NCERT Solution: Financial Statements - II (Part- 2)

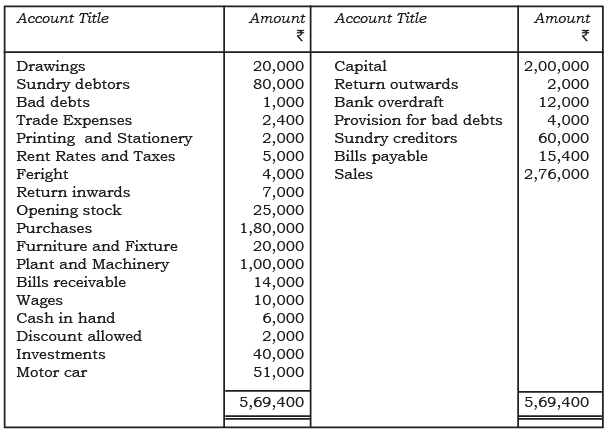

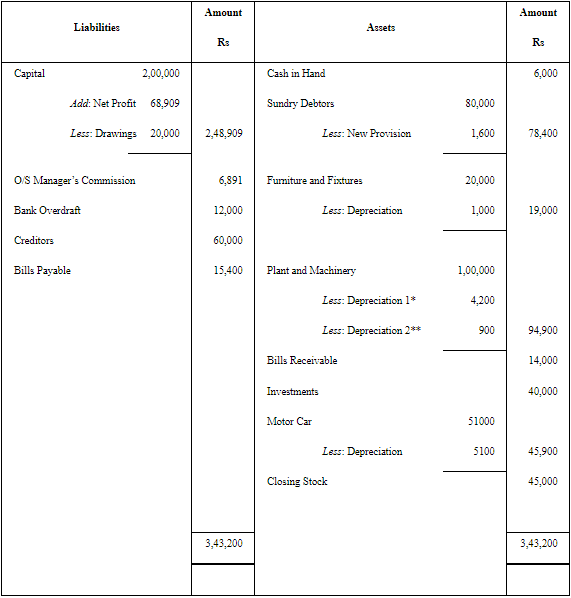

Q5: From the following information prepare trading and profit and loss account of M/s Indian sports house for the year ending December 31, 2017.

Adjustments

1. Closing stock was Rs 45,000.

2. Provision for doubtful debts is to be maintained @ 2% on debtors.

3. Depreciation charged on : furniture and fixture @ 5%, plant and Machinery @ 6% and motor car @ 10%.

4. A Machine of Rs 30,000 was purchased on July 01, 2016.

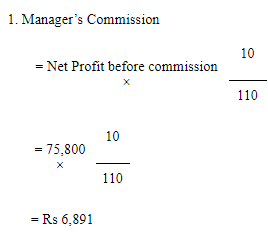

5. The manager is entitle to a commission of @ 10% of the net profit after charging such commission.

Answer :

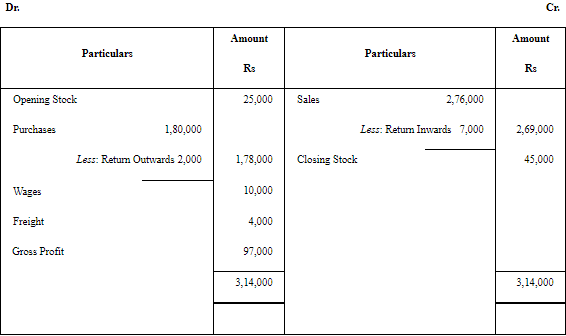

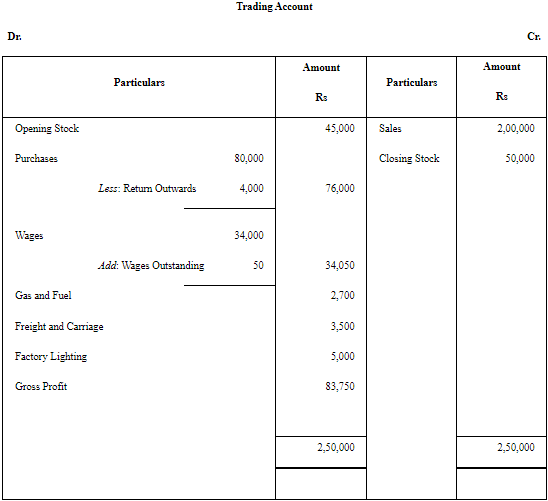

Trading Account

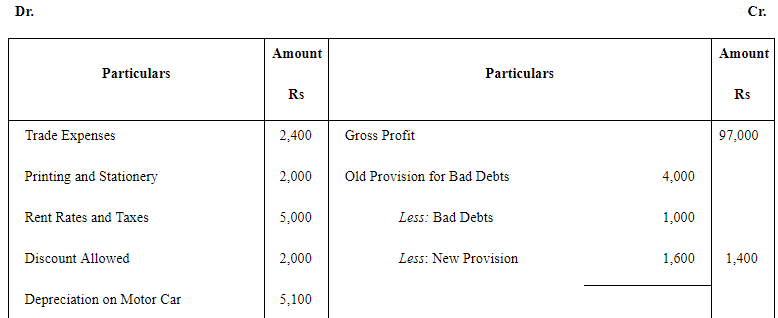

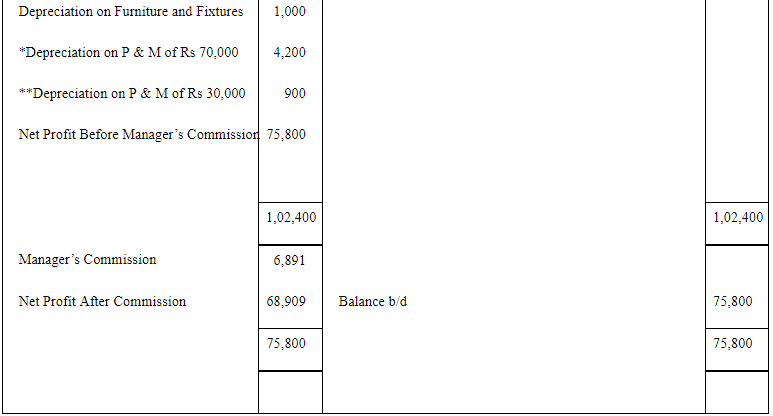

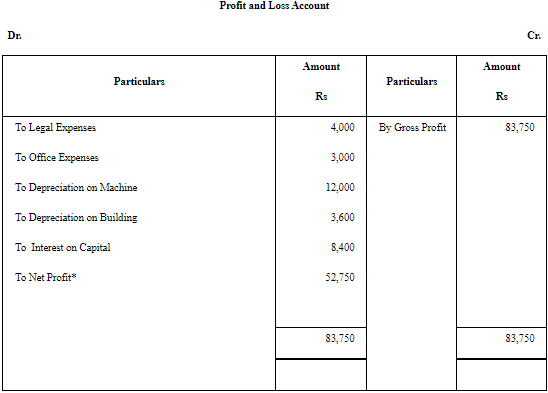

Profit and Loss Account

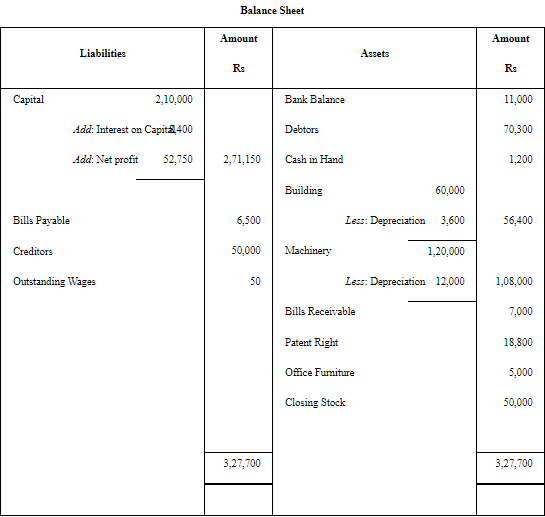

Balance Sheet

Working Notes

2. Out of the machinery of Rs 1,00,000, Rs 30,000 worth of machinery was purchased on 01/October/2016. Therefore, the depreciation on this machinery will be for 6 months at 6% p.a.

The rest of the machinery of Rs 70,000 will bear depreciation at 6% p.a.

Note: As per our solution Gross Profit is Rs 97,000, however, as per book it is Rs 1,01,000.

Working Notes / Explanation :

1. Closing Stock: Closing stock of Rs 45,000 is taken to the Trading Account on the credit side to arrive at gross profit.

2. Provision for Doubtful Debts: Provision is maintained at 2% on closing sundry debtors. First adjust any specific bad debts (if shown elsewhere), then calculate 2% on the balance of debtors and charge the difference (increase or decrease) to the Profit and Loss Account.

3. Depreciation: Charge depreciation at the given rates on the respective asset balances. If an asset was purchased part-way through a year, depreciate it for the period of ownership in that year. Confirm the exact purchase date from the books to compute pro rata depreciation for that asset.

4. Machine Purchased (date effect): If the machine of Rs 30,000 was bought on 01 July 2016, it will attract full-year depreciation for the year ended 31 Dec 2017. If it was bought on 01 October 2016, depreciation for 2016-17 would be for 3 months and for 2017 the full year; follow the actual date in books to decide the period for depreciation.

5. Manager's Commission (10% of net profit after charging such commission): Let P be profit before charging manager's commission. The manager's commission C satisfies C = 10% of (P - C). Hence C = (0.1/1.1) × P = P/11. Compute profit before commission, divide by 11 to get the commission, and then deduct it to arrive at net profit after commission.

These adjustments explain how figures in the Trading Account, Profit and Loss Account and Balance Sheet are arrived at and why small differences with book answers may occur if any dates or opening figures differ slightly.

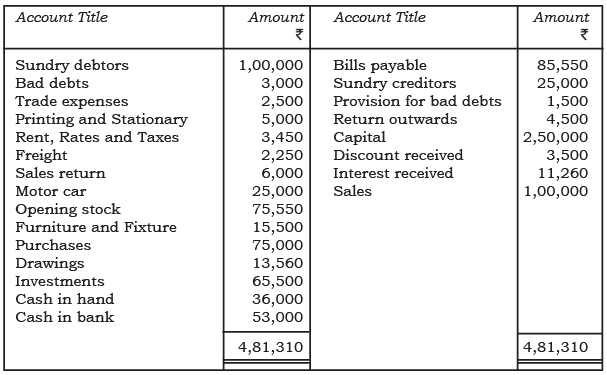

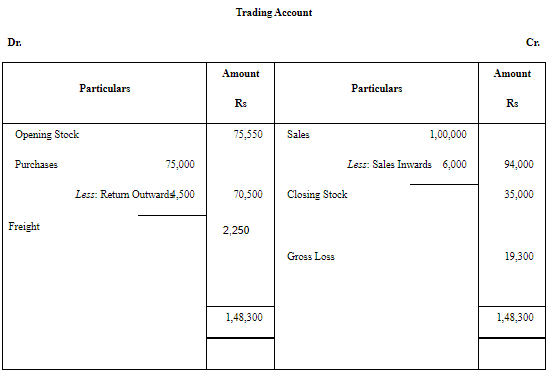

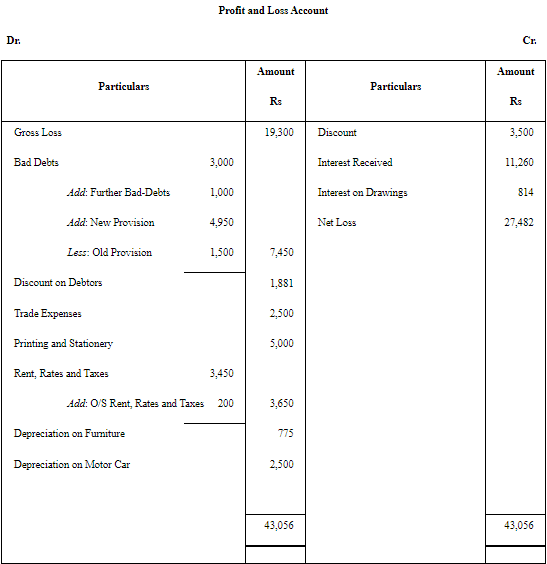

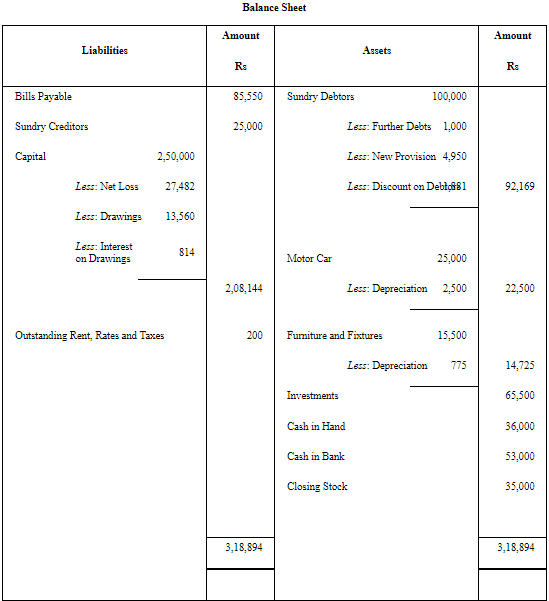

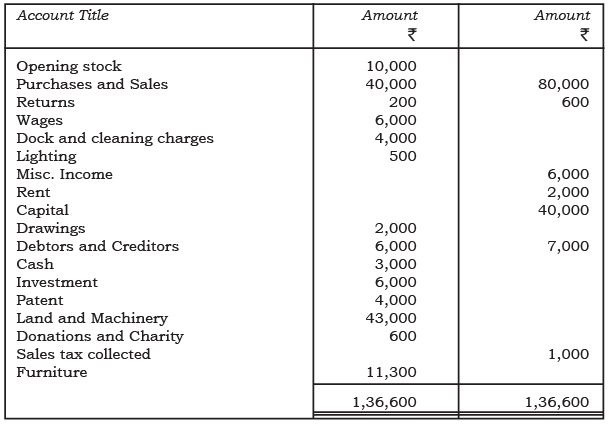

Q6: Prepare the trading and profit and loss account and a balance sheet of M/s Shine Ltd. from the following particulars.

Adjustments

1. Closing stock was valued Rs 35,000.

2. Depreciation charged on furniture and fixture @ 5%.

3. Further bad debts Rs 1,000. Make a provision for bad debts @ 5% on sundry debtors.

4. Depreciation charged on motor car @ 10%.

5. Interest on drawing @ 6%.

6. Rent, rates and taxes was outstanding Rs 200.

7. Discount on debtors 2%.

Ans:

Note: In NCERT book, the Gross Loss is Rs 17,050, the Net Loss is Rs 27,344 and the Total of Balance Sheet is Rs 3,19,032. However, as per the solution Net Loss and the Total of the Balance Sheet are Rs 27,482 and Rs 3,18,894 respectively.

Explanation / Working Notes :

1. Closing Stock: Closing stock Rs 35,000 is credited to Trading Account to compute gross loss/profit.

2. Depreciation: Charge 5% on furniture and fixture and 10% on motor car on their respective book values; treat depreciation as an expense in Profit and Loss Account and reduce the asset values in the Balance Sheet.

3. Bad Debts and Provision: First record further bad debts of Rs 1,000 as an expense. Then create a provision equal to 5% of sundry debtors after writing off bad debts. The increase (or decrease) in provision is shown in the Profit and Loss Account.

4. Interest on Drawings: Interest on drawings at 6% is shown as income in the Profit and Loss Account and added to capital (or partners' accounts) as applicable.

5. Outstanding and Discount: Outstanding rent of Rs 200 is added to expenses. Discount on debtors 2% is treated as a deduction from sundry debtors when preparing the Balance Sheet and recorded in Profit and Loss as loss/adjustment.

6. Reconcile Differences: Minor differences from NCERT answers can arise from rounding or interpretation of dates; ensure consistent treatment of provisions and rounding while preparing final figures.

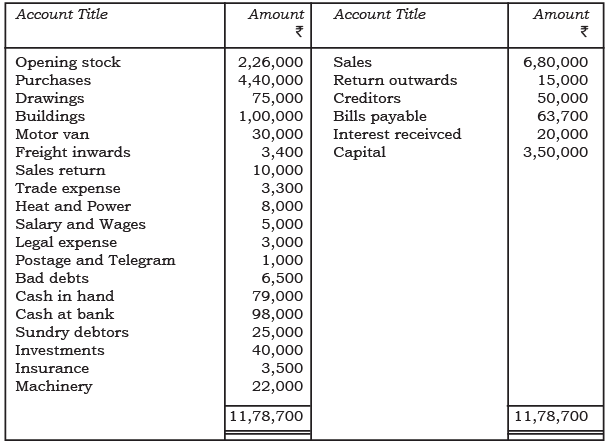

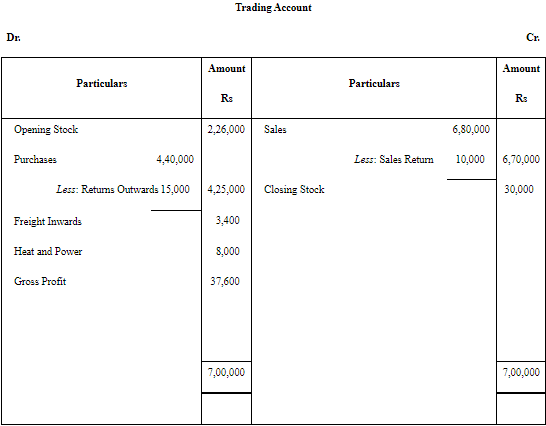

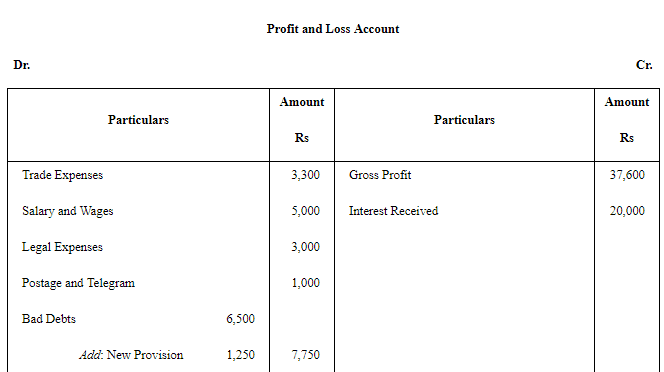

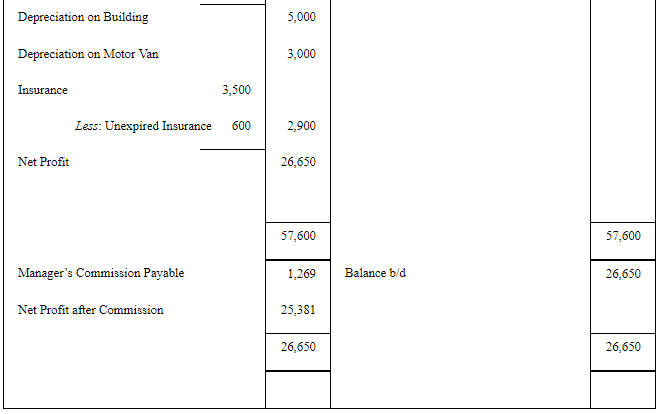

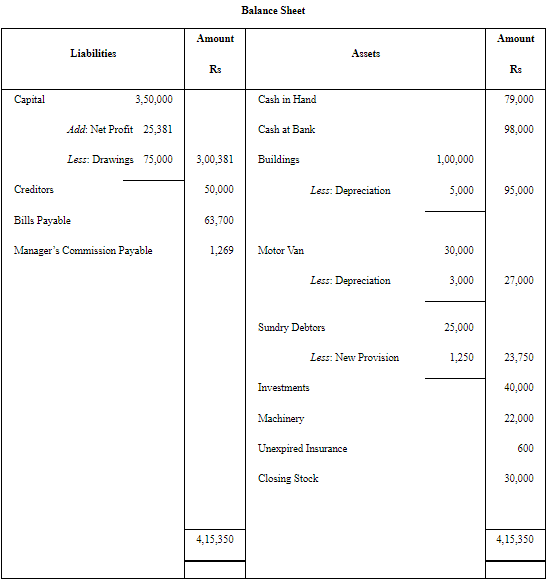

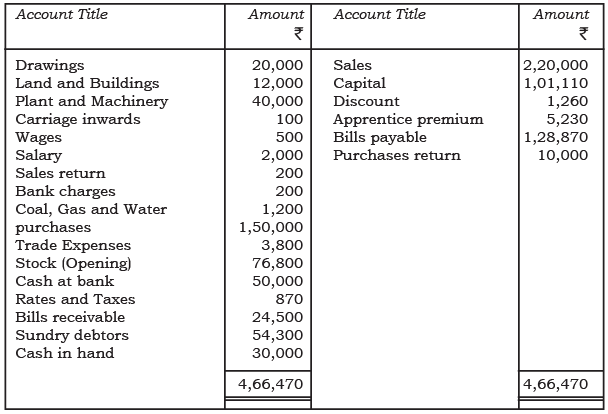

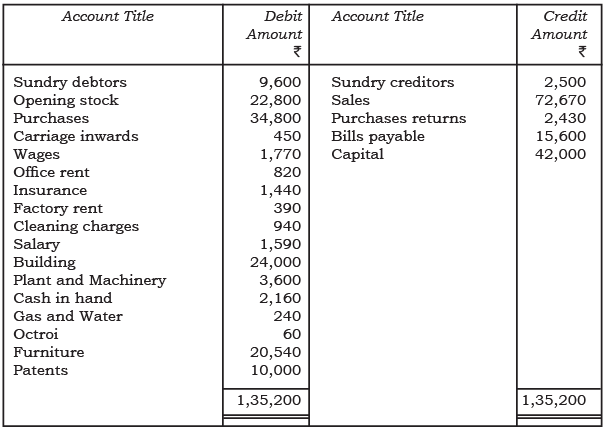

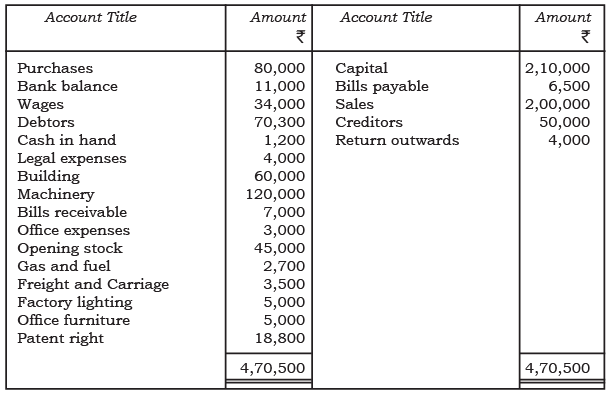

Q7: Following balances have been extracted from the trial balance of M/s Keshav Electronics Ltd. You are required to prepare the trading and profit and loss account and a balance sheet as on December 31, 2017.

The following additional information is available :

1. Stock on December 31, 2017 was Rs 30,000.

2. Depreciation is to be charged on building at 5% and motor van at 10%.

3. Provision for doubtful debts is to be maintained at 5% on Sundry Debtors.

4. Unexpired insurance was Rs 600.

5. The Manager is entitled to a commission @ 5% on net profit before charging such commission.

Ans:

Note: In NCERT, Q-7 adjustment (5) is a misprint. The answer represents the Net Profit after the Manager's Commission. However, in the adjustment, the Net Profit has been mentioned before the Manager's Commission.

Explanation / Working Notes :

1. Closing Stock: Include closing stock of Rs 30,000 in Trading Account to compute gross profit.

2. Depreciation: Charge depreciation at 5% on building and 10% on motor van; record depreciation in the Profit and Loss Account and reduce the respective asset values in the Balance Sheet.

3. Provision for Doubtful Debts: Create provision at 5% on sundry debtors after writing off any specific bad debts; show the change in provision in the Profit and Loss Account.

4. Unexpired Insurance: Unexpired insurance of Rs 600 is a current asset and should be shown under current assets in the Balance Sheet after adjusting insurance expense.

5. Manager's Commission: The adjustment wording in the question is ambiguous. If commission is 5% on net profit before charging commission, commission = 5% × (profit before commission). If it is on net profit after charging commission, a self-referential calculation is required. The note indicates a misprint in NCERT; follow the adjustment as stated in the question and the working shown in the official solution for consistency.

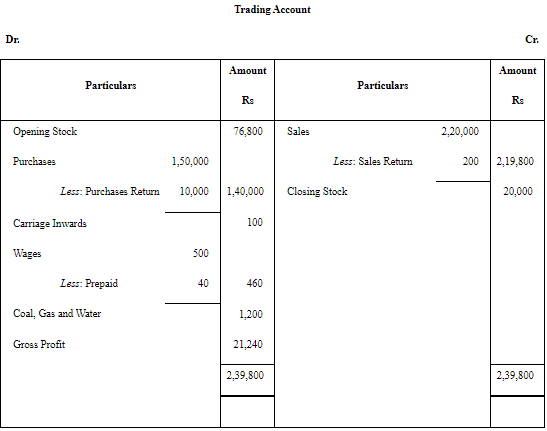

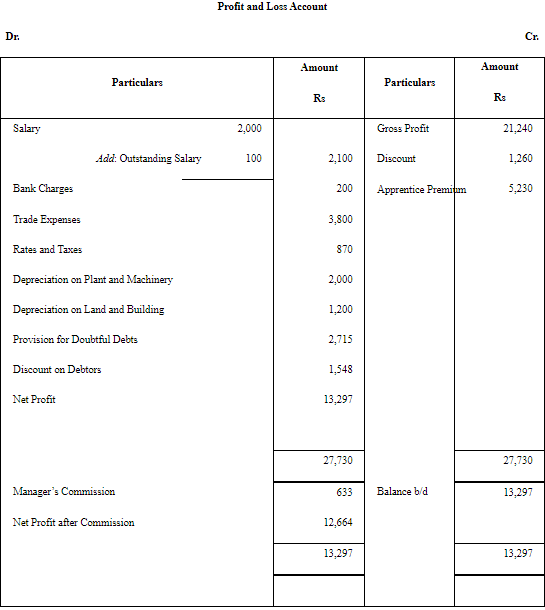

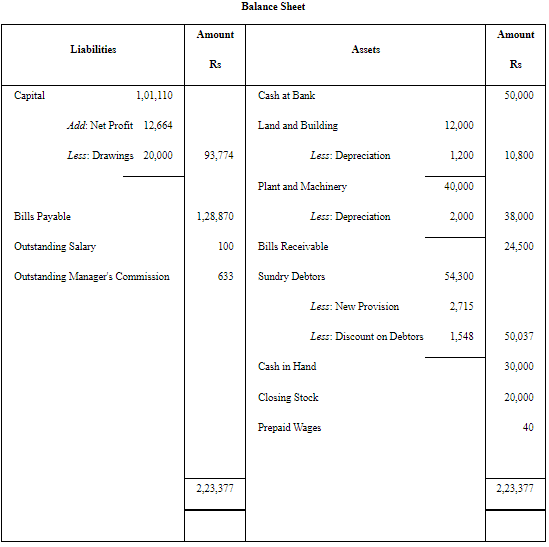

Q8: From the following balances extracted from the books of Raga Ltd. Prepare a trading and profit and loss account for the year ended December 31, 2017 and a balance sheet as on that date.

The additional information is as under:

1. Closing stock was valued at the end of the year Rs, 20,000.

2. Depreciation on plant and machinery charged at 5% and land and building at 10%.

3. Discount on debtors at 3%.

4. Make a provision at 5% on debtors for doubtful debts.

5. Salary outstanding was Rs 100 and Wages prepaid was Rs 40.

6. The manager is entitled a commission of 5% on net profit after charging such commission.

Ans:

Explanation / Working Notes :

1. Closing Stock: Close stock of Rs 20,000 is credited to Trading Account to compute gross profit.

2. Depreciation: Charge depreciation on plant and machinery at 5% and on land and building at 10%; show these as expenses in Profit and Loss and reduce asset values in the Balance Sheet.

3. Discount and Provision on Debtors: Discount on debtors at 3% reduces the debtor balance. Additionally create provision for doubtful debts at 5% on the adjusted debtors; record any change in provision in Profit and Loss Account.

4. Outstanding / Prepaid Items: Salary outstanding Rs 100 is an expense for the year and is shown in current liabilities; wages prepaid Rs 40 is an asset and shown under current assets.

5. Manager's Commission (5% on net profit after charging commission): Use the self-referential formula: if P is profit before commission, commission = (0.05/1.05) × P = P/21. Compute accordingly to arrive at net profit after commission.

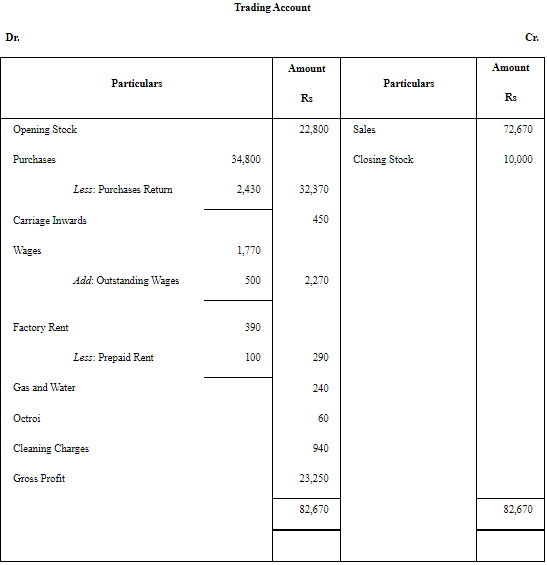

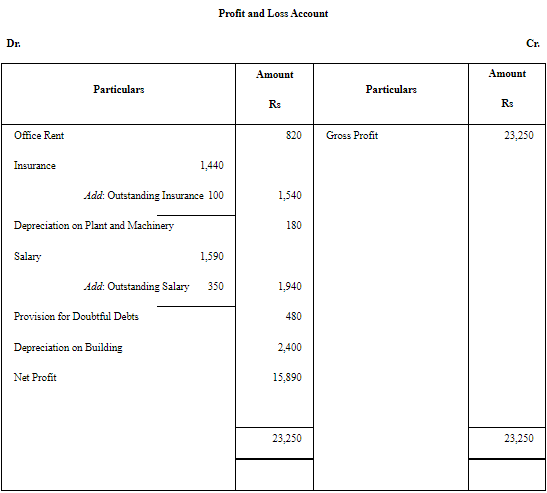

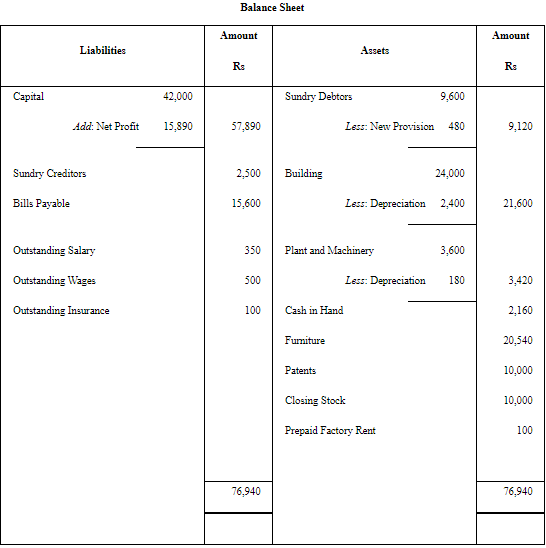

Q9: From the following balances of M/s Jyoti Exports, prepare trading and profit and loss account for the year ended March 31, 2017 and balance sheet as on this date.

Closing stock Rs 10,000.

1. To provision for doubtful debts is to be maintained at 5 per cent on sundry debtors.

2. Wages amounting to Rs 500 and salary amounting to Rs 350 are outstanding.

3. Factory rent prepaid Rs 100.

4. Depreciation charged on Plant and Machinery @ 5% and Building @ 10%.

5. Outstanding insurance Rs 100.

Ans:

Note: As per solution Net Profit is Rs 15,890 and Total of the Balance Sheet is Rs 76,940. However, NCERT shows Net Profit Rs 15,895 and Total of the Balance Sheet Rs 76,945.

Explanation / Working Notes :

1. Closing Stock: Record closing stock Rs 10,000 in Trading Account to determine gross profit.

2. Provision for Doubtful Debts: Maintain provision at 5% on sundry debtors after adjusting specific bad debts; record any increase or decrease of provision in Profit and Loss Account.

3. Outstanding & Prepaid Items: Wages Rs 500 and salary Rs 350 outstanding are treated as expenses of the year and shown as current liabilities. Factory rent prepaid Rs 100 is an asset and carried to next period. Outstanding insurance Rs 100 is an expense for the year and shown under current liabilities until paid.

4. Depreciation: Charge 5% on Plant and Machinery and 10% on Building; treat depreciation as expense and reduce asset values. Differences from NCERT answers usually arise from rounding; ensure consistent rounding when preparing the final statements.

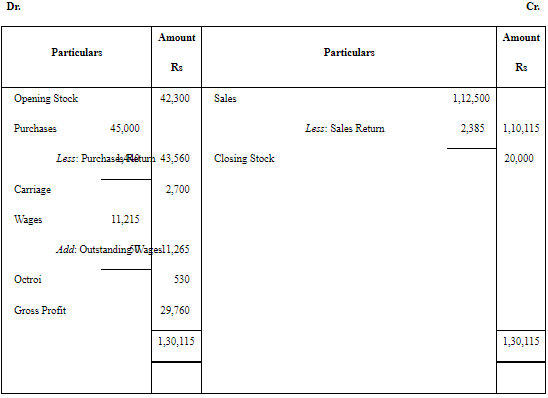

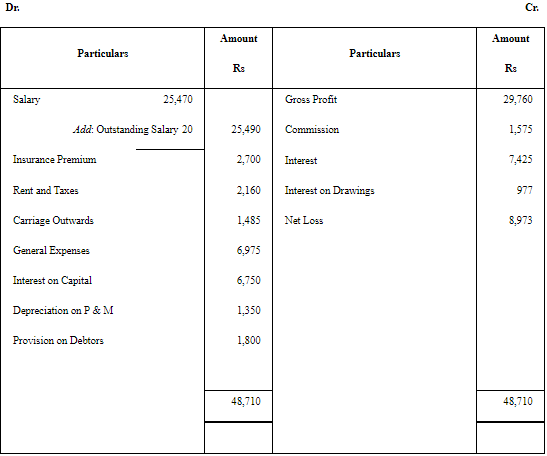

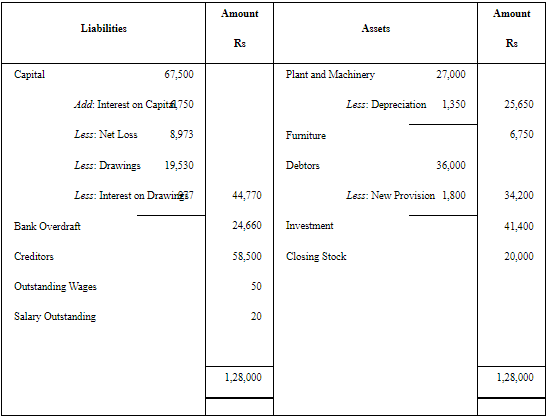

Q10: The following balances have been extracted from the books of M/s Green House for the year ended December 31, 2017, prepare trading and profit and loss account and balance sheet as on this date.

adjustments :

(a) Machinery is depreciated at 10% and buildings depreciated at 6%.

(b) Interest on capital @ 4%.

(c) Outstanding wages Rs 50.

(d) Closing stock Rs 50,000.

Ans:

Explanation / Working Notes :

1. Depreciation: Charge 10% on machinery and 6% on buildings; show these in the Profit and Loss Account and reduce asset balances in the Balance Sheet.

2. Interest on Capital: Interest on capital at 4% is treated as an expense and charged to Profit and Loss Account (unless partners' agreement states otherwise) and added to capital balance in the Balance Sheet.

3. Outstanding Wages and Closing Stock: Outstanding wages Rs 50 are an expense for the period and shown under current liabilities. Closing stock Rs 50,000 is taken to Trading Account and shown in current assets in the Balance Sheet.

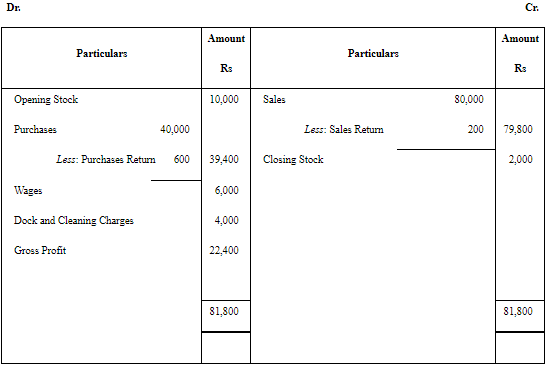

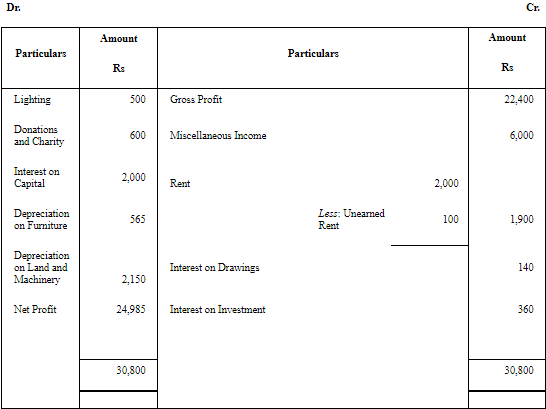

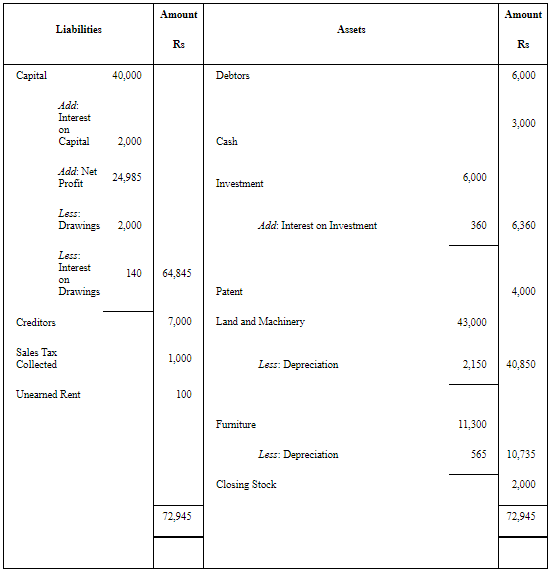

Question.11 : From the following balances extracted from the book of M/s Manju Chawla on March 31, 2017. You are requested to prepare the trading and profit and loss account and a balance sheet as on this date.

Closing stock was Rs 2,000.

(a) Interest on drawings @ 7% and interest on capital @ 5%.

(b) Land and Machinery is depreciated at 5%.

(c) Interest on investment @ 6%.

(d) Unexpired rent Rs 100.

(e) Charge 5% depreciation on furniture.

Answer :Trading Account

Profit and Loss Account

Balance Sheet

Note: In the NCERT textbook, the answer provided for question number 11 is different from the solution. However, the answer should be

Gross profit = Rs 22,400 instead of Rs 21,900

Net profit = Rs 24,985 instead of Rs 25,185

Total of Balance Sheet = Rs 72,945 instead of Rs 71,185

Explanation / Working Notes :

1. Closing Stock: Closing stock Rs 2,000 is credited to Trading Account to arrive at gross profit.

2. Interest on Capital and Drawings: Interest on capital at 5% is an expense of the business (credited to proprietor's capital). Interest on drawings at 7% is income for the business and added to capital.

3. Depreciation: Charge 5% on land & machinery and 5% on furniture as given; record as expense and reduce asset values.

4. Interest on Investments and Unexpired Rent: Interest on investments at 6% is income and appears in Profit and Loss Account. Unexpired rent Rs 100 is a prepaid expense and shown under current assets.

5. Reconciliation: The note highlights discrepancies in NCERT; such differences usually come from arithmetic rounding or different treatment of certain items-follow the workings shown in the solution images for final figures.

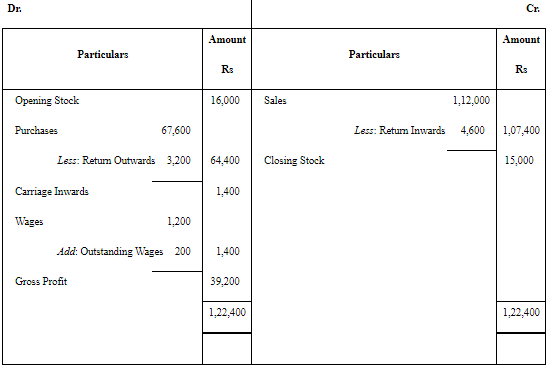

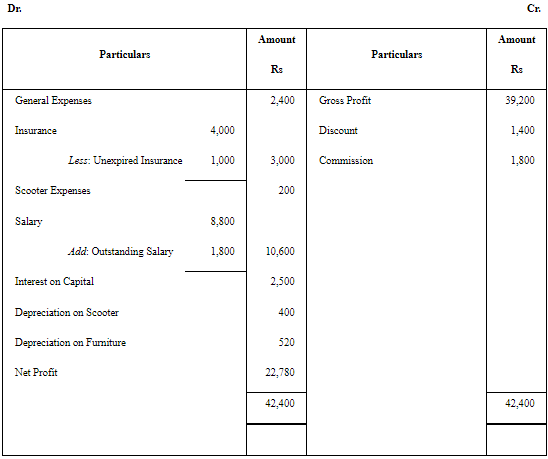

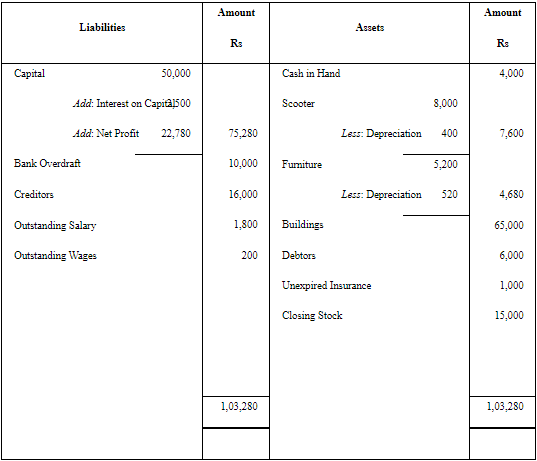

Q12: The following balances were extracted from the books of M/s Panchsheel Garments on March 31, 2017.

Prepare the trading and profit and loss account for the year ended March 31, 2017 and a balance sheet as on that date.

(a) Unexpired insurance Rs 1,000.

(b) Salary due but not paid Rs 1,800.

(c) Wages outstanding Rs 200.

(d) Interest on capital 5%.

(e) Scooter is depreciated @ 5%.

(f) Furniture is depreciated Rs @ 10%.

Answer : Trading Account

Profit and Loss Account

Balance Sheet

Explanation / Working Notes :

1. Unexpired Insurance: Unexpired insurance Rs 1,000 is a prepaid asset and is shown under current assets in the Balance Sheet. Deduct the prepaid amount from the total insurance expense charged in the year.

2. Outstanding Expenses: Salary due Rs 1,800 and wages outstanding Rs 200 are charged to the Profit and Loss Account for the year and shown as current liabilities in the Balance Sheet.

3. Interest on Capital: Interest on capital at 5% is charged to Profit and Loss Account as an expense (unless partners' deed provides otherwise) and added to capital balance.

4. Depreciation: Charge scooter at 5% and furniture at 10% on their respective book values and record depreciation as expense and reduce asset values accordingly.

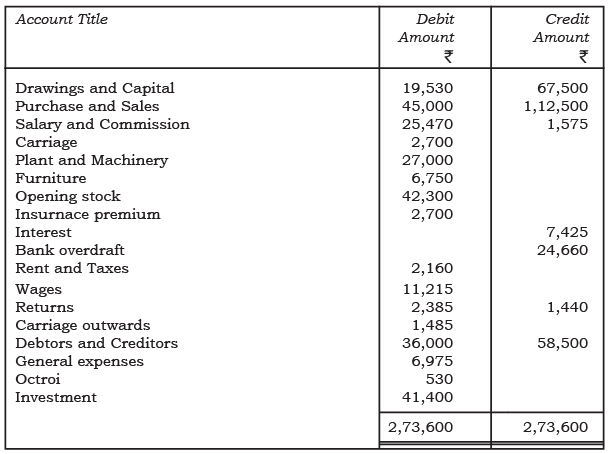

Q13: Prepare the trading and profit and loss account and balance sheet of M/s Control Device India on December 31, 2017 from the following balance as on that date.

Closing stock was valued Rs 20,000.

(a) Interest on capital @ 10%.

(b) Interest on drawings @ 5%.

(c) Wages outstanding Rs 50.

(d) Outstanding salary Rs 20.

(e) Provide a depreciation @ 5% on plant and machinery.

(f) Make a 5% provision on debtors.

Ans: Trading Account

Profit and Loss Account

Balance Sheet

Explanation / Working Notes :

1. Closing Stock: Record Rs 20,000 as closing stock in Trading Account.

2. Interest on Capital / Drawings: Interest on capital at 10% is charged as expense and added to capital; interest on drawings at 5% is treated as income of the firm and added to capital account.

3. Outstanding Wages and Salary: Wages outstanding Rs 50 and outstanding salary Rs 20 are expenses for the period and shown under current liabilities.

4. Depreciation and Provision: Provide depreciation at 5% on plant and machinery; create a 5% provision on debtors after adjusting any bad debts. Show depreciation and provision changes in Profit and Loss Account and revise asset values in the Balance Sheet.

Q14: The following balances appeared in the trial balance of M/s Kapil Traders as on March 31, 2017

The partners of the firm agreed to records the following adjustments in the books of the Firm: Further bad debts Rs.300. Maintain provision for bad debts 10%. Show the following adjustments in the bad debts account, provision account, debtors account, profit and loss account and balance sheet.

Ans: Profit and Loss Account

Explanation / Working Notes :

1. Further Bad Debts: Record further bad debts of Rs 300 by debiting Bad Debts Account and crediting Debtors Account; show the expense in the Profit and Loss Account.

2. Provision for Bad Debts (10%): After writing off additional bad debts, calculate provision as 10% of the adjusted debtor balance. The difference between the old provision and the required provision is charged or credited to Profit and Loss Account and the Provision for Doubtful Debts account is adjusted in the Balance Sheet.

3. Ledger and Statement Effects: The Debtors Account reduces by the amount written off; Bad Debts Account and Provision Account show the entries as per adjustments. Ensure the Profit and Loss Account reflects the net effect of bad debts and change in provision.

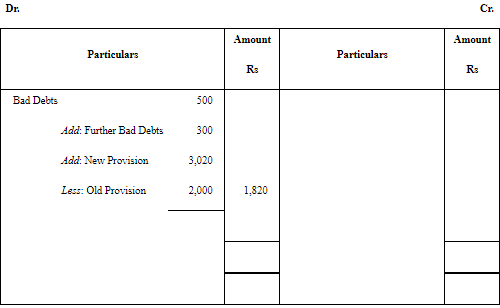

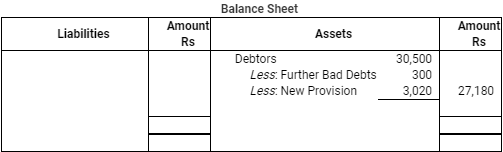

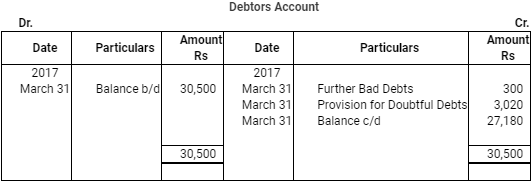

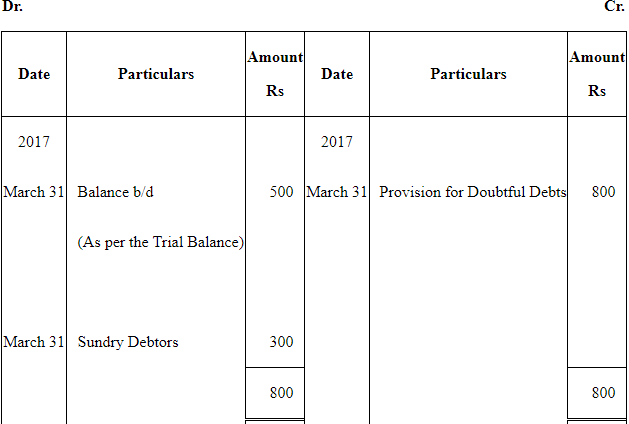

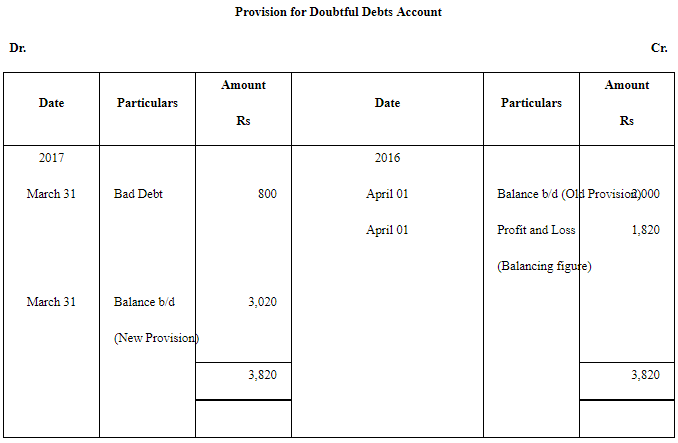

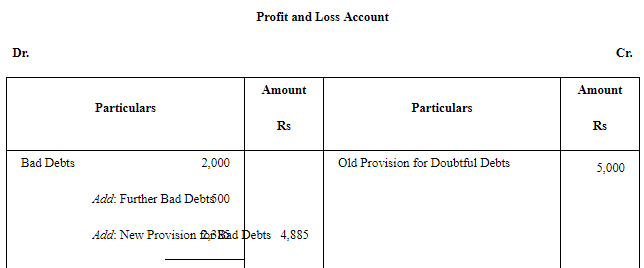

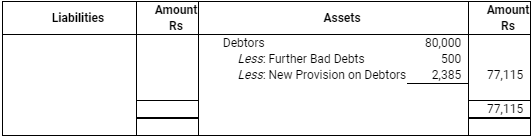

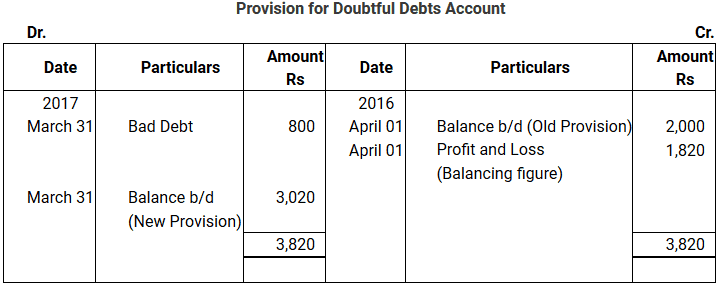

Q15: Prepare the bad debts account, provision for account, profit and loss account and balance sheet from the following information as on December 31, 2017

Adjustments:

Bad Debts Rs 500 Provision on Debtors @ 3%.

Ans:

Balance Sheet

Bad Debts Account

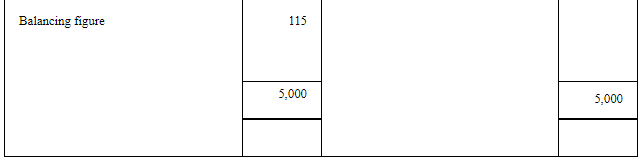

Note: In this case, the old provision exceeds the sum total of Bad debts and the New Provision. Thus, the balancing figure is Rs 115 and is calculated as Rs 2,500 + Rs 2,385 - Rs 5,000 = Rs (115)

Explanation / Working Notes :

1. Bad Debts: Write off additional bad debts of Rs 500 by debiting Bad Debts Account and crediting Debtors Account. Charge the bad debt expense to the Profit and Loss Account.

2. Provision on Debtors (3%): After writing off bad debts, compute the required provision as 3% of the adjusted debtors balance. If the existing provision (opening balance) is greater than the required provision plus new bad debts, the difference will be credited to Profit and Loss Account (or treated as a transfer to Profit & Loss). Conversely, an increase is charged to Profit & Loss.

3. Special Case (Old Provision Exceeds New Requirement): Where opening provision exceeds the total of bad debts and the new provision, a debit or credit balancing figure (as shown) arises; this difference is shown in the Profit and Loss Account so that the Provision for Doubtful Debts account carries the correct closing balance in the Balance Sheet.

These working notes explain the treatment and reconcile the ledger adjustments that appear in the image solutions above.

FAQs on NCERT Solution: Financial Statements - II (Part- 2)

| 1. What are the key components of a financial statement? |  |

| 2. How do financial statements help in decision-making for a business? | |

| 3. What is the significance of the income statement in financial analysis? | |

| 4. How is the balance sheet structured and what does it represent? | |

| 5. What information does the cash flow statement provide and why is it important? | |