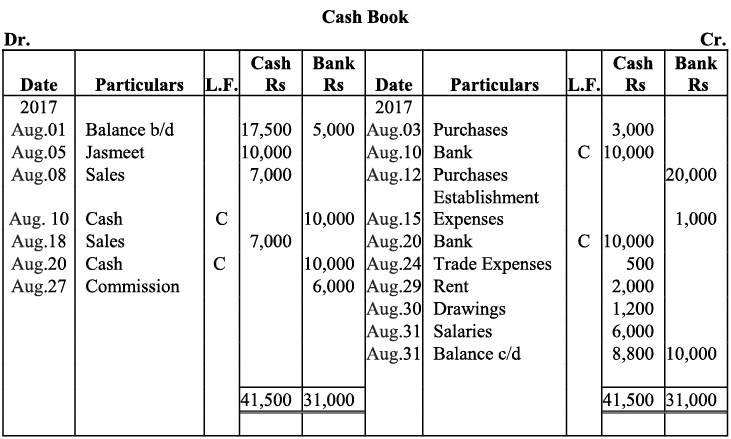

Q6: Enter the following transactions in double column cash book of M/s Ambica Traders for July 2017:

Ans: Books of M/s. Ambika Traders

Ans: Books of M/s. Ambika Traders

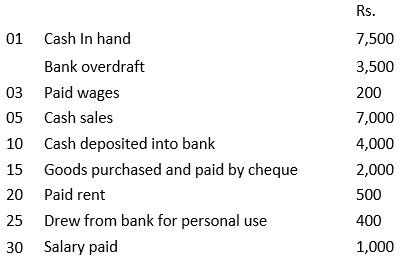

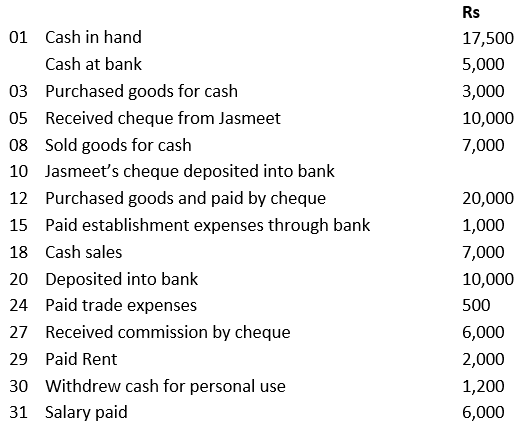

Q7: Prepare double column cash book from the following information for July 2017:

Ans: Books of M/s. Ruchi Trader

Ans: Books of M/s. Ruchi Trader

Q8: Enter the following transaction in a double column cash book of M/s.Mohit Traders for January 2017:

Ans: Books of M/s. Mohit Traders

Q9: Prepare double column cash book from the following transactions for the year August 2017: Ans:

Ans:

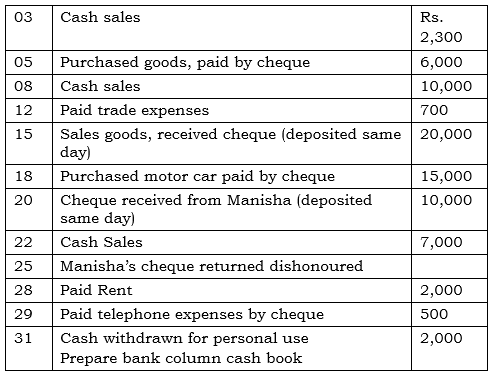

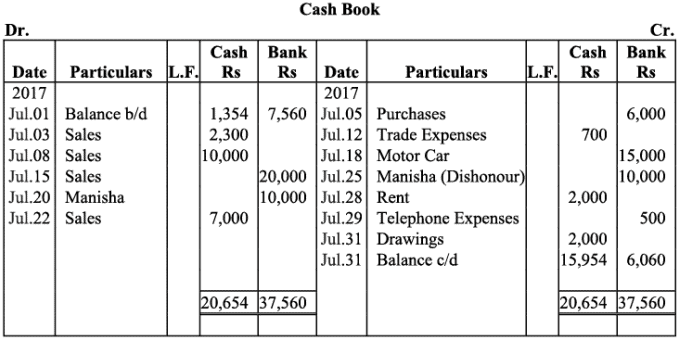

Q10: M/s Ruchi trader started their cash book with the following balances on July 2017: cash in hand ₹1,354 and balance in bank current account ₹7,560. He had the following transaction in the month of July 2017:

Ans: Books of M/s. Ruchi Trader

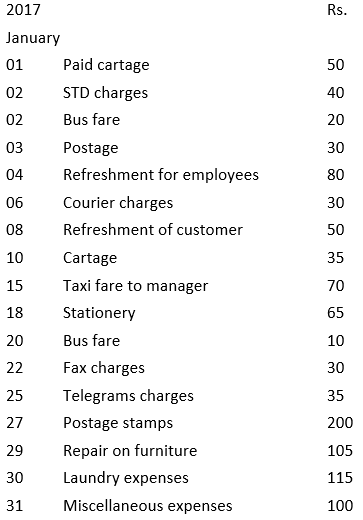

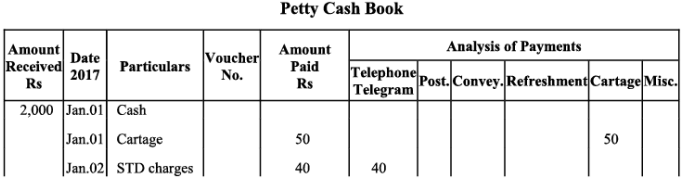

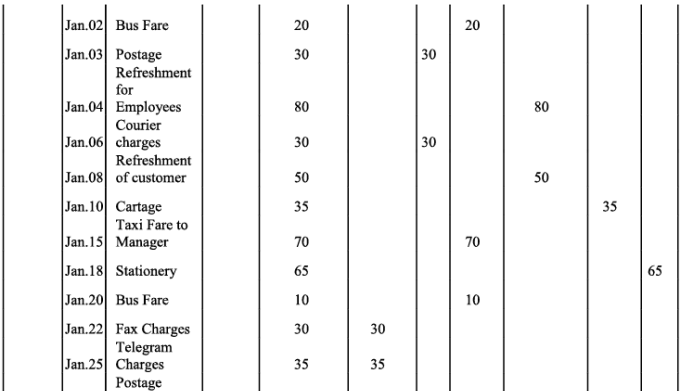

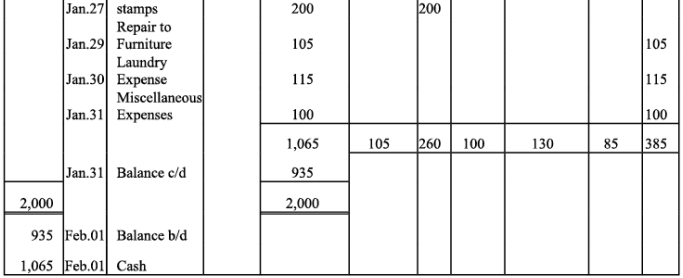

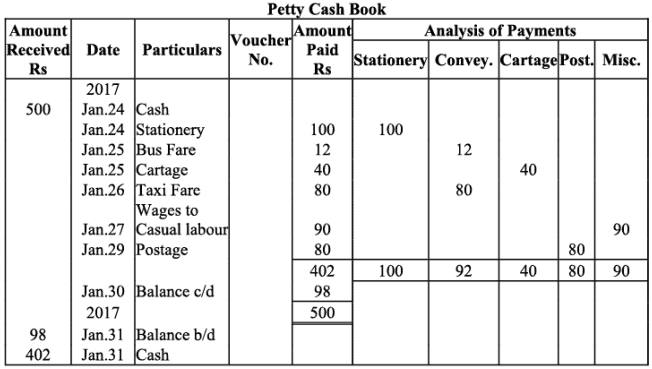

Q11: Prepare petty cash book from the following transactions. The imprest amount is ₹2,000.

Ans:

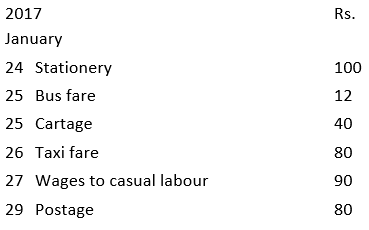

Q12: Record the following transactions during the week ending Dec.30, 2014 with a weekly imprest ₹ 500.

Ans:

Ans:

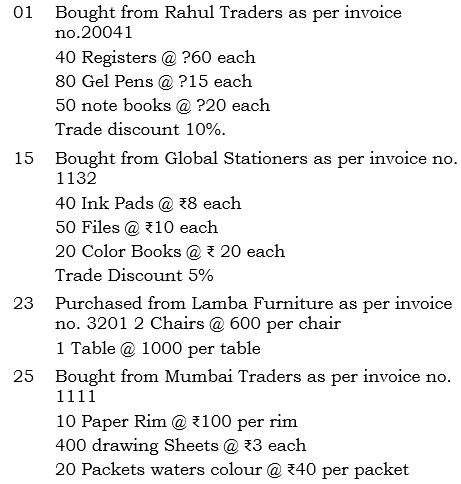

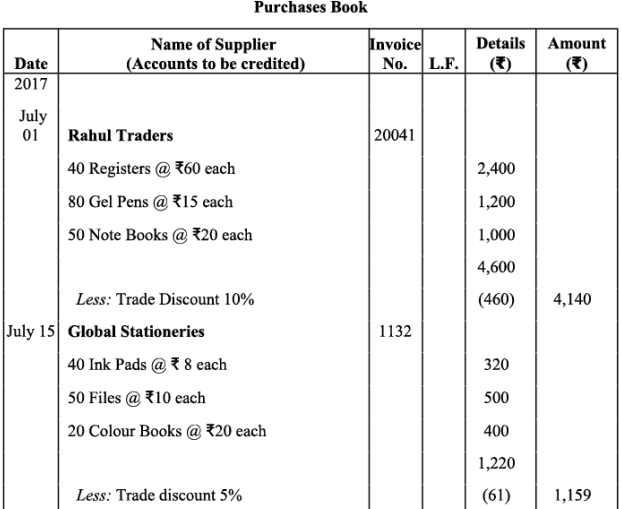

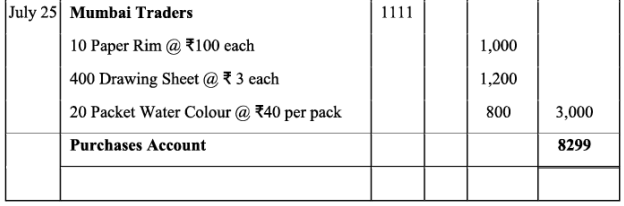

Q13: Enter the following transactions in the Purchase Journal (Book) of M/s Gupta Traders of July 2017:

Ans: Books of M/s. Gupta Traders

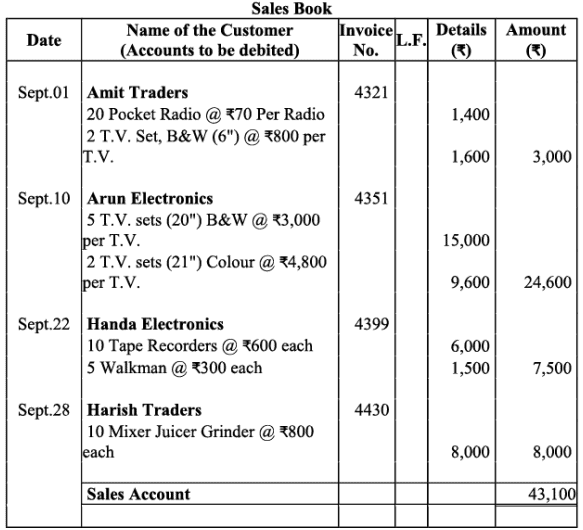

Q14: Enter the following transactions in sales (journal) book of M/s. Bansal electronics:

Ans: Books of M/s. Bansal Electronics

Ans: Books of M/s. Bansal Electronics

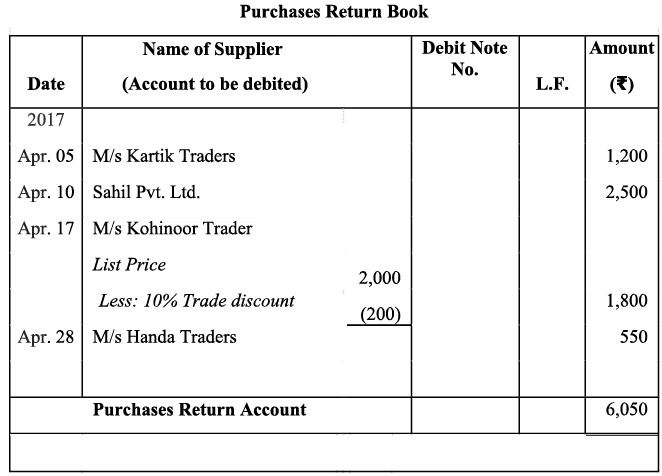

Q15: Prepare a purchases return (journal) book from the following transactions for April 2017.

Ans:

Ans:

Q16: Prepare Return Inward Journal (Book) from the following transactions of M/s Bansal Electronics for July 2017:

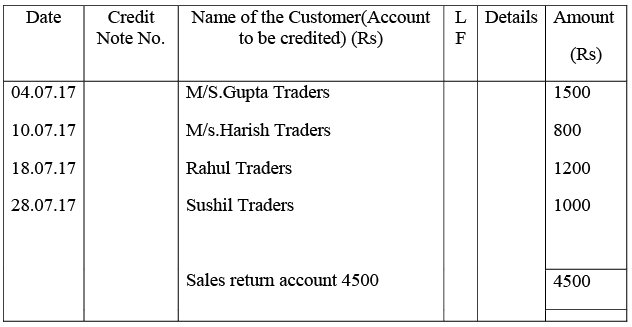

Ans: Books of M/s. Bansal electronics

Sales Returns Book

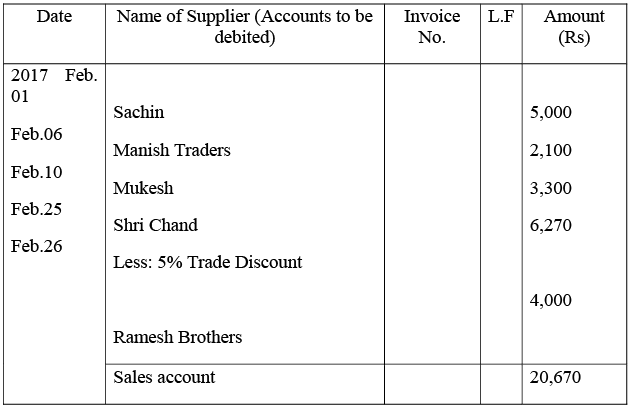

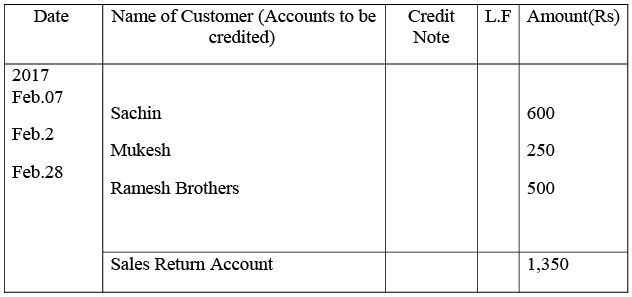

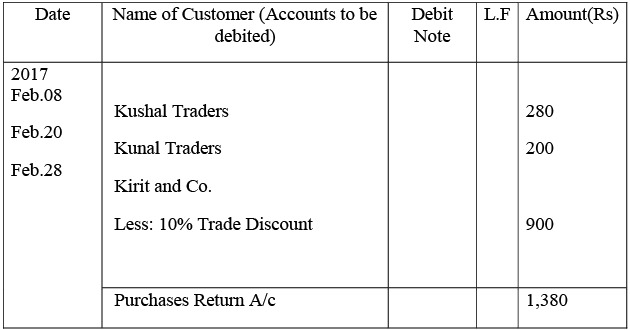

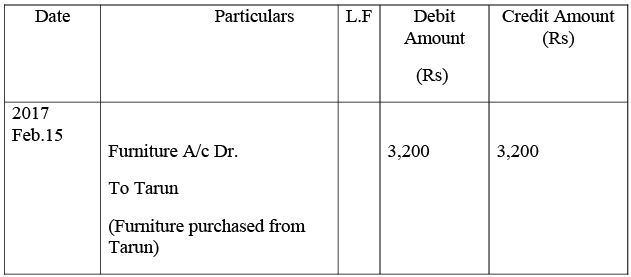

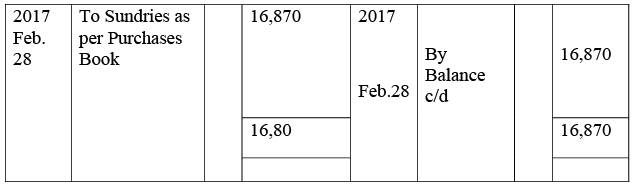

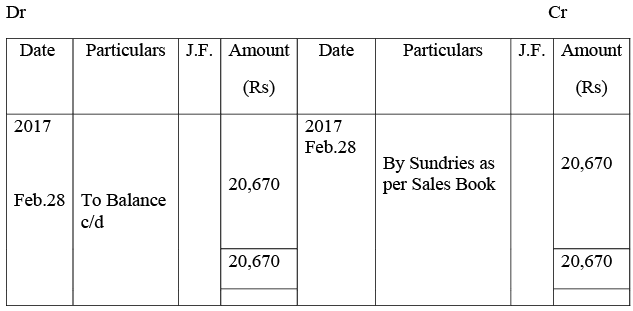

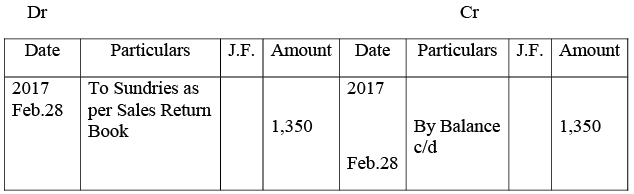

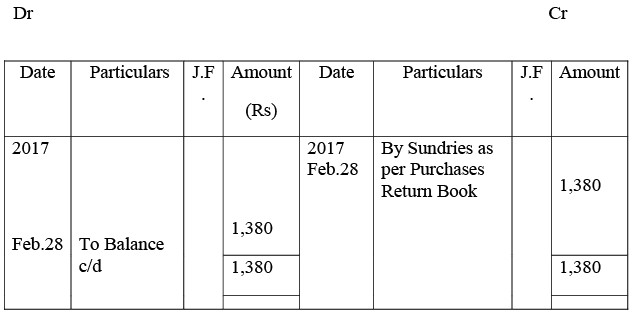

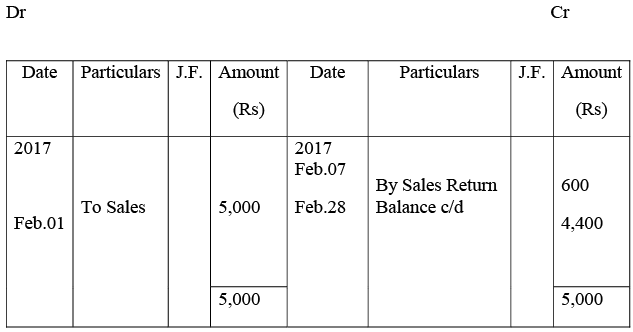

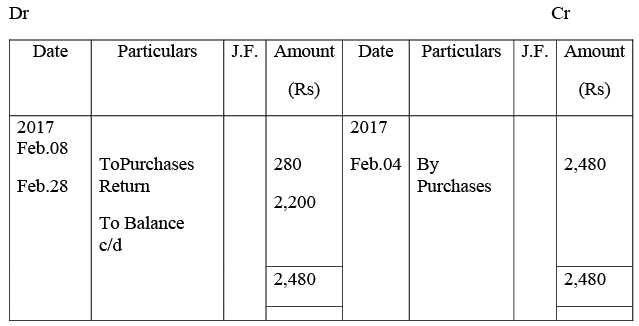

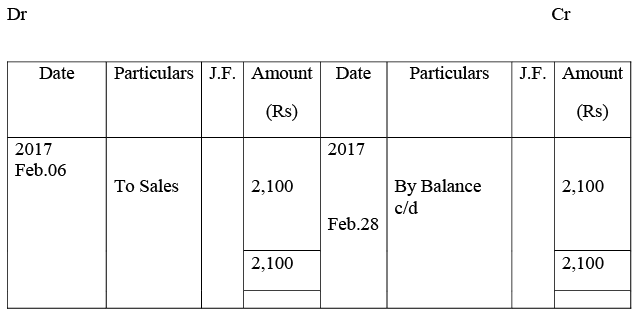

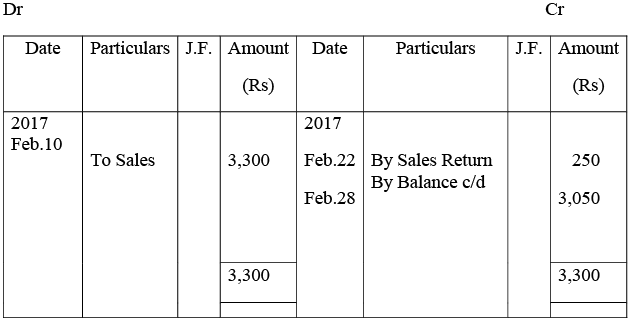

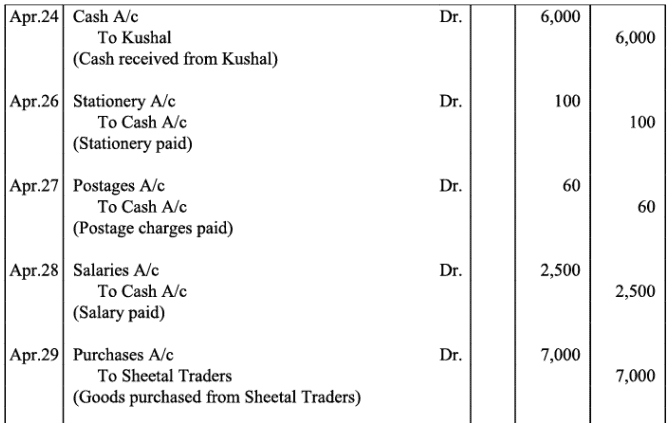

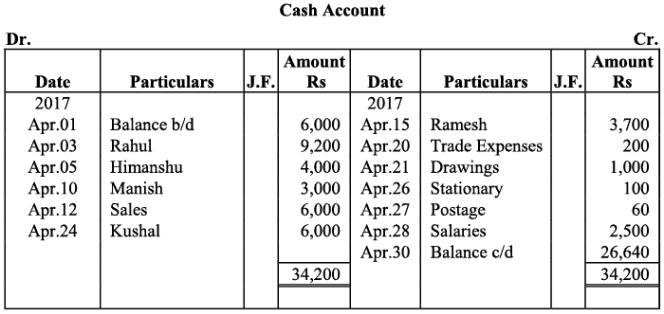

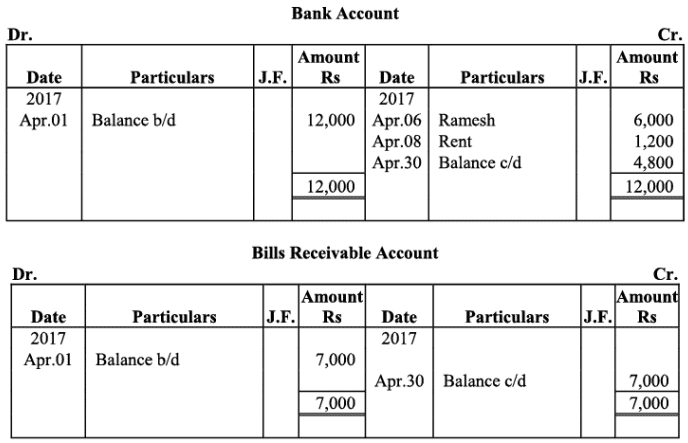

Q17: Prepare proper subsidiary books and post them to the ledger from the following transactions for the month of February 2017:

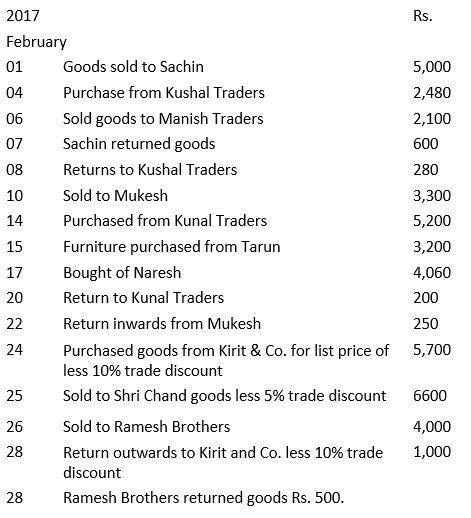

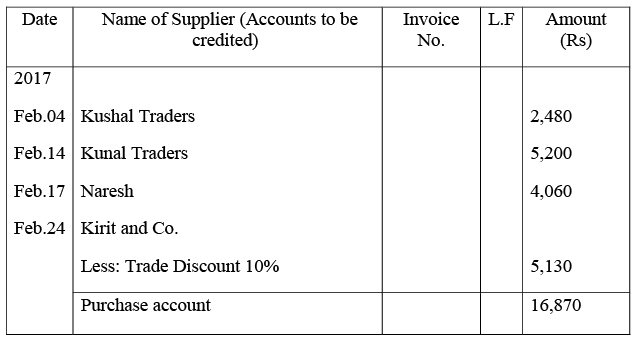

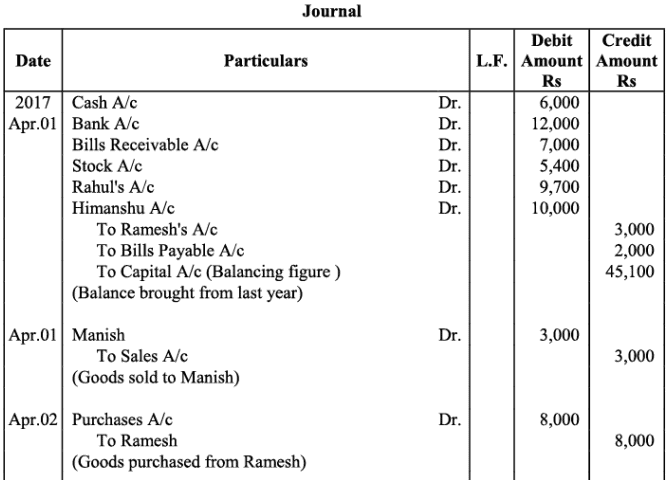

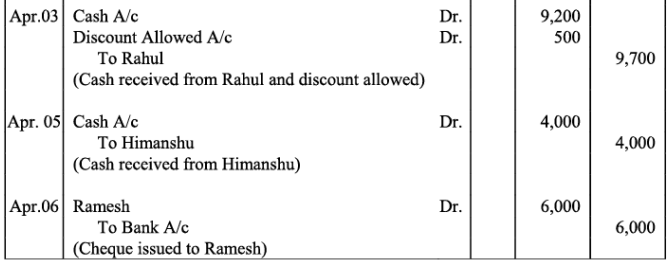

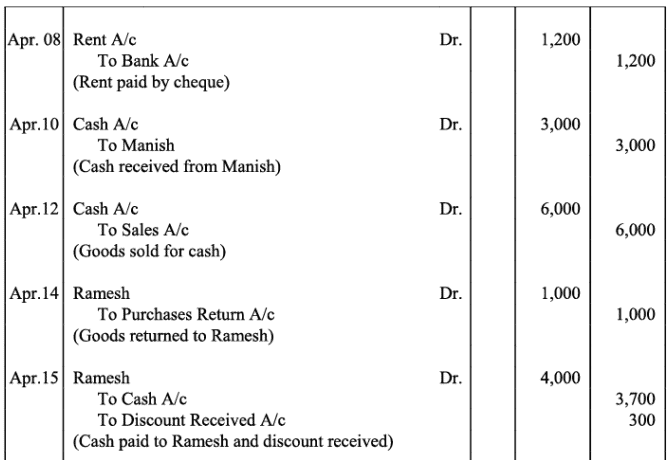

Ans: Journal

Ans: Journal

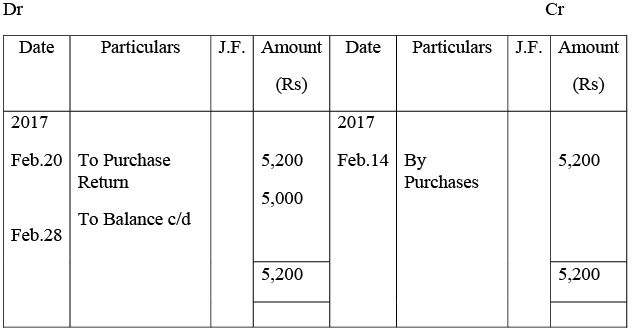

Purchases Book

Sales Book

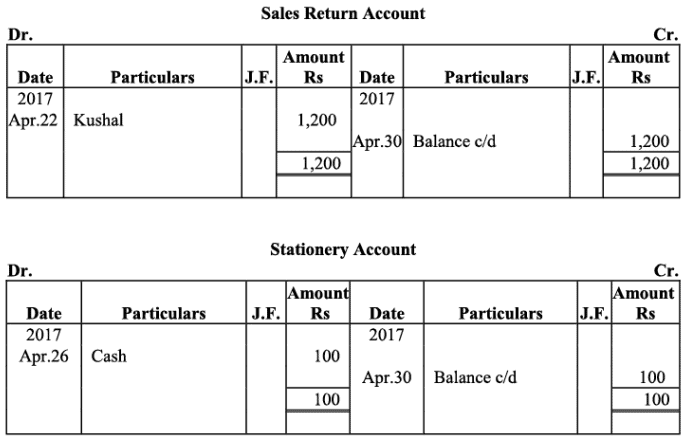

Sales Return Book

Sales Return Book

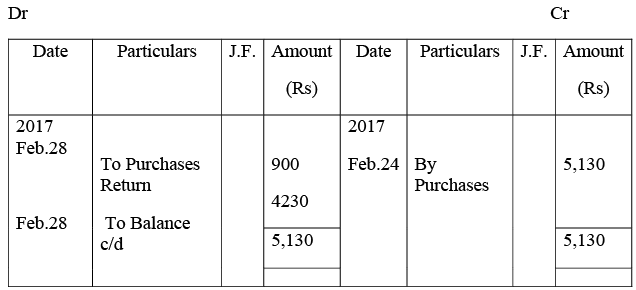

Purchases Return Book

Journal Proper

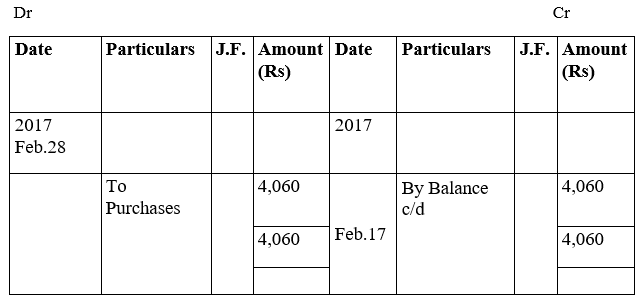

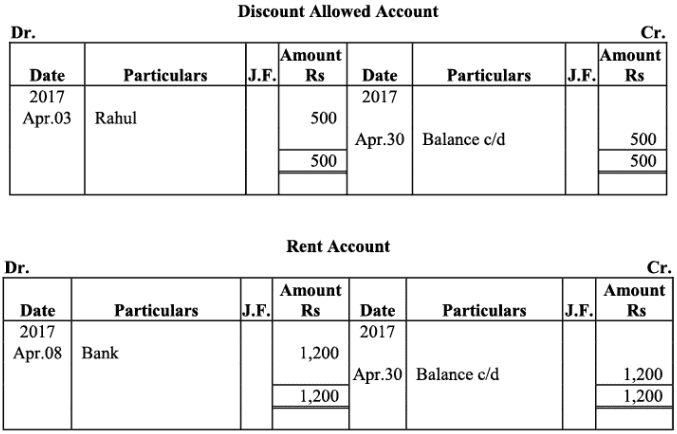

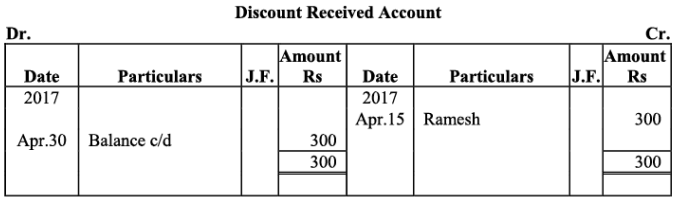

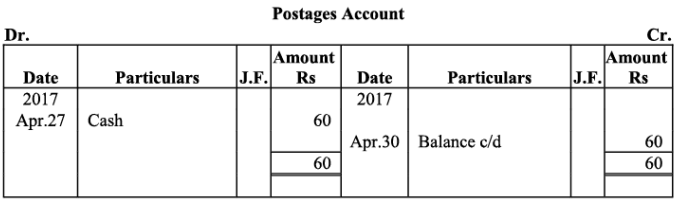

Ledger

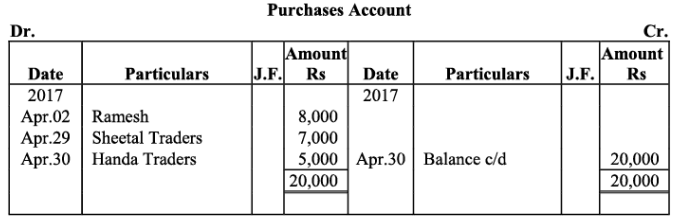

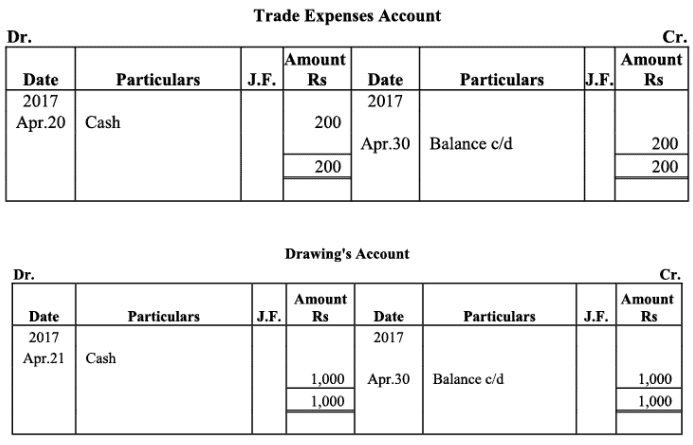

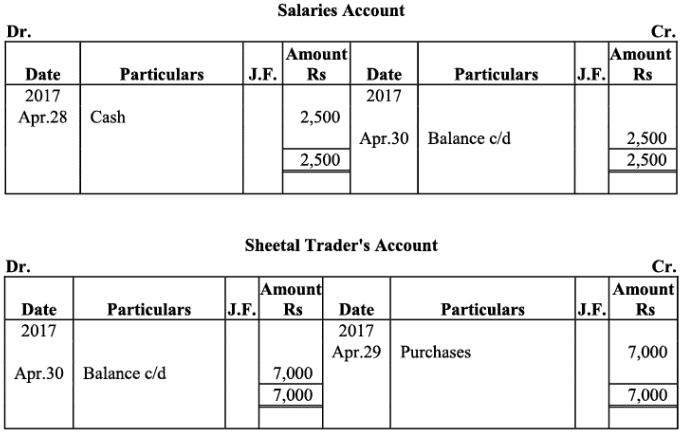

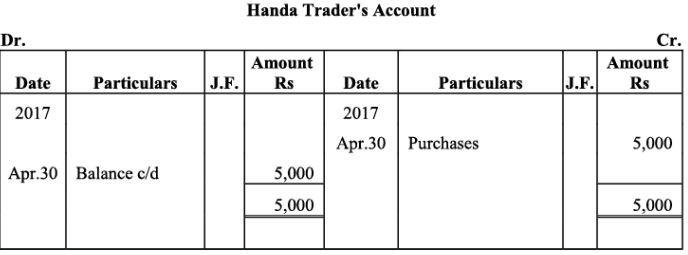

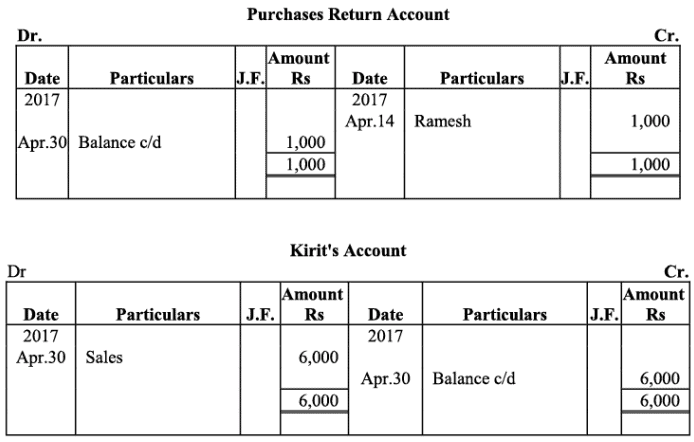

Purchases Account

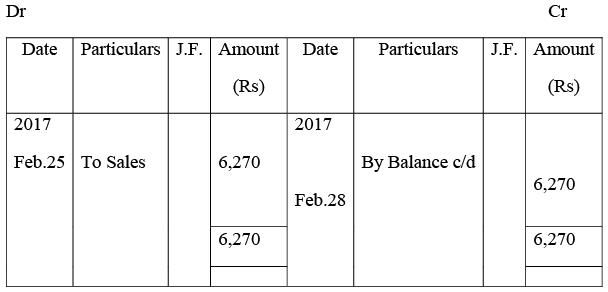

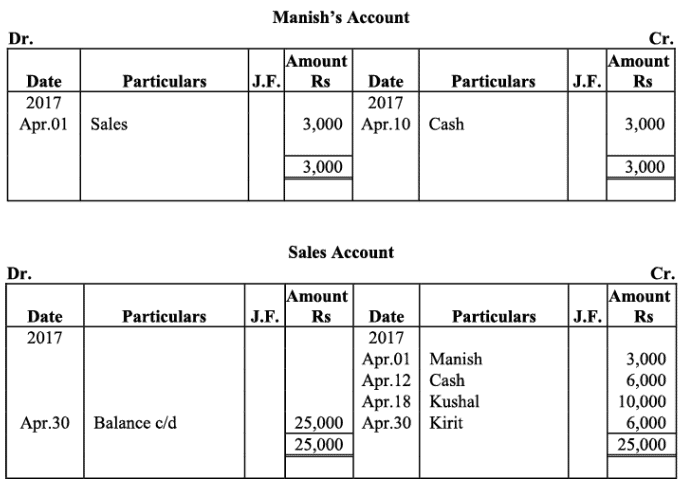

Sales Account

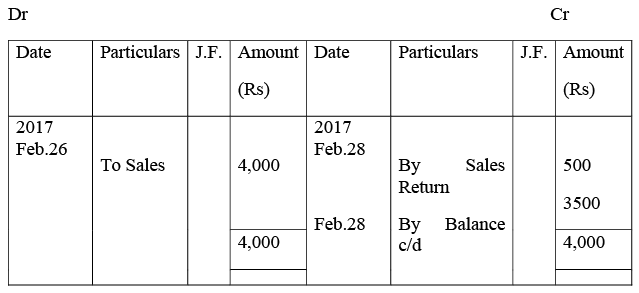

Sales Return Account

Purchases Return Account

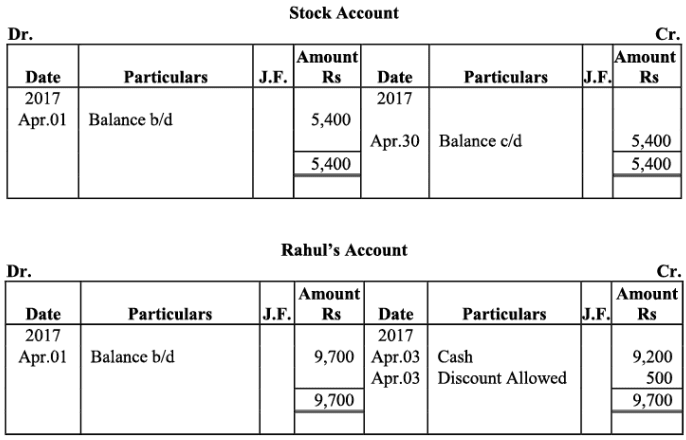

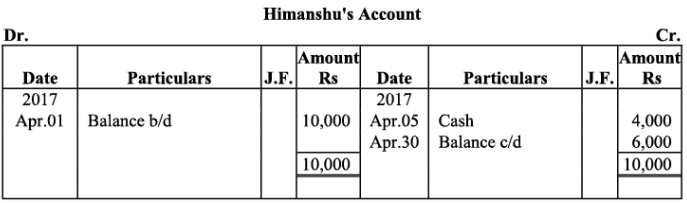

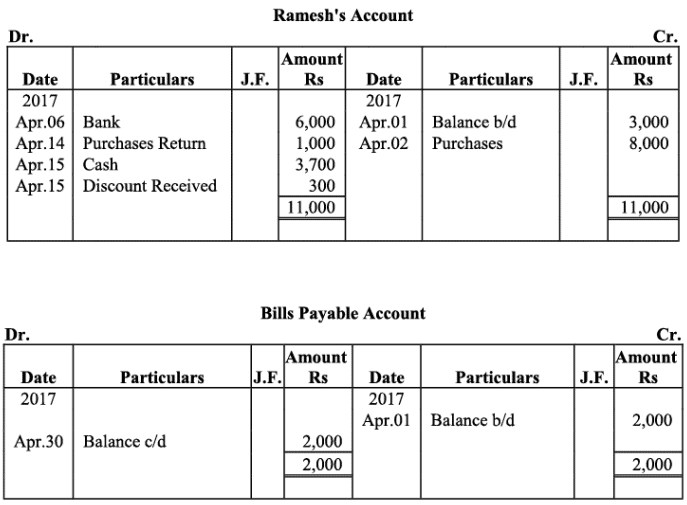

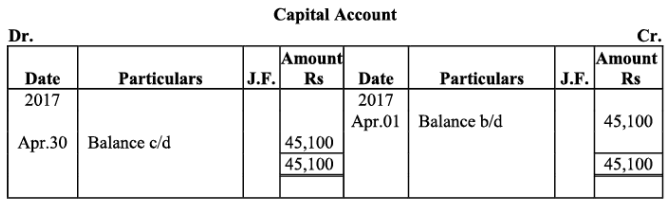

Sachin's Account

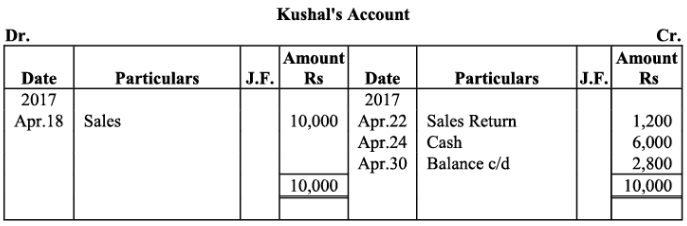

Kushal Traders' Account

Manish Traders' Account

Mukesh's Account

Kunal Traders' Account

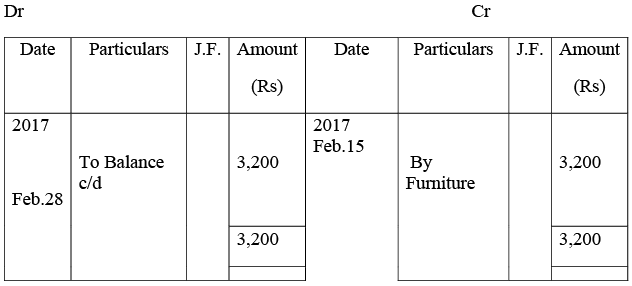

Furniture Account

Furniture Account

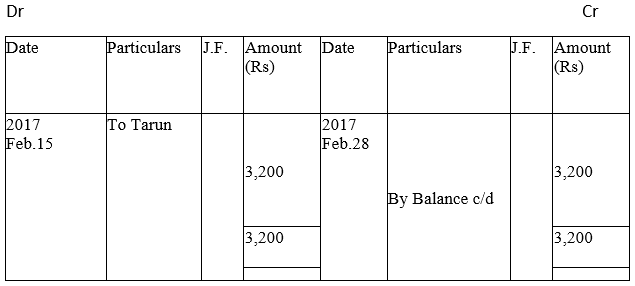

Tarun's Account

Tarun's Account

Naresh's Account

Kirit & Co. Account

Shri Chand & Co. Account

Ramesh's Account

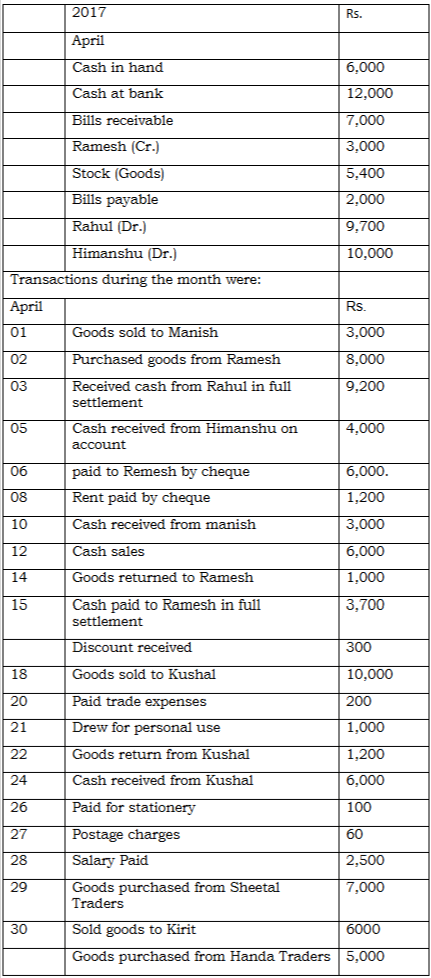

Q18: The following balances of ledger of M/s Marble Traders on April 01, 2017

Journlise the above transactions and post them to the ledger.

Ans:

Ledger

Q1: Briefly state how the cash book is both a journal and a ledger.

Ans: A cash book is a journal because it records cash receipts and cash payments in chronological order directly from source documents. It is also a ledger because it contains separate columns (for example, cash and bank) whose balances are final and need not be posted again to separate cash and bank ledger accounts. Thus, the cash book performs the functions of both a journal and a ledger.

Q2: What is the purpose of contra entry?

Ans: A contra entry is made when cash and bank accounts are involved in the same transaction, for example when cash is deposited into the bank or when cash is withdrawn from the bank. In a double-column cash book, contra entries are marked by the letter "C" in the Ledger Folio (L.F.) column and are recorded on both the cash and bank sides. Contra entries transfer funds between cash and bank but do not affect the overall cash-plus-bank position of the business.

Q3: What are special purpose books?

Ans: Special purpose books (or subsidiary books) are books of prime entry used to record frequently occurring transactions of a similar nature directly, instead of recording them first in the journal. Examples include the purchases book, sales book, purchases return book, sales return book, cash book and bills book. They save time, reduce repetition and make the later posting to ledger accounts simpler and faster.

Q4: What is petty cash book? How is it prepared?

Ans: A petty cash book is a subsidiary book used to record small day-to-day expenses such as postage, stationery, conveyance, and telephone charges. It is maintained by a petty cashier who makes payments from a small cash fund kept for this purpose. There are two common systems for maintaining a petty cash book:

i. Original System: A fixed sum is given to the petty cashier. The petty cashier pays small expenses from this sum and records each payment. When the cash is exhausted, the petty cashier submits the petty cash book and is reimbursed for the amount spent.

ii. Imprest System: A fixed amount (the imprest) is given to the petty cashier at the start of the accounting period. At regular intervals the petty cash book is checked and the petty cashier is reimbursed only for the amount spent, so that the petty cashier always holds the fixed imprest amount.

FAQs on NCERT Solution - Recording of Transactions-II

| 1. What are the main types of transactions recorded in accounting? |  |

| 2. How do journal entries play a role in recording transactions? | |

| 3. What is the significance of double-entry bookkeeping in recording transactions? | |

| 4. What are the basic components of a ledger in accounting? | |

| 5. How do financial statements relate to recorded transactions? | |