NCERT Solutions (Part - 1) - Depreciation, Provisions, and Reserves

Short Answer Questions

Q1. What is 'Depreciation'?

Ans: Depreciation is the decrease in the value of a fixed asset over time due to factors such as wear and tear, obsolescence and normal use. It is charged periodically to allocate the cost of the asset over its useful life. Common depreciable assets include machinery, furniture and buildings. Land is normally not depreciated because its value usually rises rather than falls.

Q2. State briefly the need for providing depreciation.

Ans: The main reasons for providing depreciation are:

- To recognise that fixed assets lose value over time due to wear and tear and usage.

- To present a true and fair view of the financial position by showing assets at their written down value.

- To match the cost of an asset with the revenue it helps to generate in each accounting period (matching principle).

- To provide funds gradually for replacement of the asset in future.

- To comply with statutory and tax requirements which often require depreciation to be charged in the accounts.

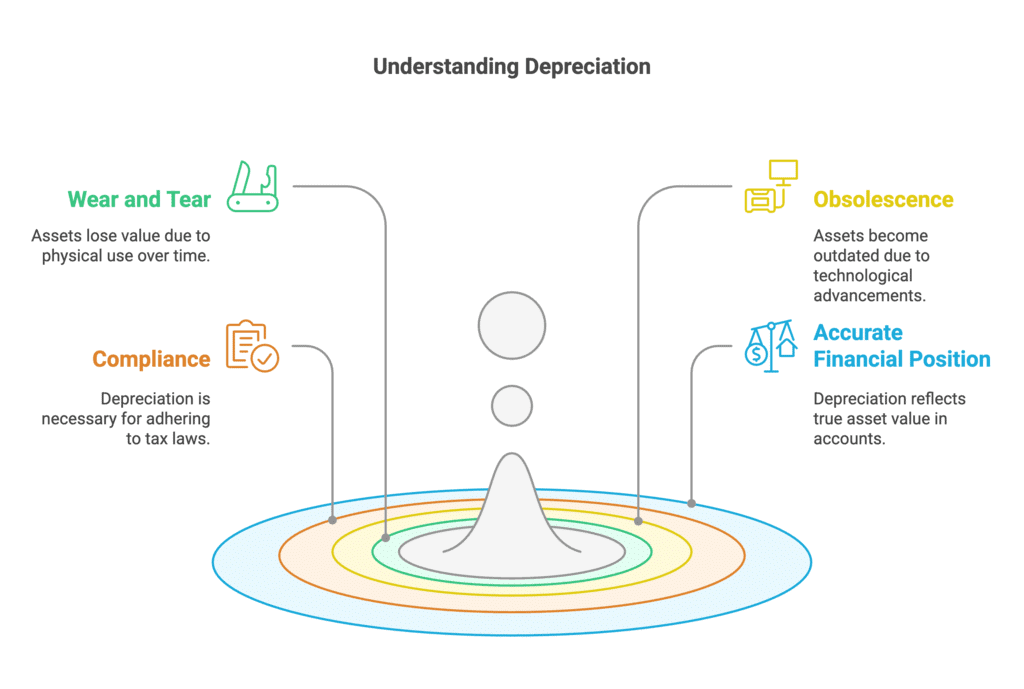

Q3. What are the causes of depreciation?

Ans: Common causes of depreciation are:

- Physical wear and tear: Regular use causes parts to wear out and value to fall.

- Obsolescence: Technological change or changes in market demand may make an asset less useful.

- Inadequacy: An asset may become inadequate to meet the requirements because of increased scale or changed processes.

- Depletion: Certain natural resources (for example, mines, oil wells) get exhausted with use.

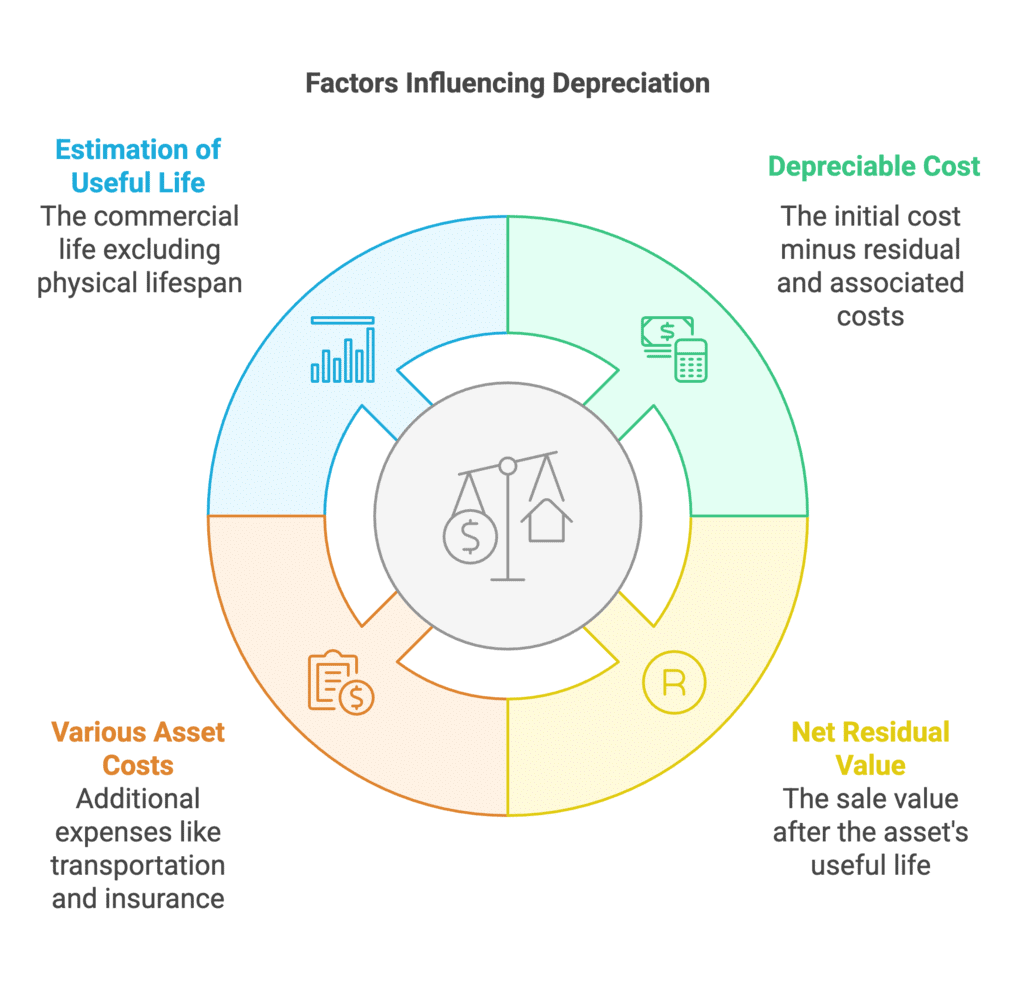

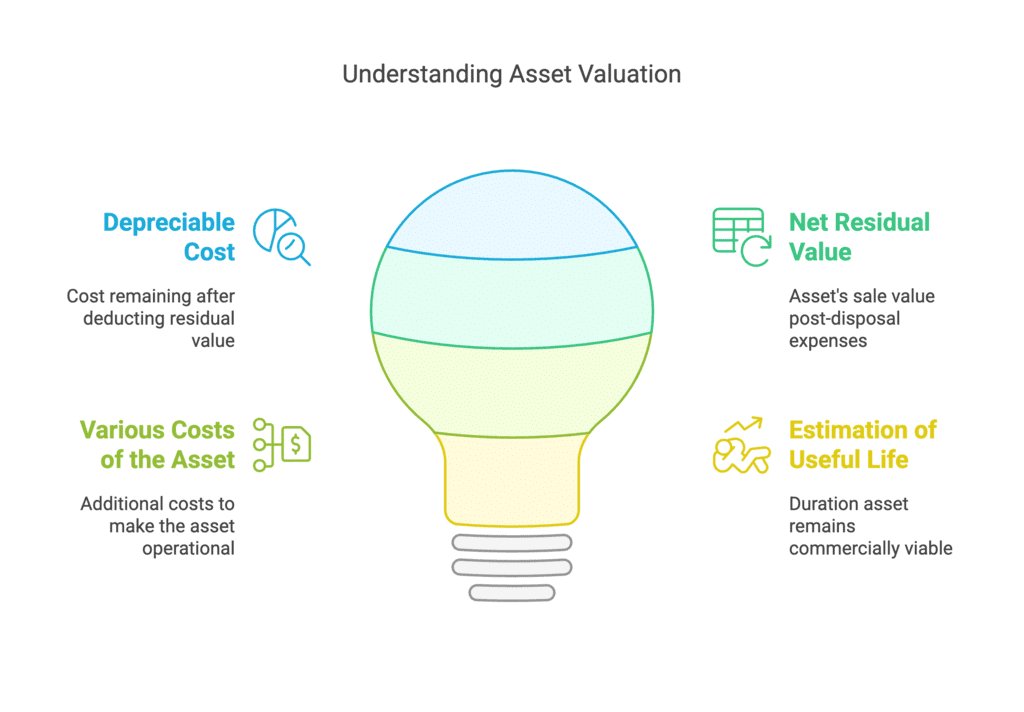

Q4. Explain basic factors affecting the amount of depreciation.

Ans: The principal factors that determine the amount of depreciation are:

- Depreciable cost: This is the cost to be depreciated and is calculated as cost of asset less its residual (scrap) value. Depreciation over the asset's life should in total equal this amount.

- Residual value (scrap value): The estimated value of the asset at the end of its useful life, after deducting disposal expenses.

- Additional costs: Expenses incurred to bring the asset to working condition (transportation, installation, insurance) form part of the asset's cost and affect depreciation.

- Estimated useful life: The period over which the asset is expected to be economically usable by the business. A longer useful life leads to a lower annual depreciation and vice versa.

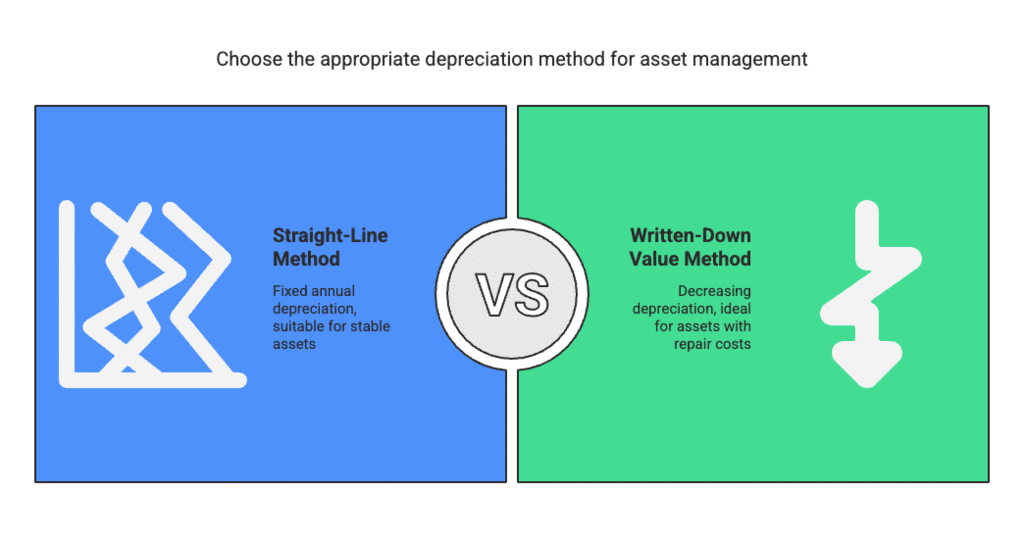

Q5. Distinguish between straight-line method and written-down value method of calculating depreciation.

Ans: Key differences between the straight-line method (SLM) and the written-down value method (WDV) are:

- Basis of calculation: SLM charges depreciation on the original (or depreciable) cost of the asset equally over its useful life. WDV charges depreciation on the carrying or book value of the asset at the beginning of each year.

- Amount each year: SLM gives a constant annual depreciation. WDV gives a declining amount each year.

- Effect on profits: Under SLM the charge is even across years; under WDV the charge is higher in early years and lower later, which often better matches assets that lose value faster initially.

- Tax treatment: In practice, tax authorities commonly allow depreciation on a written-down value basis for many asset classes.

- Suitability: SLM suits assets with even utility and low repair costs (for example, some buildings). WDV suits assets which are more productive or more valuable in early years or which incur higher repairs later (for example, machinery subject to rapid technological change).

Q6. "In case of a long term asset, repair and maintenance expenses are expected to rise in later years than in earlier year". Which method is suitable for charging depreciation if the management does not want to increase burden on profits and loss account on account of depreciation and repair.

Ans: The written-down value method is more suitable in this situation. This is because WDV charges higher depreciation in the early years and smaller amounts in later years. As repair and maintenance expenses rise in later years, the lower depreciation charge in those years helps prevent a large combined burden on the profit and loss account. Thus, WDV gives a better matching of expenses over the asset's life.

Q7. What are the effects of depreciation on profit and loss account and balance sheet?

Ans: The effects of depreciation are:

- On the profit and loss account: Depreciation is an expense and reduces the profit for the period. A higher depreciation charge lowers net profit; a lower charge increases it.

- On the balance sheet: Depreciation reduces the carrying amount of fixed assets. If accumulated depreciation is shown separately, the gross asset appears on the asset side and accumulated depreciation as a contra-asset (reduction) or provision. Lower asset values affect net worth and financial ratios (for example, return on assets).

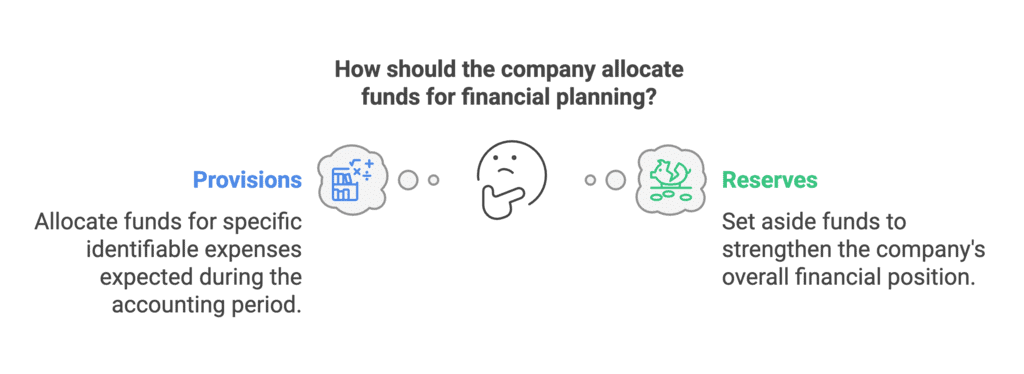

Q8. Distinguish between 'provision' and 'reserve'.

Ans: Major differences between provision and reserve are:

- Nature: A provision is a charge against profit to meet a known liability or probable loss (for example, provision for doubtful debts). A reserve is an appropriation of profits kept aside to strengthen the financial position (for example, general reserve).

- Purpose: Provisions are made to cover expected liabilities or reduction in asset values. Reserves are created out of profits to build financial strength or for specified purposes.

- Presentation: Provisions are shown as liabilities or as a deduction from the related asset (depending on the type). Reserves form part of shareholders' funds (equity) under the liabilities side of the balance sheet.

- Effect on profit: Provision reduces the profit in the period it is created. Reserve is created out of profit after it is computed (an appropriation) and does not reduce taxable profit.

- Requirement: Provisions are often required by accounting standards or prudence. Creation of reserves (except where mandated) is generally at the company's discretion.

- Distribution: Provisions are not distributable as dividends. Reserves (subject to legal restrictions) may be used for dividends or other corporate purposes.

Q9. Give four examples each of 'provision' and 'reserves'.

Ans: Examples are:

Provisions:

- Provision for bad and doubtful debts

- Provision for depreciation (accumulated depreciation)

- Provision for taxation

- Provision for warranties or repairs

Reserves:

- General reserve

- Capital reserve

- Debenture redemption reserve

- Dividend equalisation reserve

Q10. Distinguish between 'revenue reserve' and 'capital reserve'.

Ans: The differences between revenue reserves and capital reserves are:

- Source: Revenue reserves are created from revenue profits (profits earned from regular business operations). Capital reserves arise from capital profits (non-operating gains such as profit on sale of fixed assets).

- Purpose and use: Revenue reserves are generally available for distribution as dividends (subject to law) or for general corporate needs. Capital reserves are usually kept for specific capital purposes and are not normally available for distribution as dividends.

- Examples: Revenue reserve - general reserve; Capital reserve - reserve arising from revaluation surplus or premium on share issue.

Q11. Give four examples each of 'revenue reserve' and 'capital reserves'.

Ans: Examples of revenue reserves:

- General reserve

- Dividend equalisation reserve

- Workers' compensation reserve

- Debenture redemption reserve

Examples of capital reserves:

- Share premium (premium on issue of shares)

- Premium on issue of debentures

- Profit on sale of fixed assets (capital profit)

- Revaluation reserve (profit on revaluation of fixed assets)

Q12. Distinguish between 'general reserve' and 'specific reserve'.

Ans: A general reserve is created out of profits without any specific purpose and can be used for various corporate needs (expansion, writing off losses, dividend smoothing). A specific reserve is created for a particular purpose (for example, dividend equalisation reserve or debenture redemption reserve) and is to be used only for that stated purpose.

Q13. Explain the concept of 'secret reserve'.

Ans: The secret reserve is a financial concept used to manage a business's tax liability. It helps to combine profits made in profitable years with losses incurred in others, ultimately aiming to increase net profits. Notably, the secret reserve is not presented on the company's Balance Sheet. It is typically created through:

- High depreciation rates on assets.

- Classifying contingent liabilities as actual liabilities.

- Making excessive provisions for doubtful debts.

Establishing a secret reserve is permissible, provided it remains within reasonable limits.

Long Answer Questions

Q1. Explain the concept of depreciation. What is the need for charging depreciation and what are the causes of depreciation?

Ans: Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life. It recognises that fixed assets (such as machinery, furniture and buildings) lose economic value with use, passage of time or obsolescence. Land is generally excluded as it usually appreciates.

Need for charging depreciation:

- To record the reduction in the asset's value and present a true and fair view of the financial position.

- To match the cost of the asset with the revenue it helps to generate in the relevant accounting periods (matching principle).

- To provide for replacement of the asset in future by setting aside funds gradually.

- To comply with statutory and tax requirements which usually require depreciation to be charged.

Causes of depreciation:

- Wear and tear: Normal physical deterioration through use.

- Obsolescence: Technological progress or changes in market preferences.

- Depletion: Reduction in natural resources as they are used up.

- Accidental damage or inadequacy: Loss of value due to accidents or because the asset no longer meets business requirements.

Q2. Discuss in detail the straight line method and written down value method of depreciation. Distinguish between the two and also give situations where they are useful.

Ans: The two common methods of charging depreciation are:

Straight-Line Method (SLM):

- Under SLM, an equal amount of depreciation is charged every year over the asset's useful life.

- Annual depreciation = (Cost of asset - Residual value) ÷ Useful life.

- Advantages: simple to apply, easy to budget for, gives uniform charge to profit and loss account.

- Suitable where the asset's use and benefits are expected to be uniform over time (some buildings, office furniture).

Written-Down Value Method (WDV):

- WDV charges depreciation on the written down (book) value of the asset at the beginning of each year. The charge therefore declines year by year.

- Annual depreciation = Written down value × Rate of depreciation.

- Advantages: matches higher consumption or obsolescence in earlier years, recognised by many tax authorities, reduces profit impact in later years when repairs may be higher.

- Suitable for assets which are more useful or productive in early years or which become obsolete quickly (machinery subject to rapid technological change).

Differences and usefulness are summarised in Q5 above. Choice of method depends on the asset's pattern of economic benefits and tax or regulatory considerations.

Q3. Describe in detail two methods of recording depreciation. Also, give the necessary journal entries.

Ans: Depreciation can be recorded in the books in two principal ways:

(I) Charging depreciation directly to the asset account - Under this approach, the asset account is reduced directly by the amount of depreciation. The net amount (cost less depreciation) appears in the balance sheet. The balance sheet thus shows the net value of the asset after depreciation is deducted. The journal entries in this method are as follows:

- Subtracting depreciation from the asset's cost

- To charge the depreciation to profit and loss account

(II) Creating a provision (accumulated depreciation) separately - Here depreciation is credited to a separate provision account often called Provision for Depreciation or Accumulated Depreciation. The asset is shown at its gross cost in the balance sheet and the accumulated depreciation is shown as a deduction (contra asset) or as a separate item. This method keeps the original cost of the asset visible and shows total depreciation charged to date.

The journal entries in this method are as follows:

- Including depreciation in the depreciation provision

- To charge the depreciation to profit and loss account

Q4. Explain the determinants of the amount of depreciation.

Ans:

- Depreciable cost: The total amount to be depreciated is the asset's cost less its residual (scrap) value. This amount is allocated over the useful life.

- Residual value: Expected realisable value at the end of the asset's useful life, after disposal costs are deducted.

- Additional costs: Costs necessary to bring the asset to working condition (freight, installation, reconditioning) are included in the asset cost and affect the depreciation base.

- Estimated useful life: The expected period during which the asset will provide economic benefits. Shorter useful life increases annual depreciation and vice versa.

Q5. Name and explain different types of reserves in detail.

Ans: Reserves are accumulated profits set aside to strengthen the financial position of a business. Major types are:

1. Revenue Reserves: Created from profits arising in the normal course of business. They may be:

- General reserve: No specific purpose; available for various corporate needs like expansion, contingencies or dividend smoothing.

- Specific reserve: Created for a particular purpose (for example, debenture redemption reserve, dividend equalisation reserve).

2. Capital Reserves: Arise from capital profits which are not derived from ordinary trading activities (for example, profit on sale of fixed assets, premium on issue of shares). Capital reserves are generally not available for distribution as dividends and are used for capital purposes.

- Examples: premium on share issue, profit on sale of fixed assets, profit on reissue of forfeited shares, profit before incorporation.

3. Secret Reserves: Reserves created by understating assets or overstating liabilities so that profit is understated in the published accounts. They are not shown in the balance sheet and reduce apparent profitability. Intentionally creating secret reserves to mislead stakeholders is inconsistent with transparency; company law and accounting standards require disclosure of material facts and accounting policies.

Q6. What are 'provisions'. How are they created? Give accounting treatment in case of provision for doubtful Debts.

Ans: Provisions are amounts set aside out of profits to meet a known liability or a probable loss whose amount cannot be determined with certainty. They are recorded in the accounts as either liabilities or as deductions from the related assets.

Creation: A provision is created by charging the profit and loss account and crediting a provision account (or by deducting from the related asset). For example, provision for doubtful debts is created to cover debts that are considered unlikely to be fully recovered.

Accounting treatment for provision for doubtful debts is typically shown in the solution images. In brief:

- Make the provision: debit Profit & Loss A/c (or Bad Debt Expense) and credit Provision for Doubtful Debts.

- If a specific bad debt is written off: debit Provision for Doubtful Debts (or Bad Debts A/c) and credit Debtors.

- If recovery of a previously written-off debt occurs: debit Bank and credit Profit & Loss A/c or Provision for Doubtful Debts, depending on the step taken.

Numerical Question Answers

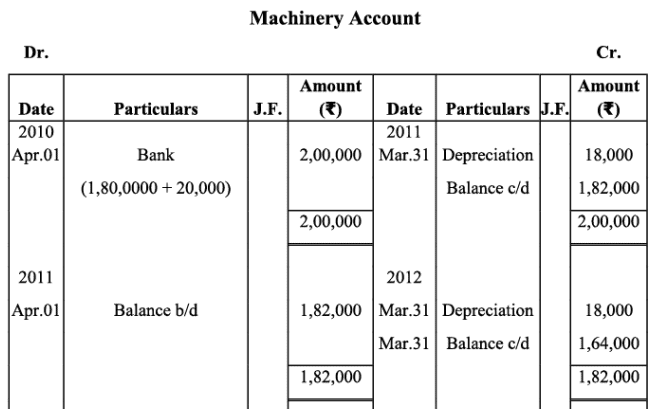

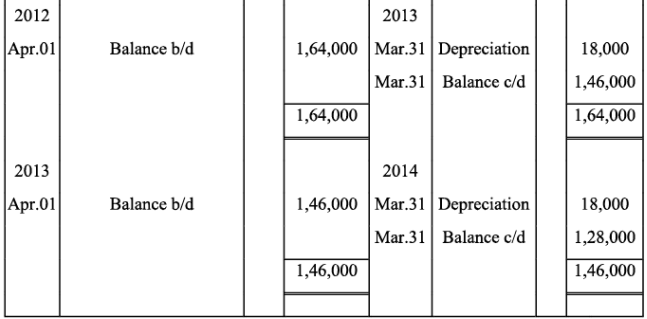

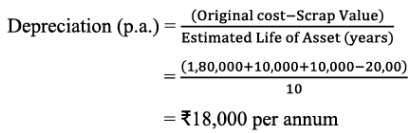

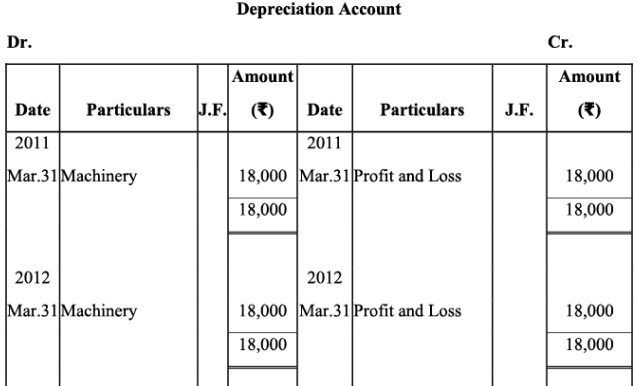

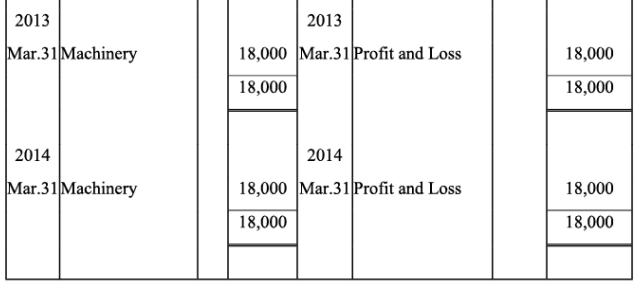

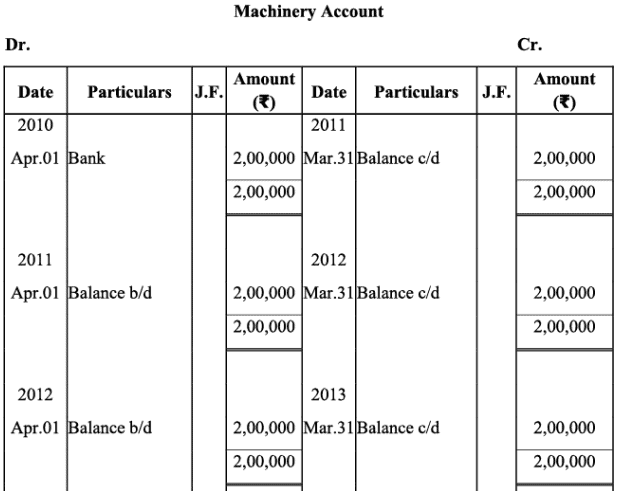

Q1: On April l, 2010, Bajrang Marbles purchased a Machine for Rs. 1,80,000 and spent Rs. 10,000 on its carnage and Rs. 10,000 on its installation. It is estimated that its working life is 10 years and after 10 years its scrap value will be Rs. 20,000.

(a)Prepare Machine account and Depreciation account for the first four years by providing depreciation on straight line method. Accounts are closed on March 31st every year.

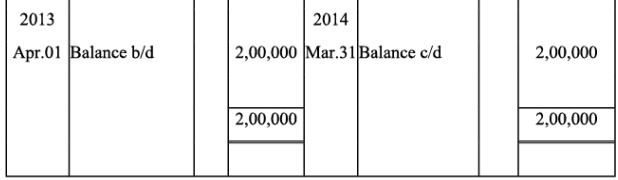

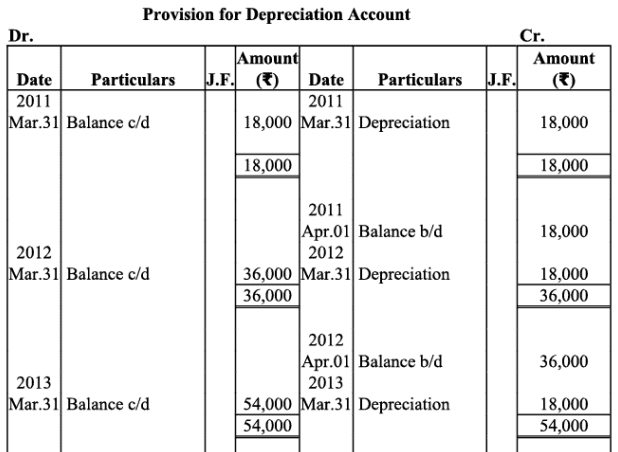

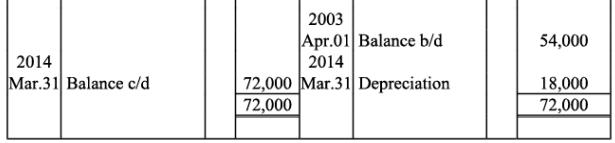

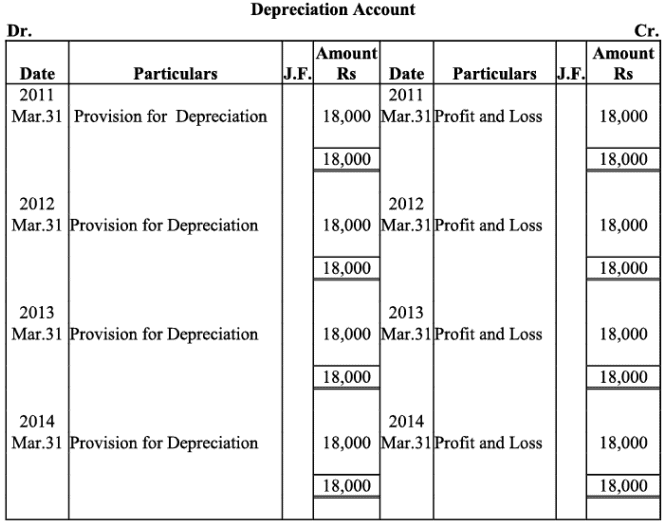

(b)Prepare Machine account, Depreciation account and Provision for depreciation account (or accumulated depreciation account) for the first four years by providing depreciation using straight line method accounts are closed on March 31 every year.

Ans:

(a) Books of Bajrang Marbles

Working notes: Calculation of annual depreciation

(b)

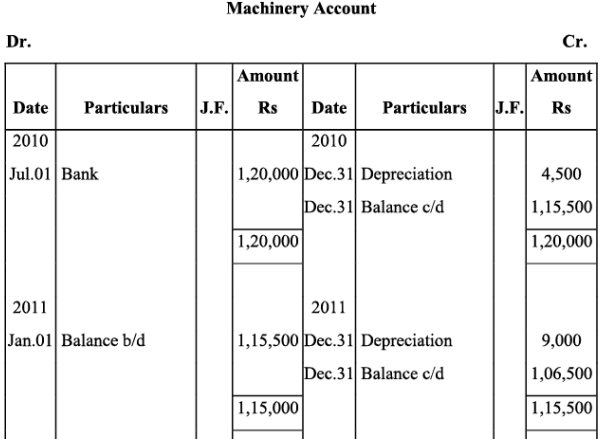

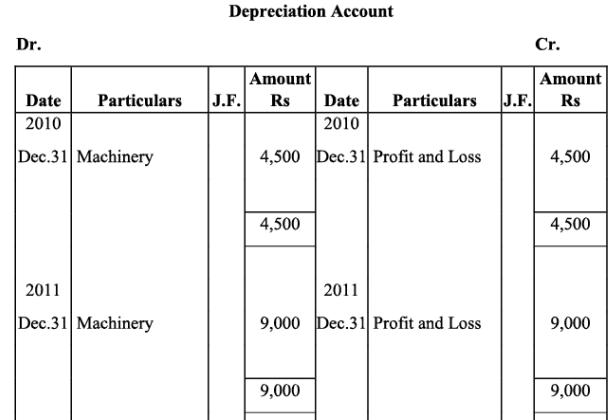

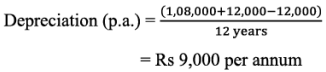

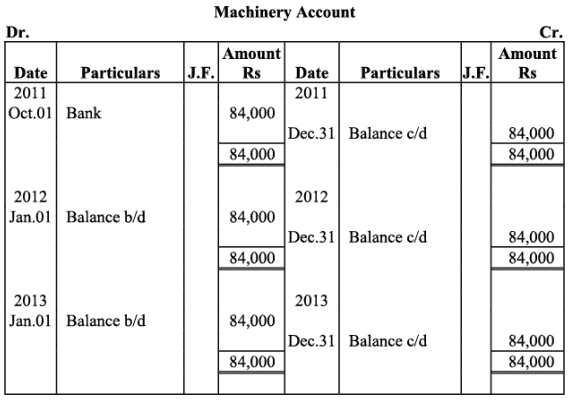

Q2: On July 01, 2010, Ashok Ltd. Purchased a Machine for Rs. 1,08,000 and spent Rs. 12,000 on its installation. At the time of purchase it was estimated that the effective commercial life of the machine will be 12 years and after 12 years its salvage value will be Rs. 12,000.

Prepare machine account and depreciation Account in the books of Ashok Ltd. For first three years, if depreciation is written off according to straight line method. The account are closed on December 31st, every year.

Ans: Books of Ashok Ltd.

Working Note: Calculation of annual depreciation

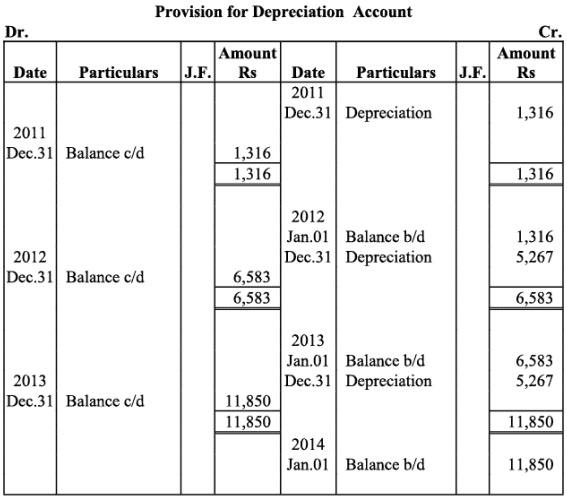

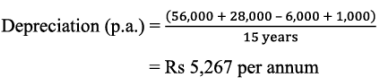

Q3: Reliance Ltd. Purchased a second hand machine for Rs. 56,000 on October 01, 2011 and spent Rs. 28,000 on its overhaul and installation before putting it to operation. It is expected that the machine can be sold for Rs. 6,000 at the end of its useful life of 15 years. Moreover, an estimated cost of Rs. 1,000 is expected to be incurred to recover the salvage value of Rs. 6,000. Prepare machine account and Provision for depreciation account for the first three years charging depreciation by fixed Instalment Method. Accounts are closed on March 31, every year.

Ans: Books of Reliance Ltd.

Working Note: Calculation of annual depreciation

Note: As per the solution, the balance of provision for depreciation account, as on March.31, 2015 is Rs 11,850; whereas, as per the book, it is Rs 18,200. However, if we ignore the scrap value and prepare provision for depreciation for 4 years, the answer would match to that of the book.

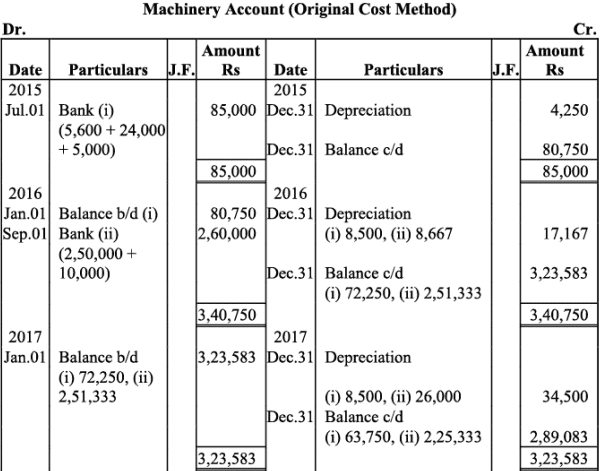

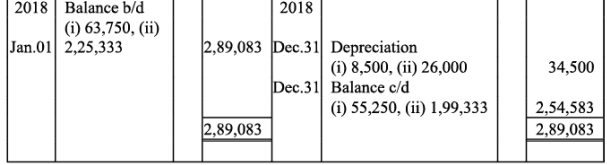

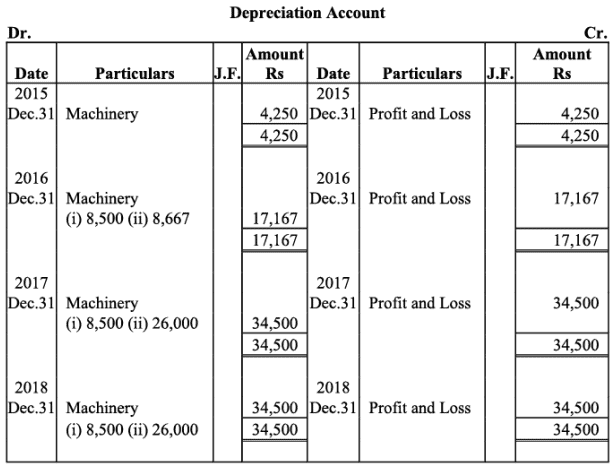

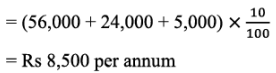

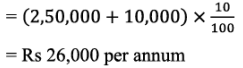

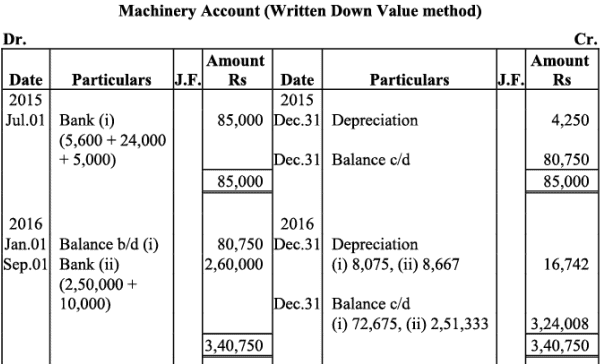

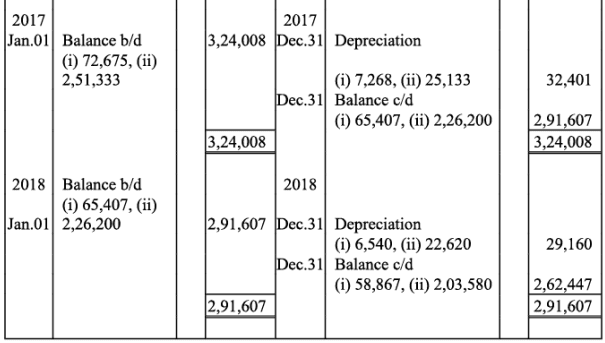

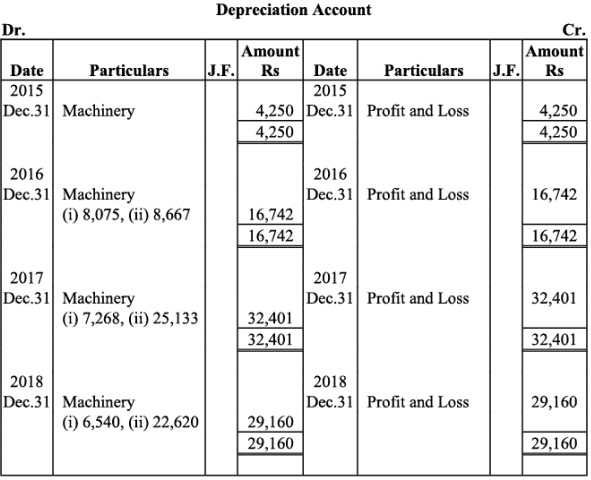

Q4: Berlia Ltd. Purchased a second hand machine for Rs 56,000 on July 01,2015 and spent Rs 24,000 on its repair and installation and Rs 5,000 for its carriage. On September 01, 2016, it purchased another machine for Rs 2,50,000 and spent Rs 10,000 on its installation.

(a) Depreciation is provided on machinery @10% p.a on original cost method annually on December 31. Prepare machinery account and depreciation account from the year 2015 to 2018.

(b) Prepare machinery account and depreciation account from the year 2015 to 20018, if depreciation is provided on machinery @10% p.a. on written down value method annually on December 31.

Ans:

(a)Books of Berlia Ltd.

Working notes: Calculation of annual depreciation

(i) Depreciation (p.a.) on Machinery Purchased on July 01, 2015

(ii) Depreciation (p.a.) on Machinery purchased on September 01, 2016.

(b)

FAQs on NCERT Solutions (Part - 1) - Depreciation, Provisions, and Reserves

| 1. What is depreciation and how is it calculated ? |  |

| 2. What are provisions and how do they differ from reserves ? | |

| 3. Why is it important for a business to maintain reserves ? | |

| 4. What are the different methods of calculating depreciation ? | |

| 5. How does depreciation affect a company's financial statements ? | |