NCERT Solution (Part - 3) - Financial Statements - II

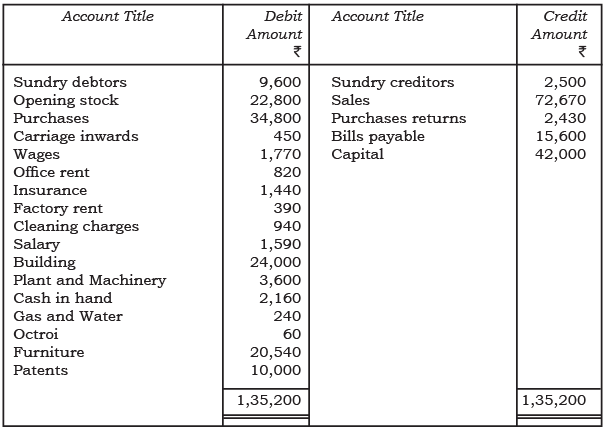

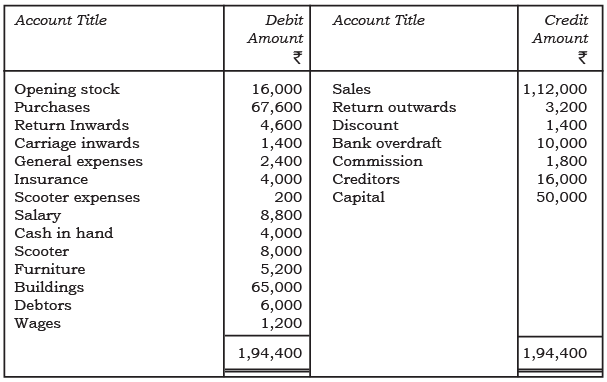

Q9: From the following balances of M/s Jyoti Exports, prepare trading and profit and loss account for the year ended March 31, 2017 and balance sheet as on this date.

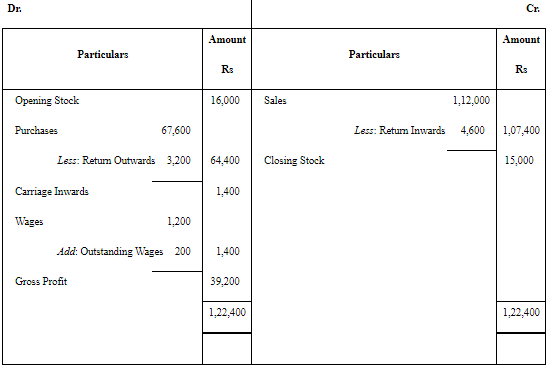

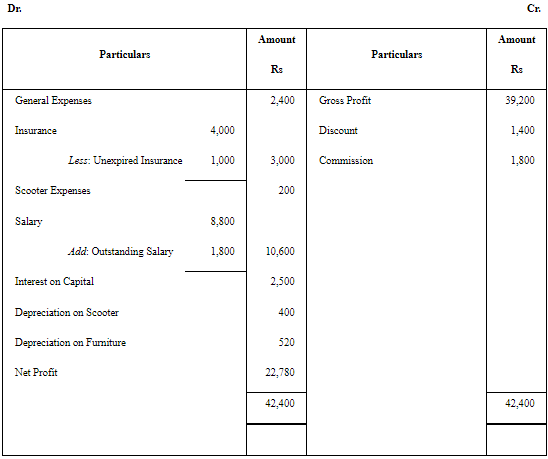

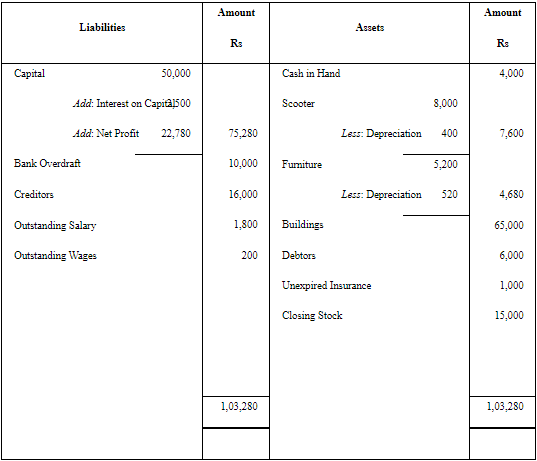

1. To provision for doubtful debts is to be maintained at 5 per cent on sundry debtors.

2. Wages amounting to Rs 500 and salary amounting to Rs 350 are outstanding.

3. Factory rent prepaid Rs 100.

4. Depreciation charged on Plant and Machinery @ 5% and Building @ 10%.

5. Outstanding insurance Rs 100.

Ans:

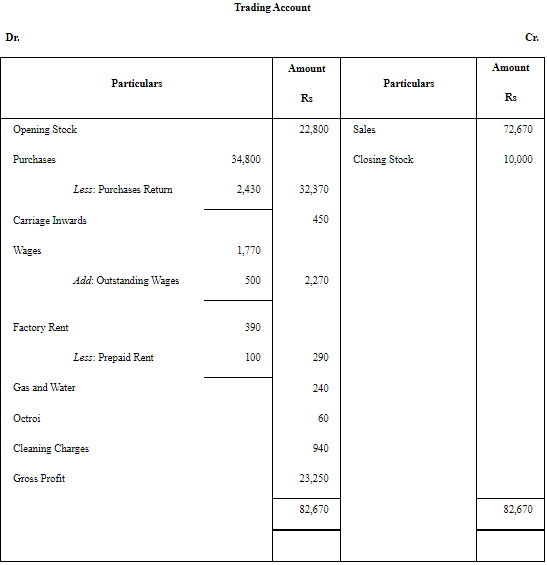

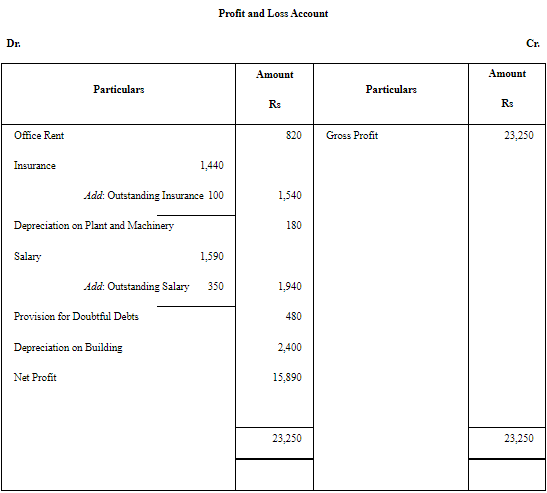

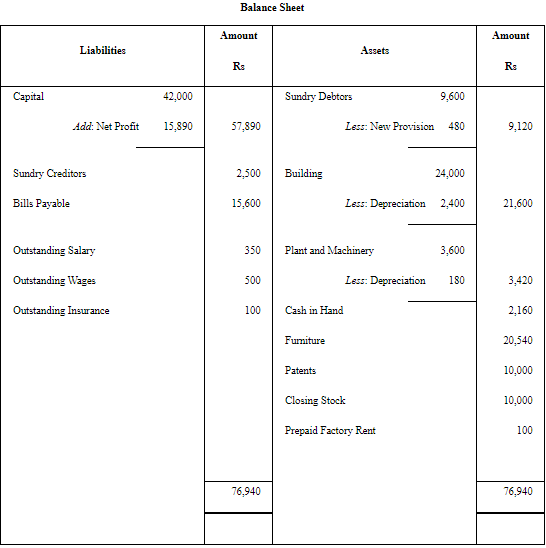

Adjustments applied before preparing the final accounts:

• Maintain provision for doubtful debts at 5% on sundry debtors (reduce debtors by the provision in the balance sheet and charge the movement in provision to Profit and Loss Account).

• Charge outstanding wages Rs 500 and salary Rs 350 to the Profit and Loss Account and show as current liabilities in the balance sheet.

• Treat factory rent prepaid Rs 100 as a current asset (deduct from rent expense in P&L or show separately under current assets).

• Provide depreciation on Plant & Machinery @ 5% and on Building @ 10% - charge these to Profit and Loss Account and reduce asset values in the balance sheet.

• Charge outstanding insurance Rs 100 as an expense in P&L and show as a current liability in the balance sheet.

Final results as per workings shown in the prepared accounts (see images below). Note that a small difference from NCERT arises because of rounding or treatment differences while computing percentage-based provisions and depreciation; the solution here gives Net Profit as Rs 15,890 and Balance Sheet total as Rs 76,940, whereas NCERT shows Net Profit Rs 15,895 and Balance Sheet total Rs 76,945.

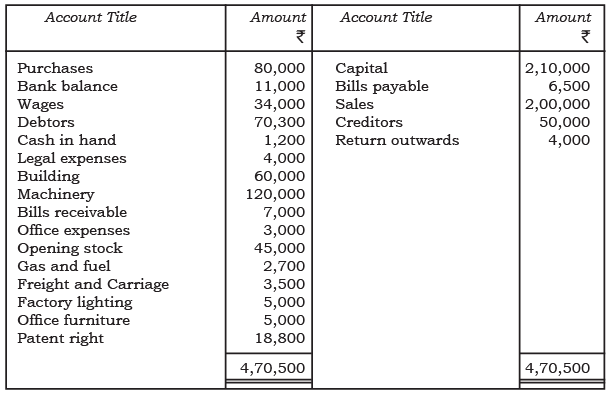

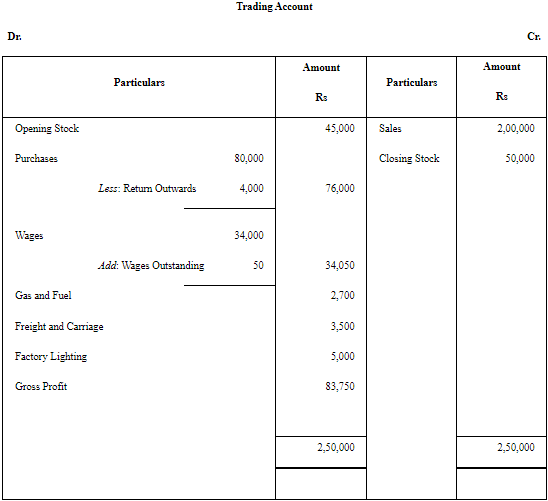

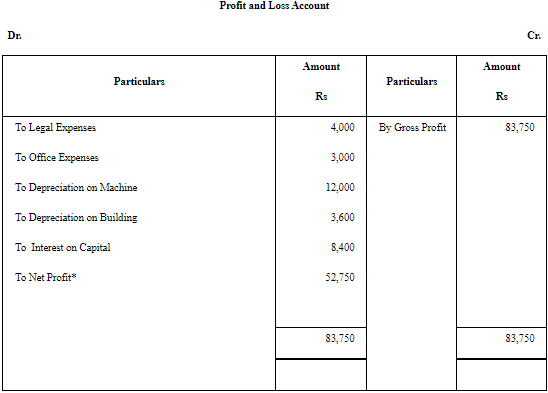

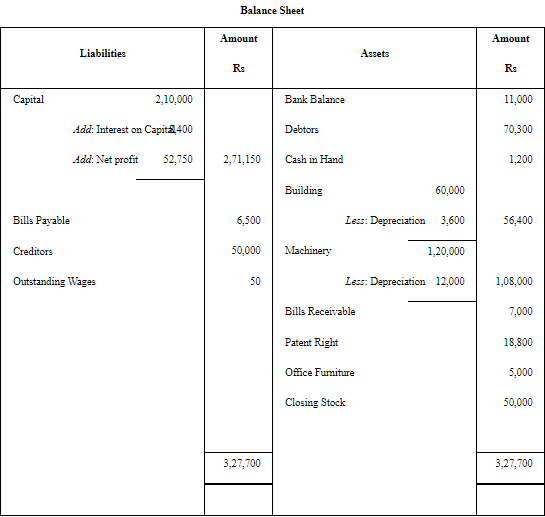

Q10: The following balances have been extracted from the books of M/s Green House for the year ended December 31, 2017, prepare trading and profit and loss account and balance sheet as on this date.

(a) Machinery is depreciated at 10% and buildings depreciated at 6%.

(b) Interest on capital @ 4%.

(c) Outstanding wages Rs 50.

(d) Closing stock Rs 50,000.

Ans:

Adjustments applied:

• Charge depreciation on Machinery @ 10% and on Buildings @ 6%; enter depreciation in the Profit and Loss Account and reduce the respective asset values in the balance sheet.

• Provide interest on capital @ 4% as an expense of the firm and record it in the Profit and Loss Account (and in partners' capital accounts if applicable).

• Record outstanding wages Rs 50 as an expense in P&L and as a current liability in the balance sheet.

• Include closing stock Rs 50,000 in the Trading Account (as current asset in the balance sheet).

The completed Trading Account, Profit and Loss Account and Balance Sheet with figures are presented in the images below.

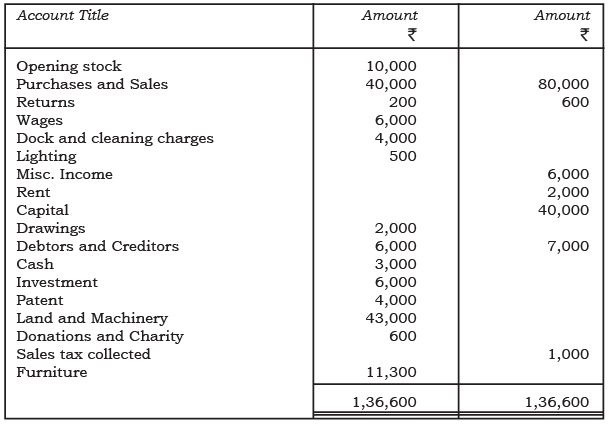

Question.11 : From the following balances extracted from the book of M/s Manju Chawla on March 31, 2017. You are requested to prepare the trading and profit and loss account and a balance sheet as on this date.

(a) Interest on drawings @ 7% and interest on capital @ 5%.

(b) Land and Machinery is depreciated at 5%.

(c) Interest on investment @ 6%.

(d) Unexpired rent Rs 100.

(e) Charge 5% depreciation on furniture.

Answer :

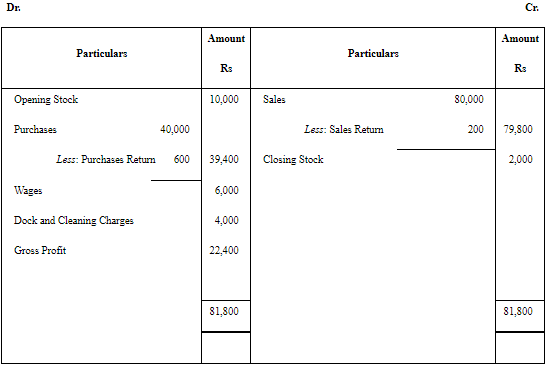

Trading Account

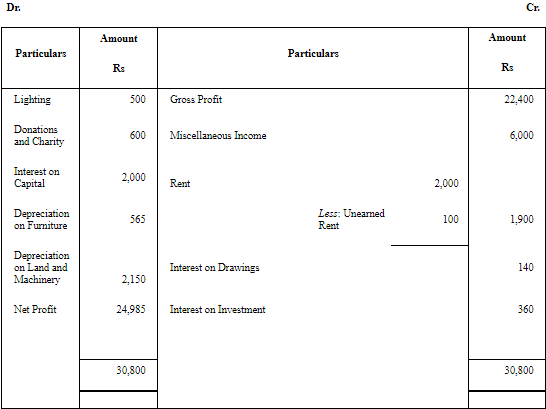

Adjustment summary and working notes:

• Charge interest on capital @ 5% to the Profit and Loss Account and interest on drawings @ 7% to be deducted directly from the proprietor's capital (or shown in P&L appropriation section if required).

• Provide depreciation on Land and Machinery @ 5% and on Furniture @ 5%; include depreciation charge in P&L and reduce asset values in the balance sheet.

• Record interest on investment @ 6% as income in the Profit and Loss Account.

• Treat unexpired rent Rs 100 as a prepaid expense (current asset).

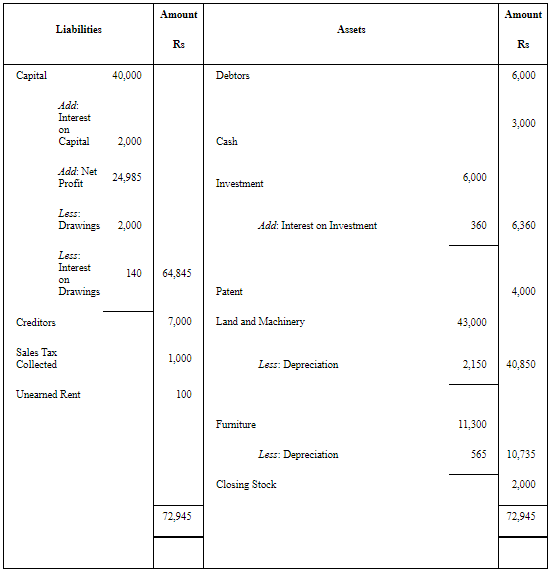

The prepared accounts are shown in the images above. Note: The corrected final figures (after careful application of the adjustments) give Gross Profit = Rs 22,400, Net Profit = Rs 24,985 and Balance Sheet Total = Rs 72,945, which differ from the NCERT figures quoted in the original book; the differences arise from the method of applying interest and rounding in depreciation and provision computations.

Q12: The following balances were extracted from the books of M/s Panchsheel Garments on March 31, 2017.

(a) Unexpired insurance Rs 1,000.

(b) Salary due but not paid Rs 1,800.

(c) Wages outstanding Rs 200.

(d) Interest on capital 5%.

(e) Scooter is depreciated @ 5%.

(f) Furniture is depreciated Rs @ 10%.

Answer : Trading Account

Profit and Loss Account

Key adjustments applied:

• Treat unexpired insurance Rs 1,000 as a prepaid expense (current asset).

• Record salary due Rs 1,800 and wages outstanding Rs 200 as expenses and current liabilities.

• Charge interest on capital @ 5% to P&L (or in appropriation section) as per firm's agreement.

• Provide depreciation on scooter @ 5% and on furniture @ 10%, charge to P&L and reduce fixed asset values in the balance sheet.

The trading, profit and loss accounts and balance sheet showing the computed figures are given in the images above.

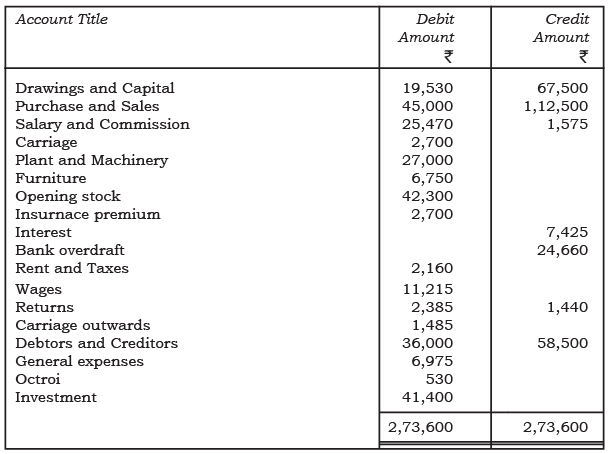

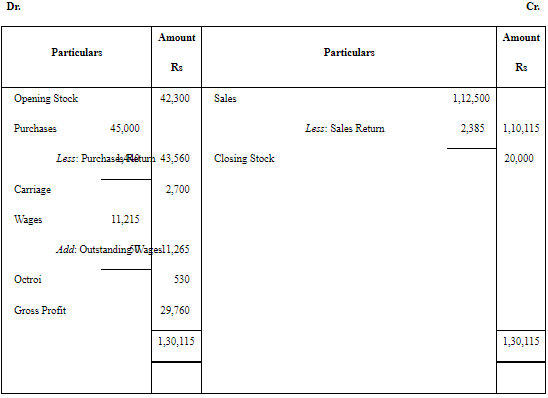

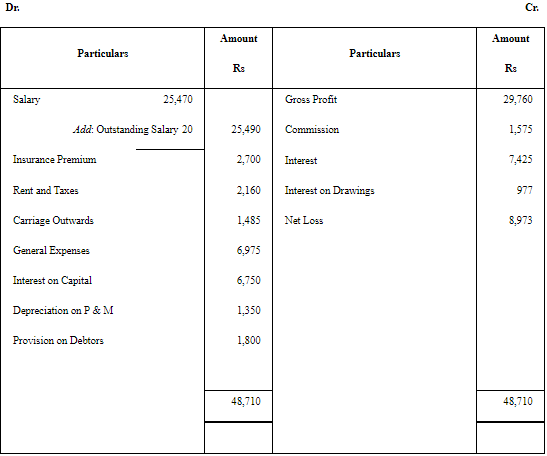

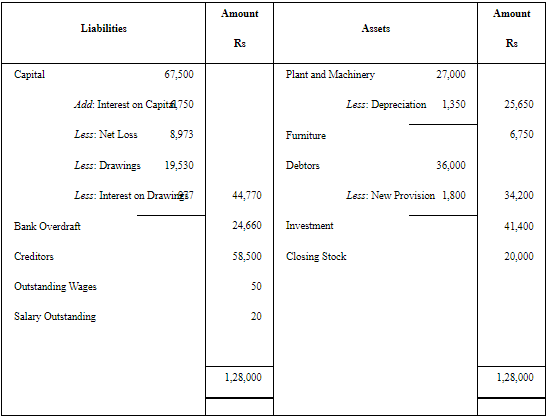

Q13: Prepare the trading and profit and loss account and balance sheet of M/s Control Device India on December 31, 2017 from the following balance as on that date.

(a) Interest on capital @ 10%.

(b) Interest on drawings @ 5%.

(c) Wages outstanding Rs 50.

(d) Outstanding salary Rs 20.

(e) Provide a depreciation @ 5% on plant and machinery.

(f) Make a 5% provision on debtors.

Ans:

Applied adjustments summary:

• Charge interest on capital @ 10% as an expense (capital remuneration).

• Deduct interest on drawings @ 5% from proprietor's account or treat appropriately.

• Record wages outstanding Rs 50 and salary outstanding Rs 20 as current liabilities and charge to P&L.

• Provide depreciation @ 5% on plant and machinery; charge to P&L and reduce asset value in the balance sheet.

• Create a provision for doubtful debts @ 5% on debtors - charge change to P&L and show provision in the balance sheet by reducing debtors.

The completed Trading Account, Profit and Loss Account and Balance Sheet are presented in the images below.

Trading Account

Balance Sheet

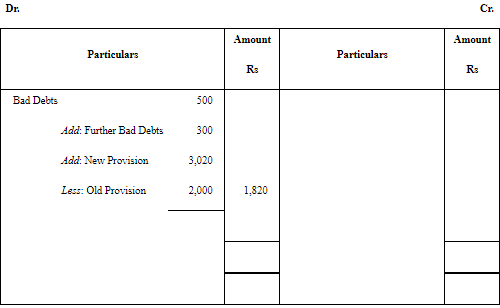

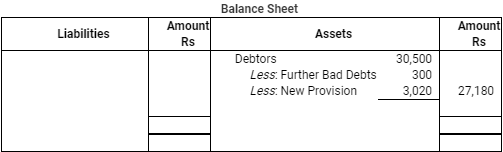

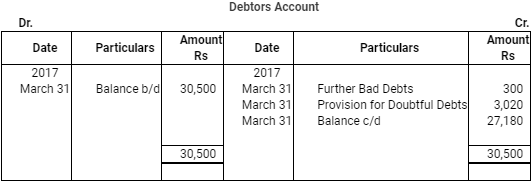

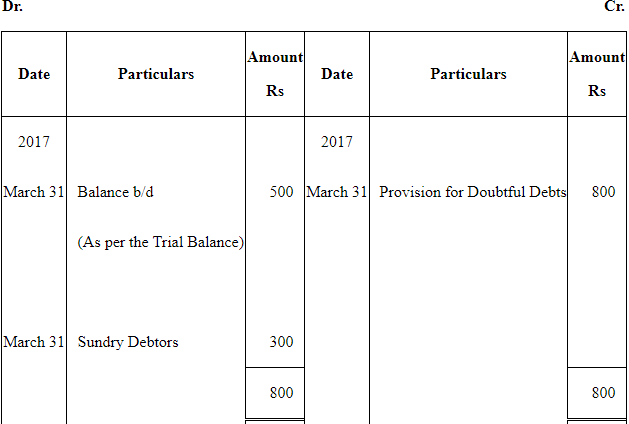

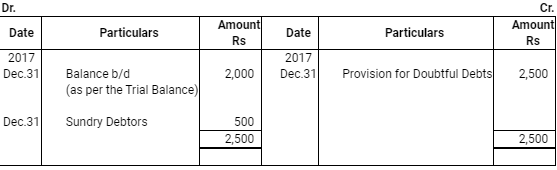

Q14: The following balances appeared in the trial balance of M/s Kapil Traders as on March 31, 2017

Ans:

Procedure followed and effect on accounts:

• Record the additional bad debts Rs 300 by debiting Bad Debts Account and crediting Debtors Account.

• Recalculate provision for doubtful debts at 10% on the revised debtors balance and adjust the difference between the old provision and the new provision through the Profit and Loss Account (or through Provision for Doubtful Debts account as appropriate).

• Update the Debtors Account for bad debts written off and for provision movements; present the net debtors figure (debtors less provision) in the balance sheet.

• The entries and the movement in accounts - Bad Debts Account, Provision for Doubtful Debts Account, Debtors Account and the impact on Profit and Loss Account and Balance Sheet - are shown in the images below for clear reference.

Profit and Loss Account

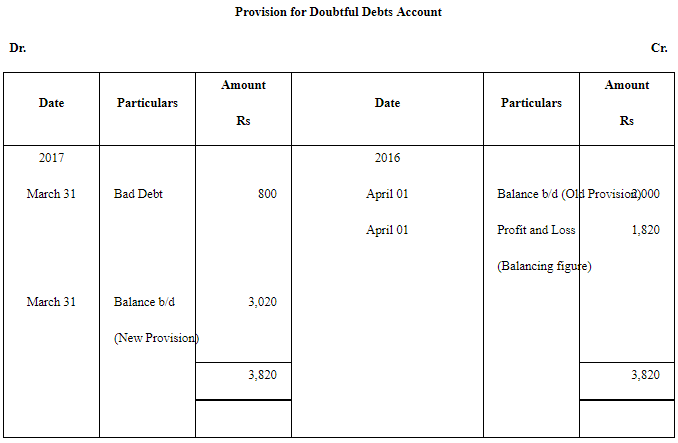

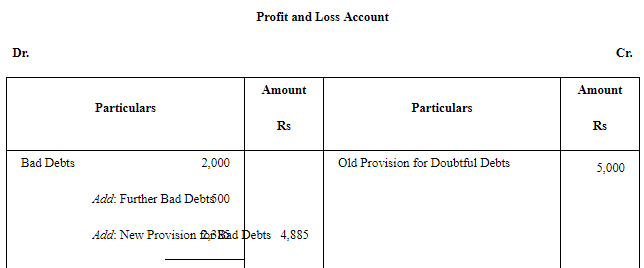

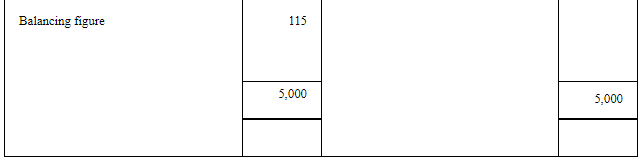

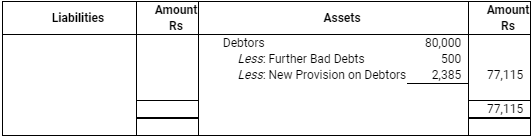

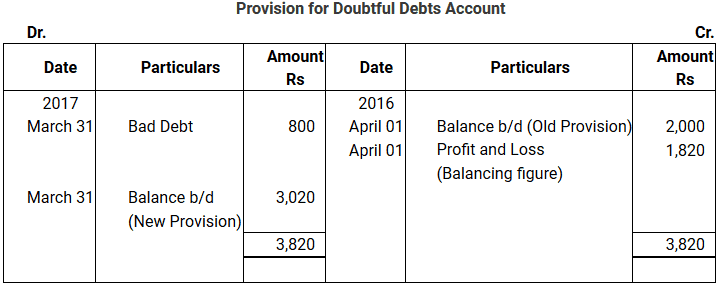

Q15: Prepare the bad debts account, provision for account, profit and loss account and balance sheet from the following information as on December 31, 2017

Adjustments:

Bad Debts Rs 500 Provision on Debtors @ 3%.

Ans:

Explanation of the balancing figure:

• When the existing (old) provision for doubtful debts is greater than the amount required after charging current bad debts and creating the new provision, the excess provision is written back to the Profit and Loss Account as an income (that is, a favourable adjustment).

• In the working shown, the calculation is: Old provision Rs 2,500 + Bad debts Rs 2,385 - Required provision Rs 5,000 = Rs (115). This negative balancing figure represents an amount to be written back to the Profit and Loss Account (a credit), thereby increasing net profit by Rs 115.

FAQs on NCERT Solution (Part - 3) - Financial Statements - II

| 1. What are the key components of a financial statement? |  |

| 2. How do financial statements help in decision-making for a business? | |

| 3. What is the difference between the cash flow statement and the income statement? | |

| 4. Why is it important to prepare financial statements at the end of an accounting period? | |

| 5. What role do financial ratios play in analyzing financial statements? | |