NCERT Solution (Part - 3) - Depreciation, Provisions and Reserves

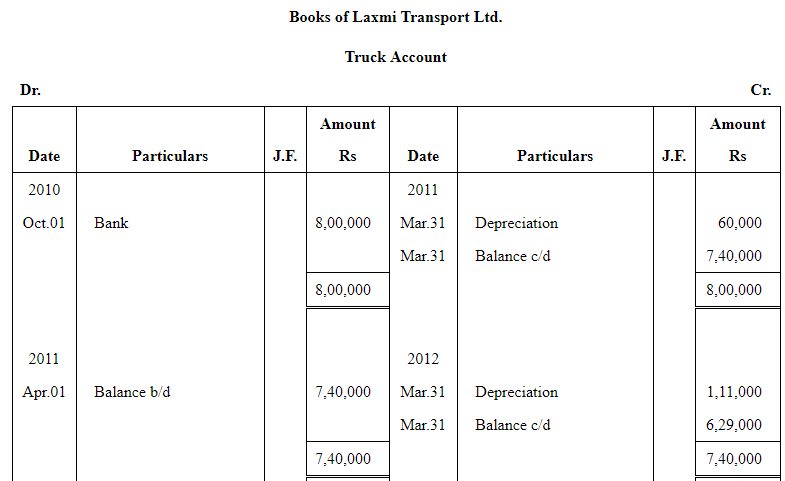

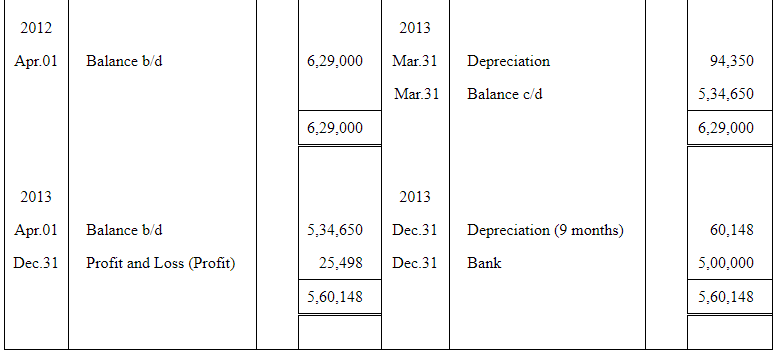

Question 13: On October 01, 2010, a Truck was purchased for Rs 8,00,000 by Laxmi Transport Ltd. Depreciation was provided at 15% p.a. on the diminishing balance basis on this truck. On December 31, 2013 this Truck was sold for Rs 5,00,000. Accounts are closed on 31st March every year. Prepare a Truck Account for the four years

Answer:

Note: As per the solution, the profit on the sale of truck, as on December 31, 2013 is Rs 25,498; however, the answer given in the book is Rs 58,237.

Explanation: Depreciation on diminishing balance is charged on the written down value (WDV) at the specified rate for the exact period the asset is held. Key points to check when reproducing the truck account and reconciling the difference shown above:

• Determine depreciation periods carefully: first year (2010-11) runs from 01 Oct 2010 to 31 Mar 2011 (6 months). Subsequent full years are charged for 12 months. For 2013-14 depreciation is required up to the date of sale (01 Apr 2013 to 31 Dec 2013 = 9 months) because the truck was sold on 31 Dec 2013.

• Apply 15% p.a. to the opening WDV for each full year and prorate for part-years: Depreciation for n months = (annual rate × WDV × n/12).

• Compute WDV immediately before sale, compare with sale proceeds to find profit or loss. Differences with the book answer may arise from: (a) different treatment of part-year depreciation (whether rounded or treated as full year), (b) rounding conventions, or (c) computational error. Recalculate each year's WDV using the prorated method above to verify which figure (Rs 25,498 or Rs 58,237) is correct.

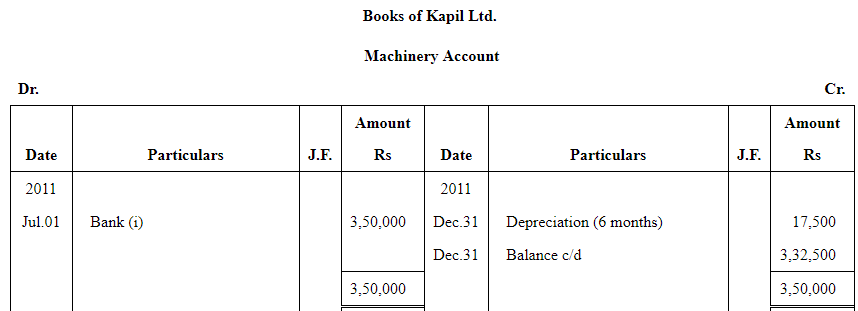

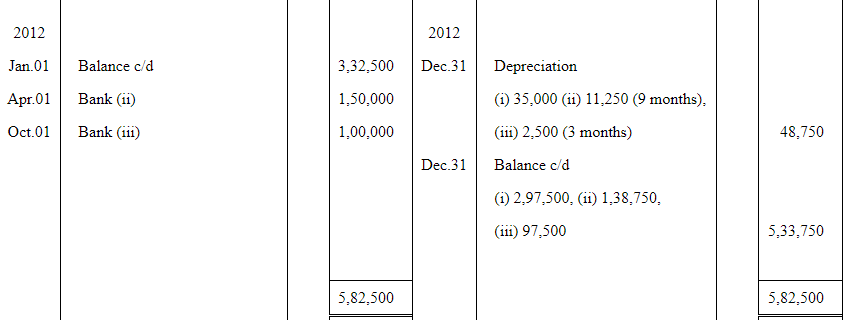

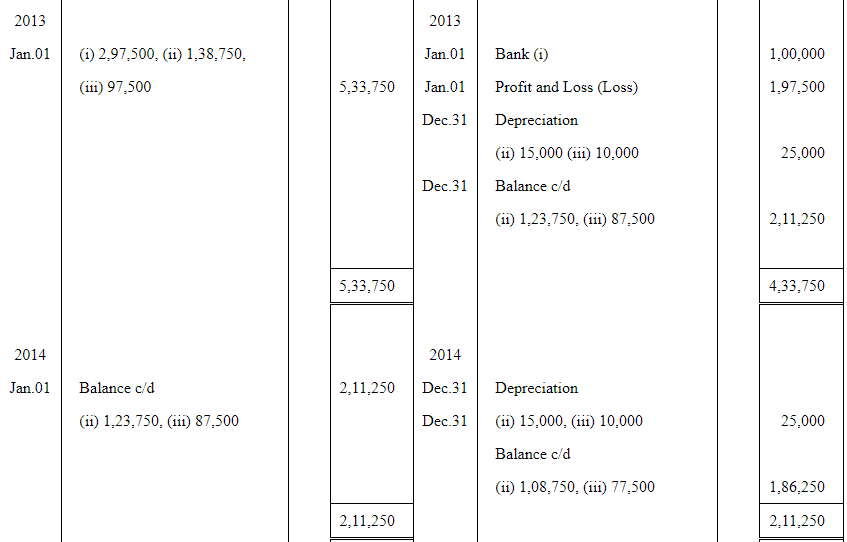

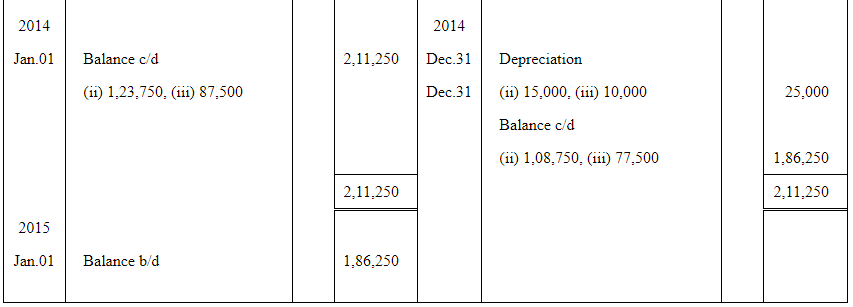

Question 14: Kapil Ltd. purchased a machinery on July 01, 2011 for Rs 3,50,000. It purchased two additional machines, on April 01, 2012 costing Rs 1,50,000 and on October 01, 2012 costing Rs 1,00,000. Depreciation is provided @10% p.a. on straight line basis. On January 01, 2013, first machinery become useless due to technical changes. This machinery was sold for Rs 1,00,000, prepare machinery account for 4 years on the basis of calendar year.

Answer:

Explanation: Under straight line method depreciation = cost × 10% p.a., prorated for part-years. Follow these steps to prepare the machinery account:

• Compute depreciation for each machine from its date of purchase to year-end (calendar year: 1 Jan-31 Dec). For the machine bought on 01 Jul 2011, first year (2011) depreciation is for 6 months (Jul-Dec).

• For the machines bought on 01 Apr 2012 and 01 Oct 2012, compute depreciation in 2012 for 9 months and 3 months respectively.

• The first machine became useless on 01 Jan 2013; no depreciation is taken for 2013 on it. On sale, compare the accumulated depreciation and carrying amount with sale proceeds to determine profit or loss.

• Post additions and disposals in the machinery ledger and balance each year. The image entries show the year-wise posting and final balances.

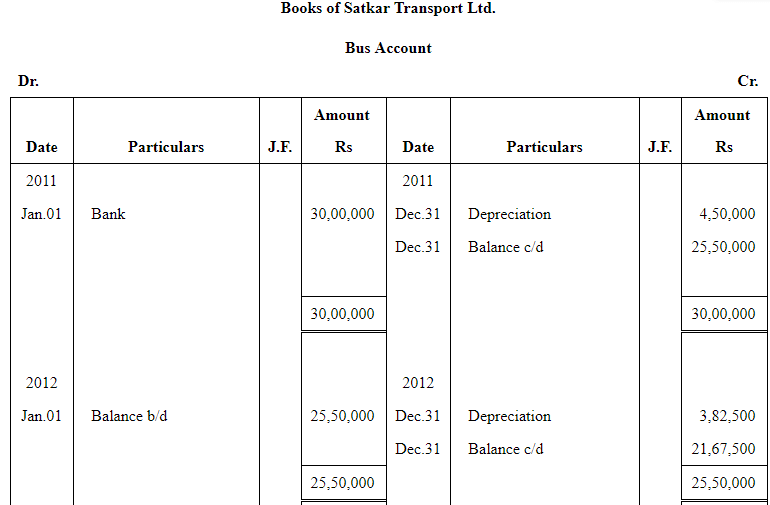

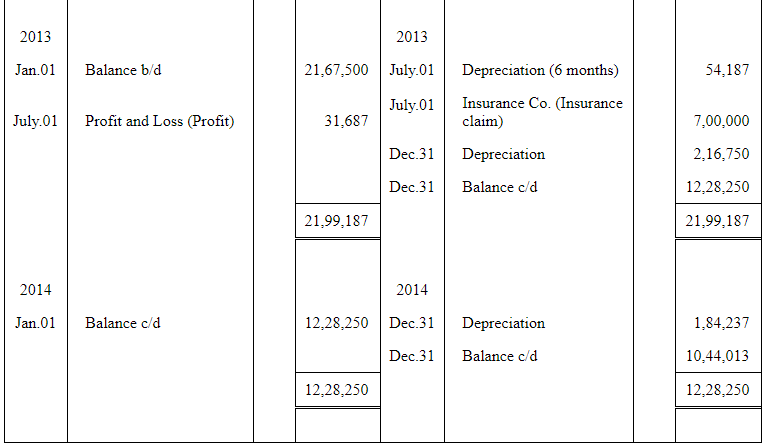

Question 15: On January 01, 2011, Satkar Transport Ltd, purchased 3 buses for Rs 10,00,000 each. On July 01, 2013, one bus was involved in an accident and was completely destroyed and Rs 7,00,000 were received from the Insurance Company in full settlement. Depreciation is writen off @15% p.a. on diminishing balance method. Prepare bus account from 2011 to 2014. Books are closed on December 31 every year.

Answer:

Explanation: Treat each bus as an individual asset and apply diminishing balance depreciation at 15% p.a. Steps:

• Charge depreciation on each bus from 01 Jan of the year until either year-end or date of accident. For the bus destroyed on 01 Jul 2013, charge depreciation for six months in 2013 (Jan-Jun) pro-rata.

• On accident date, remove the bus at its WDV (cost less accumulated depreciation) and record the insurance receipt of Rs 7,00,000. Any shortfall between WDV and insurance proceeds is recorded as a loss on disposal; any excess as profit.

• Continue depreciation on the remaining buses for subsequent years. The supplied account images show year-by-year postings and the final balances.

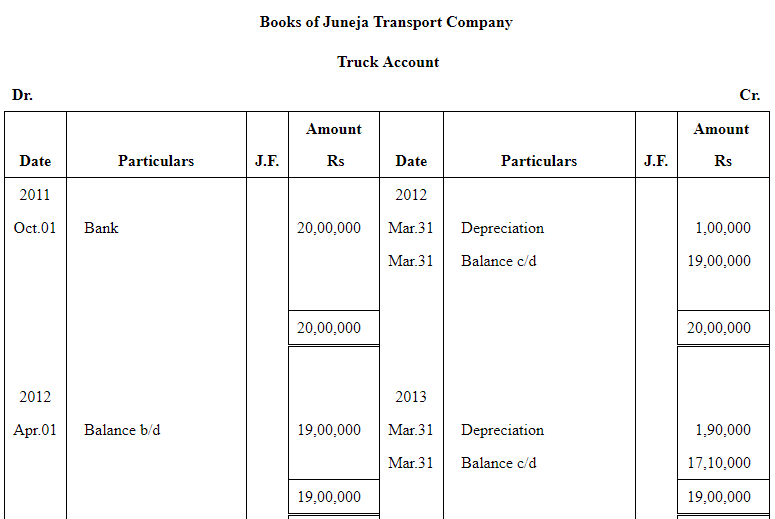

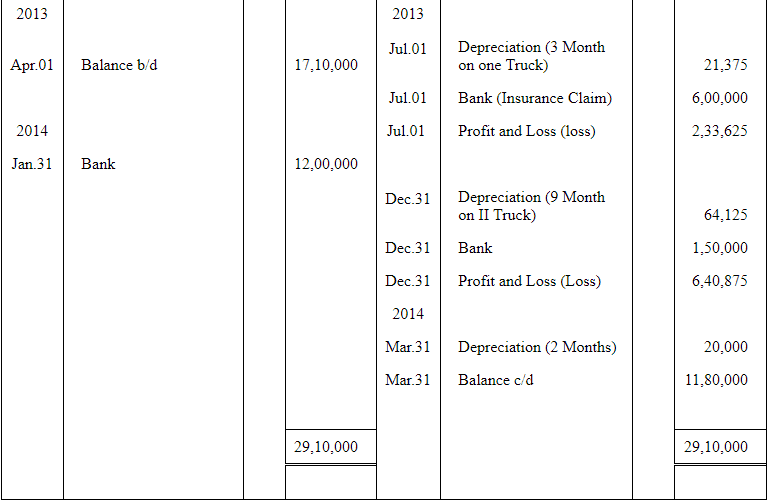

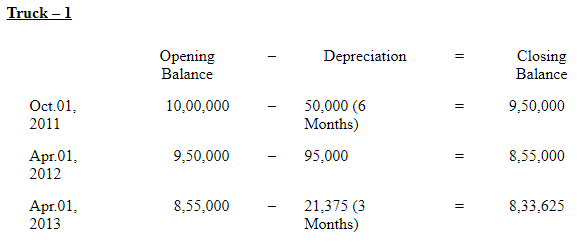

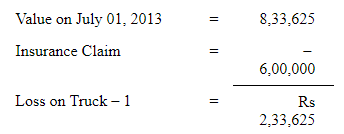

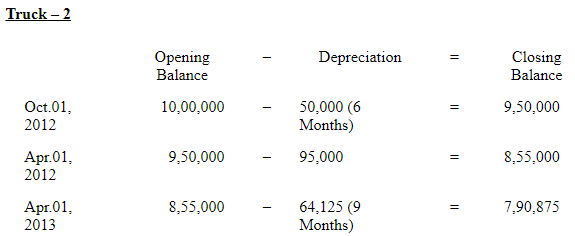

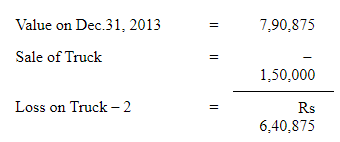

Question 16: On October 01, 2011 Juneja Transport Company purchased 2 Trucks for Rs 10,00,000 each. On July 01, 2013, One Truck was involved in an accident and was completely destroyed and Rs 6,00,000 were received from the insurance company in full settlement. On December 31, 2013 another truck was involved in an accident and destroyed partially, which was not insured. It was sold off for Rs 1,50,000. On January 31, 2014 company purchased a fresh truck for Rs 12,00,000. Depreciation is to be provided at 10% p.a. on the written down value every year. The books are closed every year on March 31. Give the truck account from 2011 to 2014.

Answer:

Note: As per solution, loss on truck one is as Rs 2,33,625; however, as per NCERT book, loss is of Rs 3,26,250.

Explanation: Depreciation at 10% on WDV must be prorated to the accounting year ending 31 Mar. Key considerations:

• For trucks bought on 01 Oct 2011, first accounting year (2011-12) covers 6 months (Oct-Mar). Thereafter charge full-year depreciation to 31 Mar of each year until disposal.

• When the first truck is destroyed on 01 Jul 2013, charge depreciation for the period 01 Apr 2013-30 Jun 2013 (3 months) in that accounting year before writing off the truck and recording the insurance receipt. Any difference between WDV on date of destruction and insurance proceeds is loss or gain on disposal.

• For the truck destroyed on 31 Dec 2013, charge depreciation up to that date (pro-rata) and then treat sale proceeds of Rs 1,50,000 as disposal value. The fresh truck purchased on 31 Jan 2014 is added to the ledger from that date; depreciation for 2013-14 is charged only for the months held in that year.

• The discrepancy noted likely arises from different pro-rata calculations or rounding; recheck prorations (months used) and rounding conventions to reconcile the two figures.

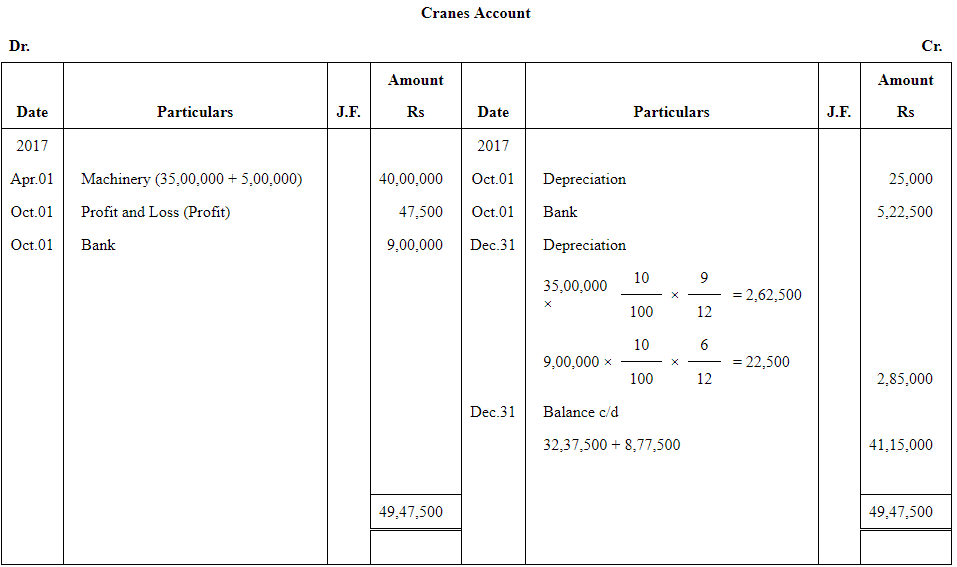

Question 17: A Noida based Construction Company owns 5 cranes and the value of this asset in its books on April 01, 2017 is Rs 40,00,000. On October 01, 2017 it sold one of its cranes whose value was Rs 5,00,000 on April 01, 2017 at a 10% profit. On the same day it purchased 2 cranes for Rs 4,50,000 each. Prepare cranes account. It closes the books on December 31 and provides for depreciation on 10% written down value.

Answer:

Explanation: Work as follows:

• Compute depreciation on the opening book values from 01 Apr 2017 to 30 Sep 2017 (6 months) for the crane sold, and for the remaining cranes over the whole year as appropriate.

• The crane sold had opening value Rs 5,00,000 on 01 Apr 2017. It was sold at 10% profit, so sale proceeds = 5,00,000 × 110% = Rs 5,50,000. Compare sale proceeds with the WDV at sale date (after charging pro-rata depreciation) to record profit or loss on disposal.

• Immediately on 01 Oct 2017 two new cranes of Rs 4,50,000 each are added; charge depreciation on them for the period they are held in 2017 (Oct-Dec = 3 months).

• The image shows the ledger postings, balancing and closing entries for 2017 as required.

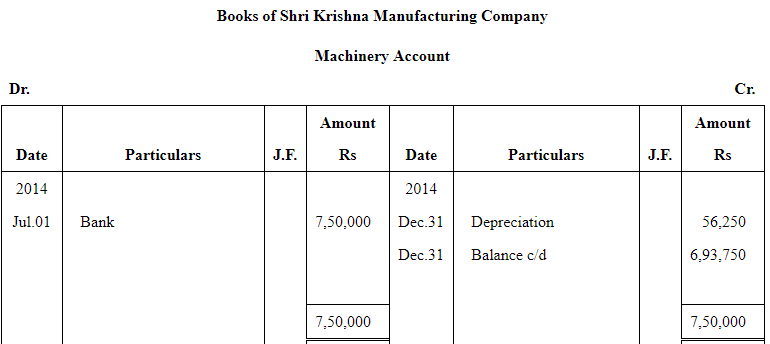

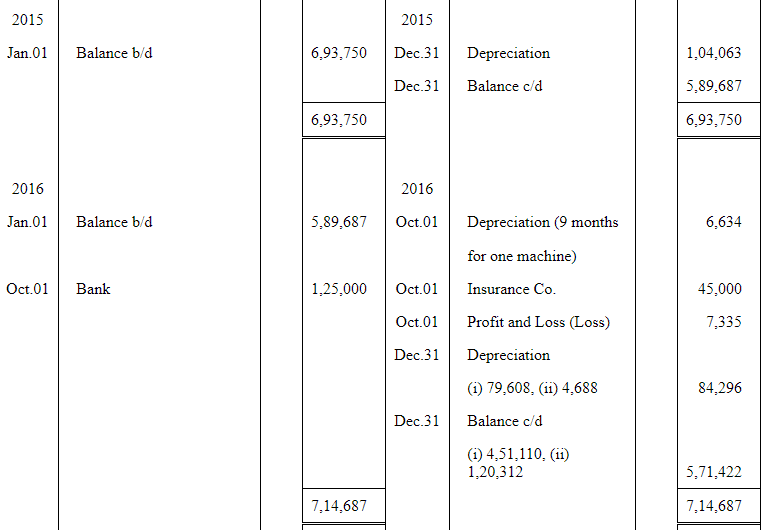

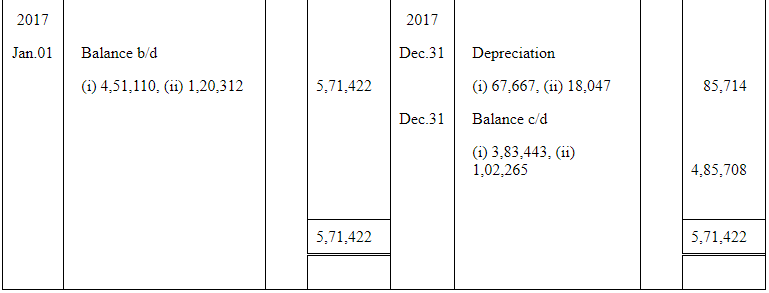

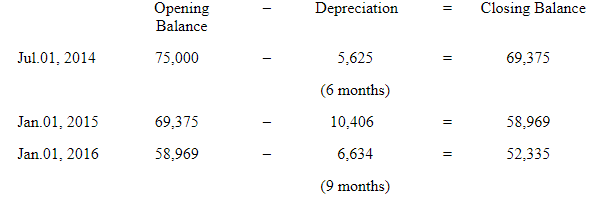

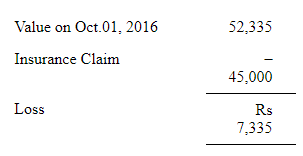

Question 18: Shri Krishan Manufacturing Company purchased 10 machines for Rs 75,000 each on July 01, 2014. On October 01, 2016, one of the machines got destroyed by fire and an insurance claim of Rs 45,000 was admitted by the company. On the same date another machine is purchased by the company for Rs 1,25,000.

The company writes off 15% p.a. depreciation on written down value basis. The company maintains the calendar year as its financial year. Prepare the machinery account from 2014 to 2017.

Answer:

Working Note:

Machine Costing Rs 75,000 sold on Oct.01, 2002

Explanation: Use the written down value method at 15% p.a. and calendar year periods:

• First year (2014) depreciation is charged for six months (01 Jul-31 Dec) on each of the ten machines bought on 01 Jul 2014.

• For 2015 and part of 2016 charge full years as long as machines remain. For the machine destroyed on 01 Oct 2016, charge depreciation up to 30 Sep 2016 (9 months in 2016) before removing it and noting the insurance claim of Rs 45,000. Any difference between WDV and claim is loss or gain on disposal.

• Immediately record the purchase of the replacement machine for Rs 1,25,000 on 01 Oct 2016 and charge depreciation for Oct-Dec 2016 (3 months) on that machine.

• The images show the year-wise ledger entries and working notes for depreciation and disposals.

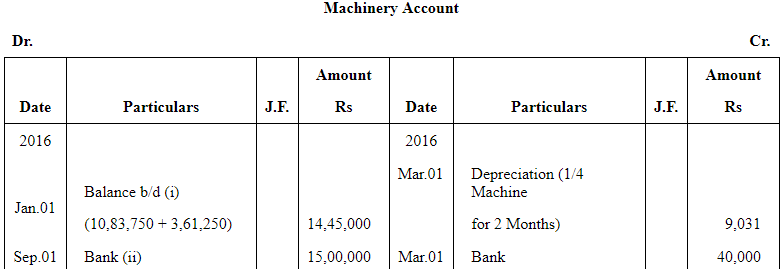

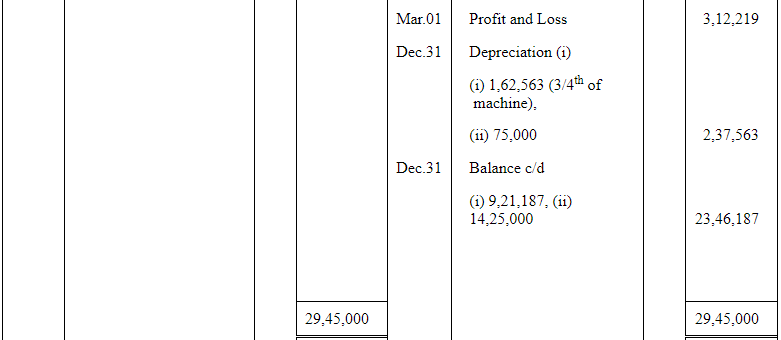

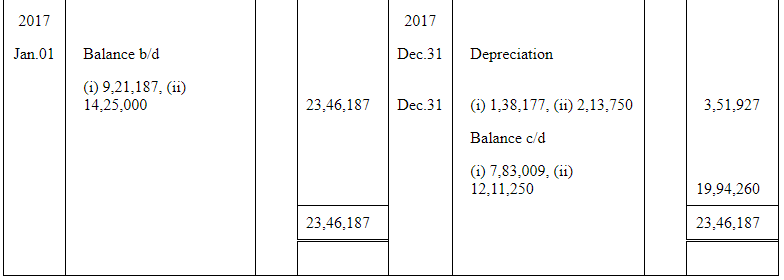

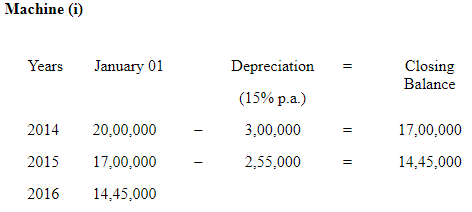

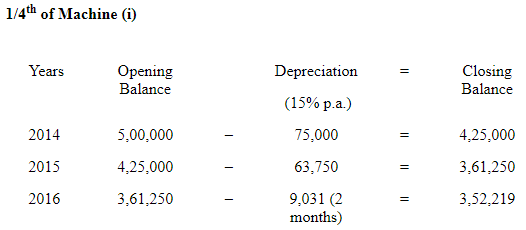

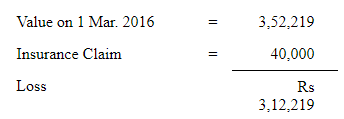

Question 19: On January 01, 2014, a Limited Company purchased machinery for Rs 20,00,000. Depreciation is provided @15% p.a. on diminishing balance method. On March 01, 2016, one fourth of machinery was damaged by fire and Rs 40,000 were received from the insurance company in full settlement. On September 01, 2016 another machinery was purchased by the company for Rs 15,00,000.

Write up the machinery account from 2016 to 2017. Books are closed on December 31, every year.

Answer:

Working Note:

Explanation: Steps to prepare the machinery ledger for 2016-17 under 15% WDV:

• Compute WDV at 01 Jan 2016 after charging depreciation for 2014 and 2015.

• On 01 Mar 2016 one fourth of the machinery is lost by fire. Determine the WDV attributable to that one fourth immediately before the fire (that is: opening WDV × 1/4). Charge depreciation up to 29 Feb 2016 on the whole asset before removing the damaged portion from the books.

• Record the insurance receipt of Rs 40,000 and compute loss/gain: Loss = WDV of one fourth - insurance receipt (if positive) or Profit = insurance - WDV (if negative).

• On 01 Sep 2016 record the fresh purchase of machinery for Rs 15,00,000 and charge depreciation for the period held in 2016 (Sep-Dec = 4 months) and for the full year 2017.

• The attached images contain the stepwise ledger postings and working notes showing the calculations used.

Page No 287:

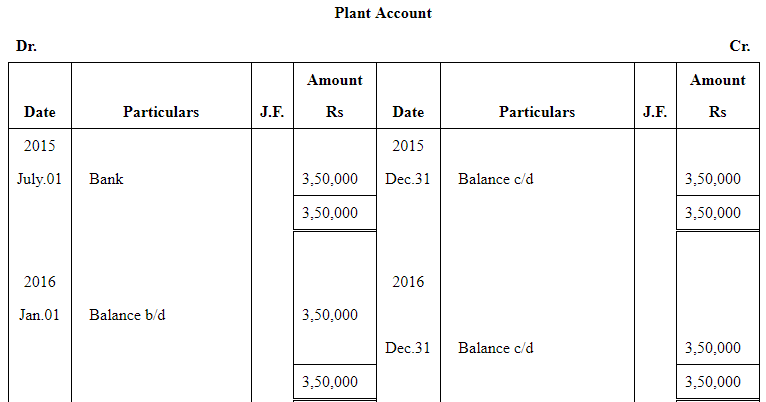

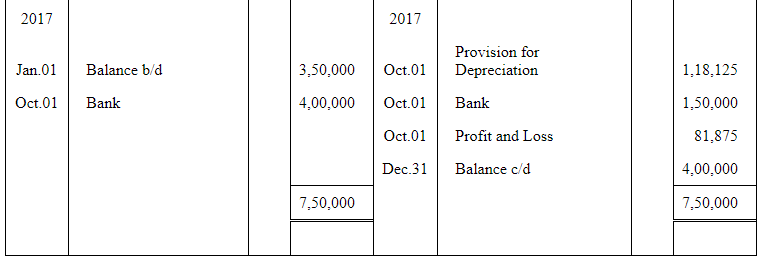

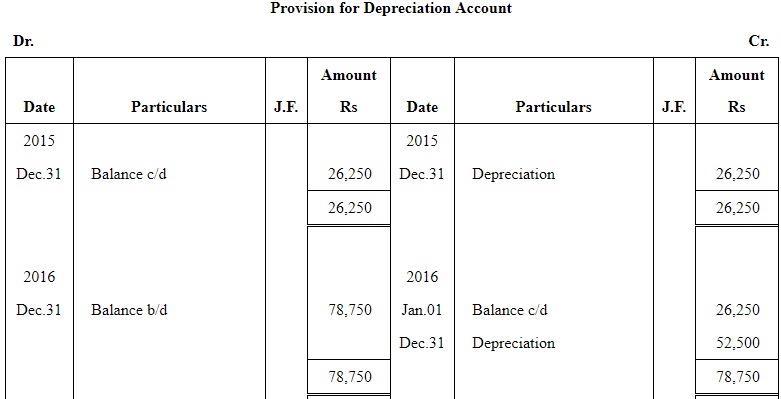

Question 20: A Plant was purchased on 1st July, 2015 at a cost of Rs 3,00,000 and Rs 50,000 were spent on its installation. The depreciation is written off at 15% p.a. on the straight line method. The plant was sold for Rs 1,50,000 on October 01, 2017 and on the same date a new Plant was installed at the cost of Rs 4,00,000 including purchasing value. The accounts are closed on December 31 every year.

Show the machinery account and provision for depreciation account for 3 years

Answer:

Explanation: Using straight line method at 15% p.a.:

• Capitalise cost and installation: total cost = Rs 3,50,000 (3,00,000 + 50,000). Charge depreciation at 15% on this cost, prorated in the first year (2015) from 01 Jul to 31 Dec = 6 months.

• Continue to charge full-year depreciation for 2016. For 2017, charge depreciation up to the date of sale (01 Oct 2017) if plant is disposed on that date; then remove it from books and record sale proceeds of Rs 1,50,000. Compute any profit or loss by comparing carrying amount at the date of sale with sale proceeds.

• On 01 Oct 2017, capitalise the new plant at Rs 4,00,000 and charge depreciation from that date to 31 Dec 2017 (3 months).

• The provision for depreciation account should accumulate depreciation charged each year and be adjusted on disposal (reduce provision by depreciation on the disposed asset up to the disposal date). The images present the full machinery and provision for depreciation ledgers with numerical workings.

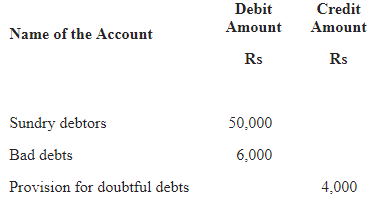

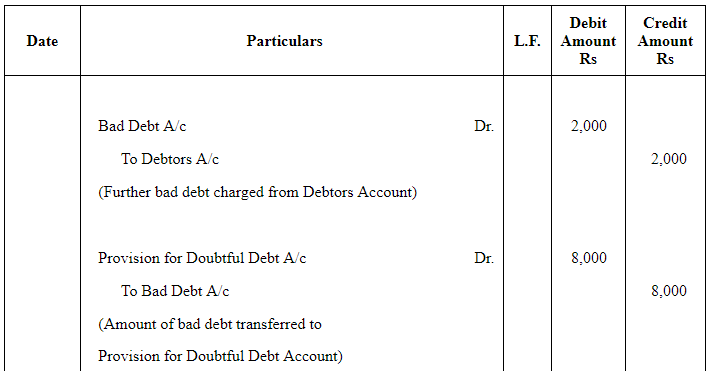

Question 21: An extract of Trial balance from the books of Tahiliani and Sons Enterprises on Marc 31 2017 is given below:

Additional Information:

- Bad Debts proved bad; however, not recorded amounted to Rs 2,000.

- Provision is to be maintained at 8% of debtors

Give necessary accounting entries for writing off the bad debts and creating the provision for doubtful debts account. Also, show the necessary accounts.

Answer:

Explanation: The provided images contain the numeric trial balance and the worked ledger accounts. The general procedure to pass entries and prepare accounts is as follows:

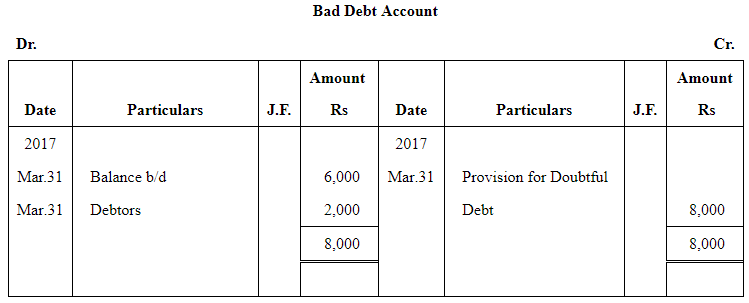

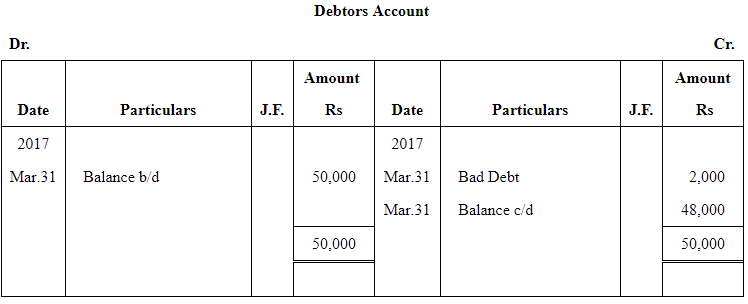

• To write off bad debts of Rs 2,000:

Journal entry:

Bad Debts A/c Dr. Rs 2,000

To Debtors A/c Rs 2,000

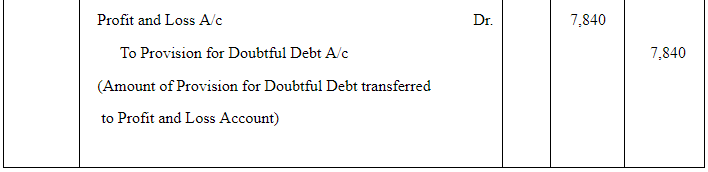

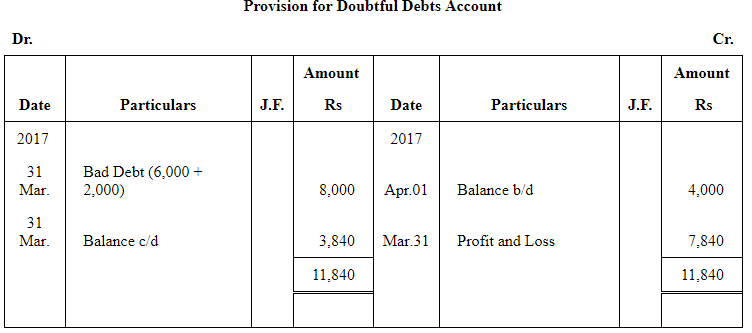

• To create or adjust Provision for Doubtful Debts to 8% of debtors:

(i) Compute debtors' balance after writing off the bad debts (use the trial balance figure less Rs 2,000).

(ii) Calculate 8% of this adjusted debtors' balance - this is the required provision.

(iii) If a provision already exists, the difference is charged or credited to Profit & Loss A/c.

Journal entry (if provision needs additional creation):

Profit & Loss A/c Dr. (difference)

To Provision for Doubtful Debts A/c (difference)

• Prepare ledger accounts: post the above journal entries to Bad Debts A/c, Debtors A/c, Provision for Doubtful Debts A/c and Profit & Loss A/c. The images [IMG_32] to [IMG_36] show these postings and the balances as required.

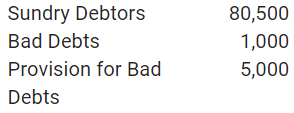

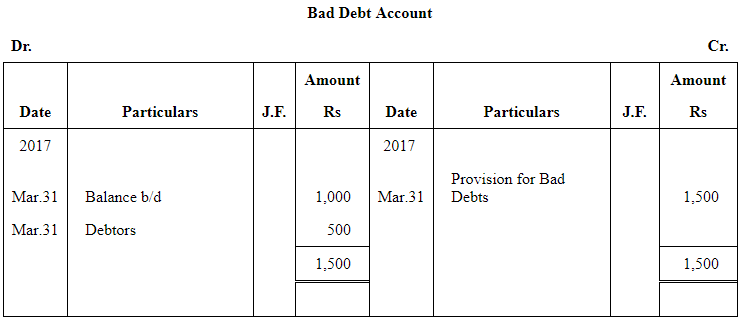

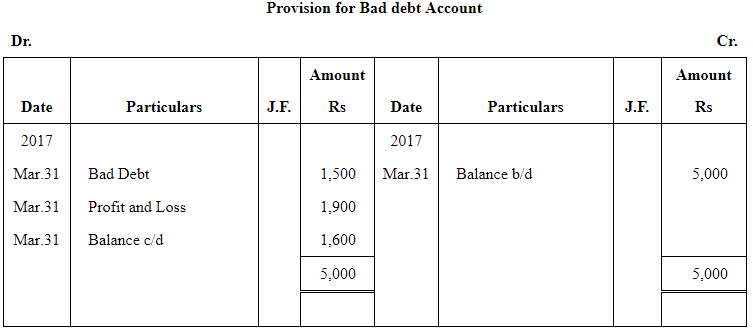

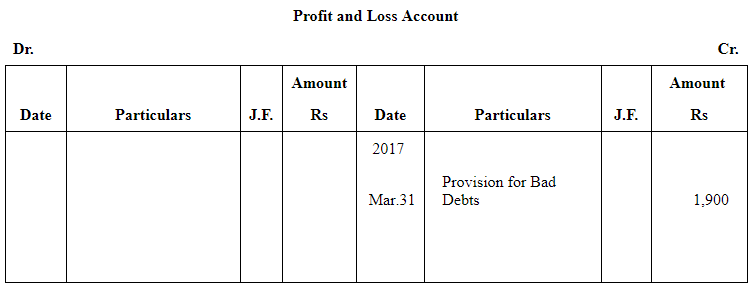

Question 22: The following information is extracted from the Trial Balance of M/s Nisha Traders on 31 March 2017.

Bad Debts Rs 500

Provision is to be maintained at 2% of Debtors

Prepare bad debts account, Provision for bad debts account and profit and loss account.

Answer:

Explanation: The images show the trial balance extract and the worked ledger accounts. The correct sequence to prepare the accounts is:

• Record the bad debts of Rs 500:

Journal entry:

Bad Debts A/c Dr. Rs 500

To Debtors A/c Rs 500

• Compute the required provision at 2% on the debtors' balance after writing off the bad debts.

• Adjust the existing provision (if any) to reach the required 2% and post the difference to Profit & Loss A/c:

Journal entry (to create provision):

Profit & Loss A/c Dr. (amount)

To Provision for Bad Debts A/c (amount)

• Post these entries to the respective ledger accounts and show the resulting Profit & Loss effect. The images [IMG_38]-[IMG_40] contain the prepared Bad Debts A/c, Provision for Bad Debts A/c and Profit & Loss extracts with the numerical workings and final balances.

FAQs on NCERT Solution (Part - 3) - Depreciation, Provisions and Reserves

| 1. What is depreciation? |  |

| 2. How is depreciation calculated? | |

| 3. What are provisions and reserves? | |

| 4. What is the difference between provisions and reserves? | |

| 5. Why are depreciation, provisions, and reserves important in financial accounting? | |