NCERT Solution (Part - 2) - Trial Balance and Rectification of Errors

Q4 : What are the different types of errors that are usually committed in recording business transaction?

Answer :

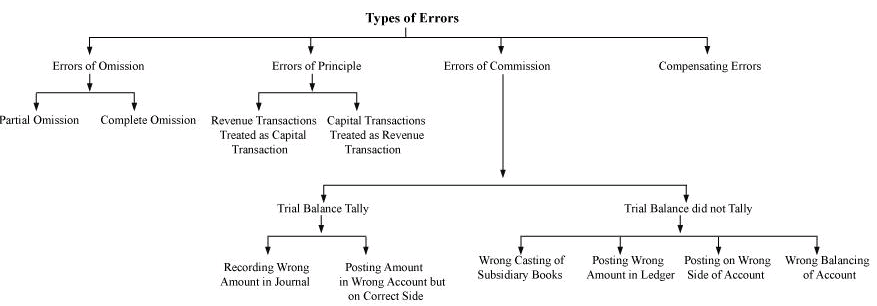

1. Errors of omission - These occur when an entry is left out either in the book of original entry or while posting to the ledger. They may be:

- Partial omission - A transaction is recorded on one side but omitted on the other. Example: goods sold to Mahesh are entered in Sales but not posted to Mahesh's account. Effect: it makes the trial balance disagree, since one side is missing.

- Complete omission - A transaction is omitted altogether from the books. Example: a credit purchase from Rakesh is not recorded in Purchases Book. Effect: it does not affect the trial balance totals because both debit and credit are missing.

2. Errors of principle - These arise when an entry is made in contravention of basic accounting principles; for example, treating a capital expenditure as revenue or recording a revenue item in a capital account. Such errors usually affect the trial balance and lead to incorrect financial statements.

3. Errors of classification - These are committed when proper distinction is not made between revenue and capital items. They are of two kinds:

- Revenue transactions treated as capital transactions.

- Capital transactions treated as revenue transactions.

- Example: repairs to machinery recorded in the Machinery account instead of Repairs (expense). Effect: trial balance may still agree but profit or asset values will be incorrect.

4. Errors of commission - These occur through carelessness while recording amounts, posting to the wrong account, wrong balancing or incorrect carrying forward. Examples: posting an amount to the wrong customer's account or writing a wrong amount. Such errors usually affect the trial balance.

5. Errors detected by the trial balance (two situations) -

- Trial balance does not agree - here there are one-sided errors that affect only one account and are easier to detect. Common causes:

- Wrong casting of subsidiary books

- Posting wrong amount in ledger

- Posting on the wrong side of an account

- Wrong balancing of an account

- Trial balance agrees - agreement does not guarantee that books are error-free. Certain errors do not disturb the equality of totals and are therefore not easily detectable. Typical causes:

- Recording wrong amount equally on both debit and credit sides (e.g. posting Rs 7,000 as Rs 700 on both sides)

- Posting to the wrong account but on the correct side

6. Compensating errors - These occur when one error is exactly offset by another error of the same amount, so that trial balance still tallies. Example: Mr A's account is credited by Rs 2,000 instead of Rs 200 (over-credit by 1,800) and Mr B's account is credited by Rs 200 instead of Rs 2,000 (under-credit by 1,800); the two errors cancel out in the totals. Effect: trial balance will agree, but individual account balances will be incorrect.

Q5 : As an accountant of a company, you are disappointed to learn that the totals in your new trial balance are not equal. After going through a careful analysis, you have discovered only one error. Specifically, the balance of the Office Equipment account has a debit balance of Rs. 15,600 on the trial balance. However, you have figured out that a correctly recorded credit purchase of pen-drive for Rs 3,500 was posted from the journal to the ledger with a Rs. 3,500 debit to Office Equipment and another Rs. 3,500 debit to creditors accounts. Answer each of the following questions and present the amount of any misstatement :

(a) Is the balance of the office equipment account overstated, understated, or

correctly stated in the trial balance?

(b) Is the balance of the creditors account overstated, understated, or correctly stated in the trial balance?

(c) Is the debit column total of the trial balance overstated, understated, or correctly stated?

(d) Is the credit column total of the trial balance overstated, understated, or correctly stated?

(e) If the debit column total of the trial balance is Rs. 2,40,000 before correcting the error, what is the total of credit column.

Answer : A correctly recorded credit purchase of Rs 3,500 should have been posted as:

- Office equipment - Debit Rs 3,500

- Creditors - Credit Rs 3,500

But it was posted as:

- Office equipment - Debit Rs 3,500 (correct)

- Creditors - Debit Rs 3,500 (wrong; should be credit)

Therefore:

- (a) Office equipment is correctly stated. The required debit of Rs 3,500 was posted correctly to this account, so its balance of Rs 15,600 is not misstated.

- (b) Creditors account is understated (with respect to its correct credit balance). Because it was debited by Rs 3,500 instead of being credited by Rs 3,500, the net error in the creditors' balance is Rs 7,000 (a credit of Rs 3,500 expected but a debit of Rs 3,500 shown → difference of Rs 7,000). Thus the creditors' credit balance is understated by Rs 7,000.

- (c) The debit column of the trial balance is overstated by Rs 3,500, since an extra debit of Rs 3,500 (to creditors) was posted in addition to the correct debit to office equipment.

- (d) The credit column of the trial balance is understated by Rs 3,500, because the expected credit of Rs 3,500 to creditors is missing.

- (e)The shown trial balance totals will differ by Rs 7,000 (debit total minus credit total = Rs 7,000). If the debit column total is Rs 2,40,000 before rectifying the error, the credit column total is:

- Credit total = Debit total - Rs 7,000 = Rs 2,40,000 - Rs 7,000 = Rs 2,33,000.

(Brief justification) The wrong posting produced an extra debit of Rs 3,500 and omitted a credit of Rs 3,500; together these create a difference of Rs 7,000 between the columns. Office equipment was posted correctly, so its individual balance is unaffected.

Page No. : 228

Numerical questions :

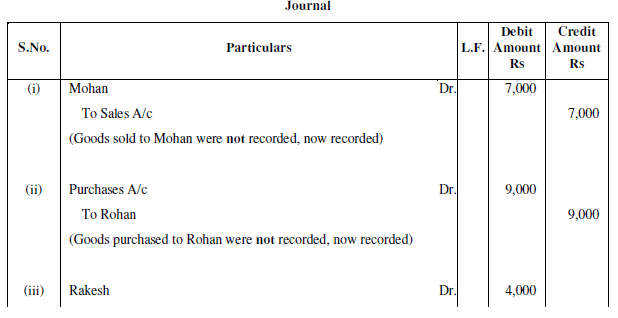

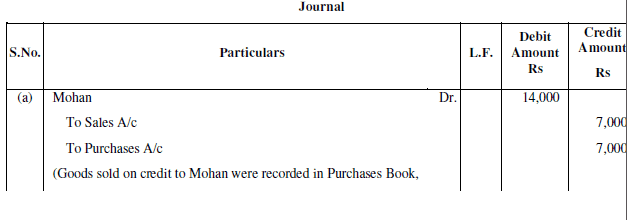

Q1 : Rectify the following errors:

(i) Credit sales to Mohan Rs 7,000 were not recorded.

(ii) Credit purchases from Rohan Rs 9,000 were not recorded.

(iii) Goods returned to Rakesh Rs 4,000 were not recorded.

(iv) Goods returned from Mahesh Rs 1,000 were not recorded.

Answer :

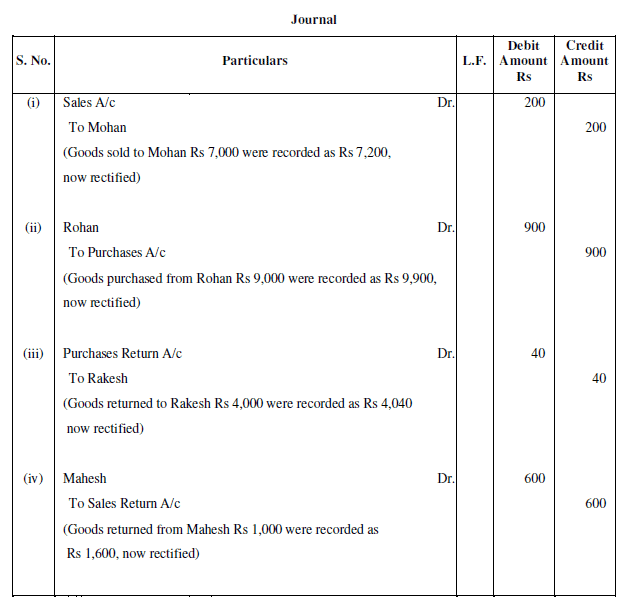

Q2 : Rectify the following errors:

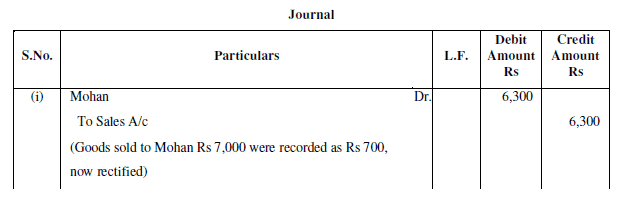

(i) Credit sales to Mohan Rs 7,000 were recorded as Rs 700.

(ii) Credit purchases from Rohan Rs 9,000 were recorded. as Rs 900.

(iii) Goods returned to Rakesh Rs 4,000 were recorded as Rs 400.

(iv) Goods returned from Mahesh Rs 1,000 were recorded as Rs 100.

Answer :

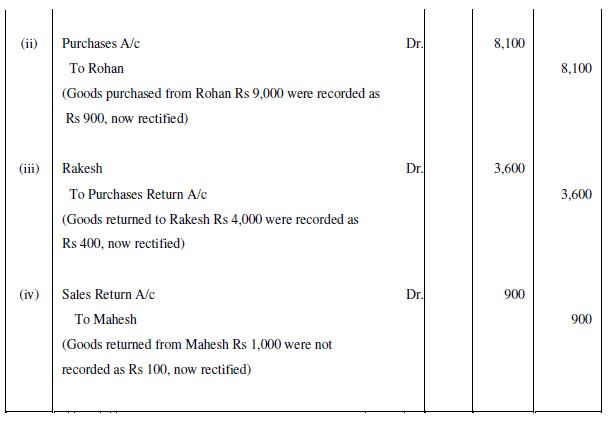

Q3 : Rectify the following errors:

(i) Credit sales to Mohan Rs 7,000 were recorded as Rs 7,200.

(ii) Credit purchases from Rohan Rs 9,000 were recorded as Rs 9,900.

(iii) Goods returned to Rakesh Rs 4,000 were recorded as Rs 4,040.

(iv) Goods returned from Mahesh Rs 1,000 were recorded as Rs 1,600.

Answer :

Page No. : 228

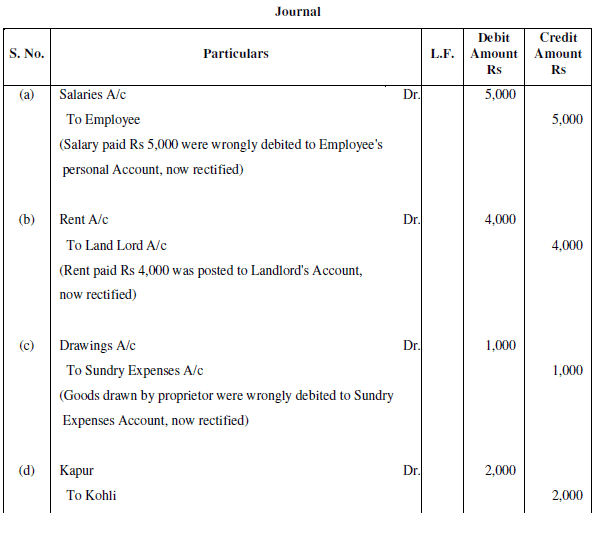

Q4 : Rectify the following errors:

(a) Salary paid Rs 5,000 was debited to employee's personal account.

(b) Rent Paid Rs 4,000 was posted to landlord's personal account.

(c) Goods withdrawn by proprietor for personal use Rs 1,000 were debited to sundry expenses account.

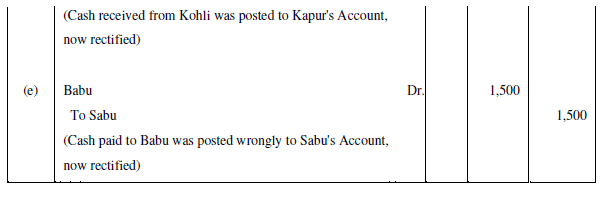

(d) Cash received from Kohli Rs 2,000 was posted to Kapur's account.

(e) Cash paid to Babu Rs 1,500 was posted to Sabu's account.

Answer :

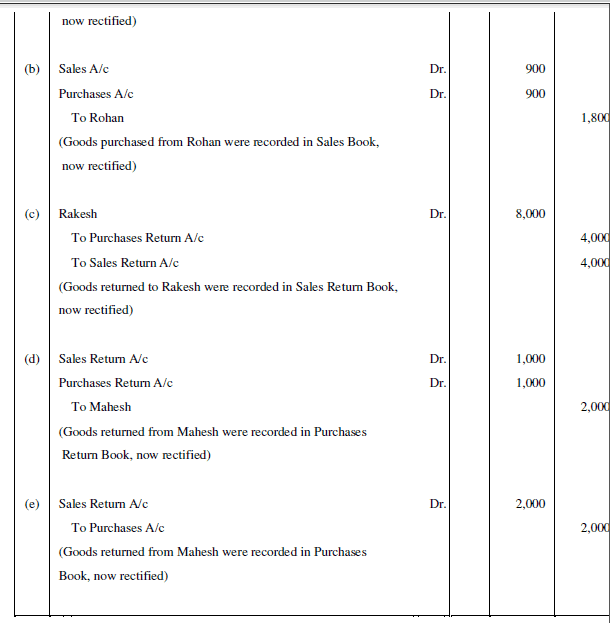

Q5 : Rectify the following errors:

(a) Credit Sales to Mohan Rs 7,000 were recorded in purchases book.

(b) Credit Purchases from Rohan Rs 900 were recorded in sales book.

(c) Goods returned to Rakesh Rs 4,000 were recorded in the sales return book.

(d) Goods returned from Mahesh Rs 1,000 were recorded in purchases return book.

(e) Goods returned from Nahesh Rs 2,000 were recorded in purchases book.

Answer :

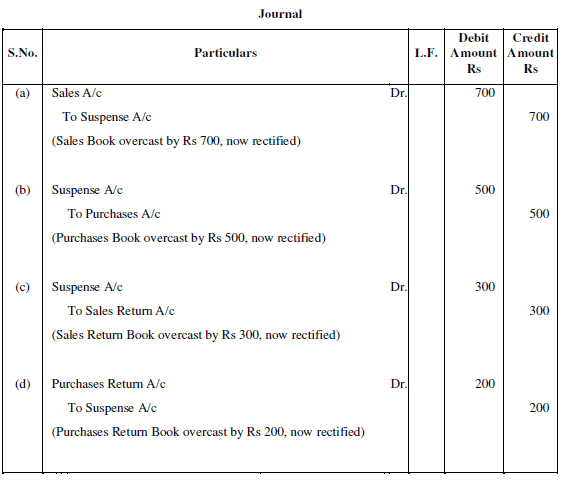

Q6 : Rectify the following errors:

(a) Sales book overcast by Rs 700.

(b) Purchases book overcast by Rs 500.

(c) Sales return book overcast by Rs 300.

(d) Purchase return book overcast by Rs 200.

Answer :

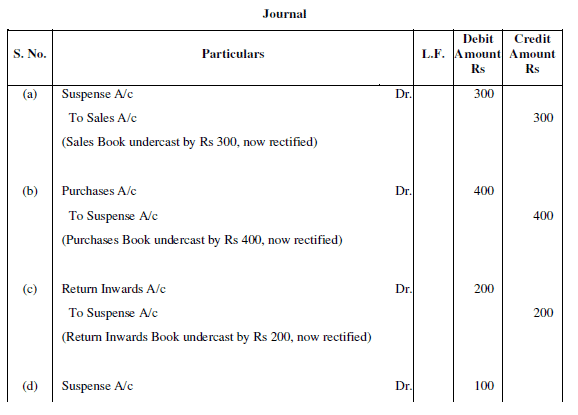

Q7 : Rectify the following errors :

(a) Sales book undercast by Rs 300.

(b) Purchases book undercast by Rs 400.

(c) Return Inwards book undercast by Rs 200.

(d) Return outwards book undercast by Rs 100.

Answer :

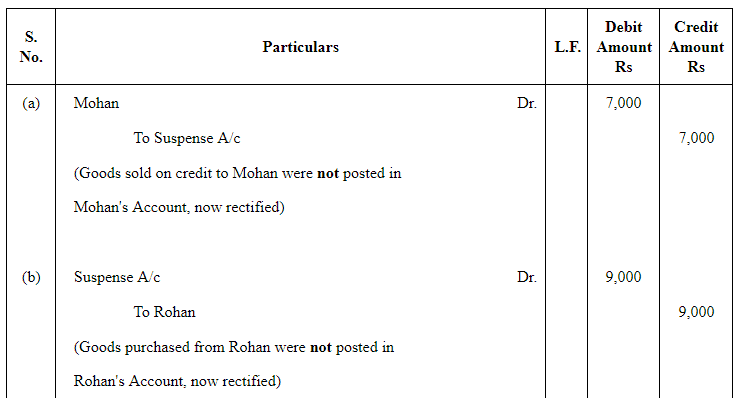

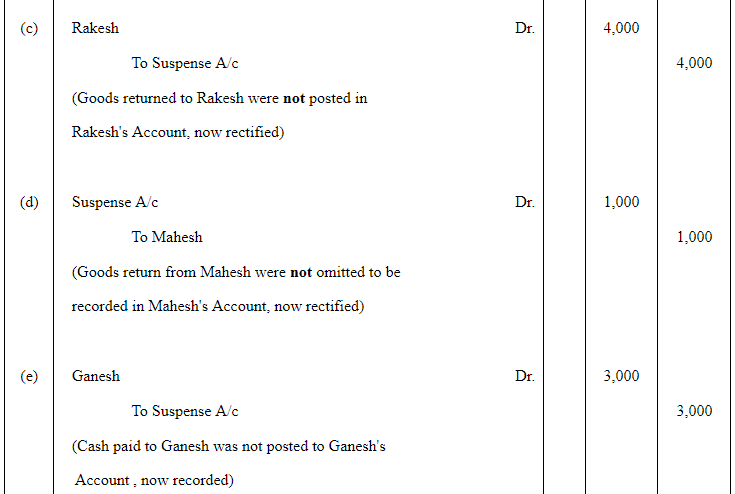

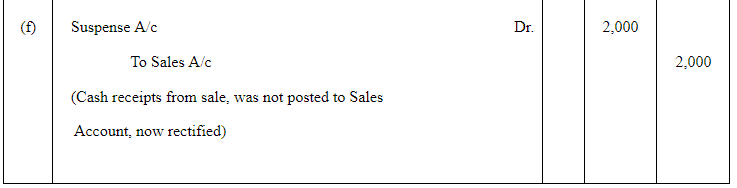

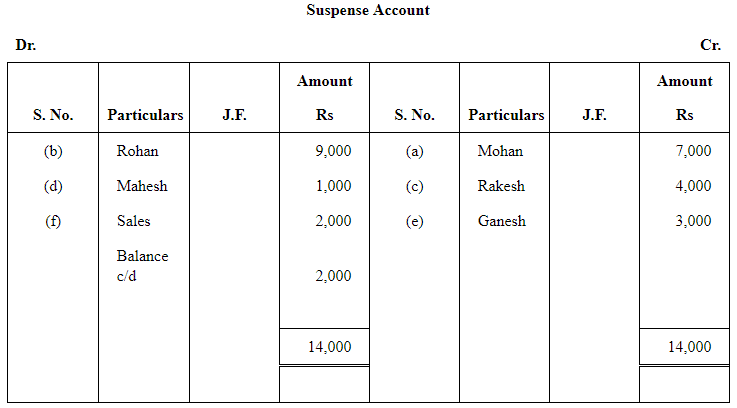

Q8 : Rectify the following errors and ascertain the amount of difference in trial balance by preparing suspense account:

(a) Credit sales to Mohan Rs 7,000 were not posted.

(b) Credit purchases from Rohan Rs 9,000 were not posted.

(c) Goods returned to Rakesh Rs 4,000 were not posted.

(d) Goods returned from Mahesh Rs 1,000 were not posted.

(e) Cash paid to Ganesh Rs 3,000 was not posted.

(f) Cash sales Rs 2,000 were not posted.

Answer :

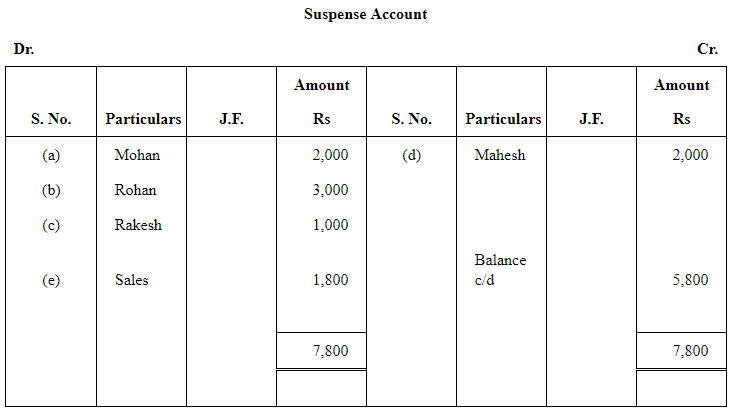

Q9 : Rectify the following errors and ascertain the amount of difference in trial balance by preparing suspense account:

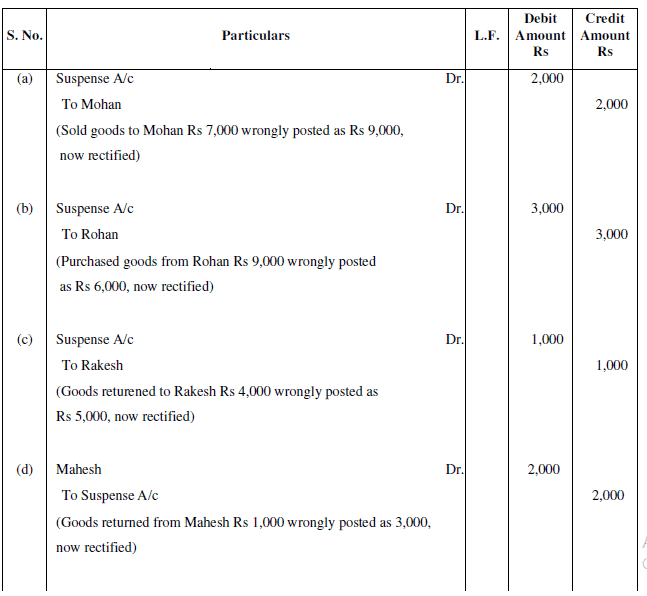

(a) Credit sales to Mohan Rs 7,000 were posted as Rs 9,000.

(b) Credit purchases from Rohan Rs 9,000 were posted as Rs 6,000.

(c) Goods returned to Rakesh Rs 4,000 were posted as Rs 5,000.

(d) Goods returned from Mahesh Rs 1,000 were posted as Rs 3,000.

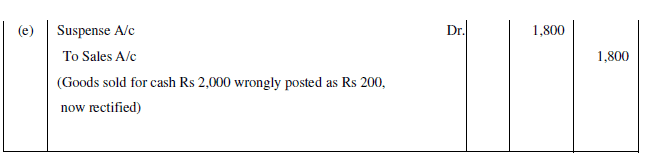

(e) Cash sales Rs 2,000 were posted as Rs 200.

Answer :

Note: In order to match answer with that of the answer given in the book it has been assumed that all the errors mentioned in this question are errors of partial omission.

FAQs on NCERT Solution (Part - 2) - Trial Balance and Rectification of Errors

| 1. What is a trial balance? |  |

| 2. What is the purpose of rectifying errors in accounting? | |

| 3. What are the different types of errors that can occur in accounting? | |

| 4. What is the difference between a suspense account and an error account? | |

| 5. How can errors in accounting be prevented? | |