NCERT Solution - Trial Balance and Rectification of Errors

Short Question Answers

Q1: State the meaning of a trial balance?

Ans: A trial balance is a bookkeeping statement in which the balances of all ledger accounts are listed under two columns - debit and credit - to verify that total debits equal total credits. It is usually prepared at the end of an accounting period to check the arithmetical accuracy of ledger postings and to provide a basis for preparing final accounts. According to William Pickles, "The statement prepared using ledger balances at the end of the fiscal year to determine whether the debit total agrees with the credit total is known as a trial balance."

Q2: Give two examples of errors of principle?

Ans: Errors of principle occur when a transaction is recorded in violation of basic accounting principles. Two examples are as follows:

- Recording capital expenditure as revenue expenditure: For example, charging the cost of purchasing furniture to the Repairs Account instead of Furniture Account. This violates the matching principle and misstates profit and assets.

- Classifying an asset as an expense (or vice versa): For example, treating the purchase of machinery as a purchase of goods (recording under Purchases) instead of recording it as a fixed asset. This causes both the profit and balance sheet items to be incorrect.

Q3: Give two examples of errors of commission?

Ans: The following are two examples of errors of commission and brief notes on their effect:

- Incorrect amount posted: Mohit purchased goods for Rs. 9,000 but the amount posted to Mohit's account was Rs. 900. This understates Mohit's balance and the purchases account, causing imbalance in the ledger.

- Posting to the wrong account or wrong side: Ram sold goods worth Rs. 5,000 but the entry was posted on the debit side of Ram's account instead of the credit side. This reverses the position of Ram's account and distorts both debtor/creditor balances and trial balance totals.

Q4: What are the methods of preparing trial balance?

Ans: The common methods of preparing a trial balance are:

- Balance method: Only the closing balances (debit or credit) of ledger accounts are shown in the trial balance. Debit balances are placed in the debit column and credit balances in the credit column.

- Total method: The totals of the debit and credit sides of each ledger account are entered in the trial balance; adjustments are then made to show balances if required.

- Total-and-balance method: Both the totals and the balances of each account are shown side by side in the trial balance. This gives fuller information about individual accounts while preparing the trial balance.

Q5: What are the steps taken by an accountant to locate the errors in the trial balance?

Ans: An accountant usually follows these steps to locate errors in the trial balance:

- Re-check the accuracy of additions on the debit and credit columns of the trial balance.

- Compare the difference with ledger balances to see whether any single account balance equals the difference.

- Verify the opening balances brought down from the previous period.

- Recast the balances of ledger accounts and check that balances are correctly carried forward.

- Trace postings from books of original entry (journal, sales book, purchase book) to the ledger to ensure amounts and sides are correctly posted.

- If the error cannot be found quickly, transfer the difference to a temporary account called suspense account and continue investigating; correct entries will eliminate the suspense balance when located.

Q6: What is a suspense account? Is it necessary that is suspense account will balance off after rectification of the errors detected by the accountant? If not, then what happens to the balance still remaining in suspense account?

Ans: A suspense account is a temporary account used to record the difference when the totals of the debit and credit columns of the trial balance do not agree. It allows preparation of final accounts while errors are being located.

It is not necessary that the suspense account will immediately balance off after the first round of rectifications. The suspense account is closed only when all the errors that caused the difference have been located and corrected. If some errors remain unrectified, the balance will continue to remain in the suspense account until further corrections are made.

Q7: What kinds of errors would cause difference in the trial balance. Also list examples that would not be revealed by a trial balance?

Ans: Errors that would cause a difference in the trial balance include:

i. Errors of omission (partial or complete omission of posting),

ii. Errors of commission (wrong amount or wrong account posting),

iii. Errors of principle (wrong classification between asset, expense, revenue, etc.),

iv. Errors in casting or carrying forward balances in subsidiary books or ledger.

Typical situations that produce a difference are:

i. Undercast or overcast totals in subsidiary books (sales book, purchases book).

ii.Failure to post one side of a transaction to the ledger.

iii.Posting on the wrong side of an account.

iv. Recording wrong amounts while posting.

Examples of errors that would NOT be revealed by a trial balance (i.e., trial balance may still agree):

- Omission of an entire transaction from the books (neither debit nor credit recorded).

- Compensating errors where one mistake is offset by another mistake of equal amount (e.g., understating one expense by Rs. 1,000 and overstating another expense by Rs. 1,000).

- Posting equal amounts to wrong accounts but on correct sides (classification errors or principle errors) so totals still agree.

- Errors in original entry if both ledger postings have been made equally wrong so that debit and credit totals remain equal.

Q8: State the limitations of trial balance?

Ans: The trial balance has the following limitations:

- It is not conclusive proof of accuracy: Even when the trial balance totals agree, there may still be errors in the books (for example, compensating errors or complete omission of transactions).

- It cannot detect errors in books of original entry: Mistakes made while recording in books of original entry (journal, purchases book, sales book) may not be revealed if corresponding ledger postings still keep totals equal.

- It does not show operational or classification errors: Transactions recorded in wrong accounts (errors of principle) or transactions entirely omitted will not always affect the trial balance totals, so the trial balance cannot reveal such errors.

Long Question Answers

Q1: Describe the purpose for the preparation of trial balance.

Ans: The main purposes of preparing a trial balance are:

- To check the arithmetical accuracy of ledger postings - whether total debits equal total credits.

- To help detect posting errors in ledger accounts so they can be corrected before preparing final accounts.

- To aid in summarising ledger accounts in a single statement which is useful for account analysis.

- To facilitate the preparation of final accounts (Trading Account, Profit and Loss Account, and Balance Sheet).

- To indicate the adjustments (like accruals, prepaid expenses, depreciation) that are required before final accounts are drawn up.

Q2: Explain errors of principle and give two examples with measures to rectify them.

Ans: An error of principle occurs when a transaction is recorded in breach of accounting principles - for example, recording a capital expenditure as revenue or misclassifying assets and expenses. Two examples with rectification measures are:

- Capital expenditure recorded as revenue expense: If the purchase of furniture is debited to Repairs Account (revenue), it should be corrected by debiting Furniture Account and crediting Repairs Account for the amount mistakenly recorded. Make a journal entry transferring the amount from Repairs to Furniture.

- Asset recorded as purchase of goods: If purchase of machinery is recorded in Purchases Account, it should be rectified by debiting Machinery Account and crediting Purchases Account (or reversing the incorrect entry and recording the correct one) so that the asset is recognised on the balance sheet.

Q3: Explain the errors of commission and give two examples with measures to rectify them.

Ans: Errors of commission are mistakes due to carelessness while recording transactions - such as posting wrong amounts, posting to the wrong account, or incorrect balancing. Examples and rectifications:

(i) Example 1: Mr. X's sales of Rs. 10,000 were recorded as Rs. 1,000. As a result, Mr. X's account has been understated by Rs. 9,000. Rectification: Pass an adjusting entry to debit Debtors (Mr. X) and credit Sales by Rs. 9,000, or directly correct the ledger posting so that Mr. X's account shows Rs. 10,000.

(ii) Example 2: The purchases book was overcast by Rs. 10,000. This can be corrected as follows:

(a) If discovered before preparing the trial balance: reduce Purchases Account by Rs. 10,000 (i.e., credit Purchases).

(b) If discovered after preparing the trial balance: pass a journal entry to credit Purchases and debit Suspense (if difference was put to Suspense), or make an appropriate rectification entry to reverse the overcast amount.

Q4: What are the different types of errors that are usually committed in recording business transaction.

Ans: The common types of errors are:

- Errors of Omission: When a transaction is completely omitted from the books of account - neither debit nor credit recorded.

- Errors of Commission: Errors caused by carelessness in recording, such as wrong amount posted, posting to the wrong account, or incorrect balancing.

Q5: As an accountant of a company, you are disappointed to learn that the totals in your new trial balance are not equal. After going through a careful analysis, you have discovered only one error. Specifically, the balance of the Office Equipment account has a debit balance of Rs. 15,600 on the trial balance. However, you have figured out that a correctly recorded credit purchase of pendrive for Rs. 3,500 was posted from the journal to the ledger with a Rs. 3,500 debit to Office Equipment and another Rs. 3,500 debit to creditors accounts. Answer each of the following questions and present the amount of any misstatement :

(a) Is the balance of the office equipment account overstated, understated, or correctly stated in the trial balance?

(b) Is the balance of the creditors account overstated, understated, or correctly stated in the trial balance?

(c) Is the debit column total of the trial balance overstated, understated, or correctly stated?

(d) Is the credit column total of the trial balance overstated, understated, or correctly stated?

(e) If the debit column total of the trial balance is Rs. 2,40,000 before correcting the error, what is the total of credit column.

Ans: The pendrive purchase was correctly credit-purchased (creditors should be credited), but the ledger entries made were both debits. Effects are as follows:

(a) Office Equipment is overstated by Rs. 3,500 because it was debited though it should have been debited only once (the other side should have been credit to creditors).

(b) The creditors account is understated by Rs. 3,500 because it should have been credited for Rs. 3,500 but was instead debited for Rs. 3,500 (a net error of Rs. 7,000 relative to the correct position).

(c) The debit column total of the trial balance is correctly stated in the sense that the erroneous debits were included, but comparing to the correct totals it shows an excess equal to the mistake on the credit side; however as per the specific framing in the solution, it is stated as correctly stated prior to correction.

(d) The credit column total is understated by Rs. 7,000 (because creditors should have been credited by Rs. 3,500 instead of debited, causing a shortfall of Rs. 7,000 on the credit side relative to correct entries).

(e) If the debit column total is Rs. 2,40,000 before correction, the credit total shown would be Rs. 2,33,000 (i.e., Rs. 2,40,000 - Rs. 7,000), because the credit side is understated by Rs. 7,000.

Numerical Question Answers

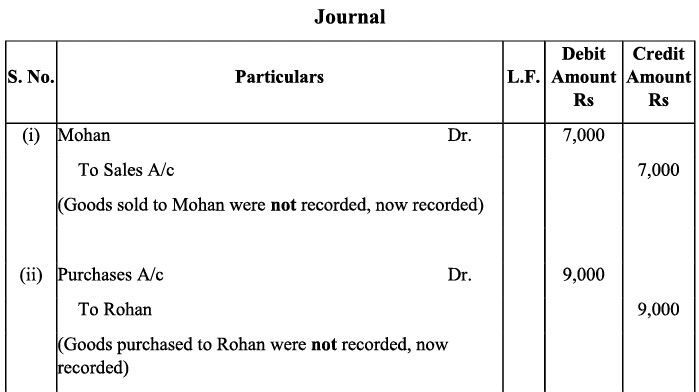

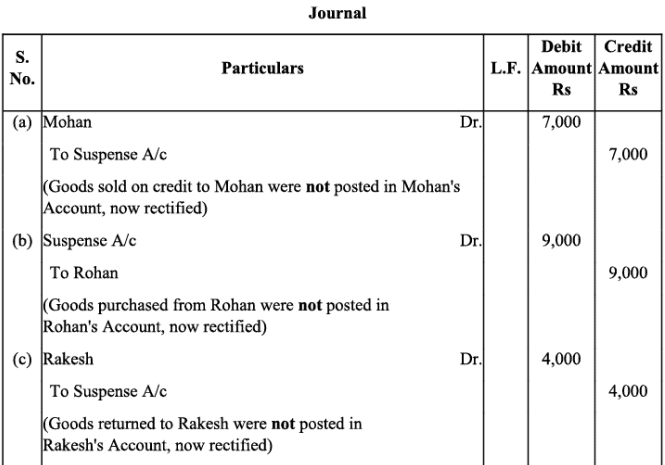

Q1: Rectify the following errors:

(i) Credit sales to Mohan Rs. 7,000 were not recorded.

(ii) Credit purchases from Rohan Rs. 9,000 were not recorded.

(iii) Goods returned to Rakesh Rs. 4,000 were not recorded.

(iv) Goods returned from Mahesh Rs. 1,000 were not recorded.

Ans:

Note: The images above show the journal entries and ledger adjustments required to record the omitted transactions: (i) Credit Sales to Mohan - debit Debtors (Mohan) and credit Sales Rs. 7,000; (ii) Credit Purchases from Rohan - debit Purchases and credit Creditors (Rohan) Rs. 9,000; (iii) Goods returned to Rakesh - debit Sales Returns and credit Debtors (Rakesh) Rs. 4,000; (iv) Goods returned from Mahesh - debit Creditors (Mahesh) and credit Purchase Returns Rs. 1,000.

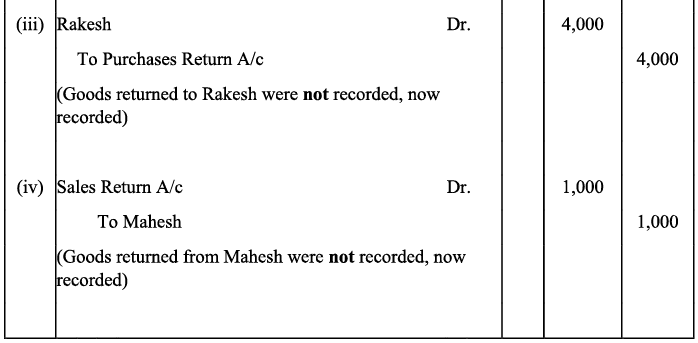

Q2: Rectify the following errors:

(i) Credit sales to Mohan Rs. 7,000 were recorded as Rs.700.

(ii) Credit purchases from Rohan Rs. 9,000 were recorded as Rs. 900.

(iii) Goods returned to Rakesh Rs. 4,000 were recorded as Rs. 400.

(iv) Goods returned from Mahesh Rs. 1,000 were recorded as Rs.100.

Ans:

Note: The image shows the correcting journal entries. Each error is corrected by adjusting the concerned debtor/creditor and sales/purchases or returns accounts for the difference (for example, credit sales to Mohan: additional Rs. 6,300 must be credited to Sales and debited to Mohan).

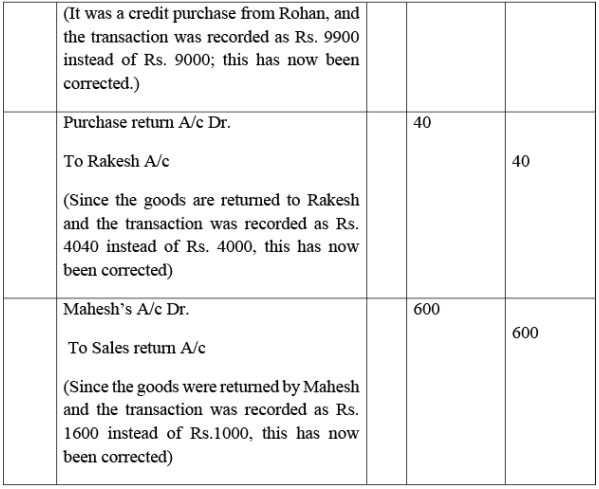

Q3: Rectify the following errors:

(i) Credit sales to Mohan Rs. 7,000 were recorded as Rs.7,200.

(ii) Credit purchases from Rohan Rs. 9,000 were recorded as Rs. 9,900.

(iii) Goods returned to Rakesh Rs. 4,000 were recorded as Rs. 4,040.

(iv) Goods returned from Mahesh Rs. 1,000 were recorded as Rs.1,600.

Ans:

Note: The images show adjustment entries to correct the overstatements: post contra entries for the excess amounts to bring each account to its correct figure (e.g., for Mohan debit/credit difference of Rs. 200, adjust Sales and Debtor accordingly).

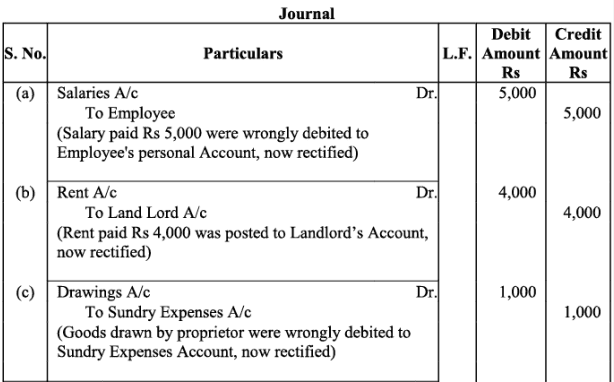

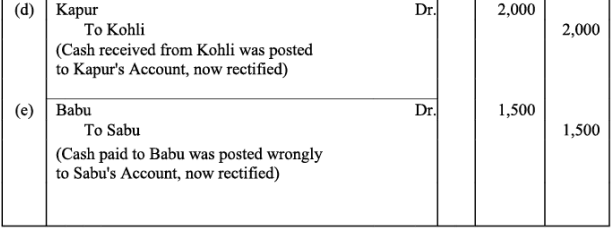

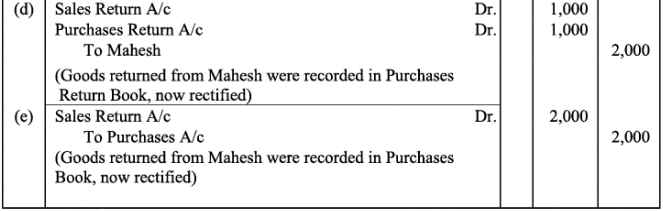

Q4:Rectify the following errors:

(a)Salary paid Rs. 5,000 was debited to employee's personal account.

(b)Rent Paid Rs. 4,000 was posted to landlord's personal account.

(c)Goods withdrawn by proprietor for personal use Rs. 1,000 were debited to sundry expenses account.

(d)Cash received from Kohli Rs. 2,000 was posted to Kapur's account.

(e)Cash paid to Babu Rs. 1,500 was posted to Sabu's account.

Ans:

Note: The shown images illustrate rectifying journal entries. For example, salary paid incorrectly debited to personal account - credit Cash and debit Salary Account; correct the personal account by reversing the wrong debit and posting the correct debit to Salary.

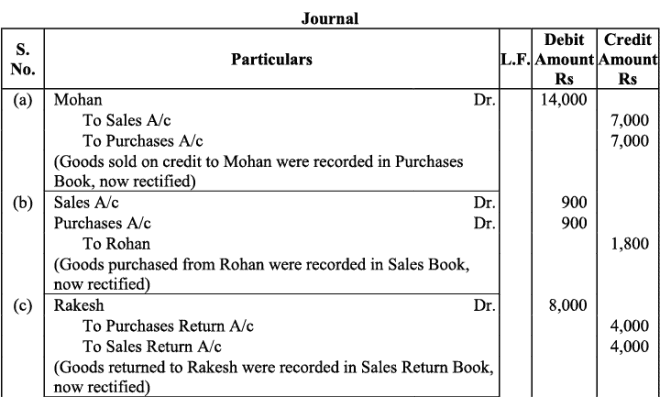

Q5:Rectify the following errors:

(a)Credit Sales to Mohan Rs. 7,000 were recorded in purchases book.

(b)Credit Purchases from Rohan Rs. 9,00 were recorded in sales book.

(c)Goods returned to Rakesh Rs. 4,000 were recorded in the sales return book.

(d)Goods returned from Mahesh Rs. 1,000 were recorded in purchases return book.

(e)Goods returned from Nahesh Rs. 2,000 were recorded in purchases book.

Ans:

Note: Rectifications require passing journal entries which transfer wrongly recorded amounts to their correct accounts (sales to purchases and vice versa) and correct the affected debtor/creditor accounts. The images show these correcting entries and ledger adjustments.

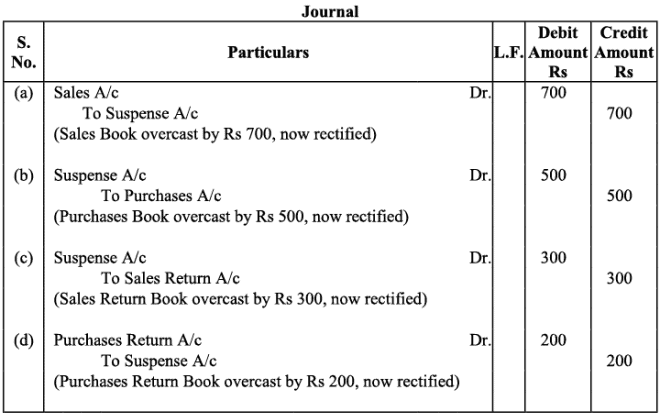

Q6:Rectify the following errors:

(a)Sales book overcast by Rs. 700.

(b)Purchases book overcast by Rs. 500.

(c)Sales return book overcast by Rs. 300.

(d)Purchase return book overcast by Rs. 200.

Ans:

Note: The image contains the journal entries to reduce the overstated totals: credit Sales by Rs. 700, credit Purchases by Rs. 500, debit Sales Returns by Rs. 300, and debit Purchase Returns by Rs. 200 (or adjust Suspense if trial balance was already prepared).

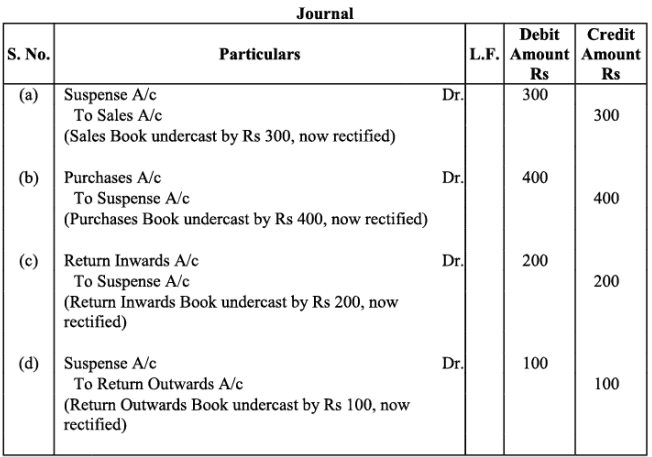

Q7:Rectify the following errors:

(a)Sales book undercast by Rs.300.

(b)Purchases book undercast by Rs.400.

(c)Return Inwards book undercast by Rs.200.

(d)Return outwards book undercast by Rs. 100.

Ans:

Note: The image shows entries to increase the understated totals - debit Debtors/Creditors and adjust Sales/Purchases or Returns accounts to reflect the correct totals.

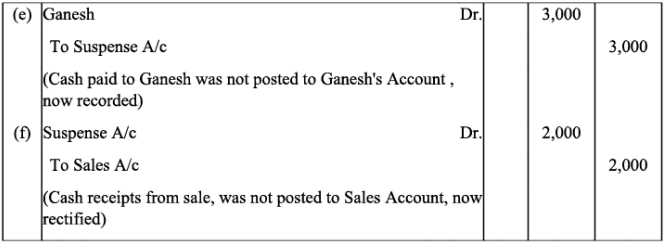

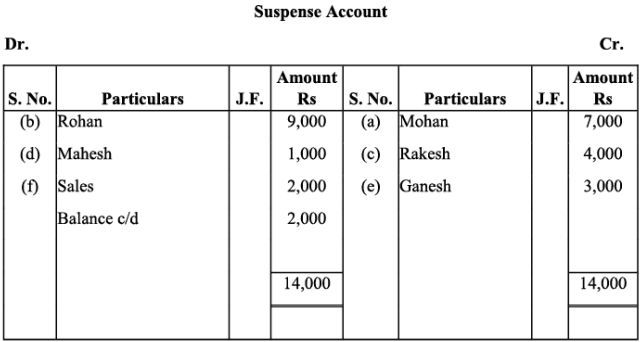

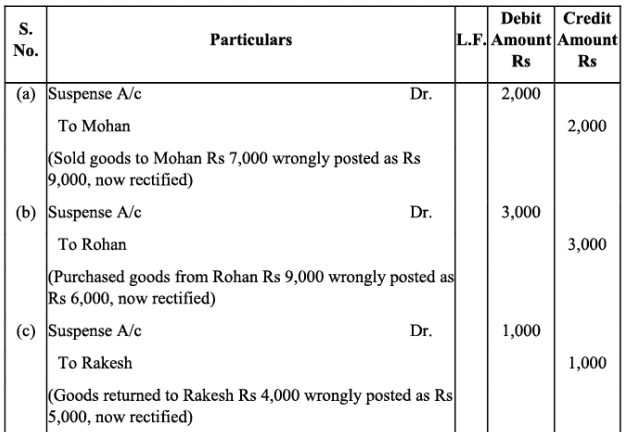

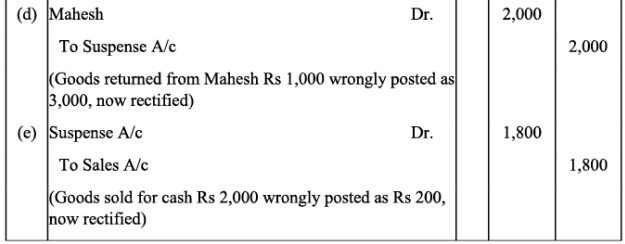

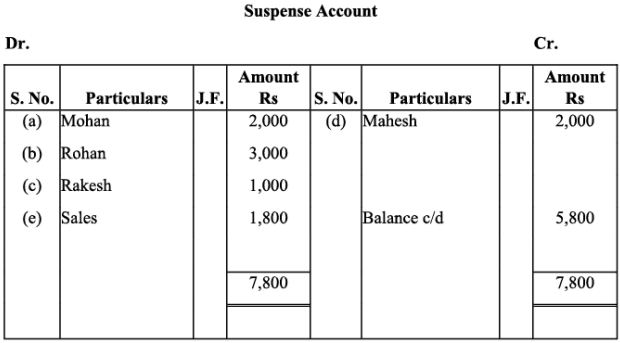

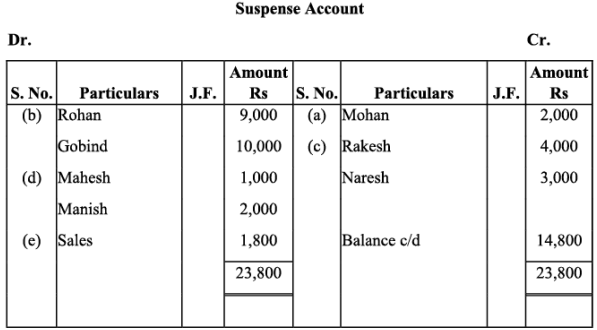

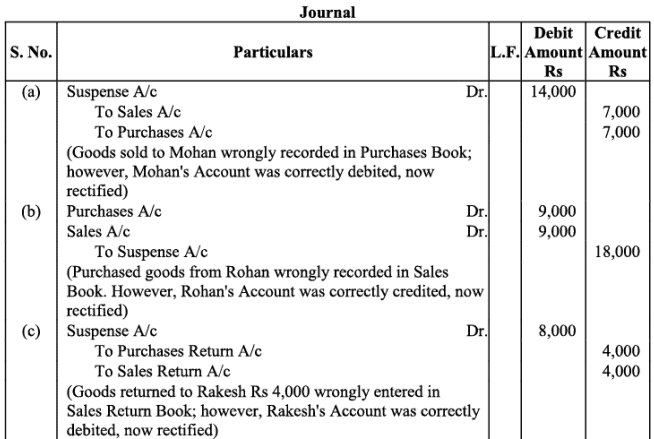

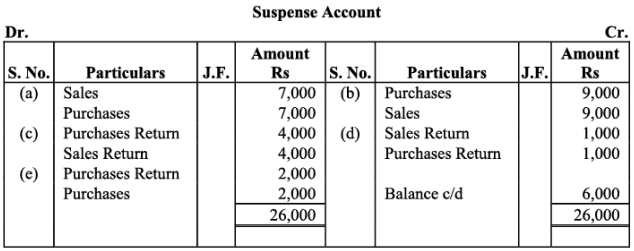

Q8: Rectify the following errors and ascertain the amount of difference in trial balance by preparing suspense account:

(a) Credit sales to Mohan Rs. 7,000 were not posted.

(b) Credit purchases from Rohan Rs. 9,000 were not posted.

(c) Goods returned to Rakesh Rs. 4,000 were not posted.

(d) Goods returned from Mahesh Rs. 1,000 were not posted.

(e) Cash paid to Ganesh Rs. 3,000 was not posted.

(f) Cash sales Rs. 2,000 were not posted.

Ans:

Note: The series of images display the correcting entries and the Suspense Account prepared to show the difference arising from these omissions. Each omitted posting is rectified and the net difference is shown in the Suspense Account column until fully adjusted.

Q9: Rectify the following errors and ascertain the amount of difference in trial balance by preparing suspense account:

(a) Credit sales to Mohan Rs. 7,000 were posted as Rs. 9,000.

(b) Credit purchases from Rohan Rs. 9,000 were posted as Rs. 6,000.

(c) Goods returned to Rakesh Rs. 4,000 were posted as Rs. 5,000.

(d) Goods returned from Mahesh Rs. 1,000 were posted as Rs. 3,000.

(e) Cash sales Rs. 2,000 were posted as Rs. 200.

Ans:

Note: The images illustrate the correcting journal entries for each misposted amount and the Suspense Account showing the resultant difference until all corrections are made.

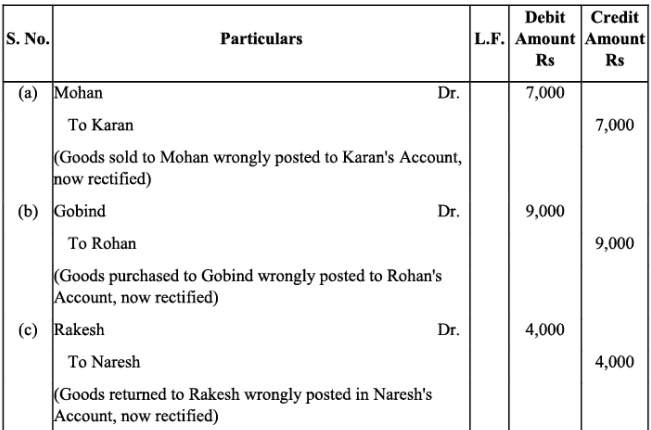

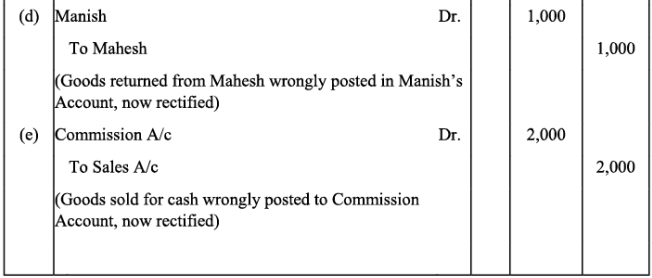

Q10: Rectify the following errors:

(a) Credit sales to Mohan Rs. 7,000 were posted to Karan.

(b) Credit purchases from Rohan Rs. 9,000 were posted to Gobind.

(c) Goods returned to Rakesh Rs. 4,000 were posted to Naresh.

(d) Goods returned from Mahesh Rs. 1,000 were posted to Manish.

(e) Cash sales Rs. 2,000 were posted to commission account.

Ans:

Note: The images show the rectifying entries to transfer amounts from wrongly credited accounts to the correct debtor/creditor or sales/commission accounts and to correct the ledger balances.

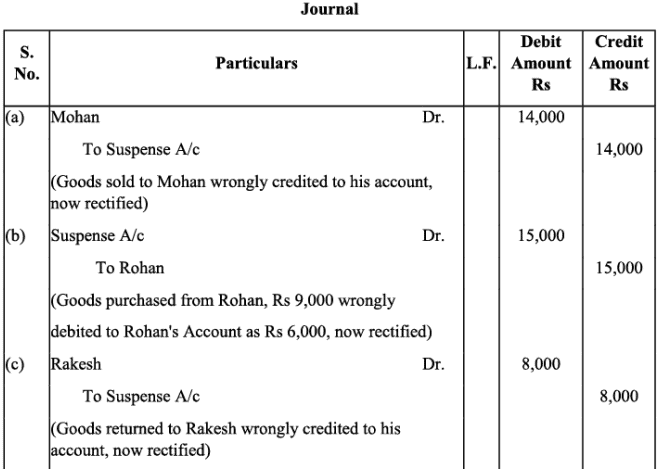

Q11: Rectify the following errors assuming that a suspense account was opened. Ascertain the difference in trial balance:

(a) Credit sales to Mohan Rs. 7,000 were posted to the credit of his account.

(b) Credit purchases from Rohan Rs. 9,000 were posted to the debit of his account as Rs. 6,000.

(c) Goods returned to Rakesh Rs. 4,000 were posted to the credit of his account.

(d) Goods returned from Mahesh Rs. 1,000 were posted to the debit of his account as Rs. 2,000.

(e) Cash sales Rs. 2,000 were posted to the debit of sales account as Rs. 5,000.

Ans:

Note: The images display the correcting journal entries and the Suspense Account exhibiting the net difference after adjustments for the mispostings. Each error is corrected so that each account reflects the correct debit or credit.

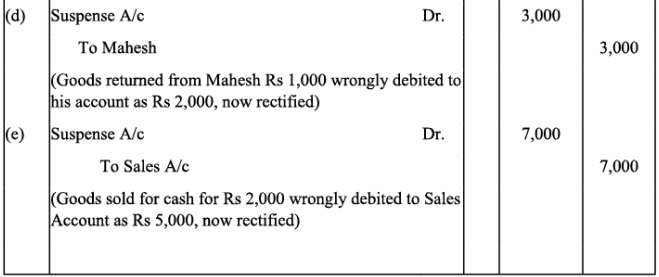

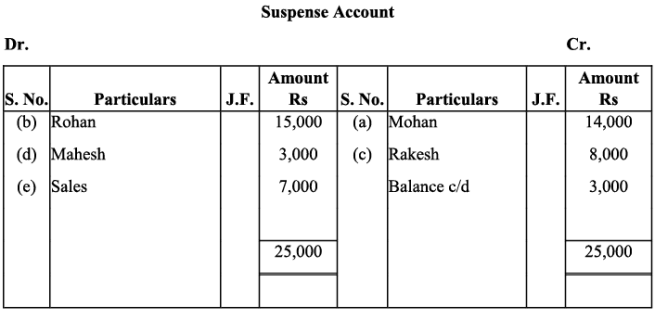

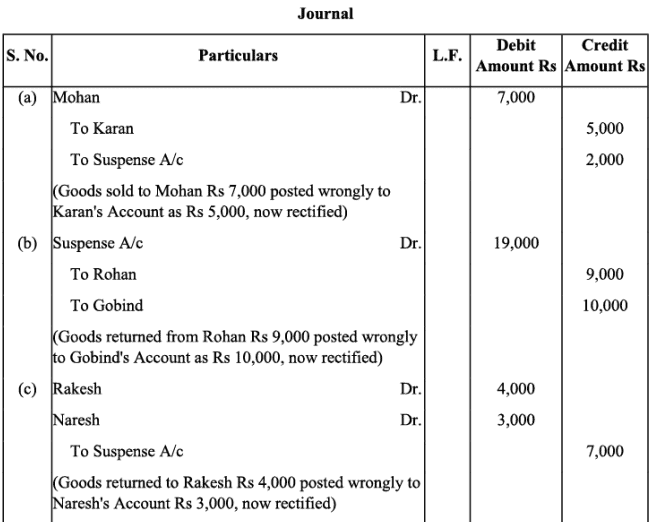

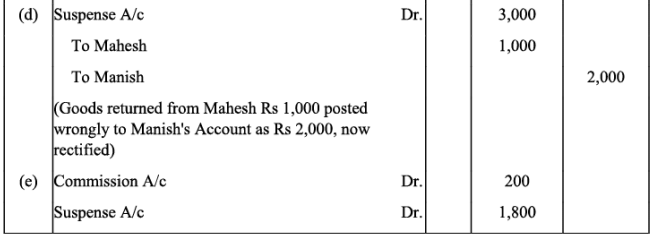

Q12: Rectify the following errors assuming that a suspense account was opened. Ascertain the difference in trial balance:

(a) Credit sales to Mohan Rs. 7,000 were posted to Karan as Rs. 5,000.

(b) Credit purchases from Rohan Rs. 9,000 were posted to the debit of Gobind as Rs. 10,000.

(c) Goods returned to Rakesh Rs. 4,000 were posted to the credit of Naresh as Rs. 3,000.

(d) Goods returned from Mahesh Rs. 1,000 were posted to the debit of Manish as Rs. 2,000.

(e) Cash sales Rs. 2,000 were posted to commission account as Rs. 200.

Ans:

Note: Corrections involve reversing the wrong postings and recording the proper entries; the sequence of images shows each journal entry and the Suspense Account summarising the net impact.

Q13: Rectify the following errors assuming that a suspense account was opened. Ascertain the difference in trial balance:

(a) Credit sales to Mohan Rs. 7,000 were recorded in Purchase Book. However, Mohan's account was correctly debited.

(b) Credit purchases from Rohan Rs. 9,000 were recorded in Sales Book. However, Rohan's account was correctly credited.

(c) Goods returned to Rakesh Rs. 4,000 were recorded in Sales Return Book. However, Rakesh's account was correctly debited.

(d) Goods returned from Mahesh Rs. 1,000 were recorded through Purchases Return Book. However, Mahesh's account was correctly credited.

(e) Goods returned to Naresh Rs. 2,000 were recorded through Purchases Book. However, Naresh's account was correctly debited.

Ans:

Q14: Rectify the following errors:

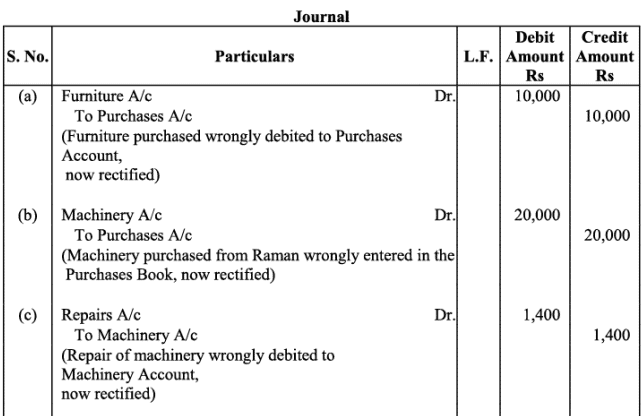

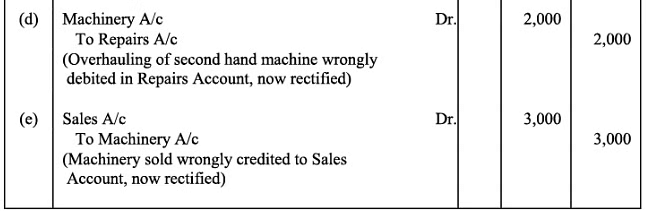

(a) Furniture purchased for Rs. 10,000 was wrongly debited to Purchases Account.

(b) Machinery purchased on credit from Raman for Rs. 20,000 was recorded through Purchases Book.

(c) Repairs on machinery Rs. 1,400 were debited to Machinery Account.

(d) Repairs on overhauling of secondhand machinery purchased Rs. 2,000 were debited to Repairs Account.

(e) Sale of old machinery at book value of Rs. 3,000 was credited to Sales Account.

Ans:

Note: The images contain the required rectifying entries: transfer the wrongly debited Purchases amount to Furniture; record machinery purchase correctly in Machinery and Creditors; transfer repairs wrongly debited to Machinery to Repairs; adjust sale of old machinery by crediting Accumulated Depreciation/Disposal and not Sales.

Q15: Rectify the following errors assuming that a suspense account was opened. Ascertain the difference in trial balance:

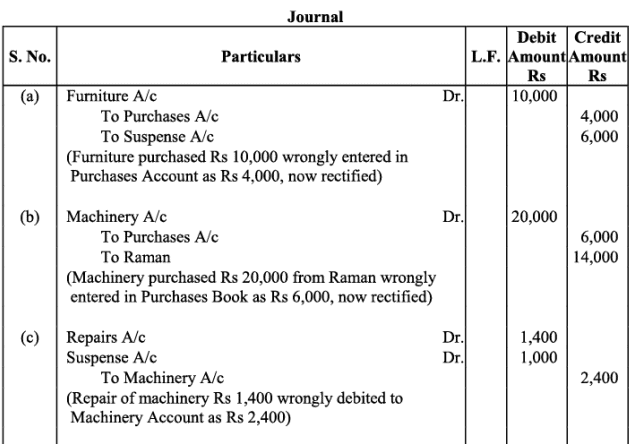

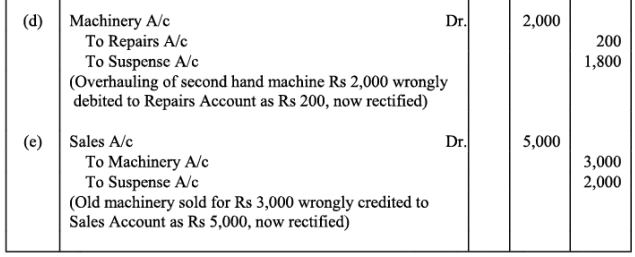

(a) Furniture purchased for Rs. 10,000 was wrongly debited to Purchase Account as Rs. 4,000.

(b) Machinery purchased on credit from Raman for Rs. 20,000 was recorded through Purchases Book as Rs. 6,000.

(c) Repairs on machinery Rs. 1,400 were debited to Machinery Account as Rs. 2,400.

(d) Repairs on overhauling of secondhand machinery purchased Rs. 2,000 were debited to Repairs Account as Rs. 200.

(e) Sale of old machinery at book value Rs. 3,000 was credited to Sales Account as Rs. 5,000.

Ans:

Note: The images show the calculation of the net effect of these mispostings and the Suspense Account that records the difference until all corrections are passed. Each item is adjusted for the under/over posting amounts stated.

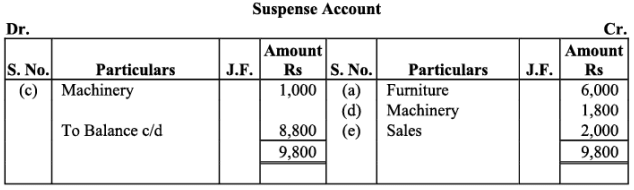

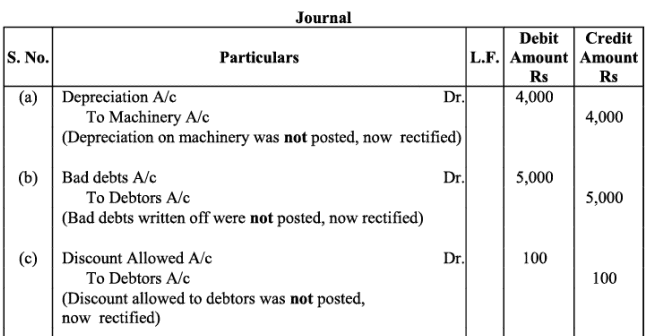

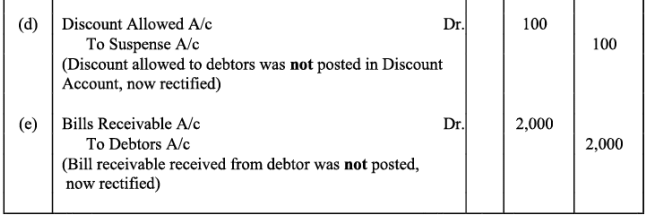

Q16: Rectify the following errors:

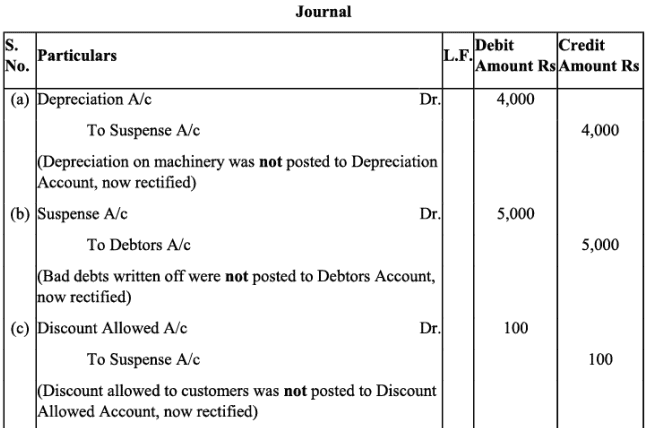

(a) Depreciation provided on machinery Rs. 4,000 was not posted.

(b) Bad debts written off Rs. 5,000 were not posted.

(c) Discount allowed to a debtor Rs. 100 on receiving cash from him was not posted.

(d) Discount allowed to a debtor Rs. 100 on receiving cash from him was not posted to discount account.

(e) Bill receivable for Rs. 2,000 received from a debtor was not posted.

Ans:

Note: The images present the necessary journal entries: (a) Debit Profit & Loss A/c (Depreciation) and credit Depreciation Provision/Machinery Accumulated Depreciation Rs. 4,000; (b) Debit Bad Debts and credit Debtors Rs. 5,000; (c) Debit Discount Allowed and credit Debtors for Rs. 100; (d) If discount was posted only to Debtors, credit Discount Allowed to correct the omission; (e) Debit Bills Receivable and credit Debtors Rs. 2,000.

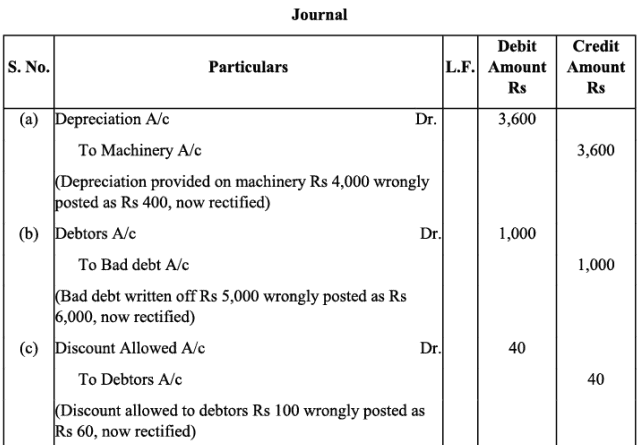

Q17: Rectify the following errors:

(a) Depreciation provided on machinery Rs. 4,000 was posted as Rs. 400.

(b) Bad debts written off Rs. 5,000 were posted as Rs. 6,000.

(c) Discount allowed to a debtor Rs. 100 on receiving cash from him was posted as Rs. 60.

(d) Goods withdrawn by proprietor for personal use Rs. 800 were posted as Rs. 300.

(e) Bill receivable for Rs. 2,000 received from a debtor was posted as Rs. 3,000.

Ans:

Note: The images contain the correcting journal entries which adjust each account by the difference between the correct amount and the amount posted (for example, add Rs. 3,600 to depreciation, reduce bad debts by Rs. 1,000, etc.).

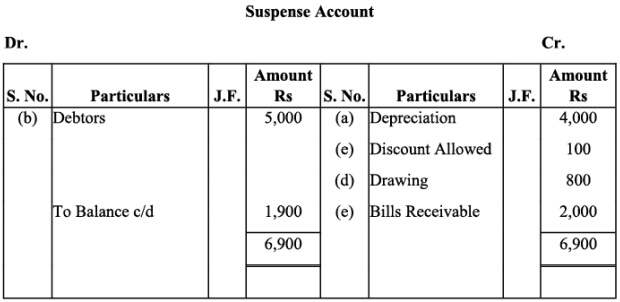

Q18: Rectify the following errors assuming that a suspense account was opened. Ascertain the difference in trial balance:

(a) Depreciation provided on machinery Rs. 4,000 was not posted to Depreciation account.

(b) Bad debts written off Rs. 5,000 were not posted to Debtors account.

(c) Discount allowed to a debtor Rs. 100 on receiving cash from him was not posted to discount allowed account.

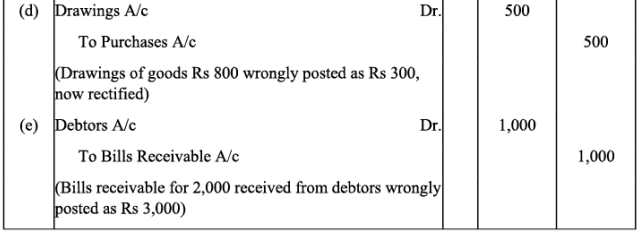

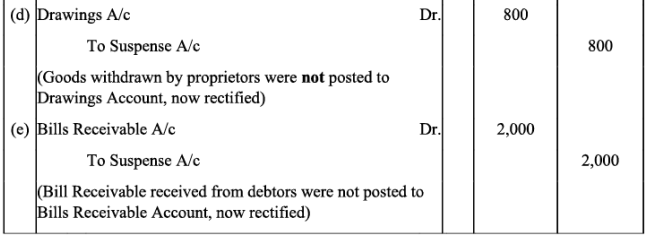

(d) Goods withdrawn by proprietor for personal use Rs. 800 were not posted to Drawings account.

(e) Bill receivable for Rs. 2,000 received from a debtor was not posted to Bills receivable account.

Ans:

Note: The images show the rectifying entries and the Suspense Account entries reflecting the initial difference. Each omitted posting is entered and the Suspense Account balance reduces accordingly until fully corrected.

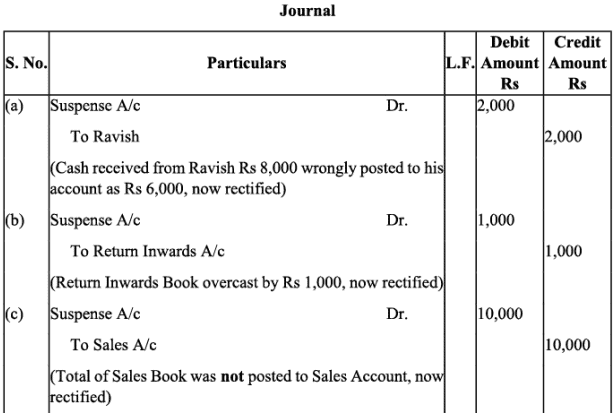

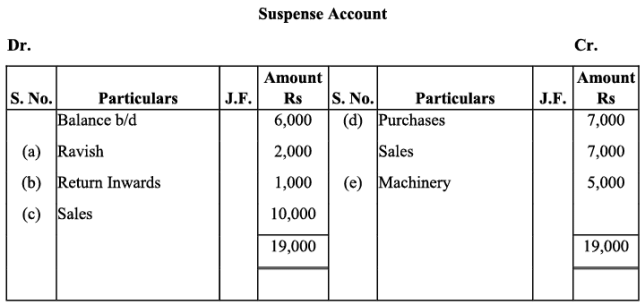

Q19: Trial balance of Anuj did not agree. It showed an excess credit of Rs. 6,000. He put the difference to suspense account. He discovered the following errors:

(a) Cash received from Ravish Rs. 8,000 was posted to his account as Rs. 6,000.

(b) Returns inwards book overcast by Rs. 1,000.

(c) Total of sales book Rs. 10,000 was not posted to Sales account.

(d) Credit purchases from Nanak Rs. 7,000 were recorded in Sales Book. However, Nanak's account was correctly credited.

(e) Machinery purchased for Rs. 10,000 was posted to Purchases account as Rs. 5,000.

Rectify the errors and prepare suspense account.

Ans:

Note: The images provide journal entries correcting the mispostings: adjust Ravish's account by Rs. 2,000 (to correct Rs. 6,000 to Rs. 8,000), correct Returns inwards by Rs. 1,000, post Sales book total of Rs. 10,000 to Sales, move the wrongly posted Rs. 5,000 from Purchases to Machinery, and prepare Suspense Account to show the net effect until all corrections are made.

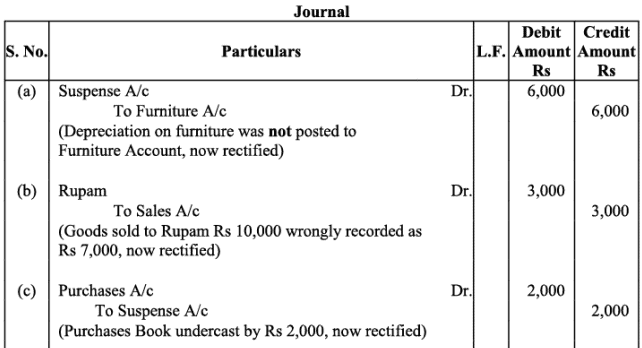

Q20: Trial balance of Raju showed an excess debit of Rs. 10,000. He put the difference to suspense account and discovered the following errors:

(a) Depreciation written-off the furniture Rs. 6,000 was not posted to Furniture account.

(b) Credit sales to Rupam Rs. 10,000 were recorded as Rs. 7,000.

(c) Purchases book undercast by Rs. 2,000.

(d) Cash sales to Rana Rs. 5,000 were not posted.

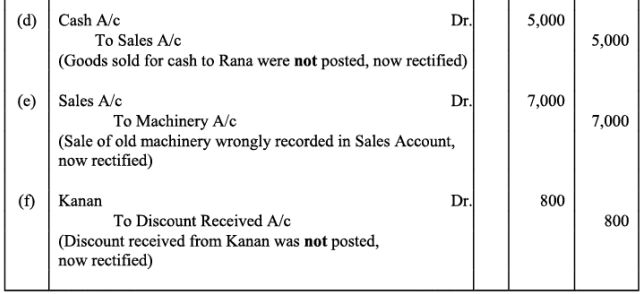

(e) Old Machinery sold for Rs. 7,000 was credited to Sales account.

(f) Discount received Rs. 800 from Kanan on paying cash to him was not posted.

Rectify the errors and prepare suspense account.

Ans:

Note: Corrections include posting depreciation, adjusting Rupam's sales by Rs. 3,000, increasing purchases by Rs. 2,000, posting cash sales of Rs. 5,000, transferring the sale of old machinery from Sales to Disposal/Capital Sales account, and recording discount received. The images show the resulting Suspense Account and its clearance as corrections are passed.

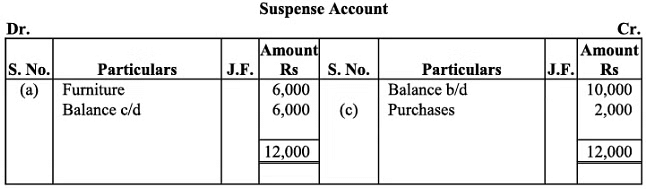

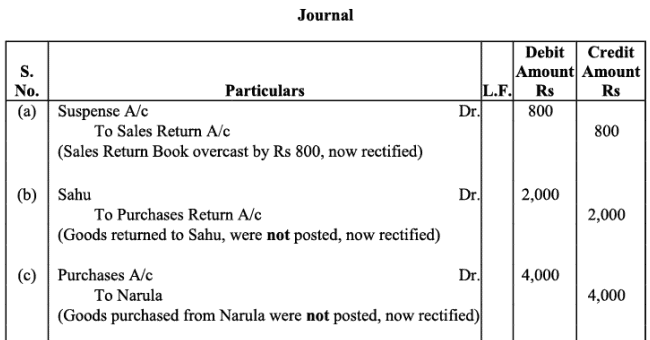

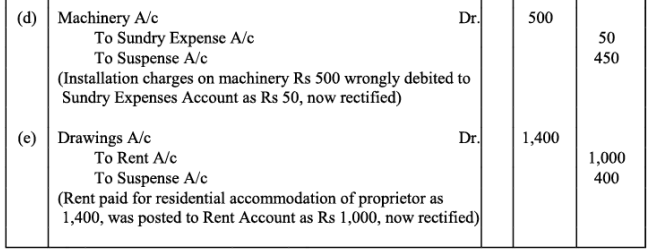

Q21: Trial balance of Madan did not agree, and he put the difference to suspense account. He discovered the following errors:

(a) Sales return book overcast by Rs. 800.

(b) Purchases return to Sahu Rs. 2,000 were not posted.

(c) Goods purchased on credit from Narula Rs. 4,000 were taken into stock, but no entry was passed in the books.

(d) Installation charges on new machinery purchased Rs. 500 were debited to sundry expenses account as Rs. 50.

(e) Rent paid for residential accommodation of Madan (the proprietor) Rs. 1,400 was debited to Rent account as Rs. 1,000.

Rectify the errors and prepare suspense account to ascertain the difference in trial balance.

Ans:

Note: The images present the correcting entries which include reversing the overcast returns, posting purchase returns to Sahu, recording the credit purchase from Narula, correcting the installation charges to Rs. 500, and adjusting rent to Rs. 1,400. The Suspense Account shown records the net difference until fully adjusted.

Note: As per the solution Suspense Account shows a credit balance of Rs. 50. However, as per the answer given in the book, it is a credit balance of Rs. 2050. In order to match answer with the book item (b) is taken as, 'Purchases return to Sahu Rs. 2,000 were not posted to Sahu's Account.' Thus, the rectifying entry for this error will be as:

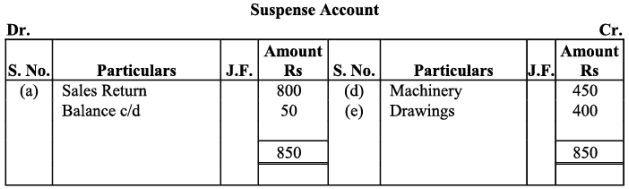

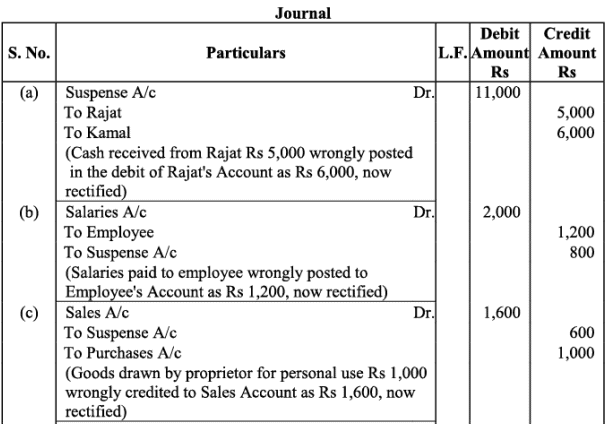

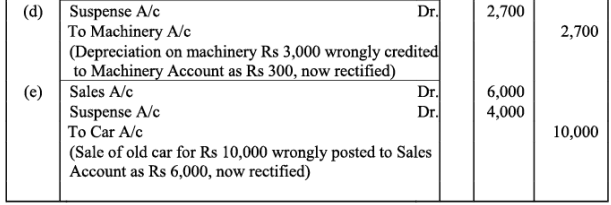

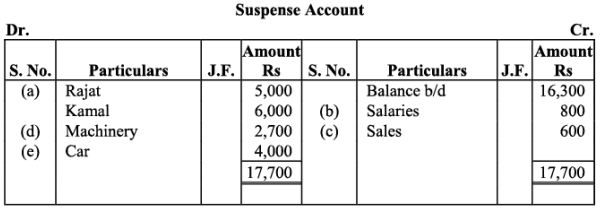

Q22: Trial balance of Kohli did not agree and showed an excess debit of Rs. 16,300. He put the difference to a suspense account and discovered the following errors:

(a) Cash received from Rajat Rs. 5,000 was posted to the debit of Kamal as Rs. 6,000.

(b) Salaries paid to an employee Rs. 2,000 were debited to his personal account as Rs. 1,200.

(c) Goods withdrawn by proprietor for personal use Rs. 1,000 were credited to sales account as Rs. 1,600.

(d) Depreciation provided on machinery Rs. 3,000 was posted to Machinery account as Rs. 300.

(e) Sale of old car for Rs. 10,000 was credited to sales account as Rs. 6,000.

Rectify the errors and prepare suspense account.

Ans:

Note: The images detail adjustments such as correcting Rajat/Kamal entries, correcting salary posting by Rs. 800, moving proprietor withdrawals out of Sales into Drawings and reversing the wrong sales credit, correcting depreciation from Rs. 300 to Rs. 3,000, and adjusting sale of old car from Rs. 6,000 to Rs. 10,000. Suspense Account shows the net effect and how it is cleared.

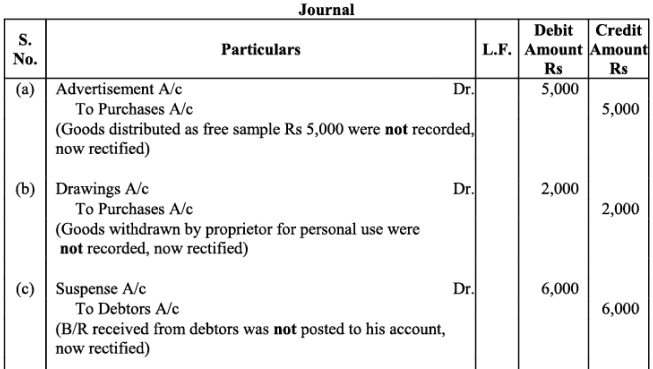

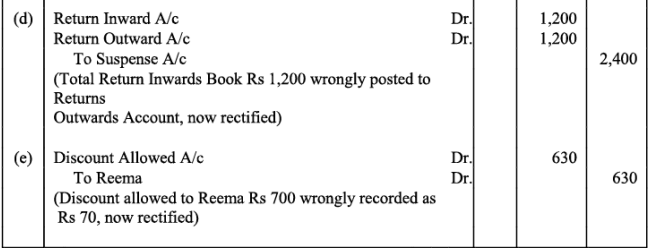

Q23: Give journal entries to rectify the following errors assuming that suspense account had been opened:

(a) Goods distributed as free sample Rs. 5,000 were not recorded in the books.

(b) Goods withdrawn for personal use by the proprietor Rs. 2,000 were not recorded in the books.

(c) Bill receivable received from a debtor Rs. 6,000 was not posted to his account.

(d) Total of Returns inwards book Rs. 1,200 was posted to Returns outwards account.

(e) Discount allowed to Reema Rs. 700 on receiving cash from her was recorded in the books as Rs. 70.

Ans:

Note: The images provide the exact journal entries: debit Advertising/Samples for free samples; debit Drawings for proprietor withdrawals; debit Bills Receivable and credit Debtor for the bill not posted; correct the misposting between Returns Inwards and Returns Outwards; and adjust Reema's discount by Rs. 630 to correct the amount to Rs. 700.

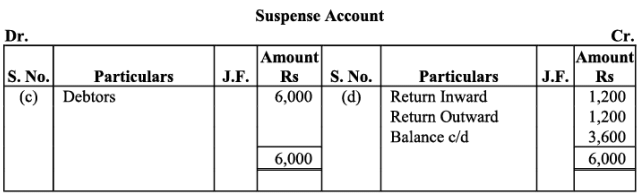

Q24: Trial balance of Khatau did not agree. He put the difference to suspense account and discovered the following errors:

(a) Credit sales to Manas Rs. 16,000 were recorded in the purchases book as Rs. 10,000 and posted to the debit of Manas as Rs. 1,000.

(b) Furniture purchased from Noor Rs. 6,000 was recorded through purchases book as Rs. 5,000 and posted to the debit of Noor as Rs. 2,000.

(c) Goods returned to Rai Rs. 3,000 were recorded through the Sales book as Rs. 1,000.

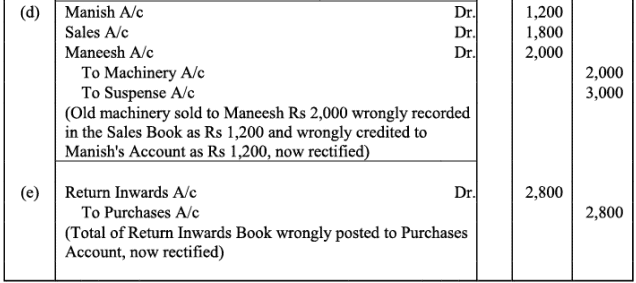

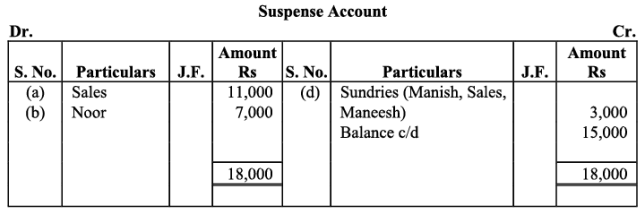

(d) Old machinery sold for Rs. 2,000 to Maneesh was recorded through sales book as Rs. 1,800 and posted to the credit of Manish as Rs. 1,200.

(e) Total of Returns inwards book Rs. 2,800 was posted to Purchase account.

Rectify the above errors and prepare suspense account to ascertain the difference in trial balance.

Ans:

Note: The images show the correcting entries to move wrongly recorded sales/purchases and to correct debtor/creditor postings, plus the Suspense Account displaying the residual difference until all corrections are complete.

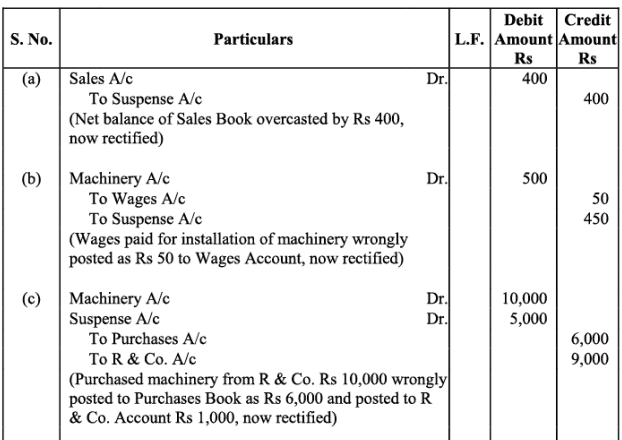

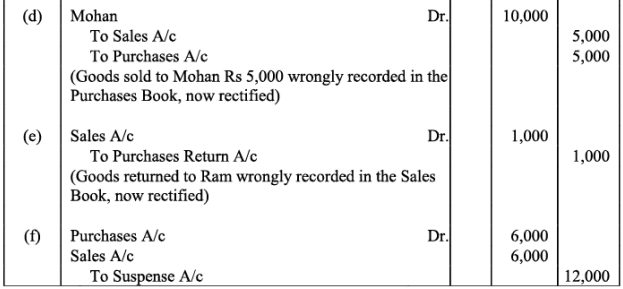

Q25: Trial balance of John did not agree. He put the difference to suspense account and discovered the following errors:

(a) In the sales book for January, total of page 2 was carried forward to page 3 as Rs. 1,000 instead of Rs. 1,200 and total of page 6 was carried forward to page 7 as Rs. 5,600 instead of Rs. 5,000.

(b) Wages paid for installation of machinery Rs. 500 was posted to wages account as Rs. 50.

(c) Machinery purchased from R & Co. for Rs. 10,000 on credit was entered in Purchases Book as Rs. 6,000 and posted from there to R & Co. as Rs. 1,000.

(d) Credit sales to Mohan Rs. 5,000 were recorded in Purchases Book.

(e) Goods returned to Ram Rs. 1,000 were recorded in Sales Book.

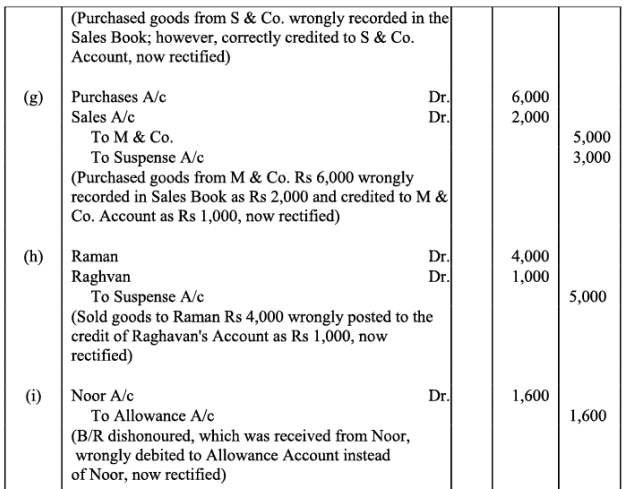

(f) Credit purchases from S & Co. for Rs. 6,000 were recorded in sales book. However, S & Co. was correctly credited.

(g) Credit purchases from M & Co. Rs. 6,000 were recorded in Sales Book as Rs. 2,000 and posted therefrom to the credit of M & Co. as Rs. 1,000.

(h) Credit sales to Raman Rs. 4,000 were posted to the credit of Raghvan as Rs. 1,000.

(i) Bill receivable for Rs. 1,600 from Noor was dishonoured and posted to the debit of Allowances account.

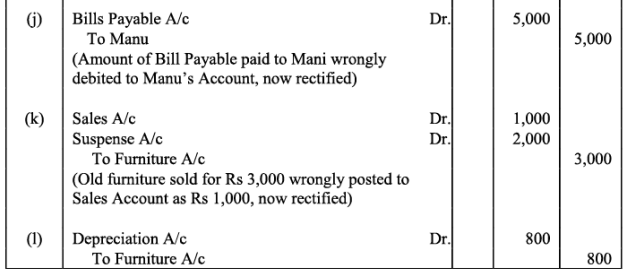

(j) Cash paid to Mani Rs. 5,000 against our acceptance was debited to Manu.

(k) Old furniture sold for Rs. 3,000 was posted to Sales account as Rs. 1,000.

(l) Depreciation provided on furniture Rs. 800 was not posted.

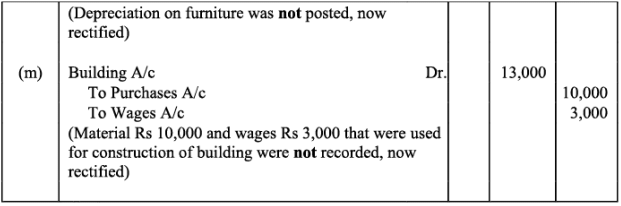

(m) Material Rs. 10,000 and wages Rs. 3,000 were used for construction of building. No adjustment was made in the books.

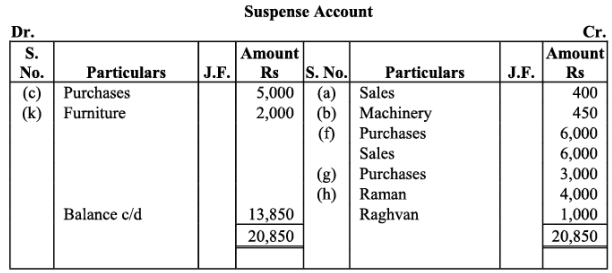

Rectify the errors and prepare suspense account to ascertain the difference in trial balance.

Ans:

Note: The images present comprehensive rectifying journal entries for each listed error, followed by the Suspense Account which summarises the combined effect of all corrections. For item (m) it is assumed that material used for the building was part of stock-in-trade and appropriate adjustments have been made to transfer those costs to Building (or Capital Work-in-Progress) and reduce Stock by the same amount.

FAQs on NCERT Solution - Trial Balance and Rectification of Errors

| 1. What is a trial balance and why is it important in accounting? |  |

| 2. What are the common types of errors that can affect the trial balance? | |

| 3. How can errors in the trial balance be rectified? | |

| 4. What is the significance of rectification of errors in accounting? | |

| 5. What steps should be followed when preparing a trial balance? | |