NCERT Solution (Part - 3) - Financial Statements-I

NCERT Solution - Chapter 1 : Financial Statements - I (Part - 3), Class 11, commerce

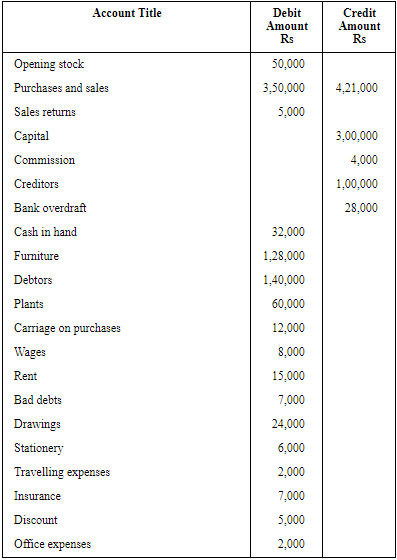

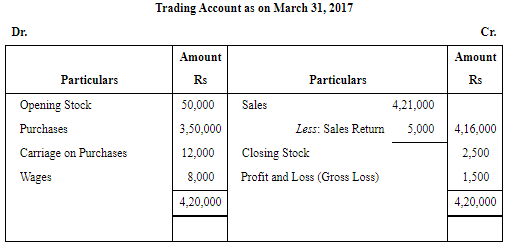

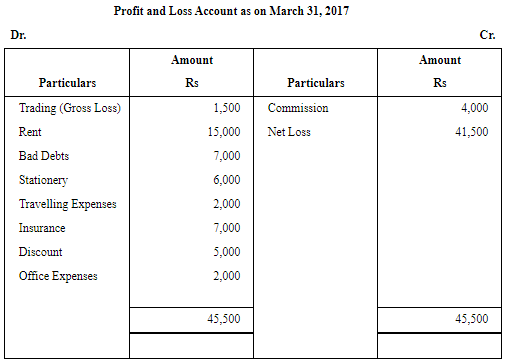

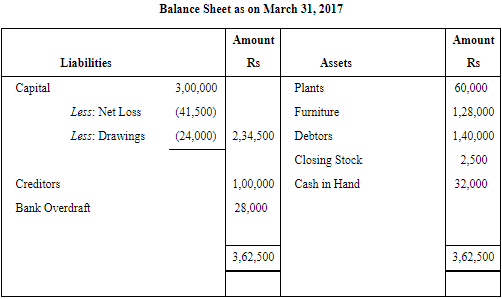

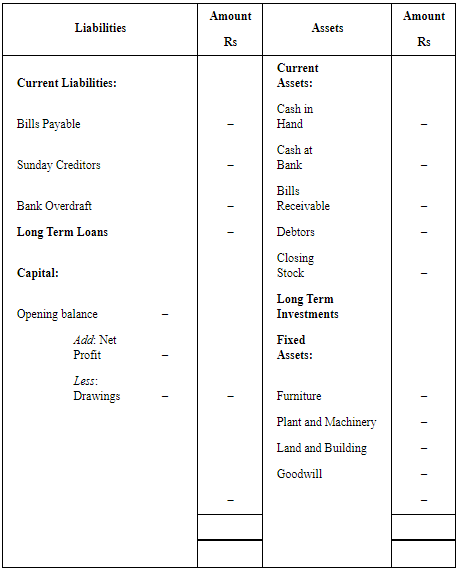

Question.15 : Prepare trading and profit and loss account of M/s Sports Equipments for the year ended March 31, 2017 and balance sheet as on that date:

Closing stock as on March 31, 2017 Rs 2,500

Ans:

Explanation: The Trading Account, Profit and Loss Account and Balance Sheet are presented above in the given image blocks. The closing stock of Rs 2,500 has been included in the Trading Account as at 31 March 2017 and is shown as a current asset in the Balance Sheet. All direct expenses and incomes have been adjusted in the Trading Account to arrive at gross profit, while indirect items have been posted to the Profit and Loss Account to determine net profit. The Balance Sheet summarises the assets and liabilities as at the date stated.

Short answers : Solutions of Questions on Page Number : 376

Question.1 : What are the objectives of preparing financial statements?

Ans: The main objectives of preparing financial statements are as follows.

1. To ascertain the profit earned or loss incurred by a business during an accounting period. This is shown by the Trading and Profit and Loss Account.

2. To determine the financial position of the business at a particular date; this is shown by the Balance Sheet.

3. To enable comparison of performance over time (intra-firm) and with other firms in the same industry (inter-firm).

4. To assess the solvency and credit worthiness of the business for lending and investment decisions.

5. To ensure adequate provision of reserves and provisions to meet unforeseen future requirements and to strengthen the financial position.

6. To provide reliable information to various users (owners, management, investors, creditors, tax authorities, etc.) to support decision making.

Question.2 : What is the purpose of preparing trading and profit and loss account?

Ans: The purposes are as follows.

The purposes of preparing Trading Account are:

1. To calculate gross profit earned or gross loss incurred during an accounting period.

2. To determine the cost of goods sold by adjusting purchases, opening and closing stocks and direct expenses.

3. To record and control direct expenses incurred on purchases and production of goods.

4. To assess the reasonableness and adequacy of direct expenses by comparing them with purchases or production output.

5. To compare actual trading performance with planned or past performance and take corrective action.

The purposes of preparing Profit and Loss Account are:

1. To calculate net profit or net loss after charging indirect expenses and adding indirect incomes.

2. To help compute ratios such as net profit ratio and to compare current performance with targets or past years.

3. To evaluate the adequacy and reasonableness of indirect expenses by relating them to sales or profit.

4. To provide information for planning and control by comparing actual results with budgets or standards.

5. To determine amounts available for transfer to reserves and for distribution to owners.

Question.3 : Explain the concept of cost of goods sold?

Ans: Cost of Goods Sold (COGS) is the total cost directly attributable to the goods sold during an accounting period. It includes opening stock, purchases and direct expenses, and excludes closing stock because closing stock represents unsold goods at the period end. The formula is:

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses - Closing Stock

Thus, closing stock is subtracted since it is not consumed in the period and will be carried forward to the next period.

Question.4 : What is a balance sheet? What are its characteristics?

Ans: A Balance Sheet is a financial statement prepared to show the book value of a business's assets and liabilities at a particular date. It presents the financial position of the enterprise and shows how the business resources are financed.

Characteristics of a Balance Sheet

1. It is a statement of assets and liabilities as at a specific date.

2. The total of the Assets side must equal the total of the Liabilities side (balance must exist).

3. It is prepared for a particular date, not for a period.

4. It helps in ascertaining the financial position, solvency and capital structure of the business.

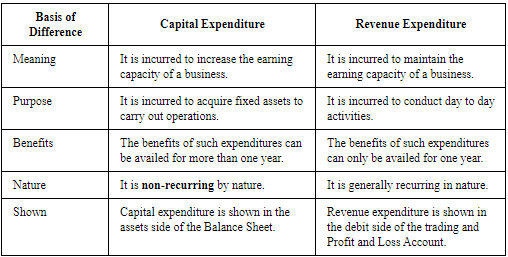

Question.5 : Distinguish between capital and revenue expenditure and state whether the following statements are items of capital or revenue expenditure:

(a) Expenditure incurred on repairs and whitewashing at the time of purchase of an old building in order to make it usable.

(b) Expenditure incurred to provide one more exit in a cinema hall in compliance with a government order.

(c) Registration fees paid at the time of purchase of a building

(d) Expenditure incurred in the maintenance of a tea garden which will produce tea after four years.

(e) Depreciation charged on a plant.

(f) The expenditure incurred in erecting a platform on which a machine will be fixed.

(g) Advertising expenditure, the benefits of which will last for four years.

Ans:

Capital expenditure is spending that acquires or improves a fixed asset or gives benefit for more than one accounting period. Revenue expenditure is for day-to-day running and benefits only the current period.

(a) Capital expenditure

(b) Revenue expenditure (required to meet statutory compliance; unless it increases asset value permanently)

(c) Capital expenditure (registration fees relate to acquisition of the asset)

(d) Capital expenditure (preparatory cost for future benefit over several years)

(e) Revenue expenditure (depreciation is an allocation of asset cost to periods)

(f) Capital expenditure (necessary to make the machine usable - part of cost of the asset)

(g) Deferred revenue expenditure (a revenue nature expense but benefits extend over several years and is written off over the benefit period)

Question.6 : What is an operating profit?

Ans: Operating profit is the profit earned from the normal, day-to-day activities of a business. It is the amount remaining after subtracting operating expenses from gross profit. It excludes non-operating incomes and expenses such as interest, dividends or extraordinary items. It is also referred to as earnings before interest and tax (EBIT).

It can be expressed as:

Operating Profit = Gross Profit - Operating Expenses

Or,

Operating Profit = Sales - Operating Cost = Sales - COGS - Operating Expenses

Operating expenses include items such as administrative expenses, selling and distribution expenses, discounts allowed and bad debts.

Long answers : Solutions of Questions on Page Number : 376

Question.1 : What are financial statements? What information do they provide?

Ans: Financial statements are formal records that present the financial activities and position of a business at the end of an accounting period. They provide a summary of the results of operations and the resources owned and owed by the enterprise. The main financial statements are:

1. Income statements (Trading and Profit and Loss Account): These show direct and indirect expenses and incomes. The Trading Account discloses gross profit or gross loss, while the Profit and Loss Account shows net profit or net loss after charging indirect expenses and adding indirect incomes.

2. Statement of financial position (Balance Sheet): This lists the book values of assets and liabilities and shows the financial position, solvency and credit worthiness of the business.

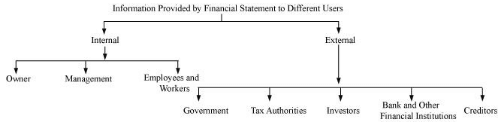

The information provided by financial statements includes the magnitude of gross and net profit or loss, and the book value of assets and liabilities. Different users derive different benefits from this information. Major users include:

1. Internal users: Owners, management, employees and workers.

a. Owners: Need information about profits to assess returns on investment.

b. Management: Uses statements for planning, control and decision making, for example by analysing expense ratios and profitability.

c. Employees and workers: Look at net profit to assess prospects for bonuses and job security.

2. External users: Government, tax authorities, investors, banks, creditors and others.

a. Government: Uses aggregate business data for economic planning and to estimate macroeconomic indicators.

b. Tax authorities: Rely on financial statements to assess taxable income and determine tax liabilities.

c. Investors: Use financial statements to evaluate earning capacity, growth potential and investment worthiness.

d. Banks and financial institutions: Assess creditworthiness, solvency and repayment capacity before lending.

e. Creditors: Examine liquidity and solvency to judge the likelihood of timely payment.

Question.2 : What are closing entries? Give four examples of closing entries.

Ans: Closing entries are journal entries made at the end of an accounting period to transfer the balances of nominal accounts (revenues, expenses, gains and losses) to the Trading Account or Profit and Loss Account so that the nominal accounts may start the next period with zero balances. Examples of closing entries are given below.

1. To transfer debit balances related to direct items to the Trading Account:

Trading A/c

To Opening Stock A/c

To Purchases A/c

To Wages A/c

To Carriage A/c

To All Other Direct Expenses A/c

(Being debit balances of direct expenses transferred to Trading Account)

2. To transfer credit balances to the Trading Account:

Sales A/c

Closing Stock A/c

To Trading A/c

(Being credit balances transferred to Trading Account)

3. To transfer debit balances of indirect expenses to the Profit and Loss Account:

Profit and Loss A/c

To Salaries A/c

To Rent A/c

To Bad Debts A/c

To All Other Indirect Expenses A/c

(Being indirect expense balances transferred to Profit and Loss Account)

4. To transfer credit balances of indirect incomes to the Profit and Loss Account:

Commission Received A/c

Interest Received A/c

All Other Indirect Income A/c

To Profit and Loss A/c

(Being indirect incomes transferred to Profit and Loss Account)

Question.3 : Discuss the need of preparing a balance sheet.

Ans: A Balance Sheet is needed for several practical reasons:

1. It shows the nature and book value of various assets (fixed assets, investments, current assets) at the end of the accounting period.

2. It discloses the nature and amount of different liabilities (long-term liabilities, current liabilities, provisions) owed by the business.

3. It provides information about the capital invested, additions to capital, drawings and the effect of profit or loss on owners' funds.

4. It helps in assessing the solvency and liquidity of the business by comparing assets and liabilities.

5. It discloses the true financial position of the business at a specific point in time, useful for owners and external parties.

6. It serves as a basis for preparing budgets, future plans and maintaining books for the next accounting period.

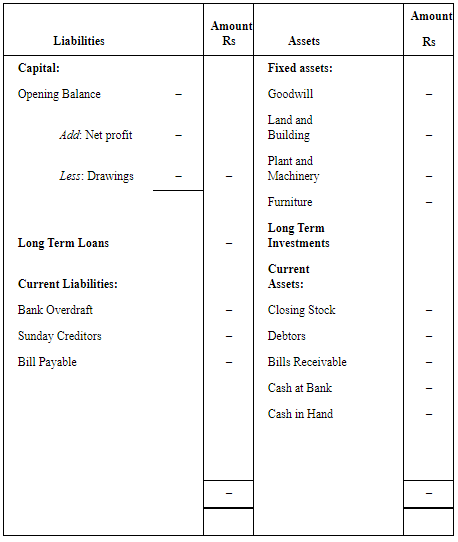

Question.4 : What is meant by Grouping and Marshalling of assets and liabilities? Explain the ways in which a balance sheet may be marshalled.

Ans : The objective of financial statements is to present summarised financial information so that users can interpret it easily and make decisions.

Grouping of assets and liabilities: Grouping means showing similar items under a single heading. For example, all assets that will be used for more than one year are shown under fixed assets (building, furniture, machinery). Current assets are grouped separately.

Marshalling of assets and liabilities: Marshalling refers to the order in which assets and liabilities are presented in the Balance Sheet. Two common methods are:

1. In order of liquidity: Assets are arranged from most liquid (convertible into cash quickly) to least liquid. Cash in hand appears first and goodwill last. Liabilities are arranged from those to be paid first (current liabilities) to those payable later (long-term liabilities and capital).

Balance Sheet of.................., as on................

2. In order of permanence: This is the reverse. Assets with the highest permanence (such as goodwill, land and building) are shown first, while most liquid assets (cash and bank balances) are shown last. Liabilities are shown with the most permanent (for example capital) at the top and less permanent liabilities below.

Balance Sheet of.................., as on................

FAQs on NCERT Solution (Part - 3) - Financial Statements-I

| 1. What are financial statements? |  |

| 2. How are financial statements prepared? | |

| 3. How do financial statements help in decision-making? | |

| 4. What is the importance of analyzing financial statements? | |

| 5. What are the limitations of financial statements? | |