NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation | SSC CGL Tier 2 - Study Material, Online Tests, Previous Year PDF Download

Q19 :

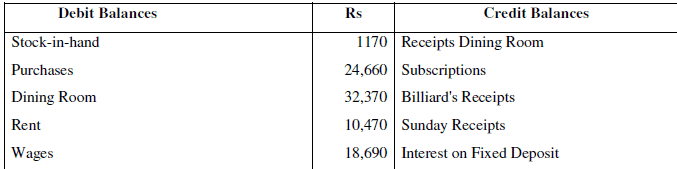

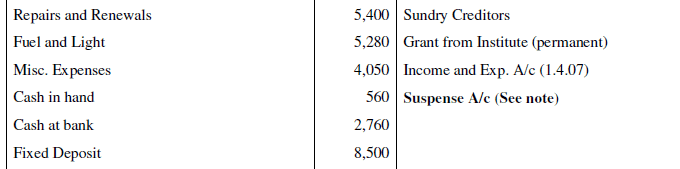

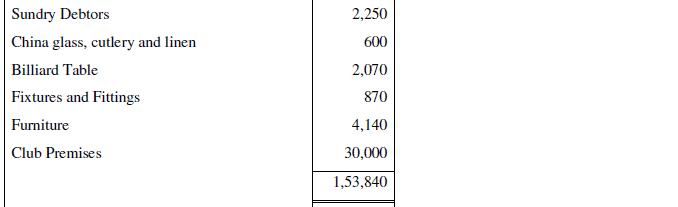

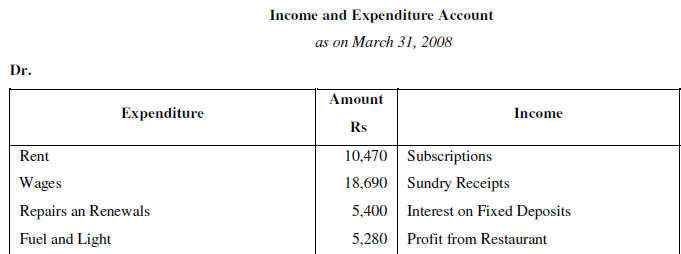

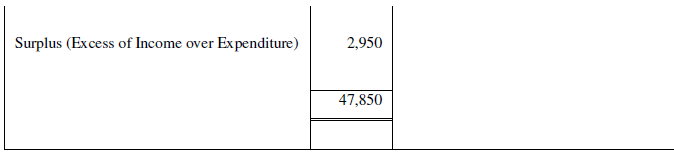

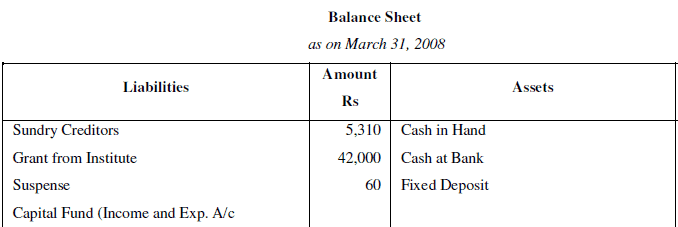

As at March 31,2008 the following balances have been extrated from the books of the

Indian Chartered Accountants Recreation Club and you are asked to prepare

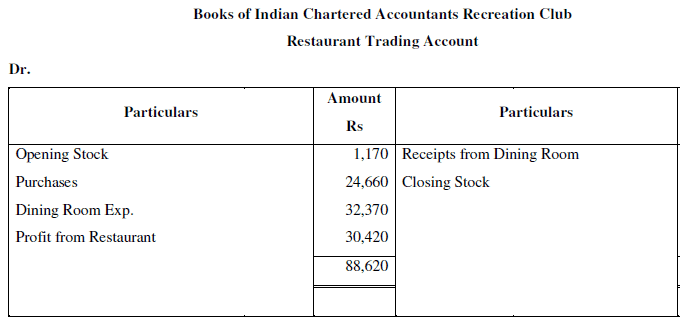

(1) Trading

Account for ascertaining gross profit derived from running restaurant and dining room

and

(2) Income and Expenditure Account for the year ended March 31, 2008

(3) and a Balance Sheet as at that date.

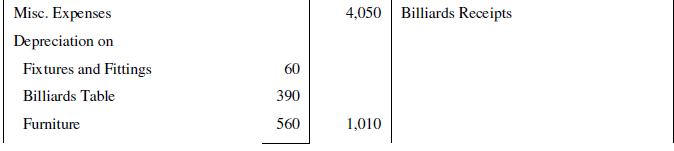

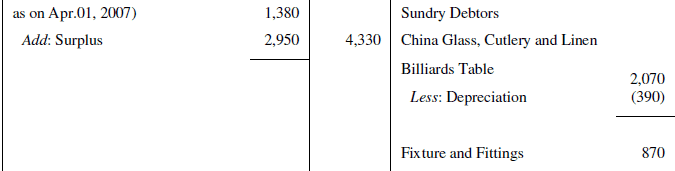

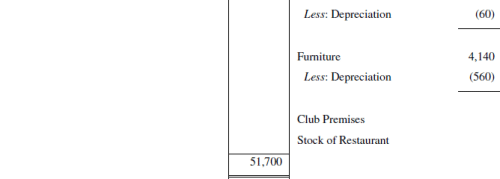

On March 31,2008 stock of restaurant consisted of Rs 900 and Rs 60 respectively. Provide

depreciations Rs 60 on fixtures and fittings, Rs 390 on billiard table and Rs 560 on

furniture.

Answer :

Important Note:

1. Credit side of the Trial Balance of the question is short by Rs 60. Thus, in order to tally

both sides of the Trial Balance, Suspense Account will be opened with the difference

amount of Rs 60.

2. In the adjustment, Closing Stock should be Rs 960 instead of Rs 900.

Long answers : Solutions of Questions on Page Number : 474

Q1 :

Explain the statement: “Receipt and Payment Account is a summarised version

of Cash Book”.

Answer :

Receipts and Payments Account is a summary of the Cash Book. This account is

prepared by those organisations which maintain their books on cash basis. All cash

receipts are recorded on the Receipts side (i.e. Debit side) and all cash payments are

recorded on the Payments side (i.e. Credit side) of Receipts and Payments Account. It

is prepared on the basis of cash and bank transactions recorded in the Cash Book. It

begins with the opening balance of cash and bank and ends with the closing balances

of cash and bank (balancing figure) at the end of the accounting period. It records all the

cash and bank transactions both of capital and revenue nature. It not only records the

cash and bank transactions relating to the current accounting period, but also cash and

bank receipts (or payments) received during the current accounting period that may be

related to the previous or next accounting period. This account only helps us to

ascertain the closing balance of the cash and bank and helps in assessing the cash

position of an NPO. It also forms the basis for the preparation of Income and

Expenditure Account.

Similarities between Receipt and Payments Account and Cash Book

The following are the features of Receipt and Payment Account that are common to

those of Cash Book:

1. Nature: It is a summarised version of the Cash Book. Similar to the Cash Book, the

Receipt and Payment Account is also a Real Account.

2. Nature of Transactions: It records only cash and bank transactions similar to a Two-

Column Cash Book. Transactions other than cash and bank like depreciation, loss/

profit on sale of assets, etc. are not recorded in this account.

3. No distinction between Capital and Revenue items: It records all the cash and

bank receipts and payments of both capital and revenue nature. Likewise, the

transactions recorded in the Cash Book are also of both capital and revenue nature.

4. Opening and closing balance: It begins with the opening balance of cash and bank

and ends with the closing balance of the cash and bank (balancing figure) at the end of

the accounting period.

5. Purpose: It reveals the cash position of an organisation. It helps to ascertain the total

amount paid and received during an accounting period. Similarly, a Cash Book also

helps us to assess the cash position of an organisation.

Thus, on the basis of the above mentioned points and similarities, the statement

'Receipt and Payment Account is a summarised version of Cash Book' is justified.

Q2 :

“Income and Expenditure Account of a Not-for-Profit Organisation is akin to Profit

and Loss Account of a business concern”. Explain the statement.

Answer :

Income and Expenditure Account (I&E) is similar to Profit and Loss Account (P&L), in

the sense that the former is prepared by Not-for-profit-Organisations and the latter is

prepared by profit earning organisations. Both the accounts are prepared on the accrual

basis.

Similar to the P&L, all the expenses and losses pertaining to the current accounting

period are recorded on the debit side (Expenditure side) and all the gains and income of

the current accounting period are recorded on the credit side (Income side) of the I&E.

The balancing figure of the I&E is surplus or deficit and that of the P&L is net profit or

net loss. Both the accounts record only revenue items which are related to the current

accounting period.

Similarities between Income and Expenditure Account and Profit and Loss Account

I&E Account of an NPO is akin to the Profit and Loss Account of a profit earning

business in the following manners.

1. Nature of Account: Both the concerned accounts are nominal in nature.

2. Basis of Recording: Both the accounts record only revenue expenses and revenue

income related to the current accounting period. The items of capital nature are not

ignored while preparing these accounts.

3. Period: Transactions related to current year are recorded in Income and Expenditure

account in the same manner in which profit and loss account is prepared. Transactions

related to previous year or next year are excluded.

4. Adjustments: The treatment of adjustments like, outstanding expenses, prepaid

expenses, income received in advance, income due but not received, depreciation, bad

debts etc. is same as that in Profit and Loss Account. Thus, both the accounts are

prepared on the accrual basis.

Q3 :

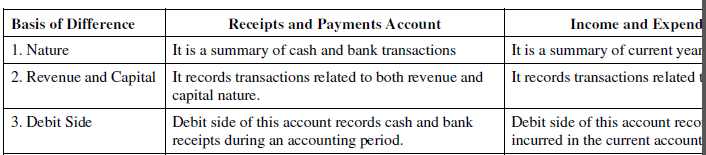

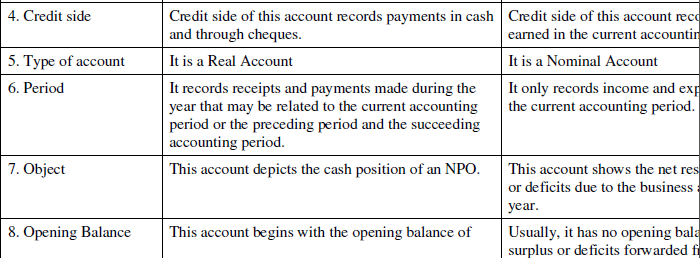

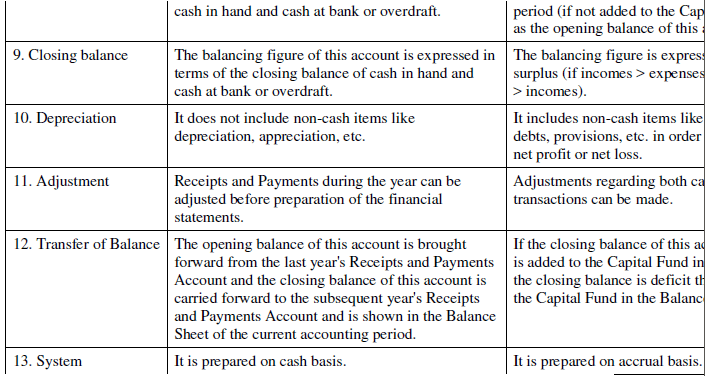

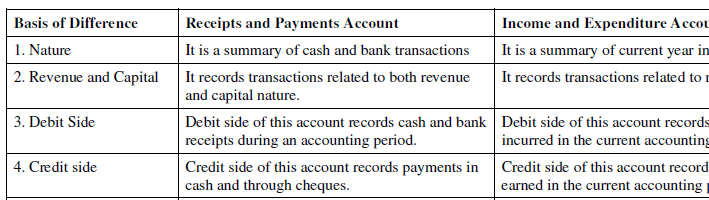

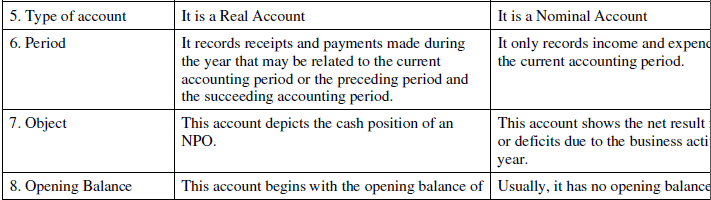

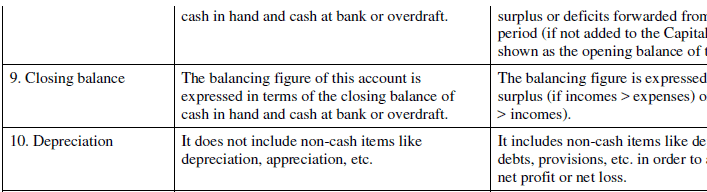

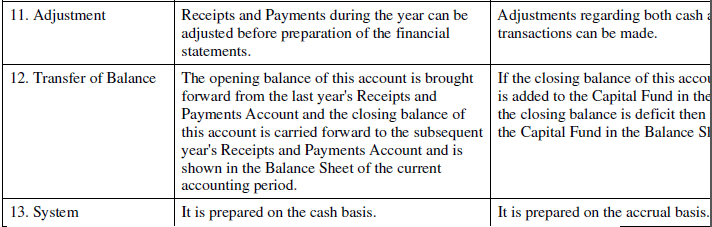

Distinguish between Receipts and Payments Account and Income and Expenditure Account.

Answer:

Q4 :

Explain the basic features of Income and Expenditure Account and of Receipt and

Payment Account.

Answer :

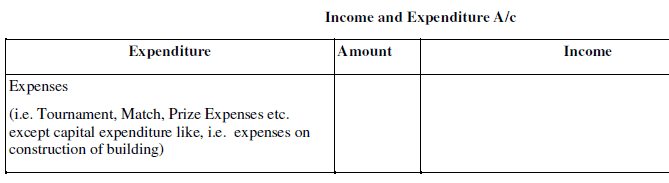

Income and Expenditure Account (I&E) Account is a Nominal Account and is prepared

on the accrual basis. It records all transactions of revenue nature that are related to the

current accounting period (whether outstanding or prepaid) for which the books are

maintained. All expenses and losses are recorded on the debit side (Expenditure side)

and all income and gains are recorded on the credit side (Income side) of I&E Account.

The closing balance or the balancing figure of I&E Account is termed as surplus (or

deficit), if the sum total of the Income side exceeds (is lesser than) the sum total of the

Expenditure side.

The following are the basic features of Income and Expenditure Account

1. Nature: It is a Nominal Account. The debit side of I&E records all expenses and

losses and the credit side records all incomes and gains related to the current

accounting period.

2. Basis: It is prepared on the basis of Receipt and Payment Account (R&P). All the

revenues items whether incomes or expenditures are transferred from R&P.

3. Excludes Capital Transactions: The transactions those are capital in nature are

excluded from this account. For example, only profit or loss on sale of fixed assets is

recorded but the total amount of sales is not recorded since sale of fixed asset is

considered as a capital receipt.

4. Akin to Profit and Loss Account: Income and Expenditure Account (I&E) is similar

to the Profit and Loss Account in the sense that while the former is prepared to

ascertain surplus or deficit during an accounting period the latter is prepared to

ascertain net profit or net loss incurred during an accounting period.

5. Records only Current Year's items: This account records only those transactions

that are related to current accounting year. In other words, transactions related to the

preceding or succeeding accounting period are excluded even if these transactions are

realised in the current period.

6. Adjustments: Various cash and non-cash items like, outstanding expenses, prepaid

expenses, income received in advance, income due but not received, depreciation, bad

debts, etc. can be adjusted in this account.

7. Balancing Figure: The balancing figure of this account is expressed in terms of

either surplus (if incomes > expenses) or deficit (if expenses > incomes). The surplus

balance, if any, is added to the Capital Fund, whereas, the deficit balance, if any, is

deducted from the Capital Fund.

Receipts and Payments Account is a summary of the Cash Book. All the cash receipts

are recorded on the Receipts side (i.e. Debit side) and all the cash payments are

recorded on the Payments side (i.e. Credit side) of Receipts and Payments Account. It

is prepared on the basis of cash and bank transactions recorded in the Cash Book. It

begins with the opening balance of cash and bank and ends with the closing balances

of cash and bank (balancing figure) at the end of the accounting period. It records all the

cash and bank transactions both of capital and revenue nature. It not only records the

cash and bank transactions relating to the current accounting period but also cash and

bank receipts (or payments) received during the current accounting period that may be

related to the previous or next accounting period.

The following are the features of Receipt and Payment Account.

1. Nature: It is a Real Account. It is a summarised version of the Cash Book.

2. Nature of Transactions: It records only cash and bank transactions. Transactions

other than cash and bank like depreciation, loss/ profit on sale of assets, etc. are not

recorded in this account.

3. No distinction between Capital and Revenue items: It records all cash and bank

receipts and payments of both capital and revenue nature.

4. Opening and closing balance: It begins with the opening balance of cash and bank

and ends with the closing balance of the cash and bank (balancing figure) at the end of

the accounting period.

5. Purpose: It reveals the cash position of an organisation. It helps to ascertain the total

amount paid and received during an accounting period.

Q5 :

Show the treatment of the following items by a Not-for-Profit Organisation:

(i) Annual subscription

(ii) Specific donation

(iii) Sale of fixed assets

(iv) Sale of old periodicals

(v) Sale of sports materials

(vi) Life membership fee

Answer :

i) Annual Subscription

a) Subscriptions received during an accounting year (whether related to the current year or

previous and subsequent year) are shown on the debit side of the Receipts and Payments

Account.

b) Subscription amount related to the current accounting year only, whether received or yet to

be received are shown on the credit side of the Income and Expenditure Account.

c) Subscriptions received in advance for the subsequent year are shown on the Liabilities side

of the Balance Sheet.

d) Subscriptions due but not received are shown in the Assets side of the Balance Sheet.

ii) Specific donation

a) The amount received for specific donation is shown on the debit side of the Receipts and

Payments Accounts.

b) The amount received for specific donation is shown on the Liabilities side of the Balance

Sheet as it is used for the specific purpose for which it is received.

iii) Sale of fixed assets

a) The amount received from the sale of fixed assets are recorded on the debit side of the

Receipts and Payments Account.

b) Profit (or loss) on the sale of fixed assets is credited (or debited) to the Income and

Expenditure Account.

c) The book-value of the fixed assets sold is deducted from its respective assets on the Assets

side of the Balance Sheet.

iv) Sale of old periodicals

a) The amount received from the sale of old periodicals are shown on the debit side of the

Receipts and Payments Account.

b) As the sale of old periodicals by any organisation is considered as revenue receipts, so it is

shown on the credit side of the Income and Expenditure Account.

v) Sale of sport Materials

a) The amount received from the sale of sport materials are debited to the Receipt and

Payments Account.

b) As the sale of sport materials by any sport club is considered as revenue income, so it is

shown on the credit side of the Income and Expenditure Account.

vi) Life Membership Fees

a) The amount paid by a person to become a member of an organisation is called life

membership fees. As this is a receipt for an NPO, so it is debited to the Receipt and Payment

Account.

b) Life Membership fees is not recurring in nature and received once for a whole life from a

member. Thus, as Life Membership Fees are capital receipts, so these are added to the Capital

Fund on the Liabilities side of the Balance Sheet.

Q6 :

Show the treatment of items of Income and Expenditure Account when there is a

specific fund for those items.

Answer :

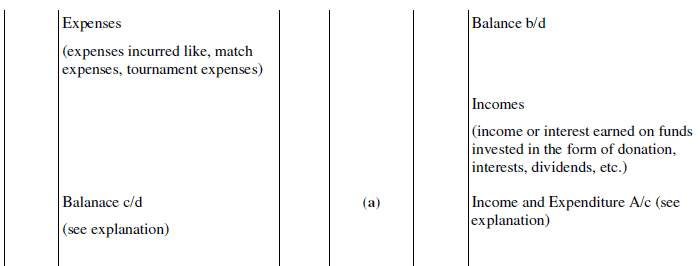

There are various sources of receipts like donations, subscriptions, government grants, etc. to an

NPO. Some receipts are specific while others are general. While the former can only be used for

the specific purpose for which they are received, the latter can be used for any purpose. For

example, if donation is received for construction of buildings, then this donation is a specific

donation and thereby can only be used for construction of the building. The specific receipts are

not considered as revenue income for the NPO and hence are not shown in the Income and

Expenditure Account. In fact, such receipts are considered as liabilities to the NPO as these

amounts are received for specific purpose and cannot be used for any other purpose. Specific

receipts are shown in the Liabilities side of the Balance Sheet, until and unless they are fully set

off against the purpose for which they are received. On the other hand, if these amounts are

invested outside the organisations (in the form of shares, debentures, etc.), then these are called

funds like, match funds, prize fund, etc. The interest and income earned on such investments are

not credited to the Income and Expenditure Account but in fact are credited to the respective

Fund Account. Similarly, the expenses incurred for such funds are not debited to the Income and

Expenditure Account but, in fact, are debited to the respective Fund Account. These special

funds are shown in the Liabilities side of the Balance Sheet. In case, if the related expenses

exceed the related receipts of the fund, then the difference is shown in the income and

Expenditure Account.

Treatment

Explanation (a)

If the receipts exceed the expenses for specific purpose then the difference between the two is

shown in the Liabilities side of the Balance Sheet

Explanation (b)

If the expenses exceed the receipts for the specific purpose then the difference between the two is

shown in the Expenditure side of the Income and Expenditure Account.

Q7 :

What is Receipt and Payment Account? How is it different from Income and Expenditure Account?

Answer :

Receipts and Payments Account is a summary of the Cash Book. All the cash receipts are

recorded on the Receipts side (i.e. Debit side) and all the cash payments are recorded on the

Payments side (i.e. Credit side) of Receipts and Payments Account. It is prepared on the basis of

cash and bank transactions recorded in the Cash Book. It begins with the opening balance of cash

and bank and ends with the closing balances of cash and bank (balancing figure) at the end of the

accounting period. It records all cash and bank transactions both of capital and revenue nature. It

not only records cash and bank transactions relating to the current accounting period, but also

cash and bank receipts (or payments) received during the current accounting period that may be

related to the previous or next accounting period.

Distinguish between Receipts and Payments Account and Income and Expenditure

Account

|

1651 videos|1645 docs|920 tests

|

FAQs on NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation - SSC CGL Tier 2 - Study Material, Online Tests, Previous Year

| 1. What is the purpose of accounting for not-for-profit organizations? |  |

| 2. How is accounting for not-for-profit organizations different from accounting for for-profit organizations? | |

| 3. What are the key financial statements prepared by not-for-profit organizations? | |

| 4. How are donations and grants accounted for in not-for-profit organizations? | |

| 5. How are expenses classified and reported in the financial statements of not-for-profit organizations? | |

Online Tests

,ppt

,practice quizzes

,Viva Questions

,Free

,video lectures

,Exam

,past year papers

,Previous Year

,mock tests for examination

,Online Tests

,study material

,NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation | SSC CGL Tier 2 - Study Material

,Online Tests

,MCQs

,Previous Year Questions with Solutions

,shortcuts and tricks

,Summary

,Previous Year

,Important questions

,NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation | SSC CGL Tier 2 - Study Material

,NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation | SSC CGL Tier 2 - Study Material

,Sample Paper

,Semester Notes

,Objective type Questions

,Extra Questions

,Previous Year

;

NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation Free PDF Download

Importance of NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation

NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation Notes

NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation SSC CGL Questions

Study NCERT Solution (Part - 4) - Accounting for Not for Profit Organisation on the App

|

© EduRev

|

Education Revolution

|

|