NCERT Solution (Part - 2) Recording of Transactions-II

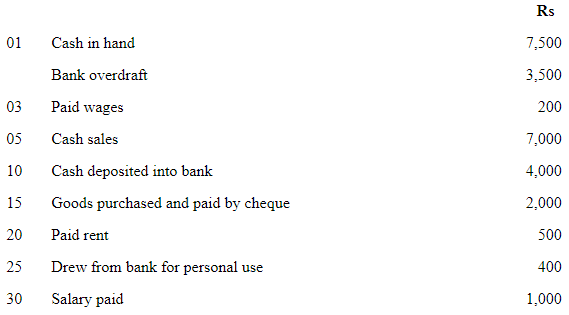

Question 7: Prepare double column cash book from the following information for July 2017 :

Explanation: The enclosed double column cash book shows entries in the cash column and the bank column for July 2017. Receipts are entered on the debit side and payments on the credit side. The discount columns (if any) record discount allowed or received. Each column is totalled and balanced to show the closing cash and bank balances to be carried forward.

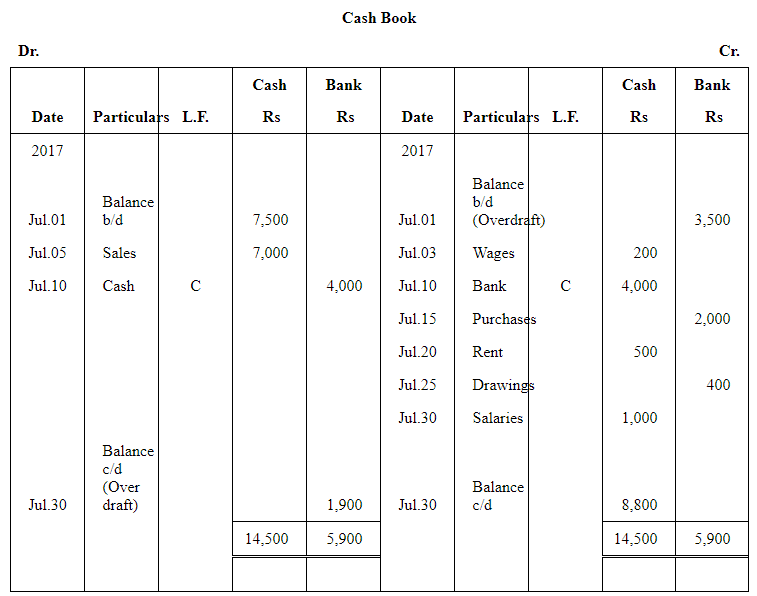

Question 8: Enter the following transaction in a double column cash book of M/s Mohit Traders for January 2017:

Explanation: The transactions are entered date-wise with particulars, ledger folio and amounts in appropriate columns. Cash receipts and payments appear in the cash column; bank receipts and payments in the bank column. Any discounts are recorded in the discount column and column totals are carried to the ledger at period end.

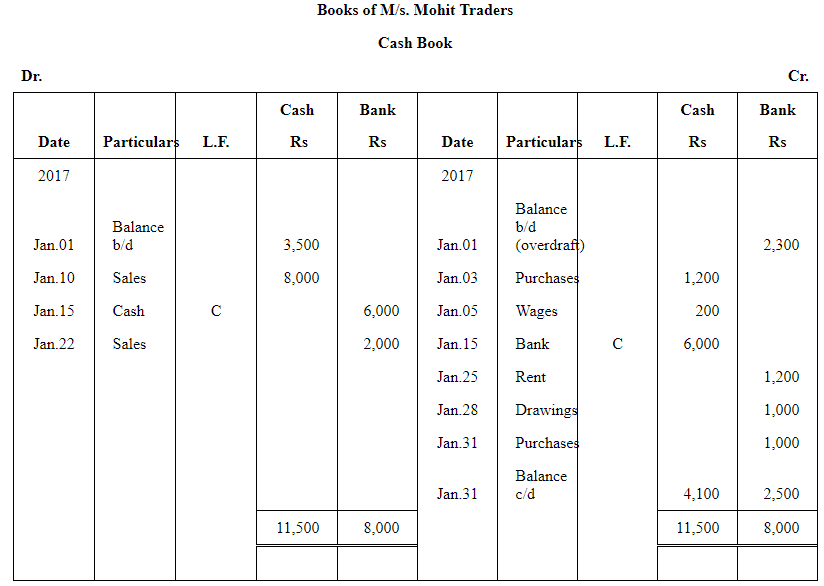

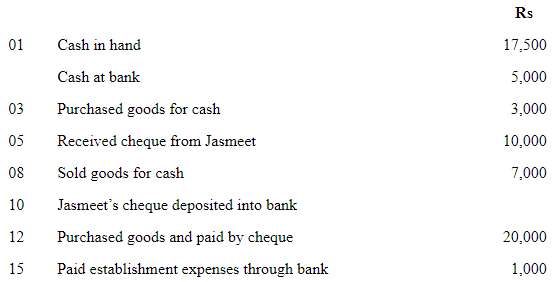

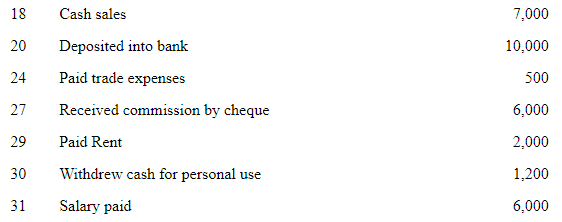

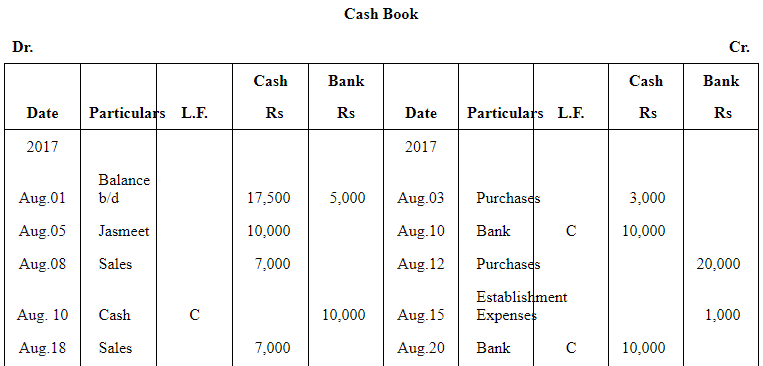

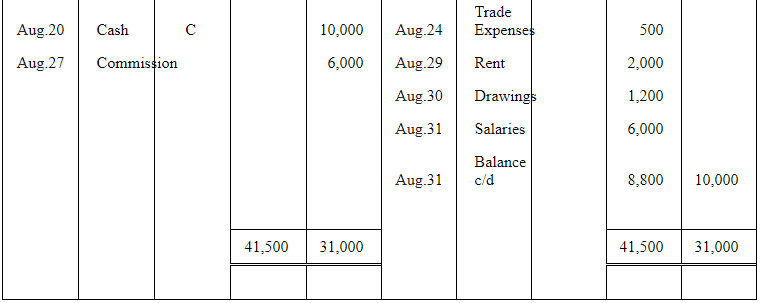

Question 9: Prepare double column cash book from the following transactions for the year August 2017:

Answer:

[[S]]

Explanation: The prepared double column cash book (images above) records the month's cash and bank transactions separately. All receipts are shown on the debit side and payments on the credit side. The book is balanced by totalling each column and carrying forward the closing cash and bank balances to the next period.

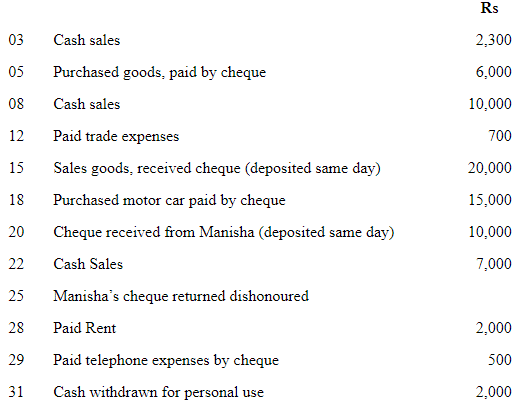

Question 10: M/s Ruchi trader started their cash book with the following balances on Dec. 01 2005 : cash in hand Rs 1,354 and balance in bank current account Rs 7,560. He had the following transaction in the month of July, 2017

Prepare bank column cash book

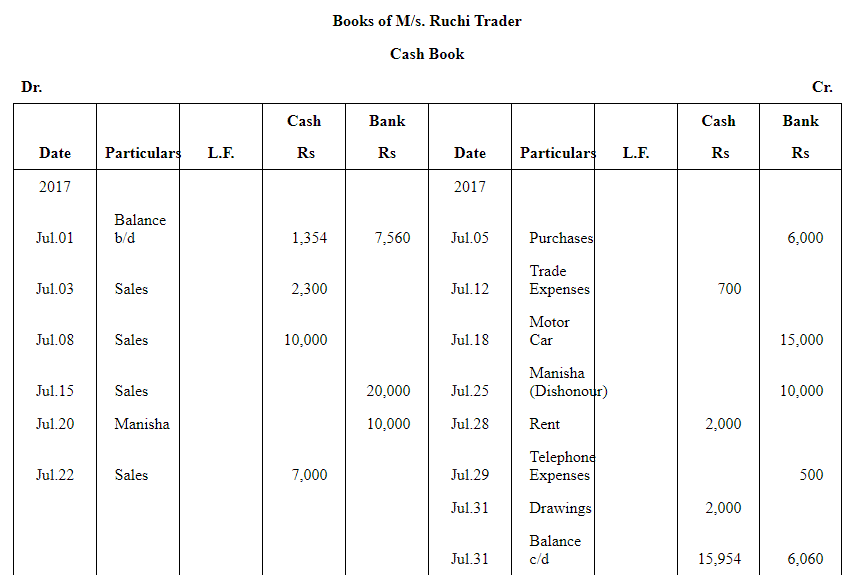

Answer:

Explanation: The bank column cash book shows only bank transactions and opening bank balance. Deposits are entered on the debit side and withdrawals (cheques issued) on the credit side. Each entry is posted to the relevant ledger account and the bank column is balanced to reveal the closing bank balance.

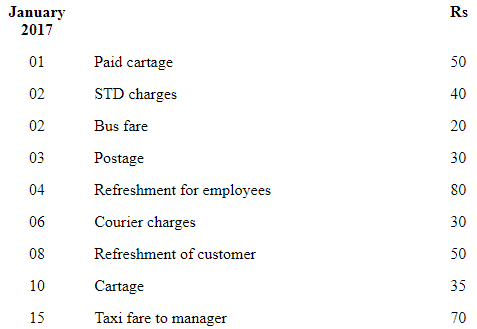

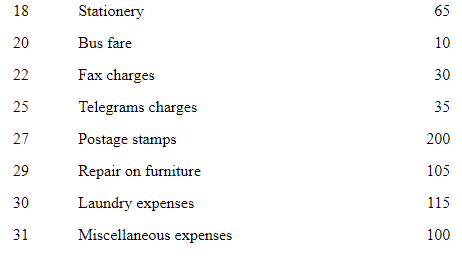

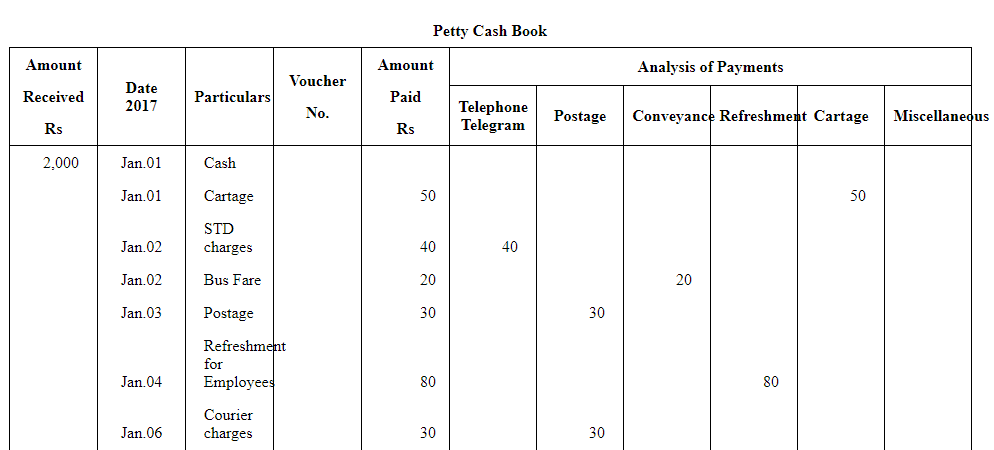

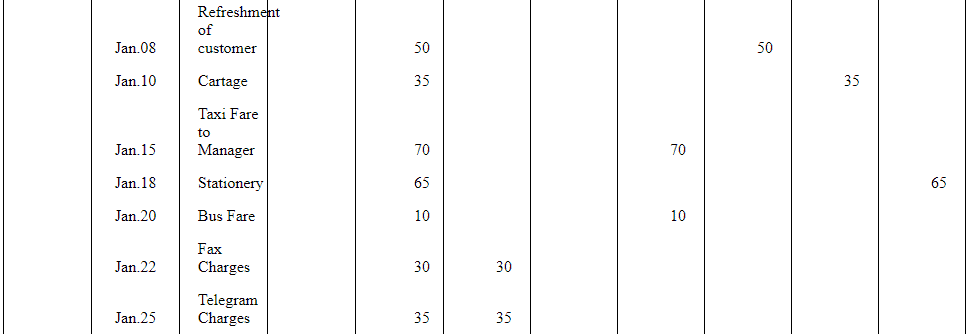

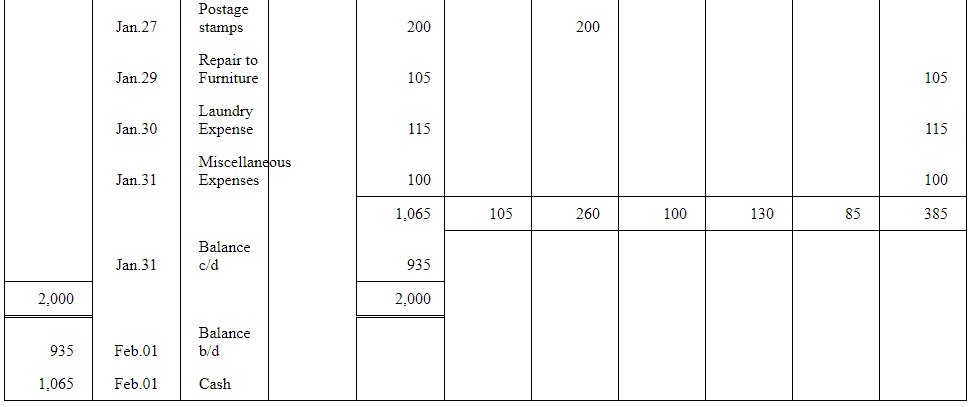

Question 11: Prepare petty cash book from the following transactions. The imprest amount is Rs 2,000.

Answer:

Explanation: The petty cash book is prepared under the imprest system where the petty cashier is reimbursed to restore the imprest of Rs 2,000. Expenses are analysed under appropriate heads (stationery, postage, conveyance, etc.) and the total of petty payments is used to calculate the amount to be reimbursed at period end.

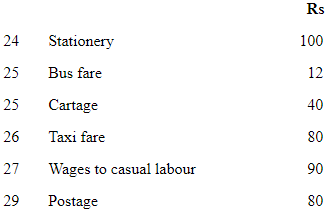

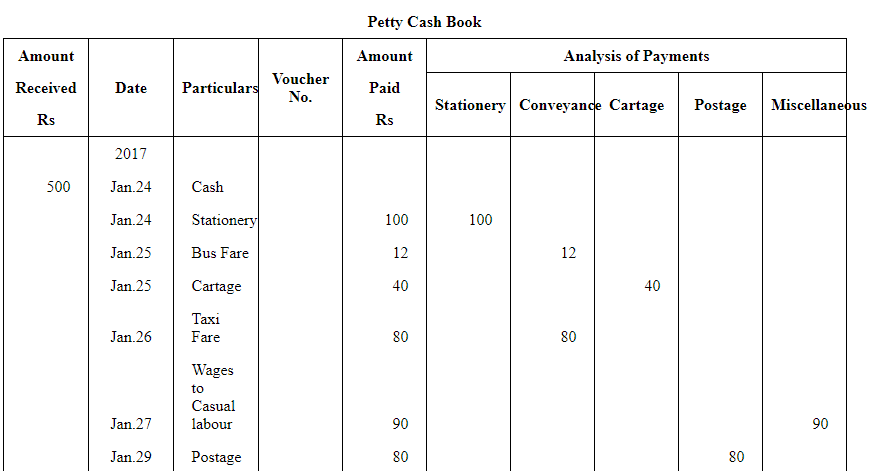

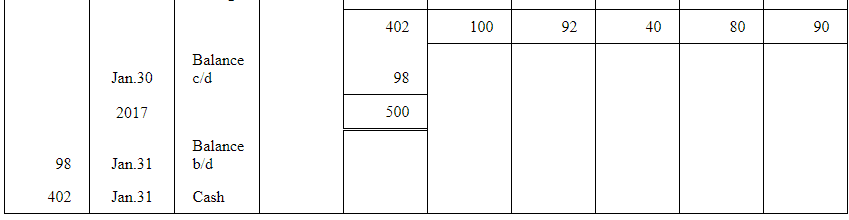

Question 12: Record the following transactions during the week ending January. 30, 2017 with a weekly imprest Rs 500

Explanation: Transactions for the week are entered in the petty cash book under the imprest of Rs 500. Each petty payment is classified, totalled and the amount required to restore the imprest is calculated by subtracting closing petty cash from the fixed imprest sum.

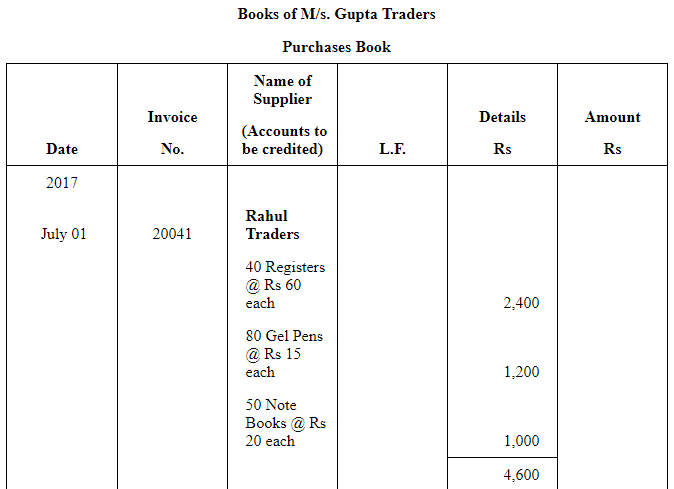

Question 13: Enter the following transactions in the Purchase Journal (Book) of M/s Gupta Traders of July 2005:

01 Bought from Rahul Traders as per invoice no. 20041

40 Registers @ Rs 60 each

80 Gel Pens @ Rs 15 each

50 note books @ Rs 20 each

Trade discount 10%.

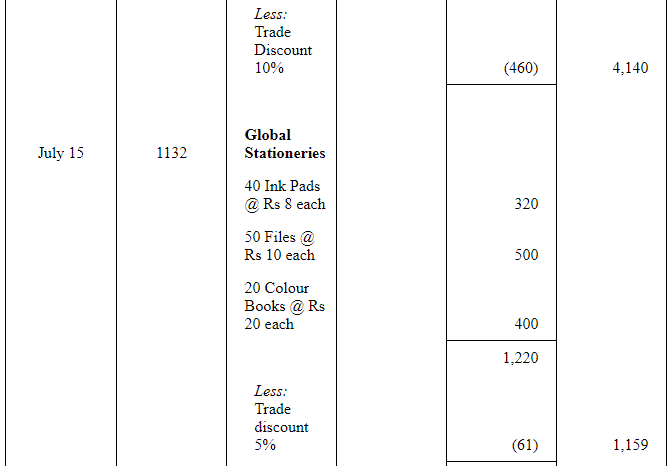

15 Bought from Global Stationers as per invoice no. 1132

40 Ink Pads @ Rs 8 each

50 Files @ Rs 10 each

20 Color Books @ Rs 20 each

Trade Discount 5%

23 Purchased from Lamba Furniture as per invoice no. 3201

2 Chairs @ 600 per chair

1 Table @ 1,000 per table

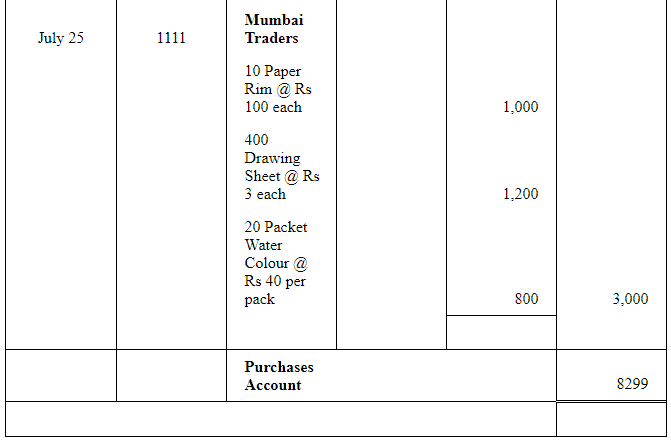

25 Bought from Mumbai Traders as per invoice no. 1111

10 Paper Rim @ Rs 100 per rim

400 drawing Sheets @ Rs 3 each

20 Packet water colour @ Rs 40 per packet

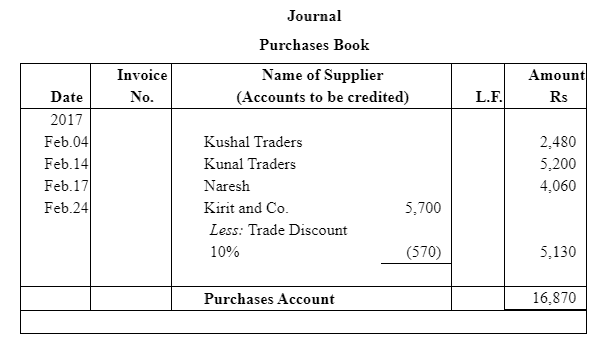

Answer:

Note: Furniture purchased from Lamba Traders will not be recorded in the Purchases Book as furniture is not to be considered as goods for the M/s Gupta Trader. This is because as per the transactions M/s. Gupta traders deals in stationery and not in furniture.

Additional Explanation: In the Purchases Journal record only credit purchases of trading goods. Trade discounts are deducted from the invoice value and the net amount is entered. Non-trading purchases (like furniture) are excluded and should be recorded in the appropriate fixed asset account, not in Purchases Book.

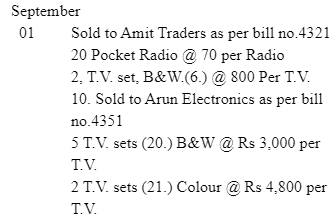

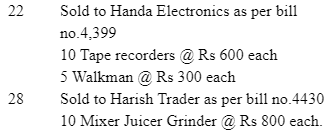

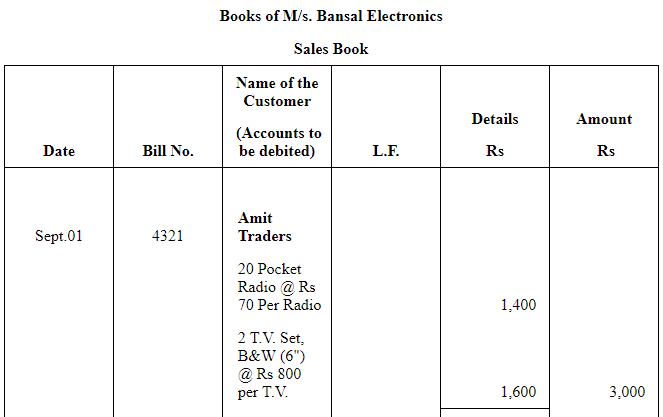

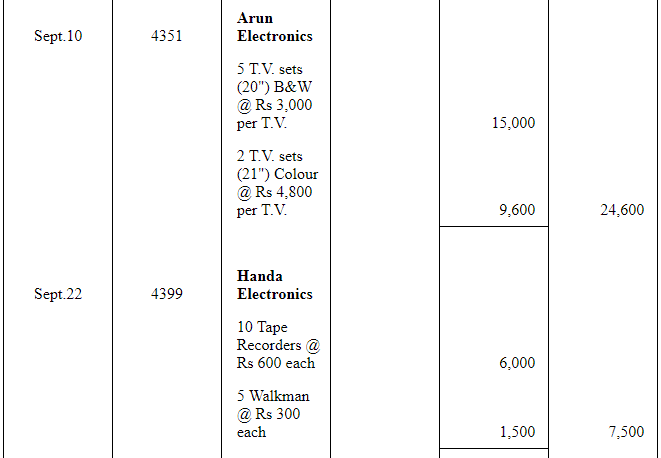

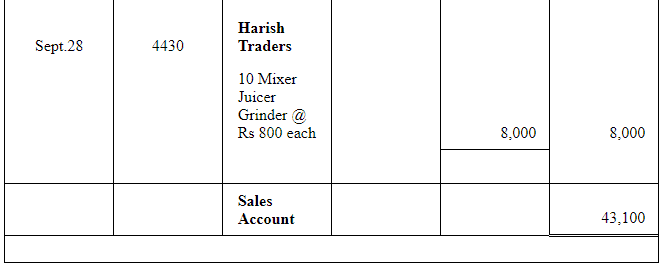

Question 14: Enter the following transactions in sales (journal) book of M/s. Bansal electronics:

Answer:

Explanation: The Sales Journal records all credit sales with invoice number, particulars and net amounts. Each entry is posted to the customer's ledger and the totals of the sales journal are posted periodically to the sales account in the general ledger. Cash sales are excluded from this book.

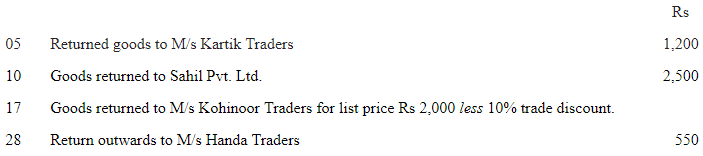

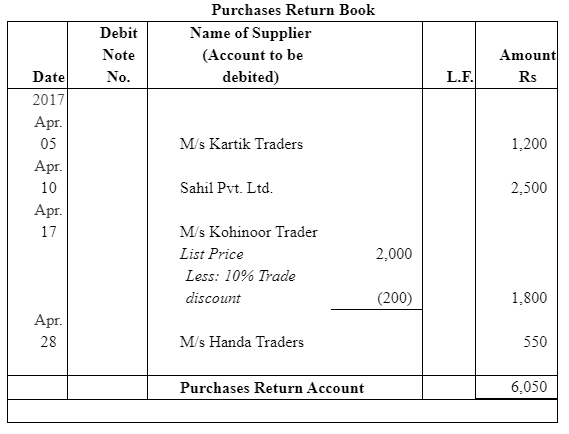

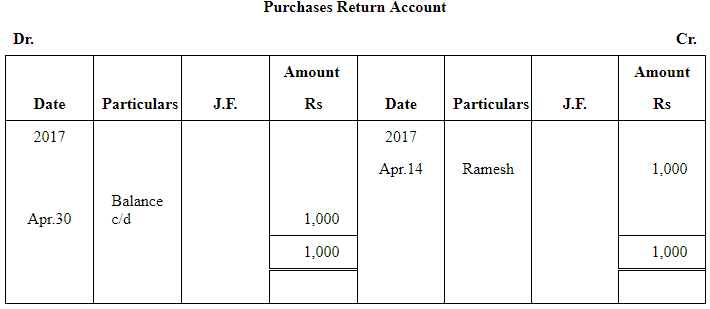

Question 15: Prepare a purchases return (journal) book from the following transactions for April 2017

Explanation: The Purchases Return Book (also called Return Outward Book) records goods returned to suppliers. Each entry cites the supplier, original invoice reference and the value of goods returned. Totals are posted to the Purchases Returns account and to individual supplier accounts where necessary.

Question 16: Prepare Return Inward Journal (Book) from the following transactions of M/s Bansal Electronics for July 2017:

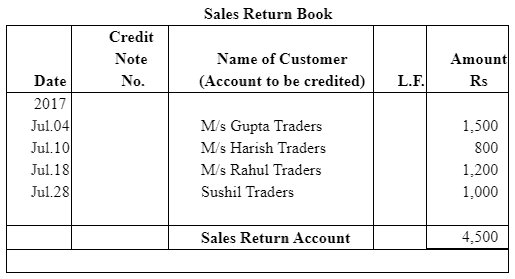

Answer:

Explanation: The Return Inward Book (Return Inwards) records goods returned by customers. It contains customer name, invoice reference and value returned. The totals are posted to the Sales Returns account and posted individually to the customer ledgers to reduce their outstanding balances.

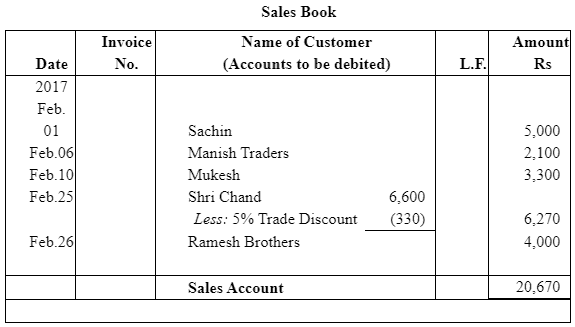

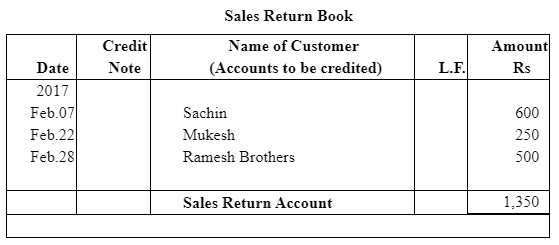

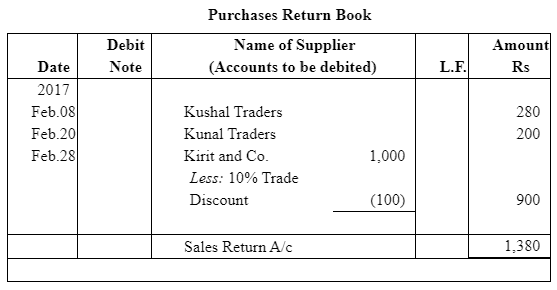

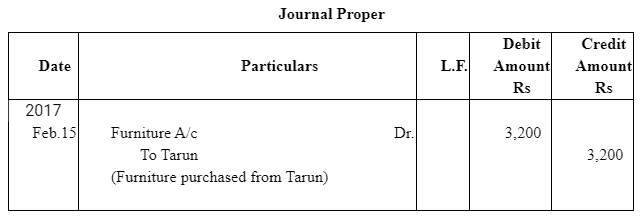

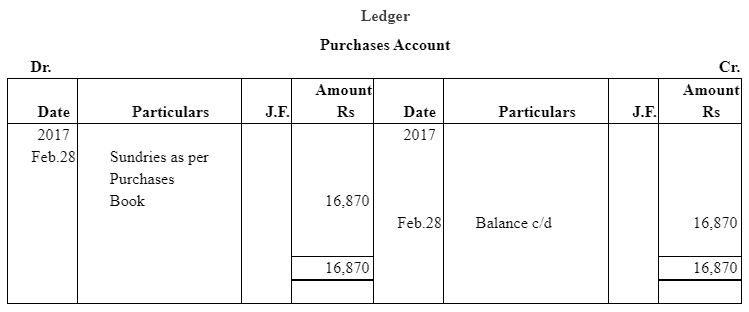

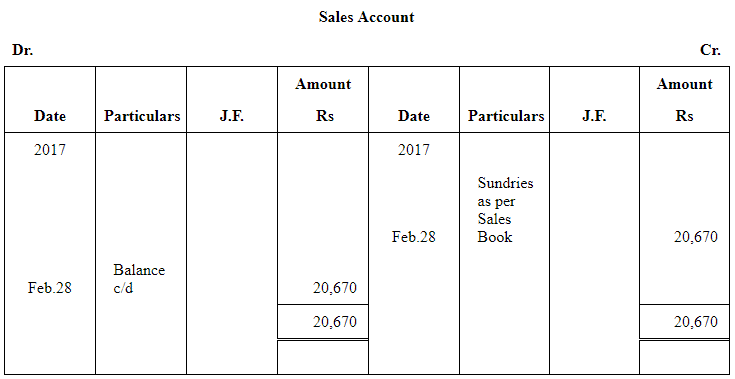

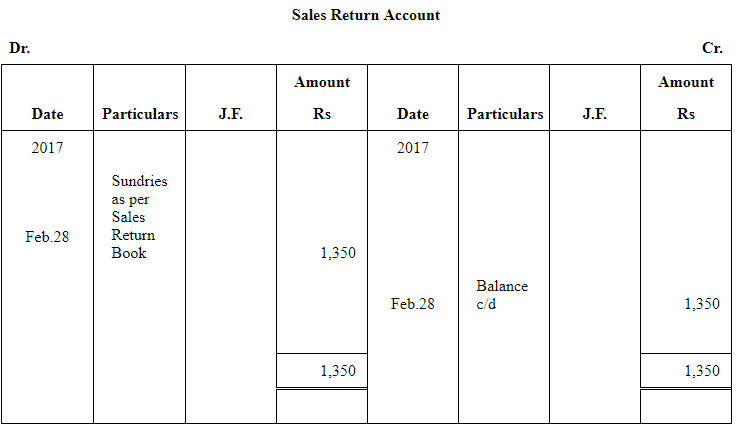

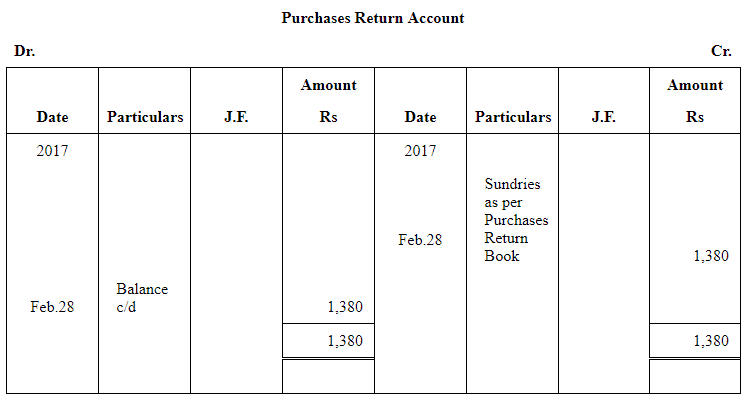

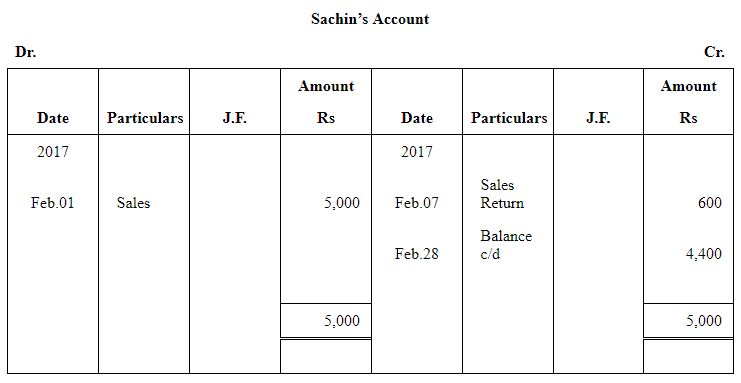

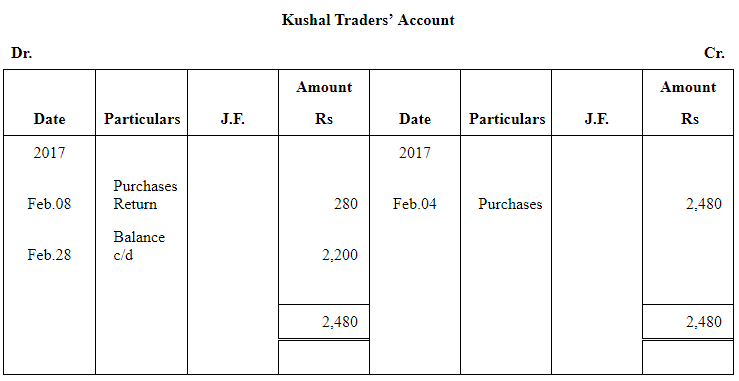

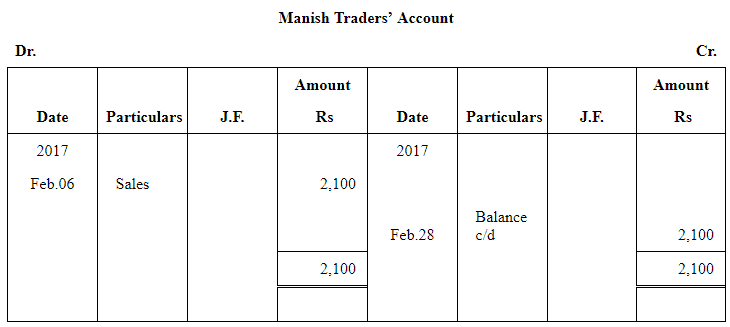

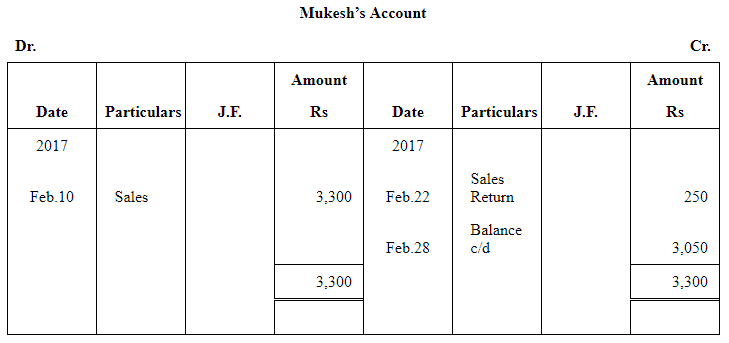

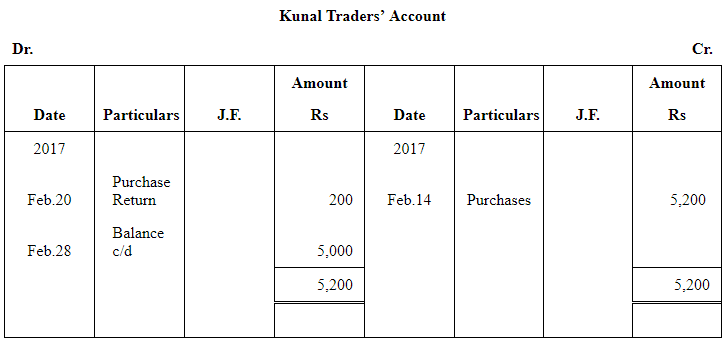

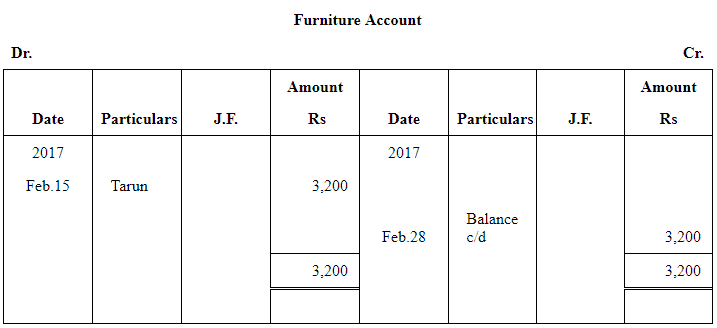

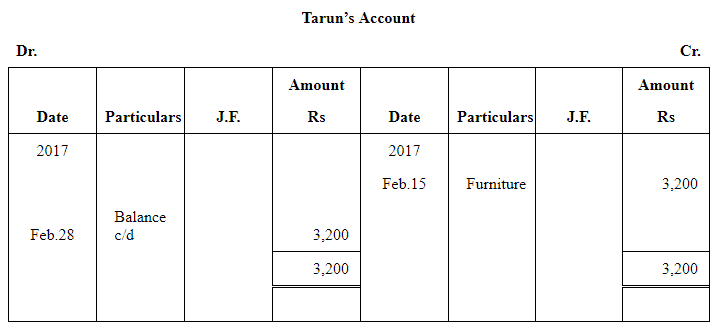

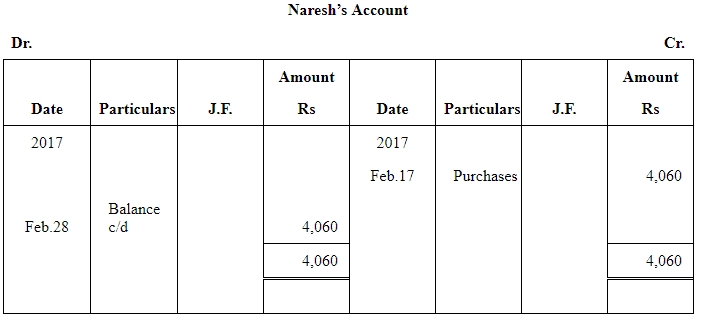

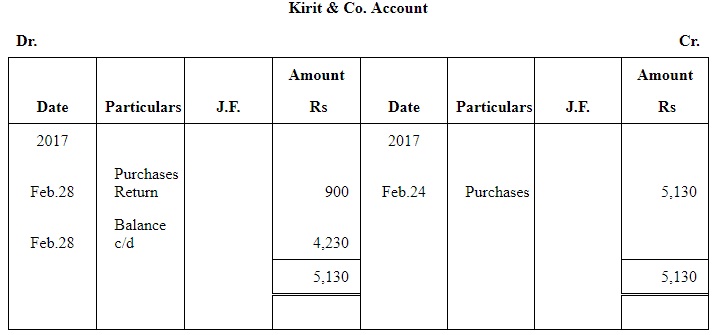

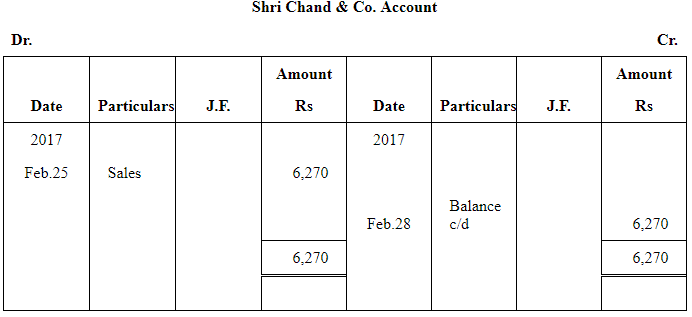

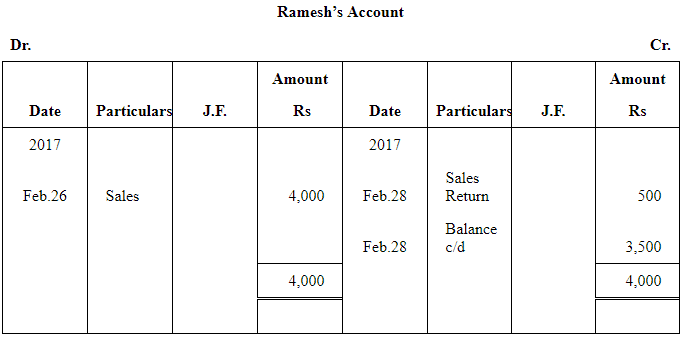

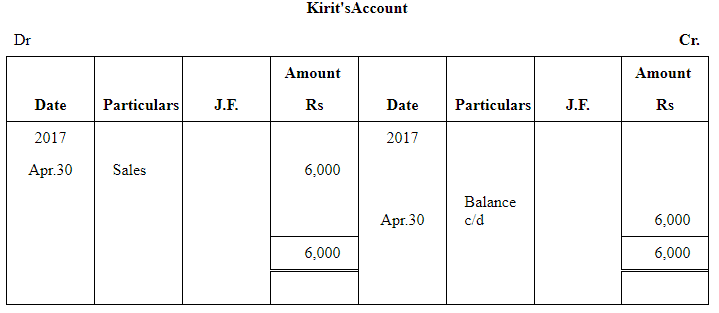

Question 17: Prepare proper subsidiary books and post them to the ledger from the following transactions for the month of February 2017:

Answer:

Explanation: The subsidiary books shown above (purchases, sales, returns, cash book, petty cash etc.) are prepared to capture routine transactions in a structured way. Totals from each subsidiary book are posted to the respective ledger accounts in the general ledger, with folio references, and individual ledgers are balanced to show closing balances for the period.

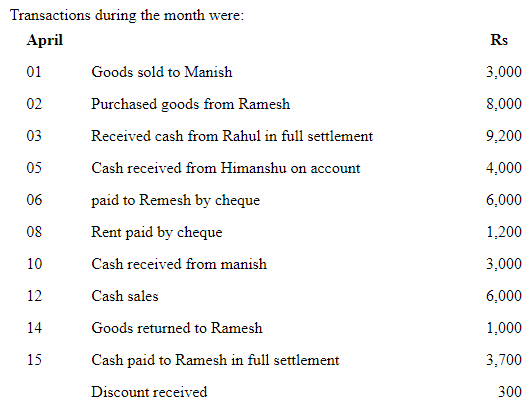

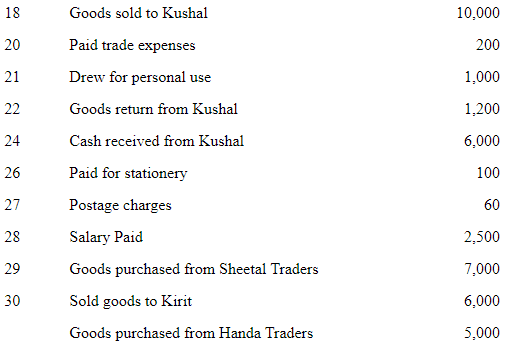

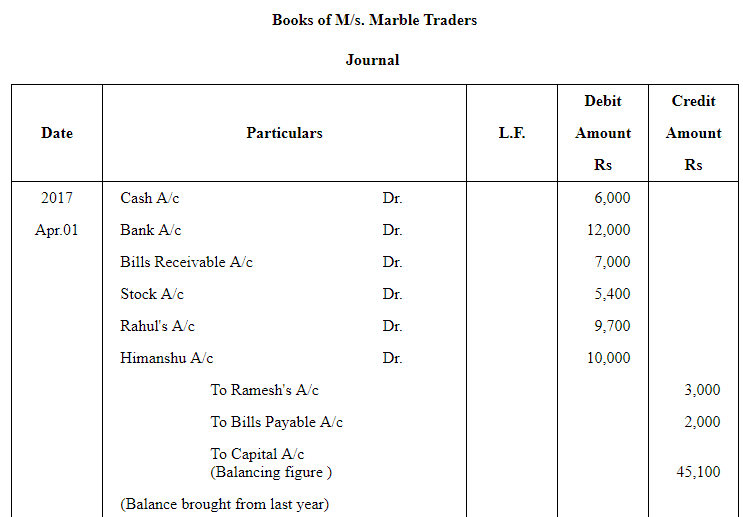

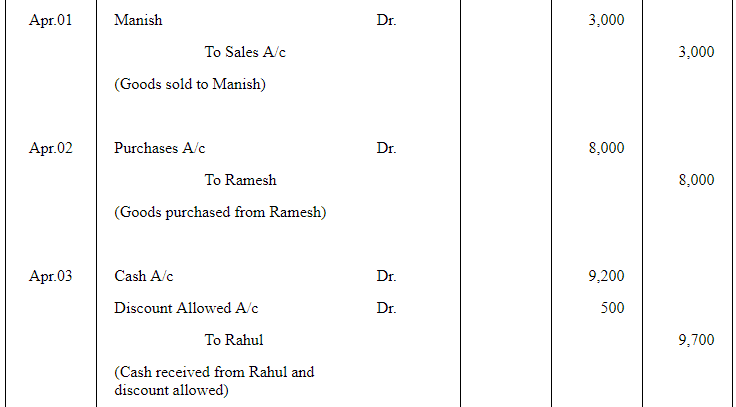

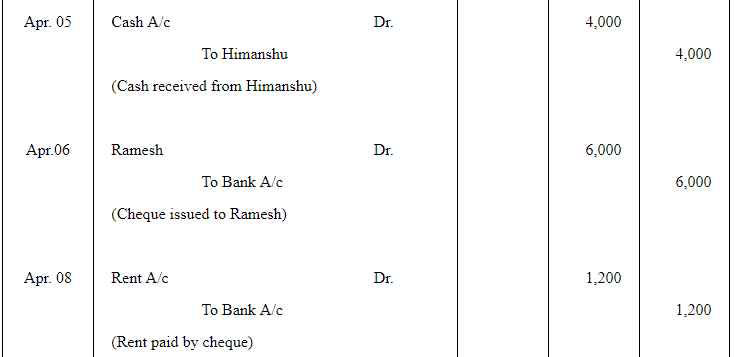

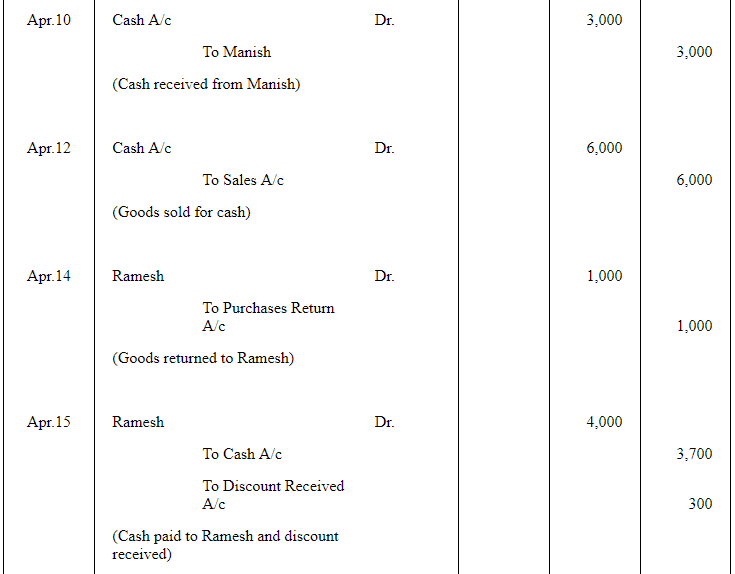

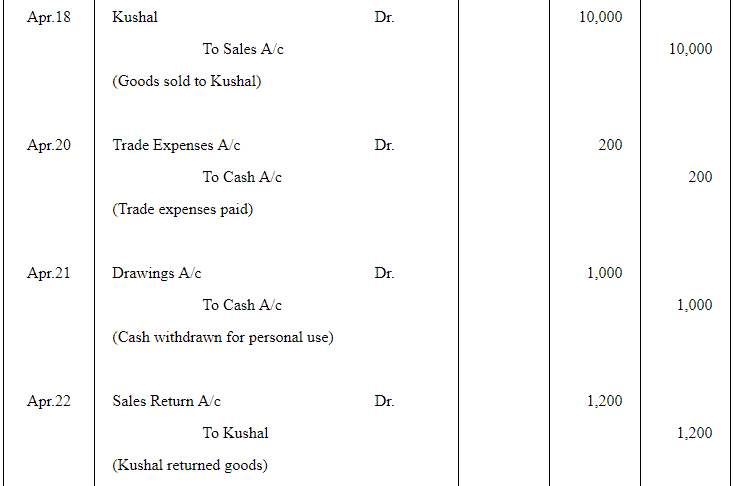

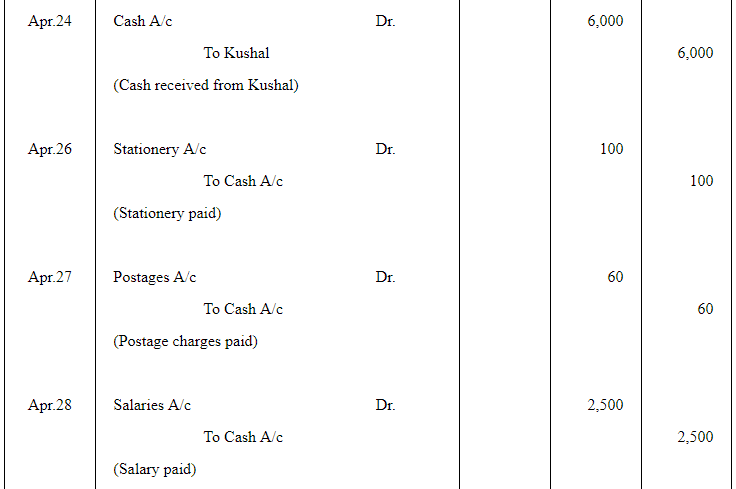

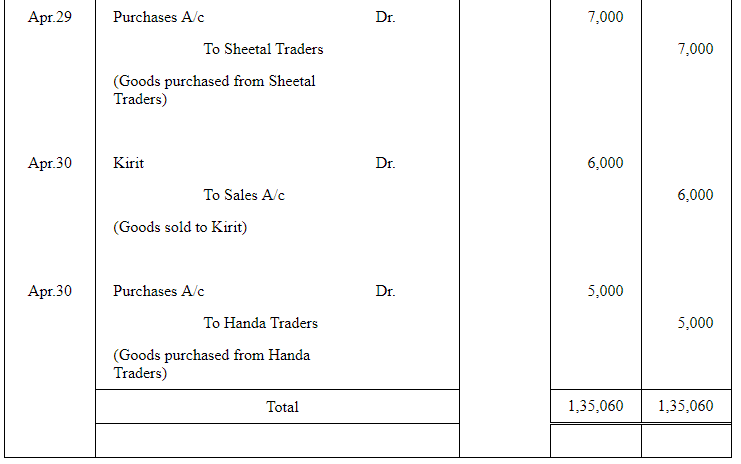

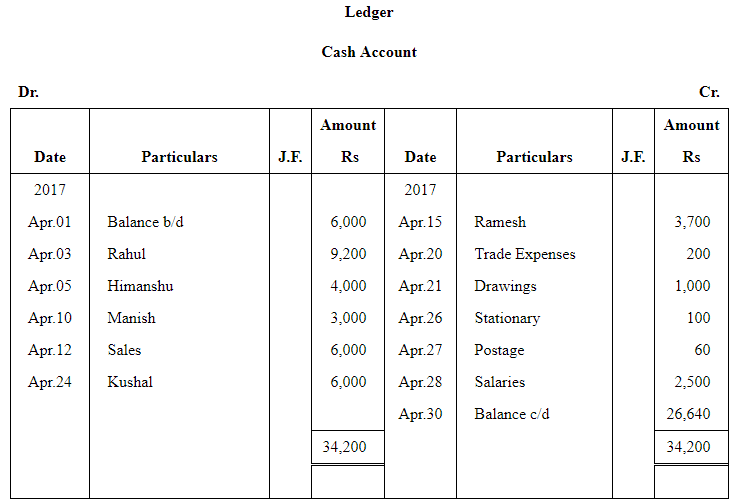

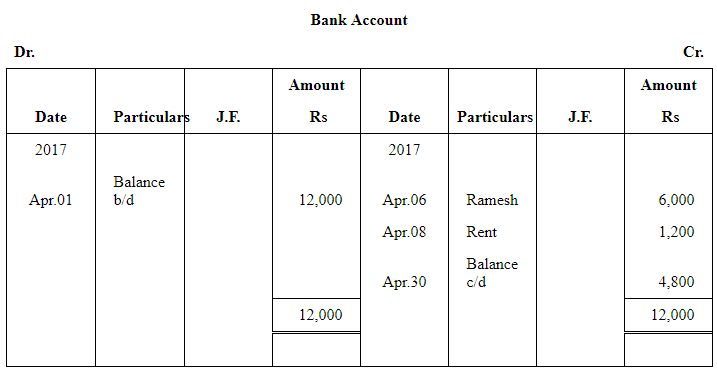

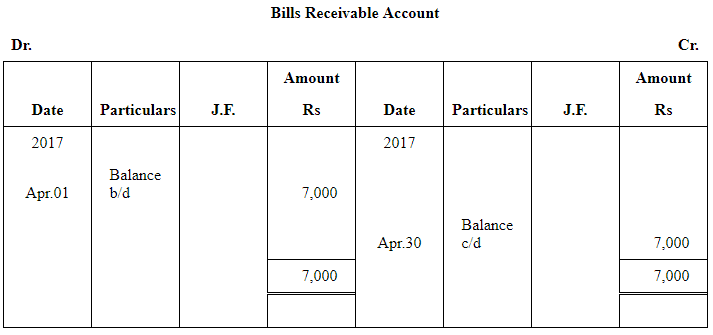

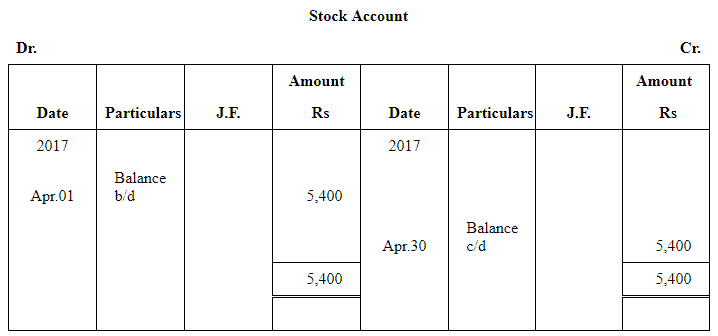

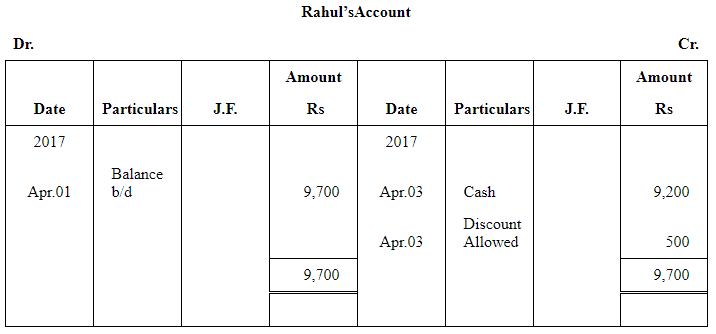

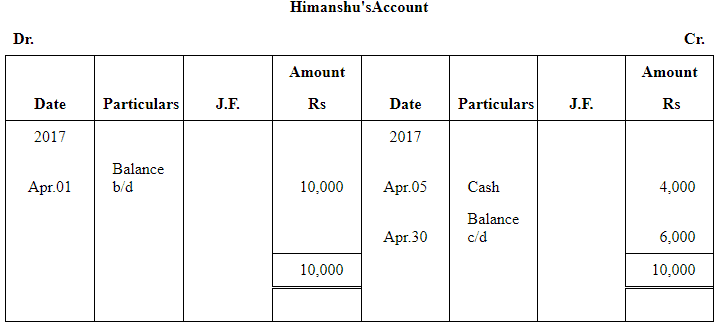

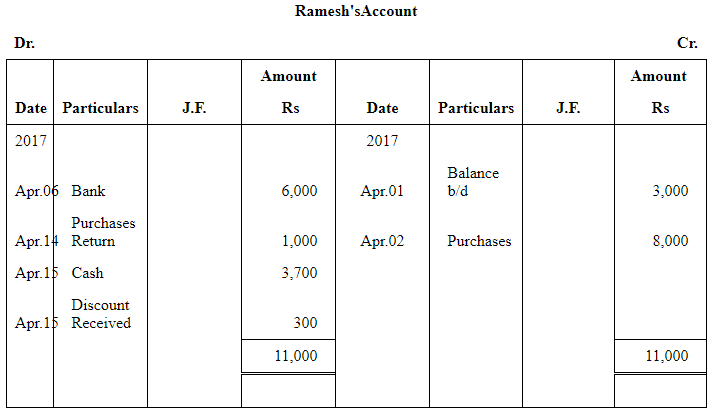

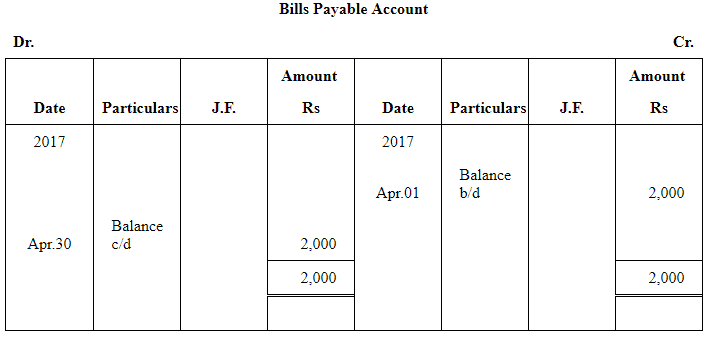

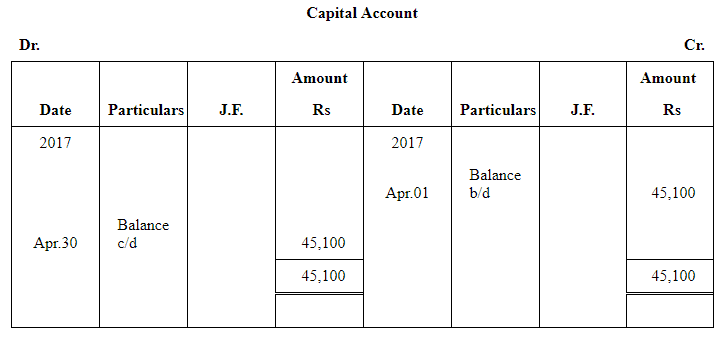

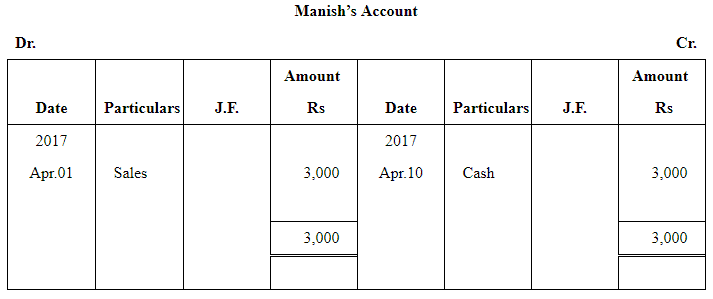

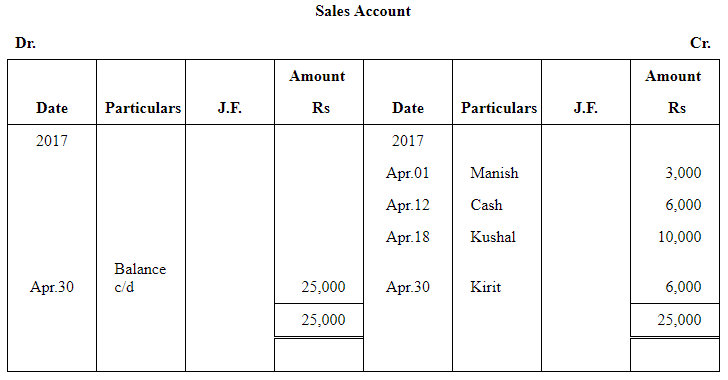

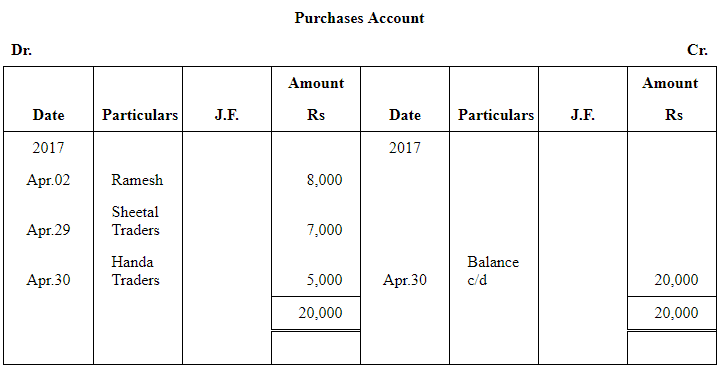

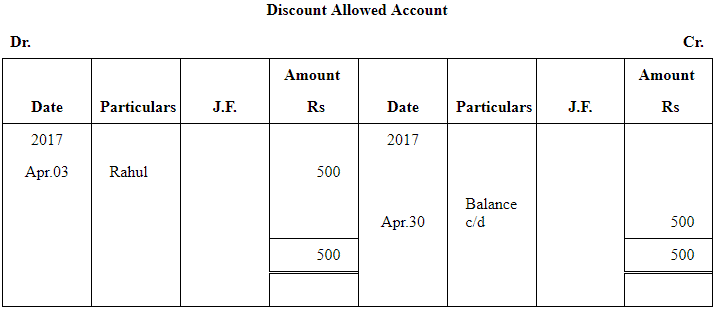

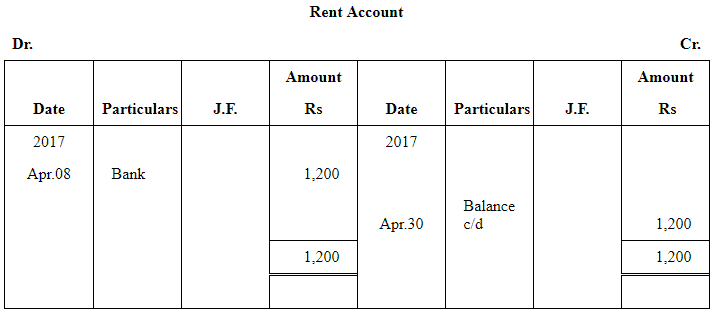

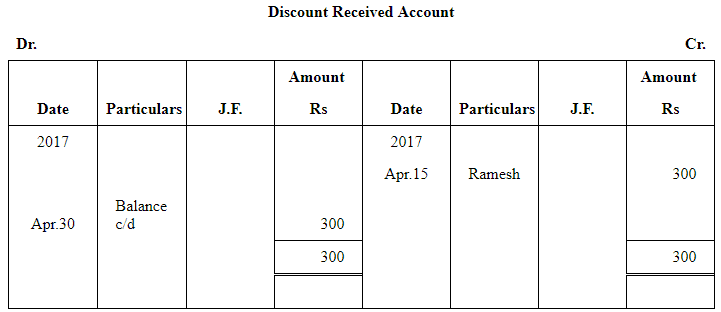

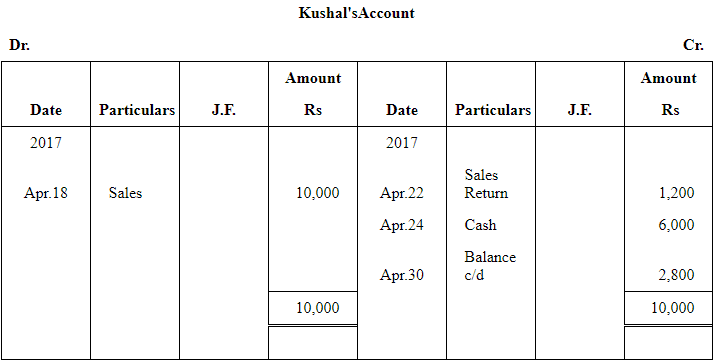

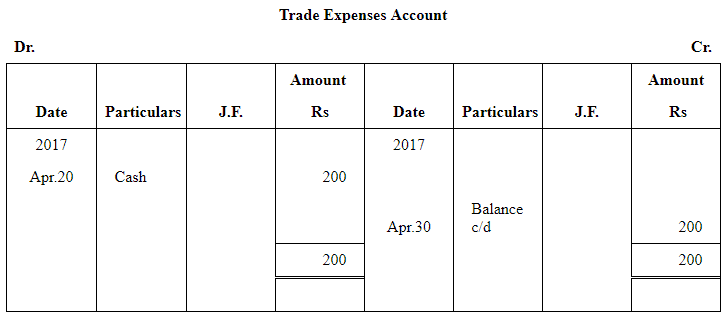

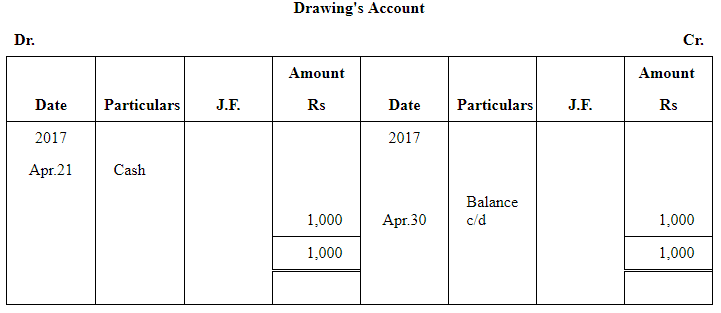

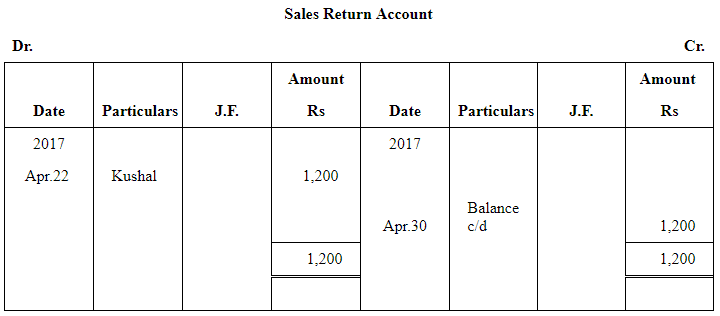

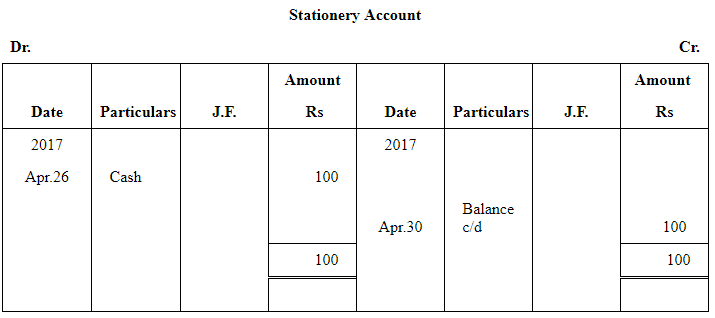

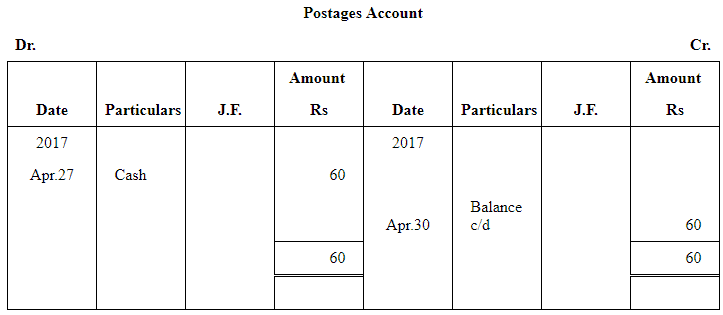

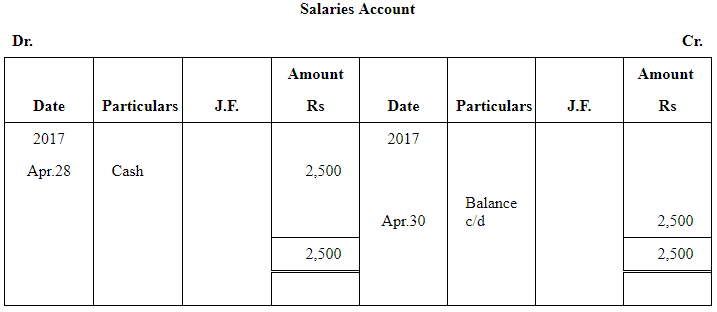

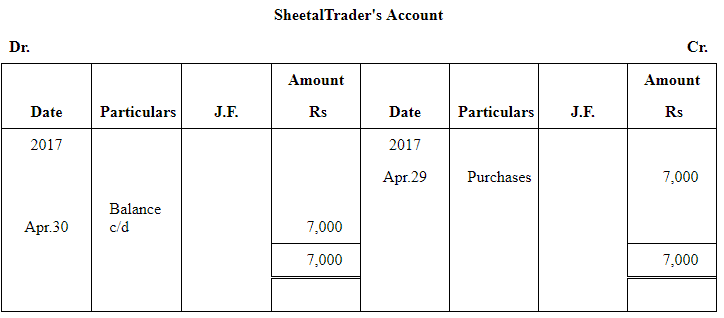

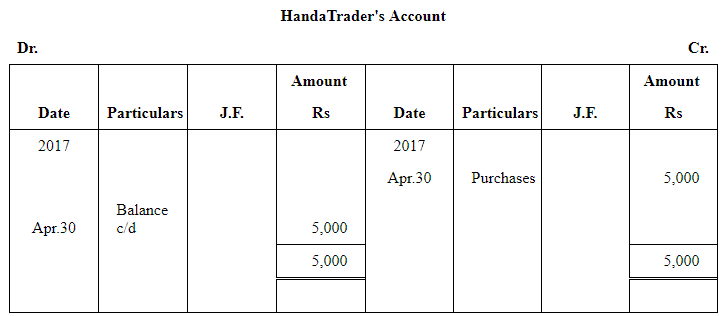

Question 18: The following balances of ledger of M/s Marble Traders on April 01, 2017

Journalise the above transactions and post them to the ledger.

Answer:

Explanation: The transactions are first journalised (recorded as debit and credit entries) and then posted to respective ledger accounts. Each ledger shows debits on the left and credits on the right; after posting all entries, balances are extracted. This process ensures the double-entry principle is maintained and helps prepare trial balance and financial statements.

FAQs on NCERT Solution (Part - 2) Recording of Transactions-II

| 1. What is the purpose of recording transactions in accounting? |  |

| 2. What are the different methods of recording transactions? | |

| 3. What are some common examples of transactions that need to be recorded? | |

| 4. How can errors in recording transactions be rectified? | |

| 5. Why is it important to maintain proper documentation for recorded transactions? | |