NCERT Solution (Part - 3) - Trial Balance and Rectification of Errors

Page No 230:

Question 10 : Rectify the following errors :

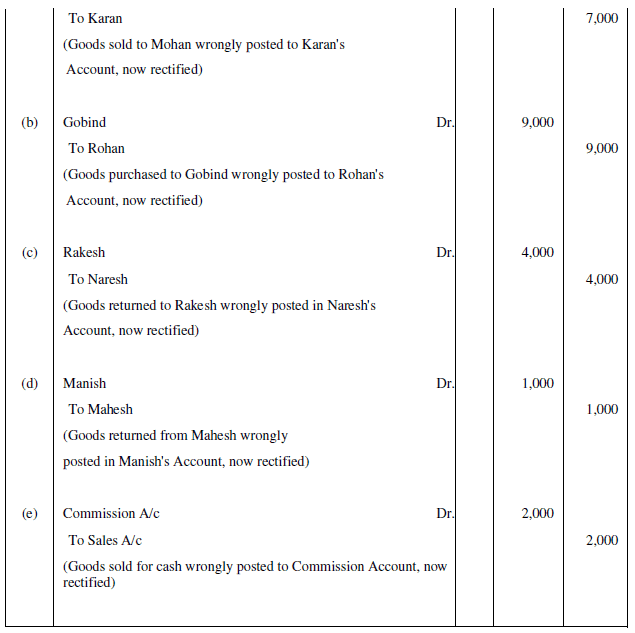

(a) Credit sales to Mohan Rs 7,000 were posted to Karan.

(b) Credit purchases from Rohan Rs 9,000 were posted to Gobind.

(c) Goods returned to Rakesh Rs 4,000 were posted to Naresh.

(d) Goods returned from Mahesh Rs 1,000 were posted to Manish.

(e) Cash sales Rs 2,000 were posted to commission account.

Answer :

Ans:

- (a) Wrong posting: Mohan was not debited; Karan was debited instead. Rectification entry:

Dr Mohan Rs 7,000

Cr Karan Rs 7,000

Note: This is a posting-to-wrong-account error. It does not affect the trial balance totals as both debit and credit were recorded, but individual ledgers are corrected by the above entry. - (b) Wrong posting: Rohan should have been credited; Gobind was credited instead. Rectification entry:

Dr Gobind Rs 9,000

Cr Rohan Rs 9,000

Note: Purchases were correctly recorded; only the creditor's account was wrongly posted. Trial balance totals remain unaffected. - (c) Wrong posting: Debit for return to Rakesh should have gone to Rakesh but was posted to Naresh. Rectification entry:

Dr Rakesh Rs 4,000

Cr Naresh Rs 4,000

Note: Purchases Return (or appropriate return account) was already recorded; this entry reverses the wrong debit and posts the correct one. - (d) Wrong posting: Credit of Mahesh (sales return) was posted to Manish. Rectification entry:

Dr Manish Rs 1,000

Cr Mahesh Rs 1,000

Note: This reverses the incorrect credit to Manish and posts the correct credit to Mahesh. - (e) Wrong posting: Cash sales should credit Sales account, but Sales was posted to Commission. Rectification entry:

Dr Commission Rs 2,000

Cr Sales Rs 2,000

Note: Cash (or Bank) entry is assumed correct. This reverses the wrong posting to Commission and restores the Sales account.

Question 11 :

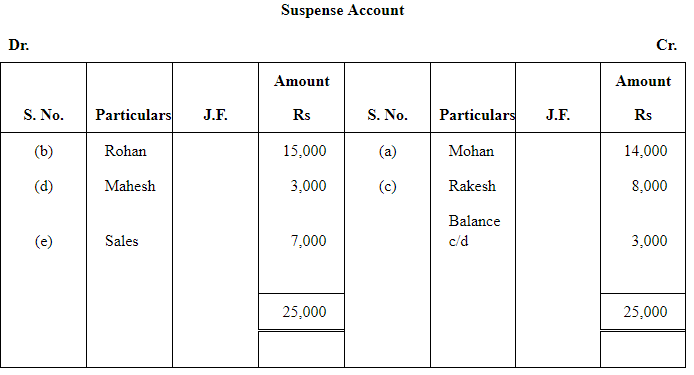

Rectify the following errors assuming that a suspense account was opened.

Ascertain the difference in trial balance.

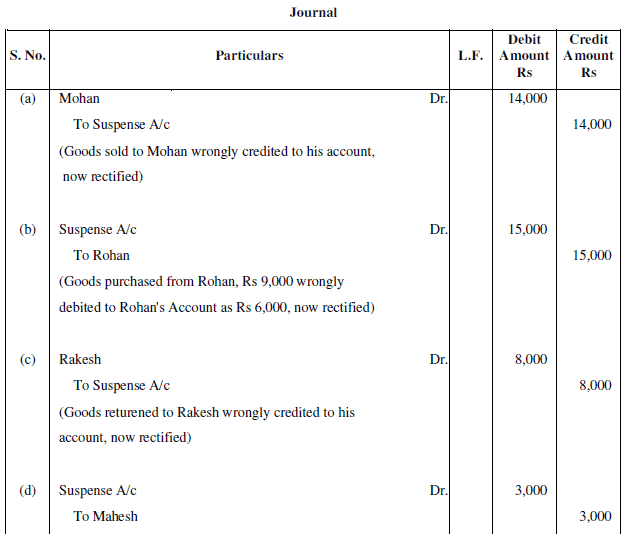

(a) Credit sales to Mohan Rs 7,000 were posted to the credit of his account.

(b) Credit purchases from Rohan Rs 9,000 were posted to the debit of his account as Rs 6,000.

(c) Goods returned to Rakesh Rs 4,000 were posted to the credit of his account.

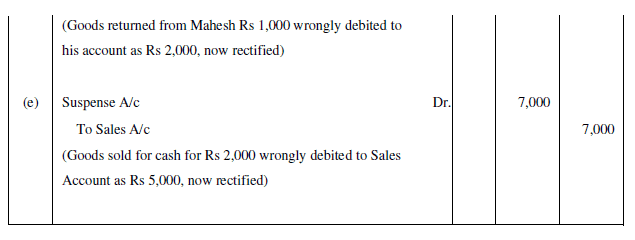

(d) Goods returned from Mahesh Rs 1,000 were posted to the debit of his account as Rs 2,000.

(e) Cash sales Rs 2,000 were posted to the debit of sales account as Rs 5,000.

Answer :

Ans:

- (a) Mistake: Credit sale of Rs 7,000 should have resulted in Mohan being debited, but he was credited. Effect on trial balance: Credits exceed debits by Rs 14,000.

Rectifying entry (to clear suspense):

Dr Mohan Rs 14,000

Cr Suspense Rs 14,000

Explanation: Posting Mohan to the credit instead of debit shifts Rs 7,000 from debit to credit; net difference = Rs 14,000. - (b) Mistake: Credit purchases Rs 9,000 were posted as a debit of Rs 6,000 to Rohan. Effect on trial balance: Debits exceed credits by Rs 15,000.

Rectifying entry:

Dr Suspense Rs 15,000

Cr Rohan Rs 15,000

Explanation: Rohan moved from a required credit of 9,000 to an actual debit of 6,000 → net change 15,000 to be corrected. - (c) Mistake: Goods returned to Rakesh Rs 4,000 were posted to his credit (instead of debit). Effect on trial balance: Credits exceed debits by Rs 8,000.

Rectifying entry:

Dr Rakesh Rs 8,000

Cr Suspense Rs 8,000 - (d) Mistake: Goods returned from Mahesh Rs 1,000 were posted to the debit of his account as Rs 2,000. Effect on trial balance: Debits exceed credits by Rs 3,000.

Rectifying entry:

Dr Suspense Rs 3,000

Cr Mahesh Rs 3,000 - (e) Mistake: Cash sales Rs 2,000 were wrongly posted to debit of Sales as Rs 5,000 (i.e., sales debited instead of credited and for wrong amount). Effect on trial balance: Debits exceed credits by Rs 7,000.

Rectifying entry:

Dr Suspense Rs 7,000

Cr Sales Rs 7,000

Question 12 : Rectify the following errors assuming that a suspense account was opened. Ascertain the difference in trial balance.

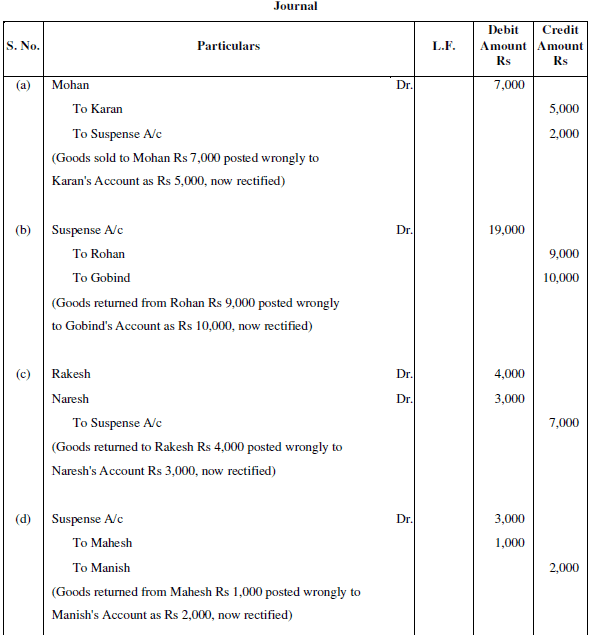

(a) Credit sales to Mohan Rs 7,000 were posted to Karan as Rs 5,000.

(b) Credit purchases from Rohan Rs 9,000 were posted to the debit of Gobind as Rs 10,000.

(c) Goods returned to Rakesh Rs 4,000 were posted to the credit of Naresh as Rs 3,000.

(d) Goods returned from Mahesh Rs 1,000 were posted to the debit of Manish as Rs 2,000.

(e) Cash sales Rs 2,000 were posted to commission account as Rs 200.

Answer :

Ans:

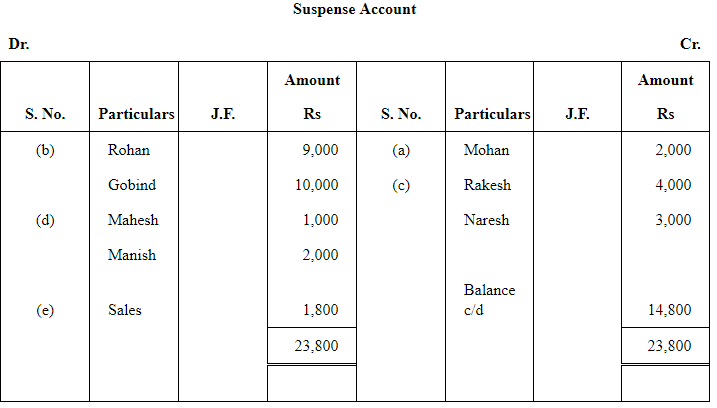

- (a) Mistake: Credit sales to Mohan Rs 7,000 were posted to Karan as Rs 5,000. Effect on trial balance:

- Mohan: should be debited Rs 7,000 but not debited; Karan was debited Rs 5,000 instead.

Net effect: Debits short by Rs 7,000 and excess debit of Rs 5,000 elsewhere → net shortage of Rs 2,000 on debit side (or credits exceed debits by Rs 2,000).

Rectifying entry:

Dr Mohan Rs 7,000

Cr Karan Rs 5,000

Cr Suspense Rs 2,000

Explanation: We remove the wrong Rs 5,000 debit to Karan by crediting him and post the correct debit to Mohan for Rs 7,000; the balance Rs 2,000 is adjusted through Suspense. - (b) Mistake: Credit purchases Rs 9,000 posted to debit of Gobind as Rs 10,000. Effect on trial balance:

- Gobind has a debit of Rs 10,000 instead of a credit of Rs 9,000 → net debit excess = Rs 19,000.

Rectifying entry:

Dr Suspense Rs 19,000

Cr Gobind Rs 19,000 - (c) Mistake: Goods returned to Rakesh Rs 4,000 posted to credit of Naresh as Rs 3,000. Effect on trial balance:

- Rakesh not debited; Naresh credited Rs 3,000 wrongly. Net effect: Credits exceed debits by Rs 7,000.

Rectifying entry:

Dr Rakesh Rs 4,000

Dr Suspense Rs 3,000

Cr Naresh Rs 3,000 - (d) Mistake: Goods returned from Mahesh Rs 1,000 posted to debit of Manish as Rs 2,000. Effect:

- Manish debited Rs 2,000 instead of Mahesh credited Rs 1,000 → net debit excess Rs 3,000.

Rectifying entry:

Dr Suspense Rs 3,000

Cr Manish Rs 2,000

Cr Mahesh Rs 1,000 - (e) Mistake: Cash sales Rs 2,000 posted to commission account as Rs 200. Effect on trial balance:

- Commission debited Rs 200 (wrong), Sales credited short by Rs 2,000 and commission wrongly affected → net difference: credits exceed debits by Rs 1,800.

Rectifying entry:

Dr Commission Rs 200

Dr Suspense Rs 1,800

Cr Sales Rs 2,000

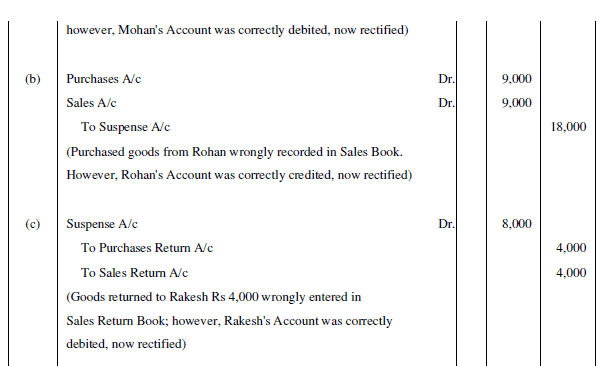

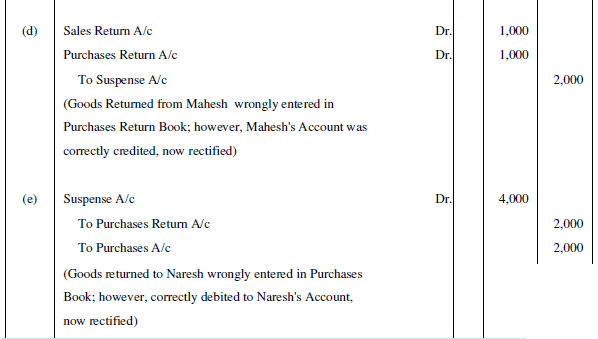

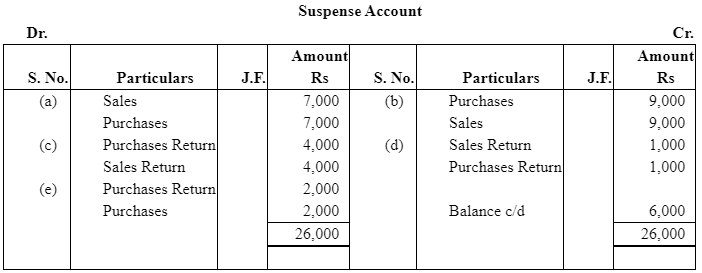

Question 13 : Rectify the following errors assuming that suspense account was opened. Ascertain the difference in trial balance.

(a) Credit sales to Mohan Rs 7,000 were recorded in Purchase Book. However, Mohan's account was correctly

(b) Credit purchases from Rohan Rs 9,000 were recorded in sales book. However, Rohan's account was correctl

(c) Goods returned to Rakesh Rs 4,000 were recorded in sales return book. However, Rakesh's account was cor

(d) Goods returned from Mahesh Rs 1,000 were recorded through purchases return book. However, Mahesh's correctly credited.

(e) Goods returned to Naresh Rs 2,000 were recorded through purchases book. However, Naresh's account was correctly debited.

Answer :

Ans:

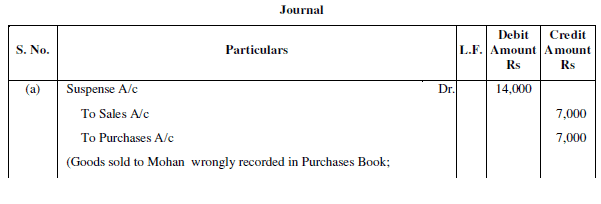

- (a) Mistake: Credit sales to Mohan Rs 7,000 were recorded in Purchase Book (i.e., treated as purchases). Mohan's personal account, however, was correctly posted. Effect on trial balance:

- Purchase book recording debited Purchases instead of Debtors; Sales credit was missing. Net effect: Credits short by Rs 7,000 and debits increased by Rs 7,000 → difference Rs 14,000 (debits exceed credits by Rs 14,000).

Rectifying entry:

Dr Sales Rs 7,000

Cr Purchases Rs 7,000

Then adjust Suspense as required (Dr/Cr) depending on earlier balancing entry. - (b) Mistake: Credit purchases Rs 9,000 were recorded in Sales Book. Rohan's account was correct. Effect:

- Sales were wrongly credited (extra credit Rs 9,000) and purchases not debited. Net effect: Credits exceed debits by Rs 18,000.

Rectifying entry:

Dr Sales Rs 9,000

Cr Purchases Rs 9,000 - (c) Mistake: Goods returned to Rakesh Rs 4,000 recorded in Sales Return Book (should have been Purchases Return). Rakesh's account correct. Effect:

- Sales Return debited instead of Purchases Return credited; net imbalance depends on how returns are shown. Rectification:

Dr Purchases Return Rs 4,000

Cr Sales Return Rs 4,000 - (d) Mistake: Goods returned from Mahesh Rs 1,000 were recorded through Purchases Return Book (should have been Sales Return). Mahesh correctly credited. Rectification:

Dr Sales Return Rs 1,000

Cr Purchases Return Rs 1,000 - (e) Mistake: Goods returned to Naresh Rs 2,000 recorded through Purchases Book though Naresh was correctly debited. Rectification:

Dr Purchases Return Rs 2,000

Cr Purchases Rs 2,000

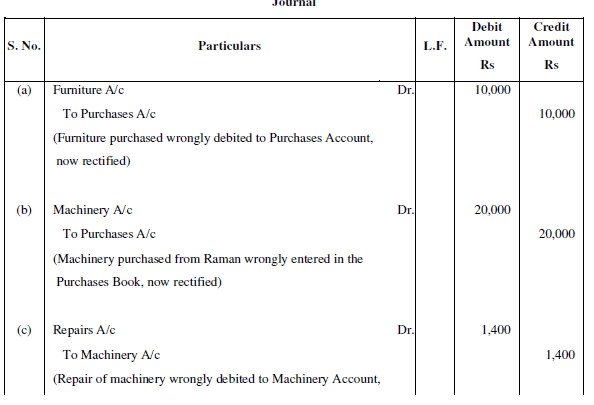

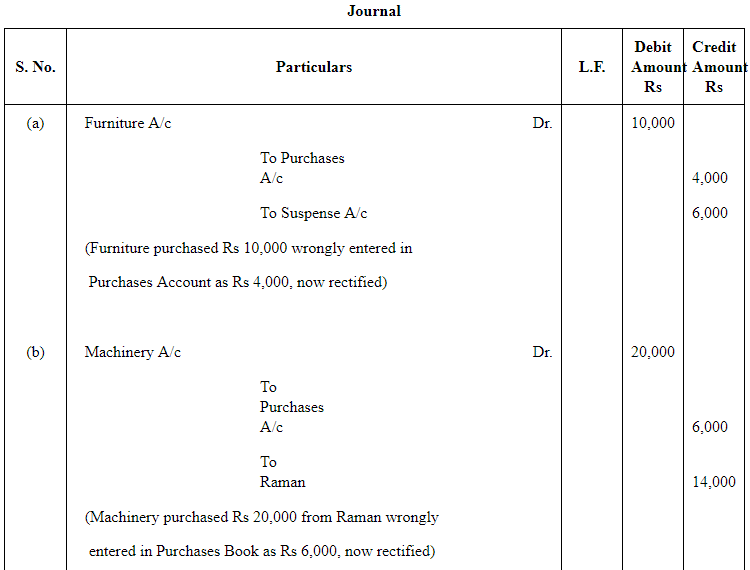

Question 14 : Rectify the following errors:

(a) Furniture purchased for Rs 10,000 wrongly debited to purchases account.(b) Machinery purchased on credit from Raman for Rs 20,000 was recorded through purchases book.

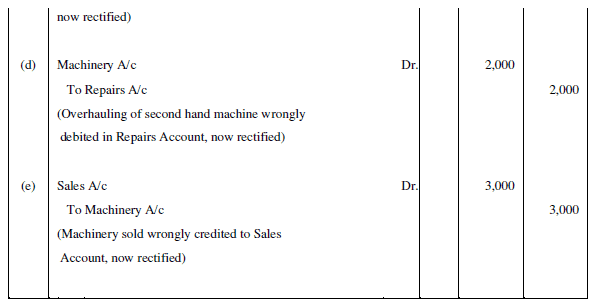

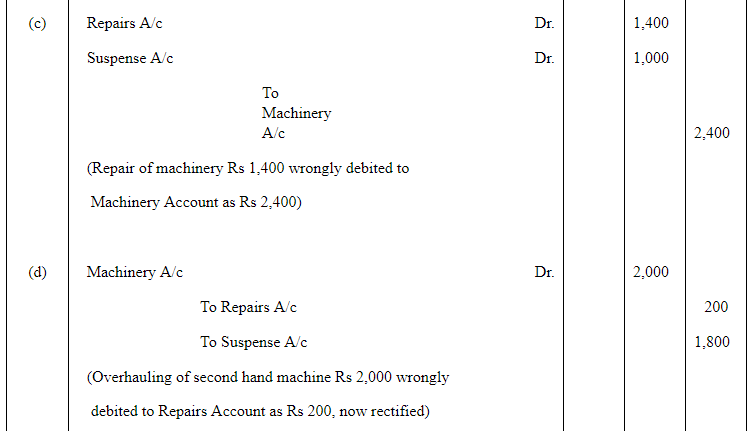

(c) Repairs on machinery Rs 1,400 debited to machinery account.

(d) Repairs on overhauling of secondhand machinery purchased Rs 2,000 was debited to Repairs account.

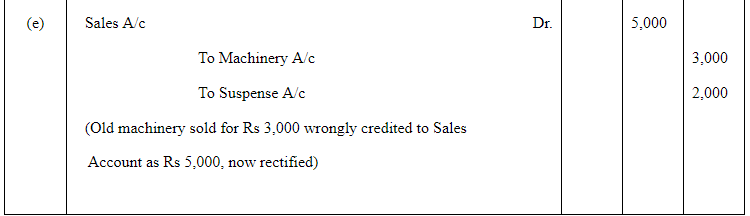

(e) Sale of old machinery at book value of Rs 3,000 was credited to sales account.

Answer :

Ans:

- (a) Rectification entry:

Dr Furniture Rs 10,000

Cr Purchases Rs 10,000

Note: Purchase of furniture is a capital asset; it must be debited to Furniture (Asset) not Purchases (Expense). - (b) Rectification entry:

Dr Machinery Rs 20,000

Cr Raman Rs 20,000

Note: Recording through Purchases Book created an expense entry; correct treatment is to record asset (Machinery) and creditor (Raman). - (c) Rectification entry:

Dr Repairs Rs 1,400

Cr Machinery Rs 1,400

Note: Repairs are an expense and should be debited to Repairs account; machinery account should be credited to reverse the wrong capitalisation. - (d) Rectification entry:

Dr Machinery Rs 2,000

Cr Repairs Rs 2,000

Note: Overhauling cost of second-hand machinery increases the cost of machinery (capital expenditure), not a revenue repairs expense. - (e) Rectification entry:

Dr Sales Rs 3,000

Cr Machinery (or Accumulated Depreciation/Old Machinery A/c) Rs 3,000

Note: Sale of old machinery at book value should not be credited to Sales (revenue). It should reduce the asset account or be recorded through a specific disposal account.

Question 15 : Rectify the following errors assuming that suspension account was opened. Ascertain the difference in trial balance.

(a) Furniture purchased for Rs 10,000 wrongly debited to purchase account as Rs 4,000.

(b) Machinery purchased on credit from Raman for Rs 20,000 recorded through Purchases Book as Rs 6,000.

(c) Repairs on machinery Rs 1,400 debited to Machinery account as Rs 2,400.(d) Repairs on overhauling of second hand machinery purchased Rs 2,000 was debited to Repairs account as Rs 200

(e) Sale of old machinery at book value Rs 3,000 was credited to sales account as Rs 5,000.

Answer :

Ans:

- (a) Error details: Furniture Rs 10,000 should be debited to Furniture A/c but Purchases was debited as Rs 4,000. Net effect:

- Purchases was understated by Rs 6,000 (should have been Rs 0 for furniture) and Furniture understated by Rs 10,000 → trial balance difference arises.

Rectification (using Suspense):

Dr Furniture Rs 10,000

Cr Purchases Rs 4,000

Cr Suspense Rs 6,000 - (b) Error details: Machinery Rs 20,000 recorded through Purchases Book as Rs 6,000 (wrong amount and wrong book). Rectification:

Dr Machinery Rs 20,000

Cr Raman Rs 20,000

Then reverse the incorrect Purchases posting:

Dr Suspense Rs 6,000

Cr Purchases Rs 6,000 - (c) Error details: Repairs Rs 1,400 debited to Machinery as Rs 2,400. Net effect: Machinery overstated and Repairs understated/overstated depending on net entries.

Rectification:

Dr Repairs Rs 1,400

Dr Suspense Rs 1,000

Cr Machinery Rs 2,400 - (d) Error details: Overhauling Rs 2,000 should be capitalised to Machinery, but was debited to Repairs as Rs 200. Rectification:

Dr Machinery Rs 2,000

Cr Repairs Rs 200

Cr Suspense Rs 1,800 - (e) Error details: Sale of old machinery at book value Rs 3,000 was credited to Sales as Rs 5,000 (excess credit of Rs 2,000). Rectification:

Dr Sales Rs 2,000

Dr Suspense Rs 1,000

Cr Machinery (or Disposal A/c) Rs 3,000

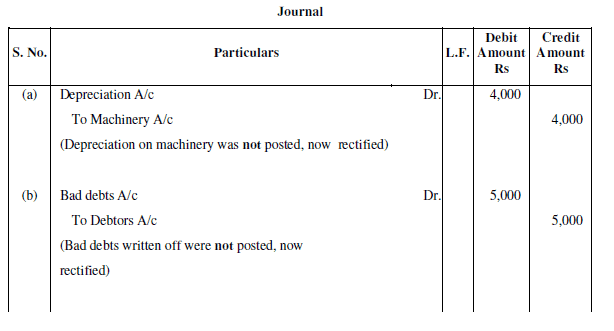

Question 16 : Rectify the following errors:

(a) Depreciation provided on machinery Rs 4,000 was not posted.

(b) Bad debts written off Rs 5,000 were not posted.

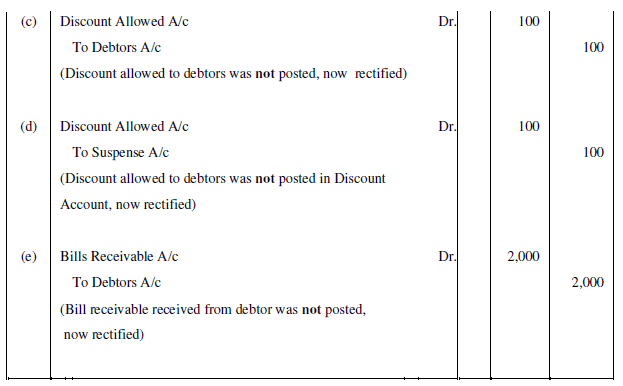

(c) Discount allowed to a debtor Rs 100 on receiving cash from him was not posted.

(d) Discount allowed to a debtor Rs 100 on receiving cash from him was not posted to discount account.

(e) Bill receivable for Rs 2,000 received from a debtor was not posted.

Answer :

Ans:

- (a) Rectification entry:

Dr Depreciation A/c Rs 4,000

Cr Machinery (Accumulated Depreciation) Rs 4,000

Note: Provision for depreciation is an expense and reduces the carrying amount of the asset. - (b) Rectification entry:

Dr Bad Debts A/c Rs 5,000

Cr Debtors Rs 5,000 - (c) If discount allowed of Rs 100 was not posted at all (neither to debtor nor to discount allowed):

Rectification entry:

Dr Discount Allowed Rs 100

Cr Debtor Rs 100 - (d) If discount was posted to debtor but not to Discount Allowed account (i.e., only debtor credited):

Rectification entry:

Dr Discount Allowed Rs 100

Cr Suspense (or appropriate clearing) Rs 100 - but usually just Dr Discount Allowed and Cr Cash/Bank if cash entry missing. Confirm ledger state and then post Dr Discount Allowed Rs 100; Cr Cash/Bank or adjust accordingly. - (e) Bill receivable for Rs 2,000 received from a debtor not posted:

Rectification entry:

Dr Bills Receivable Rs 2,000

Cr Debtor Rs 2,000

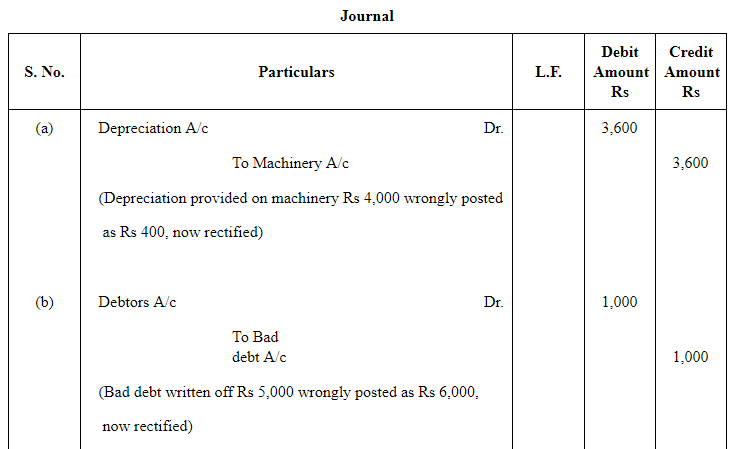

Question 17 : Rectify the following errors:

(a) Depreciation provided on machinery Rs 4,000 was posted as Rs 400.

(b) Bad debts written off Rs 5,000 were posted as Rs 6,000.

(c) Discount allowed to a debtor Rs 100 on receiving cash from him was posted as Rs 60.

(d) Goods withdrawn by proprietor for personal use Rs 800 were posted as Rs 300.

(e) Bill receivable for Rs 2,000 received from a debtor was posted as Rs 3,000.

Answer :

Ans:

- (a) Difference: Rs 4,000 should have been posted; Rs 400 posted → short by Rs 3,600.

Rectification:

Dr Depreciation A/c Rs 3,600

Cr Machinery (or Accumulated Depreciation) Rs 3,600 - (b) Difference: Bad debts written off Rs 5,000 posted as Rs 6,000 → excess Rs 1,000.

Rectification:

Dr Debtors Rs 1,000

Cr Bad Debts A/c Rs 1,000 - (c) Difference: Discount allowed Rs 100 posted as Rs 60 → short by Rs 40.

Rectification:

Dr Discount Allowed Rs 40

Cr Debtor Rs 40 - (d) Difference: Drawings Rs 800 posted as Rs 300 → short by Rs 500.

Rectification:

Dr Drawings Rs 500

Cr Purchases (or the wrong account where Rs 300 was posted) Rs 500 - reverse the wrong Rs 300 if necessary and post correct Rs 800 total. - (e) Difference: Bill receivable Rs 2,000 posted as Rs 3,000 → excess Rs 1,000 posted.

Rectification:

Dr Bills Receivable Rs 2,000 (to bring to correct balance) and

Dr Debtor Rs 1,000

Cr Bills Receivable Rs 3,000

Alternatively: Dr Debtor Rs 1,000

Cr Bills Receivable Rs 1,000 (to correct the excess).

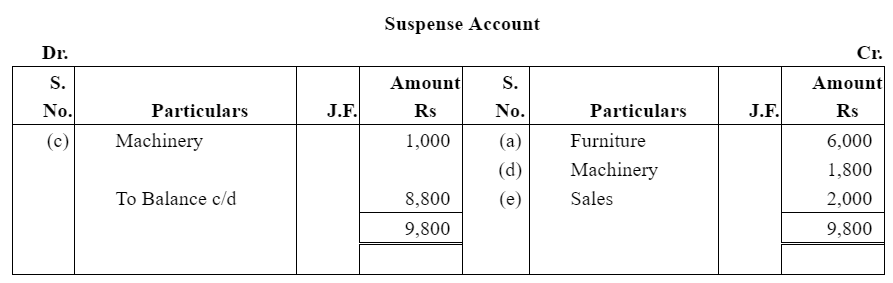

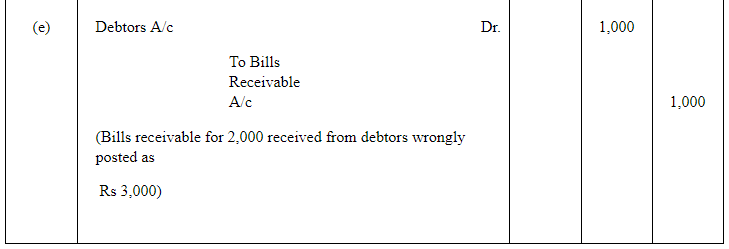

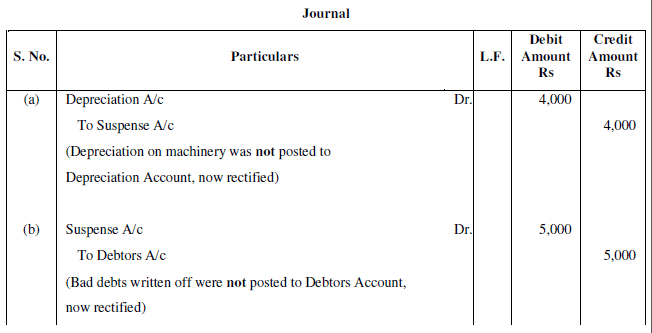

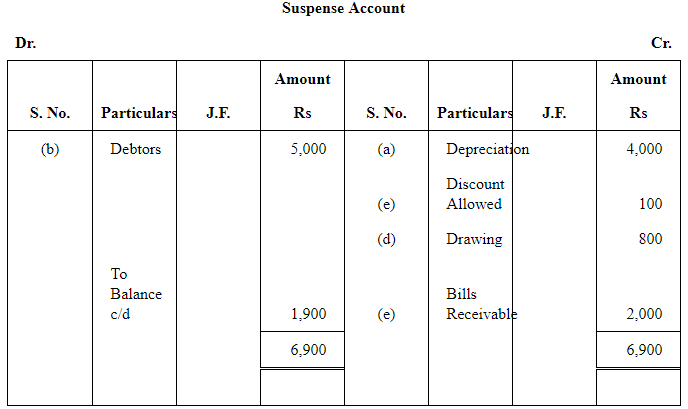

Question 18 : Rectify the following errors assuming that suspense account was opened. Ascertain the difference in trial balance.

(a) Depreciation provided on machinery Rs 4,000 was not posted to Depreciation account.

(b) Bad debts written-off Rs 5,000 were not posted to Debtors account.

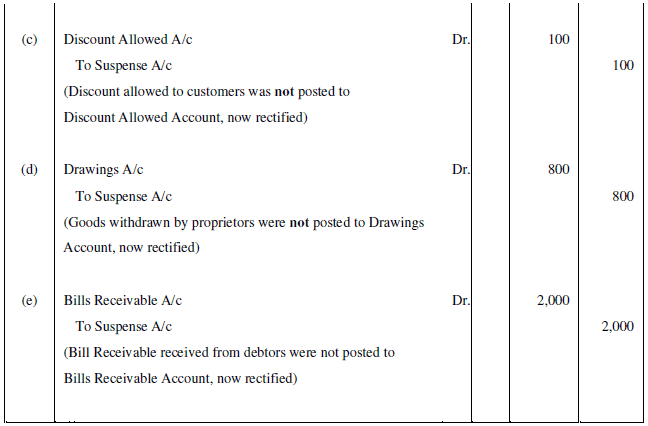

(c) Discount allowed to a debtor Rs 100 on receiving cash from him was not posted to discount allowed account.

(d) Goods withdrawn by proprietor for personal use Rs 800 were not posted to Drawings account.

(e) Bill receivable for Rs 2,000 received from a debtor was not posted to Bills receivable account.

Answer :

Ans:

- (a) Mistake: Depreciation Rs 4,000 not posted to Depreciation A/c. Effect on trial balance: Credits exceed debits by Rs 4,000 (since machinery credit was likely passed but expense debit omitted).

Rectification:

Dr Depreciation A/c Rs 4,000

Cr Suspense Rs 4,000

Then later reverse Suspense when cleared. - (b) Mistake: Bad debts Rs 5,000 not posted to Debtors A/c. Effect:

- Debtors overstated by Rs 5,000; trial balance difference: debits exceed credits by Rs 5,000.

Rectification:

Dr Bad Debts Rs 5,000

Cr Debtors Rs 5,000

Or, if Suspense was used initially: Dr Suspense Rs 5,000

Cr Debtors Rs 5,000 - (c) Mistake: Discount allowed Rs 100 not posted to Discount Allowed A/c. Effect on trial balance: Debits exceed credits by Rs 100 (discount is an expense/debit).

Rectification:

Dr Discount Allowed Rs 100

Cr Suspense Rs 100 (or Cr Cash/Bank if cash posting missing) - (d) Mistake: Drawings Rs 800 not posted to Drawings account. Effect: Debits exceed credits by Rs 800.

Rectification:

Dr Drawings Rs 800

Cr Suspense Rs 800 - (e) Mistake: Bill receivable Rs 2,000 not posted to Bills Receivable account. Effect: Credits exceed debits by Rs 2,000 (or debits short by Rs 2,000) depending on the cash/debtor entry made.

Rectification:

Dr Bills Receivable Rs 2,000

Cr Suspense Rs 2,000

FAQs on NCERT Solution (Part - 3) - Trial Balance and Rectification of Errors

| 1. What is the purpose of a trial balance in accounting? |  |

| 2. How do you prepare a trial balance? | |

| 3. What are the types of errors that can occur in a trial balance? | |

| 4. How can errors in a trial balance be rectified? | |

| 5. What is the significance of a balanced trial balance? | |