NCERT Solution (Part - 4) - Accounts from Incomplete Records | SSC CGL Tier 2 - Study Material, Online Tests, Previous Year PDF Download

Page No. 483

Question 23: Calculate the amount of bills receivable dishonoured from the following information.

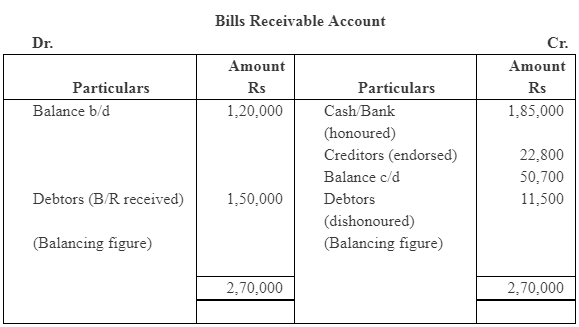

Answer :

Bills Receivable dishonoured is Rs 11,500.

Question 24: From the details given below, find out the credit sales and total sales.

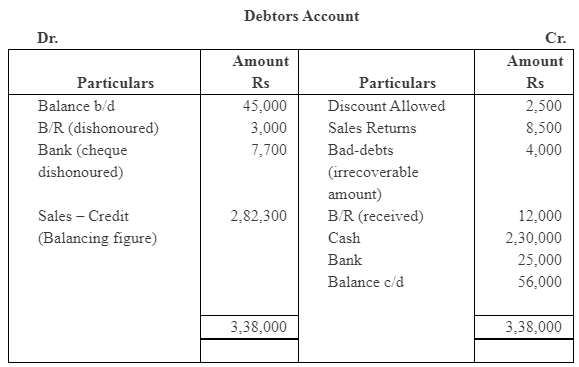

Answer :

Credit sales is Rs 2,82,300Total Sales = Cash Sales + Credit Sales

Sales

= 80,000 + 2,82,300

= Rs 3,62,300

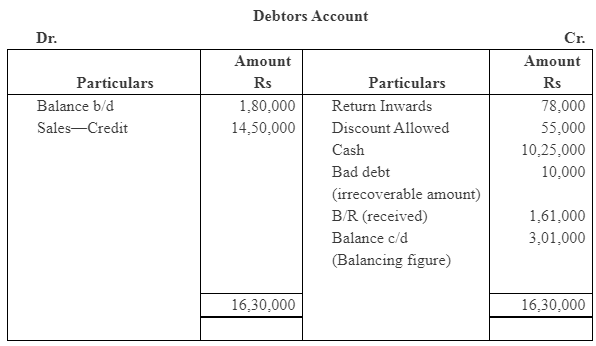

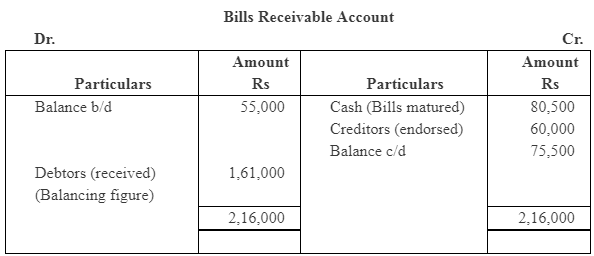

Question 25: From the following information, prepare the bills receivable account and total debtors account for the year ended December 31, 2017.

Answer :

The missing figure in the bills receivable account -B/R received from debtors Rs 1,61,000 and the missing figure in the debtors accountant-closing balance is Rs 3,01,000.

Page No. 484

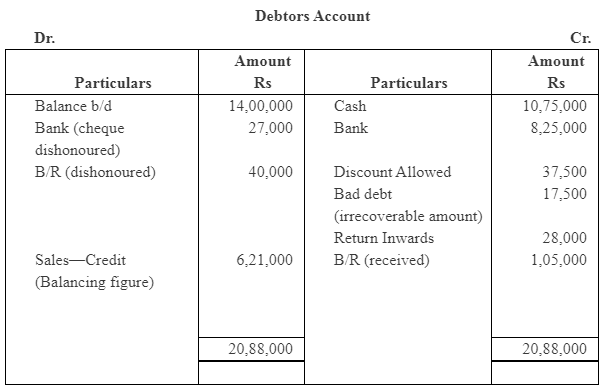

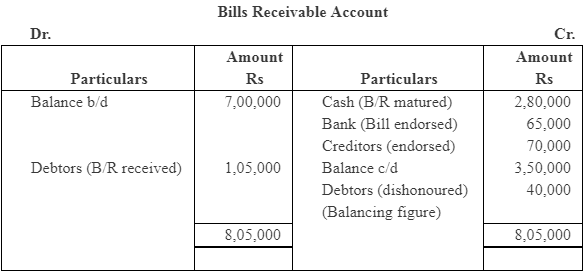

Question 26: Prepare the suitable accounts and find out the missing figure if any.

Answer :

Note: As per solution, the missing figure in the bills receivable account is

B/R dishonoured of Rs 40,000. The missing figure in the debtors account is the credit sales of Rs 6,21,000, However, the NCERT book shows a credit sales Rs 5,16,000.

In order to match our answer with that of the book, B/R received from the customers is not shown in the debtors account.

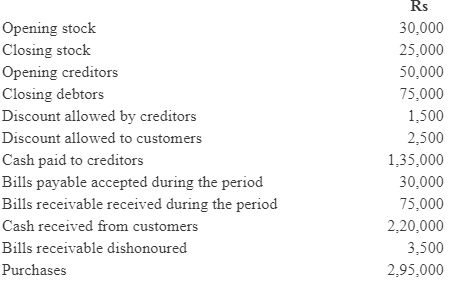

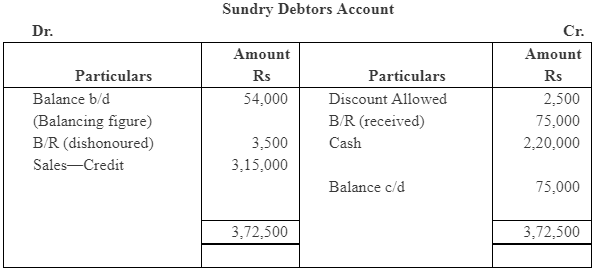

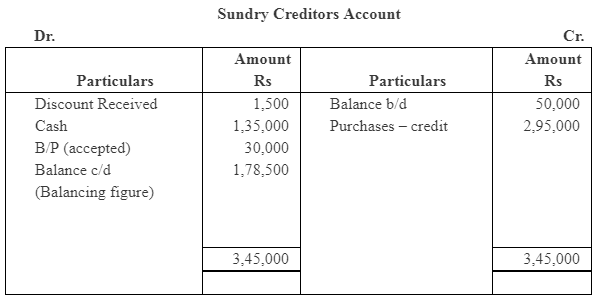

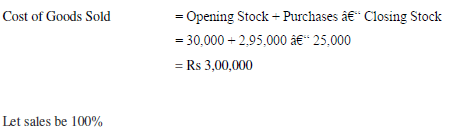

Question 27: From the following information ascertain the opening balance of sundry debtors and closing balance of sundry creditors

The rate of gross profit is 25% on selling price and out of the total sales

Rs 85,000 was for cash sales.

Answer :

Opening balance of debtors is Rs 54,000 and the closing balance of creditors is Rs 1,78,500.

Working Notes:

Total Sales = Cash Sales + Credit Sales

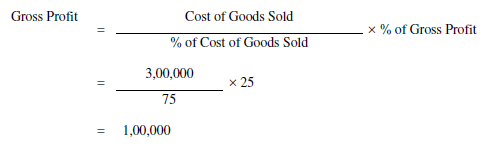

Total Sales = Cost of Goods Sold + Gross Profit

Sales = Cost of Goods sold + Gross Profit

Or, 100 = Cost of Goods sold + 25%

Cost of Goods Sold = 100% - 25% = 75%

Sales = Cost of Goods Sold + Gross Profit

= 3,00,000 + 1,00,000

= Rs 4,00,000

Note: Here, it has been assumed that all purchases were made on credit.

Page No. 485

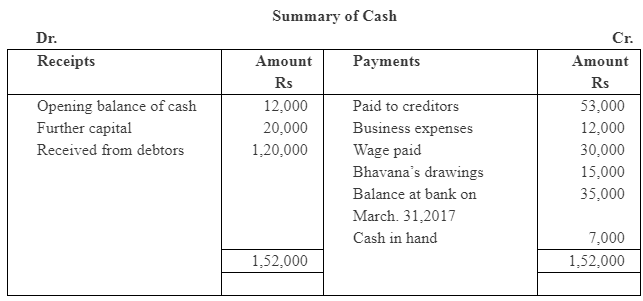

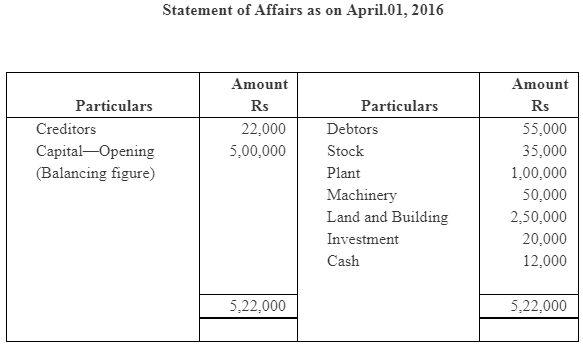

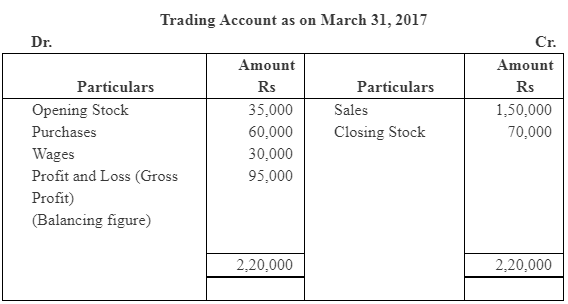

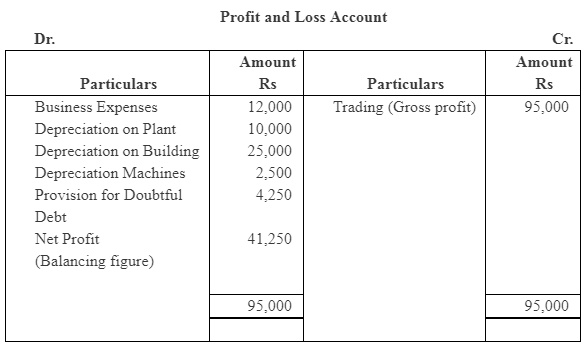

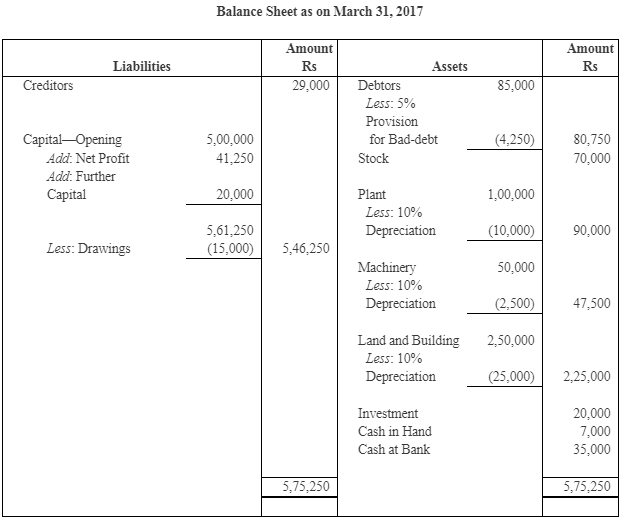

Question 28: Mrs Bhavana keeps his books by Single Entry System. You.re required to prepare final accounts of her business for the year ended December 31, 2005. Her records relating to cash receipts and cash payments for the above period showed the following particulars :

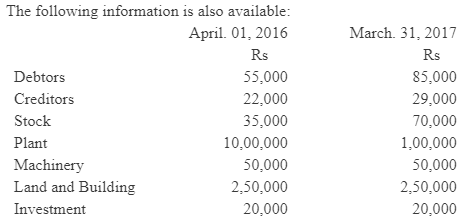

The following information is also available:

All her sales and purchases were on credit. Provide depreciation on plant and building by 10% and machinery by 5%, make a provision for bad debts by 5%.

Answer :

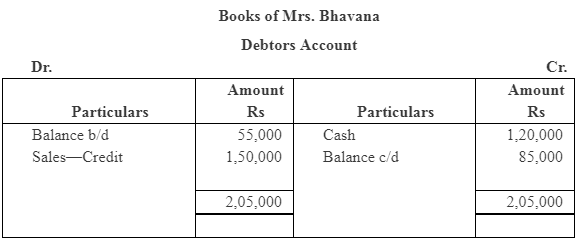

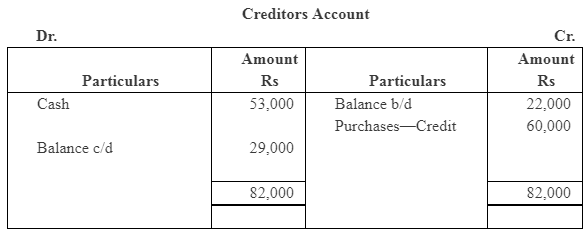

Note: It has been assumed that total sales are credit sales (i.e. all sales are made on credit) and total purchases are credit purchases (i.e. all purchases are made on credit).

Plant of Rs 1,00,000 has been taken in to the statement of affairs on January 01, 2016, instead of Rs 10,00,000.

|

1365 videos|1312 docs|1010 tests

|

FAQs on NCERT Solution (Part - 4) - Accounts from Incomplete Records - SSC CGL Tier 2 - Study Material, Online Tests, Previous Year

| 1. What is meant by accounts from incomplete records? |  |

| 2. How can accounts from incomplete records be prepared? | |

| 3. What are the limitations of accounts from incomplete records? | |

| 4. What are the advantages of accounts from incomplete records? | |

| 5. What are the key components of preparing accounts from incomplete records? | |

|

1.8K Views |

|

4.97/5 Rating |

|

Dec 25, 2024 Last updated |

|

1365 videos|1312 docs|1010 tests

|

|

Explore Courses for SSC CGL exam

|

|

MCQs

,Online Tests

,Semester Notes

,NCERT Solution (Part - 4) - Accounts from Incomplete Records | SSC CGL Tier 2 - Study Material

,Previous Year

,study material

,Previous Year

,shortcuts and tricks

,Objective type Questions

,NCERT Solution (Part - 4) - Accounts from Incomplete Records | SSC CGL Tier 2 - Study Material

,ppt

,Viva Questions

,Exam

,practice quizzes

,Free

,Online Tests

,Summary

,Online Tests

,past year papers

,Important questions

,Previous Year Questions with Solutions

,mock tests for examination

,NCERT Solution (Part - 4) - Accounts from Incomplete Records | SSC CGL Tier 2 - Study Material

,video lectures

,Extra Questions

,Sample Paper

,Previous Year

;

NCERT Solution (Part - 4) - Accounts from Incomplete Records Free PDF Download

Importance of NCERT Solution (Part - 4) - Accounts from Incomplete Records

NCERT Solution (Part - 4) - Accounts from Incomplete Records Notes

NCERT Solution (Part - 4) - Accounts from Incomplete Records SSC CGL Questions

Study NCERT Solution (Part - 4) - Accounts from Incomplete Records on the App

|

© EduRev

|

Education Revolution

|

|