NCERT Solution (Part - 1) - Bank Reconciliation Statement

Short Answers

Page No. : 181

Question 1: State the need for the preparation of bank reconciliation statement?

Answer :

The need to prepare Bank Reconciliation Statement are given below.

1. It helps to locate and correct errors and omissions made in the Cash Book and the Pass Book.

2. It identifies uncleared cheques - cheques already recorded (debited) in the Cash Book but not yet shown in the Pass Book.

3. It helps detect and prevent misappropriation or embezzlement of funds from the bank account.

4. It measures the accuracy of bank transactions recorded in the Cash Book and highlights discrepancies for correction.

5. It enables the preparation of a corrected (adjusted) Cash Book so that the true bank balance can be shown in the books.

Question 2: What is a bank overdraft?

Answer: Bank overdraft is a liability of the account holder. It arises when withdrawals from the bank exceed the available balance, resulting in a negative balance. In other words, bank overdraft is the amount by which withdrawals exceed deposits and must be repaid to the bank.

Question 3: Briefly explain the statement 'wrongly debited by the bank' with the help of an example.

Answer: When an amount is wrongly debited in the Pass Book, the bank has reduced the customer's balance in error. Typical causes are:

1. Two account holders have similar names. For example, a cheque of Rs 2,000 issued by Mr. Prem Singh was wrongly debited to Mr. Prem Kumar's account.

2. A person holds more than one account with the same bank, and the transaction is posted to the wrong account. For example, a cheque of Rs 1,000 from a Current Account is wrongly debited to the Savings Account.

3. Amounts are recorded incorrectly. For example, a payment of Rs 2,000 is accidentally debited in the Pass Book as Rs 20,000.

Question 4: State the causes of difference occurred due to time lag.

Answer: Differences due to time lag arise because transactions are recorded by the business and the bank on different dates. Common causes are:

1. Issued cheques not presented for payment in the same period

A cheque is recorded in the Cash Book on its date of issue, but the bank debits the account only when the cheque is presented for payment. If the cheque is presented later, the Pass Book will show the debit in a later period, and balances will differ temporarily.

2. Deposited cheques not yet cleared

A cheque is entered in the Cash Book when deposited, but the bank credits it only on clearance. If the cheque is deposited near the period end and clears later, the Pass Book will show the credit later, causing a timing difference between balances.

Question 5: Briefly explain the term favourable balance as per cash book

Answer: A favourable balance (also called a debit balance in the Cash Book) is an asset for the account holder. It exists when total deposits (debits) exceed total withdrawals (credits) in the bank column of the Cash Book. In simple terms, it is the excess of receipts over payments in the bank account.

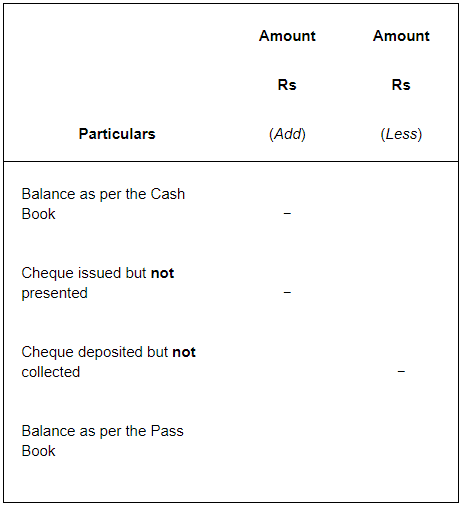

Question 6: Enumerate the steps to ascertain the correct cash book balance.

Answer: To ascertain the correct bank balance as per the Cash Book, prepare an adjusted (corrected) Cash Book by following these steps.

Step 1: Note the bank balance as shown in the Cash Book.

Step 2: Rectify all errors made in the Cash Book entries.

Step 3: Enter in the debit side of the Cash Book those transactions that appear only on the credit side of the Pass Book (for example, direct receipts recorded by the bank).

Step 4: Enter in the credit side of the Cash Book those transactions that appear only on the debit side of the Pass Book (for example, bank charges debited by the bank).

Step 5: Total and balance the Cash Book. The resulting figure is the amended cash book balance, which is used to prepare the Bank Reconciliation Statement.

Page No. : 181

Long answers :

Question 1: What is a bank reconciliation statement? Why is it prepared?

Answer: Bank Reconciliation Statement is a statement prepared to explain the differences between the bank balance shown by the Cash Book and the balance shown by the Pass Book on a particular date. It identifies and reconciles timing differences, omissions and errors so that both records agree.

In practice, an individual or organisation records bank transactions in two records: the Cash Book (internal book) and the bank's Pass Book (bank's record). Because many transactions pass through the bank and because recording times and responsibilities differ, the two balances may not match. Typical reasons include the following.

1. A cheque deposited and recorded in the Cash Book may be collected by the bank only later.

2. A cheque issued and recorded in the Cash Book may be presented to the bank for payment in a later period and so appears in the Pass Book later.

3. Items such as interest credited by the bank or bank charges are recorded first in the Pass Book and may be missing from the Cash Book until entered.

A Bank Reconciliation Statement is prepared whenever these balances do not agree, to locate and correct errors and to show the true bank balance in the books.

Specimen of Bank Reconciliation Statement

The need for preparation of the Bank Reconciliation Statement is explained below.

1. It helps in finding out the errors and omissions committed in the Cash Book and in the Pass Book.

2. It shows uncleared cheques that have been debited in the Cash Book but have not yet been recorded in the Pass Book.

3. It helps in checking the embezzlement of money from the bank account.

4. It helps in measuring the accuracy of transactions recorded in the Cash Book.

5. It facilitates the preparation of a revised Cash Book that reflects the true bank balance.

Question 2: Explain the reasons where the balance shown by the bank passbook does not agree with the balance as shown by the bank column of the cash book.

Answer: The balance per the Pass Book may differ from the balance per the Cash Book for three main reasons: timing differences, transactions recorded only in the Pass Book, and errors or omissions.

1. Differences due to time lag: When the date of recording in the Cash Book is different from the date recorded by the bank, temporary differences arise. Examples are:

2. Cheques issued but presented later or not yet presented: A cheque is recorded in the Cash Book on the date of issue. If the payee presents it to the bank later, the bank will debit the account on presentation date, causing a mismatch until the cheque is presented.

3. Cheques deposited but not yet cleared: A deposited cheque appears in the Cash Book when deposited, but the bank credits it only on clearance. If clearance occurs after the period end, the Pass Book will not yet show the credit.

4. Transactions recorded only in the Pass Book: Some transactions are first recorded by the bank and not immediately entered in the Cash Book. These include:

- Bank charges, service charges or penalties debited by the bank but not yet recorded in the Cash Book.

- Dishonour of bills or cheques previously discounted or collected by the bank.

- Interest charged on overdraft.

- Direct payments made by the bank on the account holder's instruction.

Examples of Pass Book-only credits (increase Pass Book balance):

- Interest or dividend collected by the bank on behalf of the customer but not yet entered in the Cash Book.

- Amounts deposited directly into the bank by customers (third parties).

- Interest credited by the bank.

5. Errors and omissions: Mistakes in posting amounts, double recording, wrong account posting (e.g., a current account payment posted to a savings account) or clerical errors in either book will cause differences. All such items must be identified and corrected to reconcile balances.

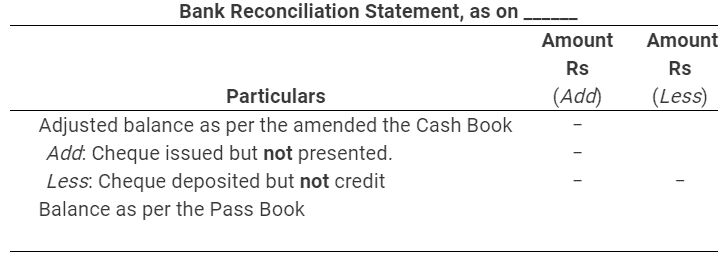

Question 3: Explain the process of preparing bank reconciliation statement with amended cash balance.

Answer: Bank Reconciliation Statement may be prepared after first amending (adjusting) the Cash Book. The steps are as follows:

Step 1: Note the bank balance as per the Cash Book.

Step 2: Rectify all errors discovered in the Cash Book.

Step 3: Enter in the debit side of the Cash Book those items that are in the credit of the Pass Book only (for example, interest credited by bank or direct receipts).

Step 4: Enter in the credit side of the Cash Book those items that are in the debit of the Pass Book only (for example, bank charges, dishonoured cheques).

Step 5: After these entries the amended Cash Book balance (or overdraft) is determined. Use this amended balance to prepare the Bank Reconciliation Statement that reconciles the amended Cash Book balance with the Pass Book balance.

The proforma of a Bank Reconciliation Statement prepared from the amended Cash Book balance is shown below.

Numerical questions :

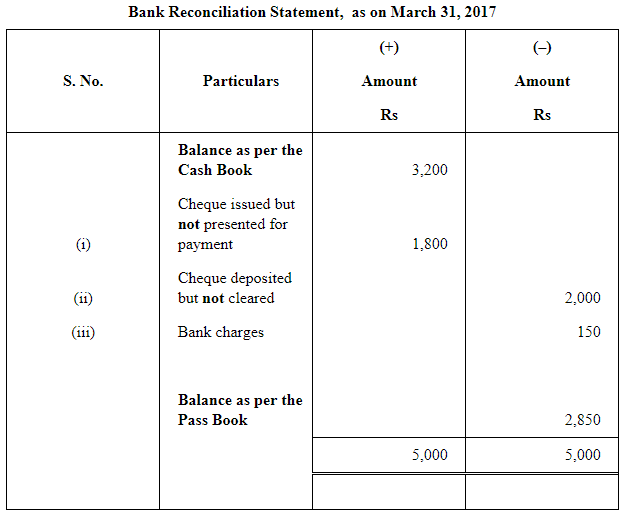

Question 1 : From the following particulars, prepare a, bank reconciliation statement as at March 31, 2017.

(i) Balance as per cash book Rs 3,200

(ii) Cheque issued but not presented for payment Rs 1,800

(iii) Cheque deposited but not collected upto March 31, 2017 Rs 2,000

(iv) Bank charges debited by bank Rs 150

Answer :

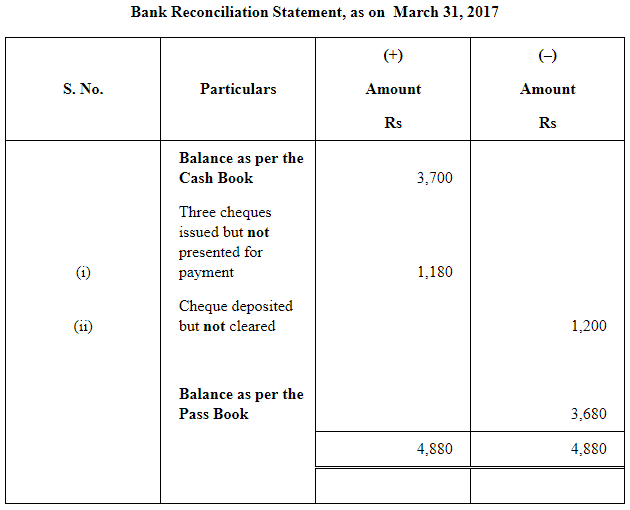

Question 2 : On March 31 2017 the cash book showed a balance of Rs 3,700 as cash at bank, but the bank passbook made up to same date showed that cheques for Rs 700, Rs 300 and Rs 180 respectively had not presented for payment, Also, cheque amounting to Rs 1,200 deposited into the account had not been credited. Prepare a bank reconciliation statement.

Answer :

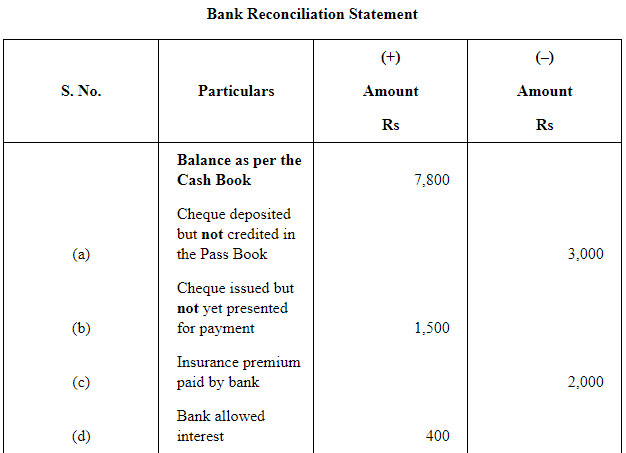

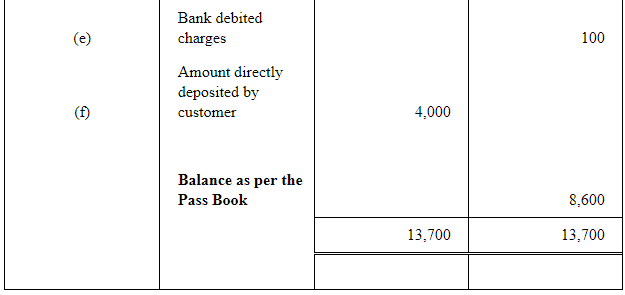

Question 3 : The cash book shows a bank balance of Rs 7,800. On comparing the cash book with passbook the following discrepancies were noted:

(a) Cheque deposited in bank but not credited Rs 3,000

(b) Cheque issued but not yet present for payment Rs 1,500

(c) Insurance premium paid by the bank Rs 2,000

(d) Bank interest credit by the bank Rs 400

(e) Bank charges Rs 100

(d) Directly deposited by a customer Rs 4,000

Answer :

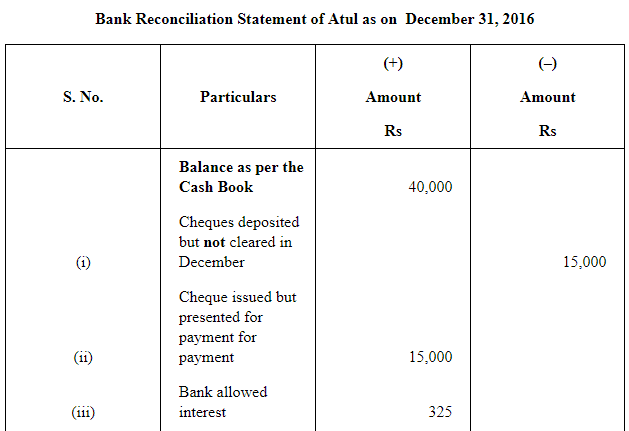

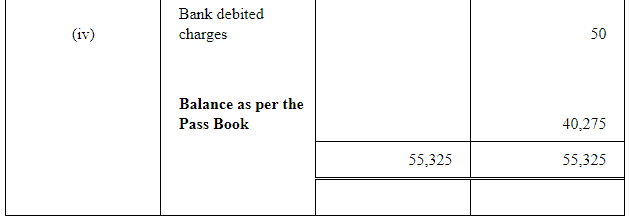

Question 4 : Bank balance of Rs 40,000 showed by the cash book of Atul on December 31, 2016. It was found that three cheques of Rs 2,000, Rs 5,000 and Rs 8,000 deposited during the month of December were not credited in the passbook till January 02, 2017. Two cheques of Rs 7,000 and Rs 8,000 issued on December 28, were not presented for payment till January 03, 2017. In addition to it bank had credited Atul for Rs 325 as interest and had debited him with Rs 50 as bank charges for which there were no corresponding entries in the cash book.

Prepare a bank reconciliation statement as on December 31, 2016.

Answer :

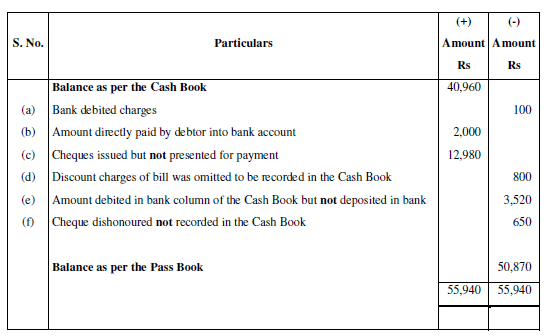

Page No 182:

Question 5 : On comparing the cash book with passbook of Naman it is found that on March 31, 2017, bank balance of Rs 40,960 showed by the cash book differs from the bank balance with regard to the following:

(a) | Bank charges Rs 100 on March 31, 2017, are not entered in the cash book. |

(b) | On March 21, 2017, a debtor paid Rs 2,000 into the company's bank in settlement of his account, but no entry was made in the cash book of the company in respect of this. |

(c) | Cheques totaling Rs 12,980 were issued by the company and duly recorded in the cash book before March 31, 2017, but had not been presented at the bank for payment until after that date. |

(d) | A bill for Rs 6,900 discounted with the bank is entered in the cash book with recording the discount charge of Rs 800. |

(e) | Rs 3,520 is entered in the cash book as paid into bank on March 31st, 2017, but not credited by the bank until the following day. |

(f) | No entry has been made in the cash book to record the dishonour or on March 15, 2017 of a cheque for Rs 650 received from Bhanu. |

Prepare a reconciliation statement as on March 31, 2017.

Answer :

FAQs on NCERT Solution (Part - 1) - Bank Reconciliation Statement

| 1. What is a Bank Reconciliation Statement? |  |

| 2. Why is Bank Reconciliation Statement important? | |

| 3. What are the steps involved in preparing a Bank Reconciliation Statement? | |

| 4. How often should a company prepare a Bank Reconciliation Statement? | |

| 5. What are the benefits of preparing a Bank Reconciliation Statement? | |