NCERT Solution: Accounting for Share Capital | Accountancy Class 12 - Commerce PDF Download

Short Answer Questions

Q1: What is public company?

Ans: A public company is defined as a company that offers a part of its ownership in the form of shares, debentures, bonds, securities to the general public through stock market. There must be atleast seven members to form a public company. As per the section 3 (1) (iv) of Companies Act 1956, public company means a company which:

a) is not a private company,

b) has a minimum paid up capital of Rs 5,00,000 or such higher paid up capital, as may be prescribed,

c) is a private company, being a subsidiary of a company which is not a private company.

A public company should not be mistakenly understood as a publicly-owned company, as the latter is exclusively owned and controlled by the government. A public company issues its share to general public without any restriction on maximum number of persons. A public company can be segmented into two types:

1. Listed Company- A Company whose shares are listed and traded in the stock exchange like, Tata Motors, Reliance, etc.

2. Unlisted Company- A Company whose shares are not listed in the stock exchange and thereby these shares cannot be traded in the stock exchange.

Q2: What is private limited company?

Ans: Private limited company is a company that is limited by shares or by guarantee by its members. A private limited company is defined as a company that has a minimum paid up share capital of Rs 1,00,000. As defined by the Section 3 (1) (iii) of Companies Act 1956, private limited company is defined by the following characteristics:

a) It restricts the right to transfer its shares.

b) There must be atleast two and a maximum of 50 members (excluding current and former employees) to form a private company.

c) It cannot invite application from the general public to subscribe its shares, or debentures.

d) It cannot invite or accept deposits from persons other than its members, Directors and their relatives.

Unlike public company, a private company cannot issue its shares or debentures to general public at large as shares of these companies are not traded in the stock exchange, for example, Coca-Cola India Private limited, etc.

Q3: When can shares be Forfeited?

Ans: When a shareholder fails to pay the allotment money or any subsequent calls, then the company informs the shareholder by giving him/her a proper notice.If even after the notice, the shareholder fails to pay the due money, then the company forfeits the shares allotted to him/her.

Q4: What is meant by Calls-in-Arrears?

Ans: When shareholder fails to pay all the instalments in due time, then company expects the shareholder to pay the outstanding amount in the later stages (or calls). Such amount of money that is being paid at the later stages is termed as Calls-in-Arrears.

Q5: What do you mean by a listed company?

Ans: Those public companies whose shares are listed and can be traded in a recognised stock exchange for public trading like, Tata Motors, Reliance, etc are called Listed Company. These companies are also called Quota Companies. The listing of securities (shares) helps the investor to determine the increase/decrease in value of their investment in a concerned listed company. This provides ample indication to the potential investors about the goodwill of the company and facilitates them to take various investment decisions and also to assess the viability of their investment in a company.

Q6: What are the uses of securities premium?

Ans: As per the Section 78 of the Companies Act of 1956, the amount of securities premium can be used by the company for the following activities:

1. For paying up unissued shares of the company to be issued to members (shareholders) of the company as fully paid bonus shares,

2. For writing off the preliminary expenses of the company,

3. For writing off the expenses of, or the commission paid or discount allowed on, any issue of shares or debentures of the company,

4. For paying up the premium that is to be payable on redemption of preference shares or debentures of the company.

5. Further, as per the Section 77A, the securities premium amount can also be utilised by the company to buy back its own shares.

Q7: What is meant by Calls-in-Advance?

Ans: Calls-in-Advance refers to a situation when a shareholder pays the whole amount or a part of the amount of shares before it becomes due, i.e. before the company calls for it. So, the amount of money that is being paid in advance at the earlier stages is termed as Calls-in-Advance.

Q8: Write a brief note on 'Minimum Subscription'.

Ans: When shares are issued to the general public, the minimum amount that must be subscribed by the public so that the company can allot shares to the applicants is termed as Minimum Subscription. As per the Company Act of 1956, the Minimum Subscription of share cannot be less than 90% of the issued amount. If the Minimum Subscription is not received, the company cannot allot shares to its applicants and it shall immediately refund the entire application amount received to the public.

Long Answer Questions

Q1: What is meant by the word 'Company'? Describe its characteristics.

Ans: The Section 3 (1) (i) of the Company Act of 1956 defines an organisation as a company that is formed and registered under the Act or any existing company that is formed and registered under any earlier company laws. In general, a company is an artificial person, created by law that has a separate legal entity, perpetual succession, common seal and has limited liability. It is a voluntary association of a person who together contribute to the capital of the company to do business. Generally, the capital of a company is divided into small parts known as shares, the ownership of which is transferable subject to certain terms and conditions. There are two types of companies, public companies and private companies.

Characteristics of Company

1. Association of Person: A company is formed voluntarily by a group of persons to perform a common business. Minimum number of people should be two for the formation of a private company and seven for a public company.

2. Artificial Person: A company is an artificial and juristic person that is created by law.

3. Separate Legal Entity: A company has a separate legal entity from its members (shareholders) and Directors. It can open a bank account, sign a contract and can own a property in its own name.

4. Limited Liability: The liability of the members of a company is limited up to the nominal value or the face value of the shares. Unlike a partnership firm, on insolvency of a company, the members and the shareholders are not liable to pay the amount due to the creditors of the company. In fact, the members and the shareholders are only liable to pay the unpaid amount of the shares held by them. For example, if the value of a share is Rs 10 and Rs 6 is paid up, then the member is liable to pay only Rs 4.

5. Perpetual Existence: The existence of the company is not affected by the death, retirement, and insolvency of its members. That is, the life of a company remains unaffected by the life and the tenure of its members in the company. The life of a company is infinite until it is properly wound up as per the Company Act.

6. Common Seal: The Company is an artificial person and has no physical existence; hence it cannot put its signature. Thus, the Common Seal acts as an official signature of a company that validates the official documents.

7. Transferability of Shares: The shares of public limited company is easily and freely transferable without any consent from other members. But the share of ownership of a private limited company is not transferable without the consent of the other members.

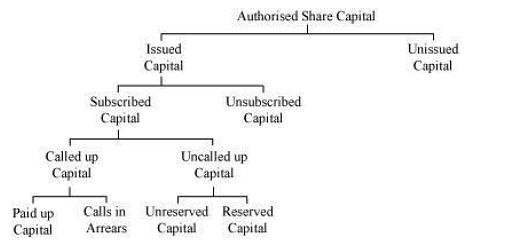

Q2: Explain in brief the main categories in which the share capital of a company is divided.

Ans: The division of the share capital of a company into main categories is diagrammatically explained below.

1. Authorised Capital: It is an amount that is stated in the Memorandum of Association. It is the maximum amount that the company can raise by issuing shares. This maximum amount can be increased as per the procedures laid down in the Company Act.

2. Issued Capital: It is a part of authorised capital which is offered by the company to the general public for subscription. For example, if the authorised capital of a company is Rs 1,00,000 divided into Rs 10 per share, then the issued capital cannot be more than Rs 1,00,000.

3. Unissued Capital: It is a part of authorised capital that is not offered till now but can be offered to the general public in future. In the above example, if the issued capital is Rs 80,000, then the unissued capital is Rs 20,000.

4. Subscribed Capital: It is a part of issued capital that is actually subscribed by the general public. For example, if the company has issued 8,000 shares of Rs 10 per share and public has subscribed for 7,500 shares, then the subscribed share capital of the company amounts to Rs 75,000.

5. Unsubscribed Capital: It is that part of the issued capital that is not subscribed by the public. For example, in the above example, 500 shares were left unsubscribed, making an unsubscribed share capital of Rs 5,000.

6. Called up Capital: It is a part of subscribed capital that is called up by the Directors from the shareholders of a company to pay. For example, if the Directors call up Rs 6 out of Rs 10 (i.e. the face value of the share) from the shareholders of 10,000 to pay, then Rs 60,000 is regarded as called up share capital.

7. Uncalled up Capital: It is that part of subscribed capital which is not called up till now but can be called up in future as per the need of the company. For example, in the above example, Rs 4 were left uncalled from shareholders holding 10,000 shares, so Rs 40,000 is uncalled up share capital.

8. Paid up capital: It is that part of called-up share capital which is actually received from the shareholders. If the entire called-up money of Rs 4 on 1,000 shares has been received except from a shareholder holding 300 shares, then the paid-up share capital is Rs 2,800 (Rs 4,000 - Rs 1,200). The amount of Rs 1,200 is called Call in Arrears that has been called up but is unpaid.

9. Reserved Capital: As per the Section 99 of the Company Act of 1956, a limited company may call up any portion of uncalled share capital in the event of winding up of the company to pay its creditors. This amount of uncalled share capital cannot be used for any other purpose and is reserved for paying back the creditors, that is why, such portion of share capital is called reserve capital.

Q3: What do you mean by the term ‘share’? Discuss the type of shares, which can be issued under the Companies Act, 2013 as amended to date.

Ans: Share is referred to as the amount of the capital which is divided into the definite value units. The people who hold such shares are called as shareholders.

Any company issues two types of shares:

i) Preference Shares: Section 85 of the Company Act,1956 defines Preference Shares to be featured by the following rights:

a. Preference Shares entitle its holder the right to receive dividends at a fixed rate or fixed amount.

b. Preference Shares entitle its holder to the preferential right to receive repayment of capital invested by them before their equity counterparts at the time of winding up of the company.

ii) Equity Shares: Equity Shareholders have a voting right and control the affairs of a company. As per Section 85 (2) of Companies Act 1956; equity share is a share that is not a preference share. It does not possess any preferential right of payment of dividend or repayment of capital. The rate of dividend is not fixed on equity shares and varies from year to year, depending upon the amount of profit available for distribution after paying dividend to the preference shareholders.

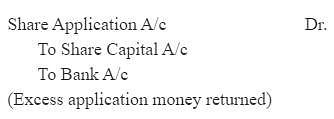

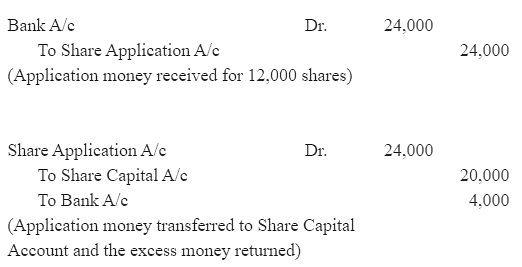

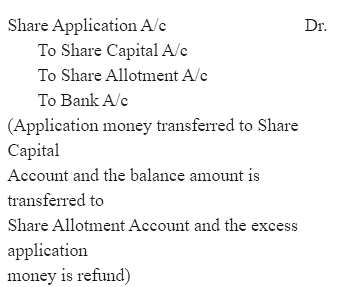

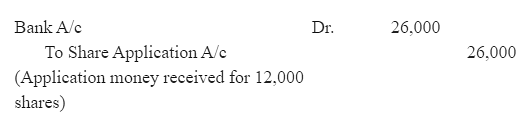

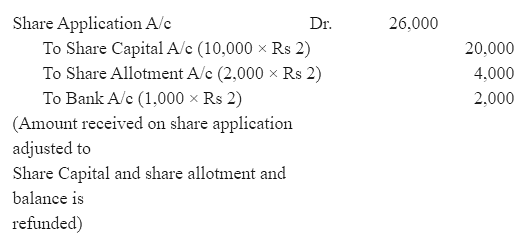

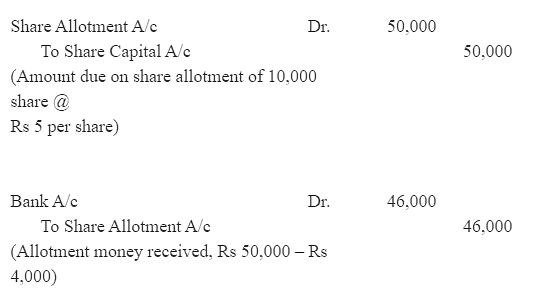

Q4: Discuss the process for the allotment of shares of a company in case of over subscription.

Ans: When the total number of applications received for shares exceeds the number of shares offered by the company to the public, the situation of oversubscription arises. A company can opt for any of the three alternatives to allot shares in case of oversubscription of shares.

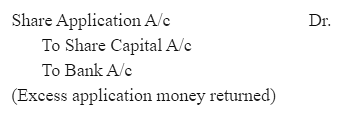

i) Excess applications are refused and money received on excess applications is returned to the applicants.

The company can refuse excess applications and the money received on these excess applications is returned to the applicants.

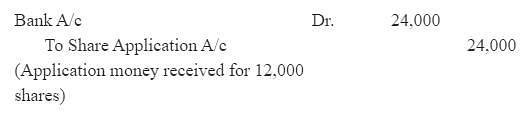

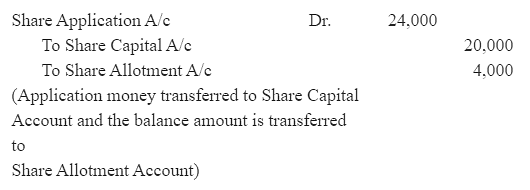

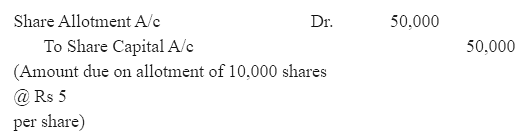

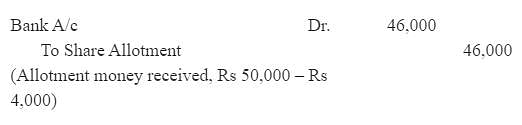

Example: Shares issued 10,000 @ Rs 10 per share and money received for 12,000 shares.

Amount is payable Rs 2 on application, Rs 5 on allotment, Rs 3 on first and final call.

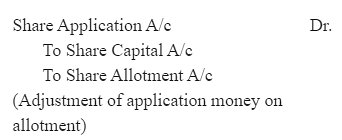

ii) Pro rata Basis

ii) Pro rata Basis

The company can allot shares on pro-rata basis to all the share applicants. The excess amount received in the application is adjusted on the allotment.

Example: Shares issued 10,000 @ Rs 10 per share and money received for 12,000 shares. Amount is payable Rs 2 on application, Rs 5 on allotment, Rs 3 on first and final call.

iii) Pro rata and refund of money

In this case, the company follows a combination of both the methods. It may reject some share applications and may allot some applications on the pro-rata basis. Example: Shares issued 10,000 @ Rs 10 per share and money received for 13,000 shares. Amount is payable Rs 2 on application, Rs 5 on allotment, Rs 3 on first and final call. If the company rejects the applications for 1,000 shares and allots the remaining on the pro-rata basis.

Example: Shares issued 10,000 @ Rs 10 per share and money received for 13,000 shares. Amount is payable Rs 2 on application, Rs 5 on allotment, Rs 3 on first and final call. If the company rejects the applications for 1,000 shares and allots the remaining on the pro-rata basis.

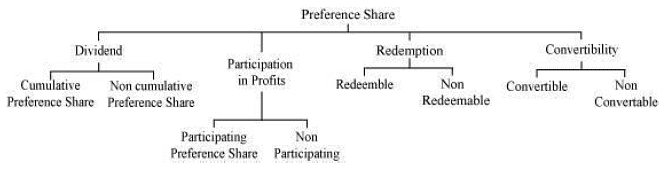

Q5: What is a 'Preference Share'? Describe the different types of preference shares.

Ans: Preference Shares: Section 85 of the Company Act,1956 defines Preference Shares to be featured by the following rights:

a. Preference Shares entitle its holder the right to receive dividend at a fixed rate or fixed amount.

b. Preference Shares entitle its holder the preferential right to receive repayment of capital invested by them before their equity counterparts at the time of winding up of the company.

Types of Preference Shares

The different types of Preference Shares are diagrammatically explained below.

1. On the basis of Dividend:

a) Cumulative Preference Shares

When a preference shareholder has a right to recover any arrears of dividend, before any dividend is paid to the equity shareholders, then the type of Preference Shares held by the shareholder is known as Cumulative Preference Shares. All Preference Shares are cumulative unless otherwise expressly stated to be non-cumulative.

b) Non Cumulative Preference Share

When a preference shareholder receives dividend only in case of profit and is not entitled to any right to recover the arrears of dividend, then the type of Preference Shares held by the shareholder is known as Non Cumulative Preference Shares.

2. On the basis of Participation:

a) Participating Preference Share

When a preference shareholder enjoys the right to participate in the surplus profit (in addition to the fixed rate of dividend) that is left after the payment of dividends to the equity shareholders, the type of shares held by the shareholder is known as Participating Preference Share.

b) Non participating Preference Share

When a preference shareholder receives only a fixed rate of dividend every year and do not enjoy the additional participation in the surplus profit, then the type of shares held by the shareholder is known as Non-Participating Preference Shares.

It must be noted that all Preference Shares are non-participating until and unless expressly stated.

3. On the basis of Redemption:

a) Redeemable preference share

When a preference shareholder is repaid by the company after a certain specified period in accordance with the term specified in Section 80 of Company Act of 1956, then the type of the shares held by him/her is known as Redeemable Preference Shares.

b) Non Redeemable Preference share

These shares are not repaid by the company during its lifetime. As per the Section 80A of the Company Act of 1956, no company can issue Non Redeemable Preference Shares. It is merely a theoretical concept.

4. On the basis of Convertibility:

a) Convertible Preference Share

The shareholders holding Convertible Preference Shares have a right to convert his/her shares into equity shares.

b) Non Convertible Preference Share

Unlike Convertible Preference Shares, the shareholders holding Non-Convertible Preference Shares do not enjoy the right to convert their shares into equity shares.

Q6: Describe the provision of law relating to 'Calls-in-Arrears' and 'Calls-in-Advance'.

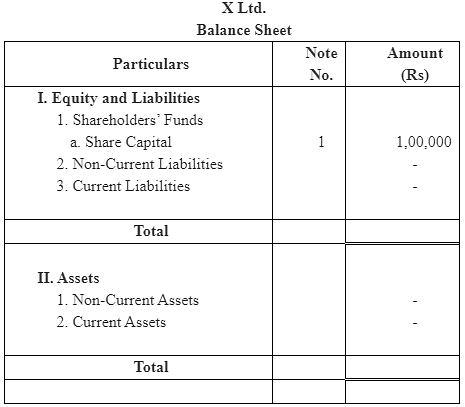

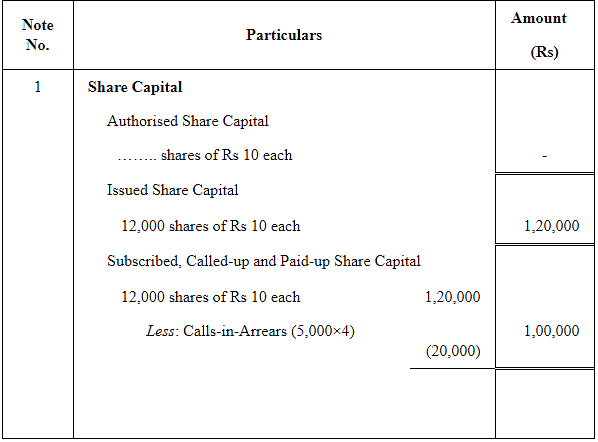

Ans: Calls-in-Arrears: When a shareholder fails to pay the amount due on allotment or any subsequent calls, then it is termed as Calls-in-Arrears. The Company is authorised by its Article of Association to charge interest at a specified rate on the amount of Call in Arrears from the due date till the date of payment. If the Article of Association is silent in this regard, then Table A shall be applicable that is interest at 5% p.a. is charged from the shareholders. As per the Revised Schedule VI of the Companies Act, Calls-in-Arrears are deducted from the Called-up Share Capital in the Notes to Accounts (that is prepared outside the Balance Sheet) under the head 'Share Capital'. The final amount of Share Capital is shown on the Equity and Liabilities side of the Company's Balance Sheet. The company can also forfeit the shares on account of nonpayment of the calls money after giving proper notice to the shareholders.

Example- X Ltd. issued 12,000 shares of Rs 10 each. All the shares were duly subscribed, however, the first and final call of Rs 4 on 5,000 shares remained unpaid.

Notes to Accounts

Calls-in-Advance: When a shareholder pays the whole amount or a part of the amount in advance, i.e. before the company calls, then it is termed as Calls-in-Advance. The company is authorised by its Article of Association to pay interest at the specified rate on call in advance from the date of payment till the date of call made. If the Article of Association is silent in this regard, then the Table A shall be applicable that is, interest at 6% p.a. is provided to the shareholders. As per the Revised Schedule VI of the Companies Act, Calls-in-Advance (along with interest on it) is added to the 'Other Current Liabilities' in the Notes to Accounts. The final amount of Other Current Liabilities is shown under the main head of 'Current Liabilities' on the Equity and Liabilities side of the Company's Balance Sheet.

Example- X Ltd. issued 12,000 shares of Rs 10 each. All the shares were duly subscribed. The final call of Rs 3 was not yet made, however, a shareholder holding 5,000 shares paid the final call instalment in advance along with the allotment money.

Notes to Accounts

Q7: Explain the terms 'Over-subscription' and 'Under-subscription'. How are they dealt with in accounting records?

Ans: When the total number of applications received for shares exceeds the number of shares offered by the company to the public, the situation of Over-subscription arises. A company can opt for any of the three alternatives to allot shares in case of Over-subscription of shares.

i) Excess applications are refused and money received on excess applications is returned to the applicants.

The company can refuse excess applications and the money received on these excess applications is returned to the applicants.

Example: Shares issued 10,000 @ Rs 10 per share and money received for 12,000 shares. Amount is payable Rs 2 on application, Rs 5 on allotment, Rs 3 on first and final call.

ii) Pro rata Basis

The company can allot shares on pro-rata basis to all the share applicants. The excess amount received in the application is adjusted on the allotment.

Example: Shares issued 10,000 @ Rs 10 per share and money received for 12,000 shares. Amount is payable Rs 2 on application, Rs 5 on allotment, Rs 3 on first and final call.

iii) Pro rata and refund of money

In this case, the company follows a combination of both methods. It may reject some share applications and may allot some applications on the pro-rata basis.

Example: Shares issued 10,000 @ Rs 10 per share and money received for 13,000 shares. Amount is payable Rs 2 on application, Rs 5 on allotment, Rs 3 on first and final call. If the company rejects the applications for 1,000 shares and allots the remaining on the pro rata basis.

Under-subscription- When the number of shares applied by the public is lesser than the number of shares issued by the company, then the situation of Under-subscription arises. As per the Company Act, the Minimum Subscription is 90% of the shares issued by the company. This implies that the company can allot shares to the applicants provided if applications for 90% of the issued shares are received. Otherwise, the company should refund the entire application amount received. In this regard, necessary Journal entry is passed only after receiving and refunding of the application money.

Q8: Describe the purposes for which a company can use 'Securities Premium Account'.

Ans: As per the Section 78 of the Companies Act of 1956, the amount of securities premium can be used by the company for the following activities:

1. For paying up unissued shares of the company to be issued to members (shareholders) of the company as fully paid bonus share,

2. For writing off the preliminary expenses of the company,

3. For writing off the expenses of, or the commission paid or discount allowed on, any issue of shares or debentures of the company,

4. For paying up the premium that is to be payable on redemption of preference shares or debentures of the company.

5. Further, as per the Section 77A, the securities premium amount can also be utilised by the company to Buy-back its own shares.

Q9: State clearly the conditions under which a company can issue shares at a discount.

Ans: As per the Section 79 of the Company Act of 1956, following are the conditions under which a company can issue shares at a discount.

- A company can issue shares at discount provided it has previously issued such type of shares.

- The issue of shares at a discount is authorised by a resolution passed by the company in the General Meeting and sanction obtained from the Company Law Tribunal.

- The resolution specifies that the maximum rate of discount is 10% of the face value of the shares unless a higher percentage of discount is allowed by the Company Law Tribunal.

- A company can issue shares at a discount at least after one year from the date of commencing business.

- If a company wants to issue shares at a discount, then it must issue them within two months of obtaining sanction from the Company Law Tribunal.

- Every prospectus related to the issue of the shares should explicitly and clearly contain particulars of the discount allowed on the issue of shares.

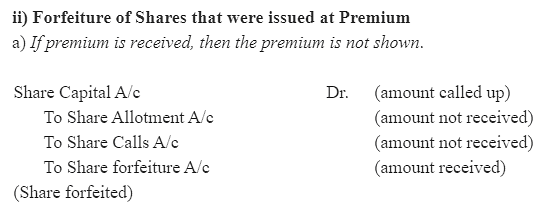

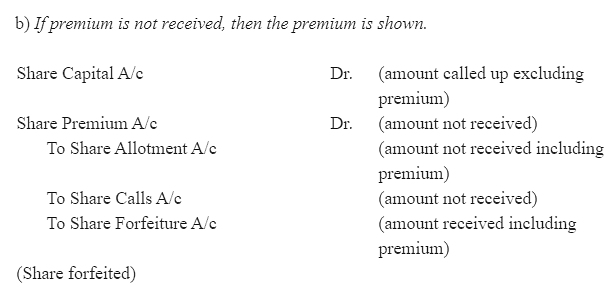

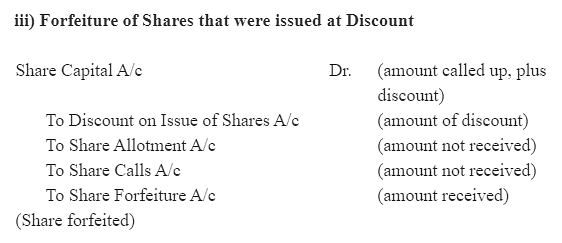

Q10: Explain the term 'Forfeiture of Shares' and give the accounting treatment on forfeiture.

Ans: If a shareholder fails to pay the allotment money and/or any subsequent calls, then the company has the right to forfeit shares by giving proper notice to the shareholder.

As per the Table A of the Company Act, the procedure of forfeiting shares is mentioned below.

1. A notice is sent to the default shareholder stating him/her to pay Calls in Arrears along with the interest accrued on the outstanding calls money within a period of 14 days of the receipt of notice, otherwise, the shares will be forfeited.

2. If the shareholder does not pay the amount, then the company has the right to forfeit his/her share by passing a resolution.

3. A notice of that resolution is sent to the default shareholder and a public notice of the same is published in a daily newspaper.

4. The name of the shareholder is removed from the register of members (i.e. shareholders).

Accounting Treatment for Forfeiture of Shares:

Numerical Questions

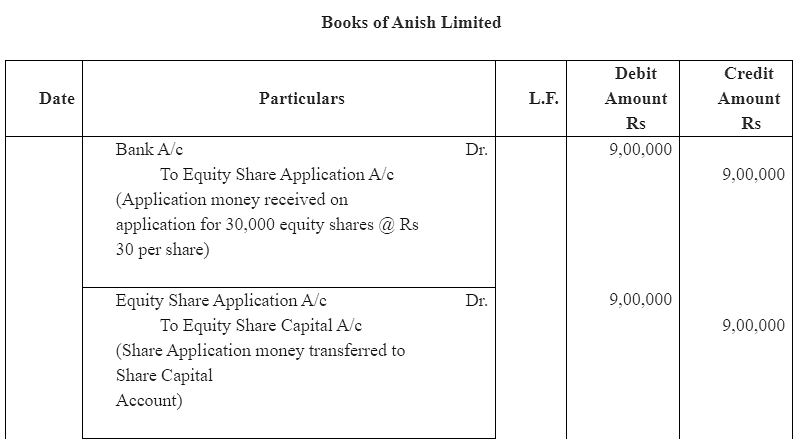

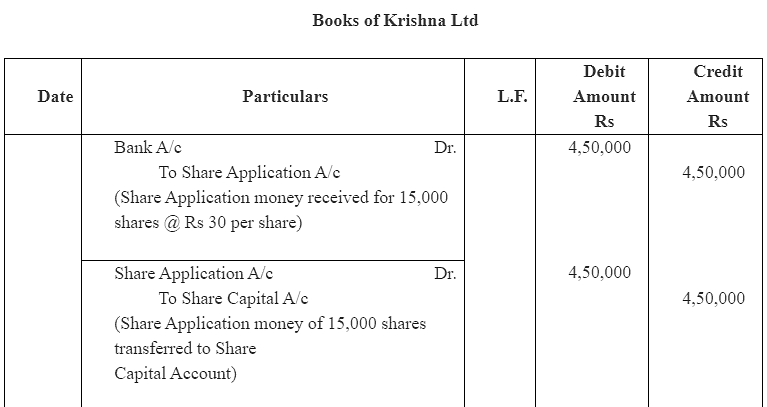

Q1: Anish Limited issued 30,000 equity shares of Rs 100 each payable at Rs 30 on application, Rs 50 on allotment and Rs 20 on Ist and final call. All money was duly received. Record these transactions in the journal of the company.

Ans:

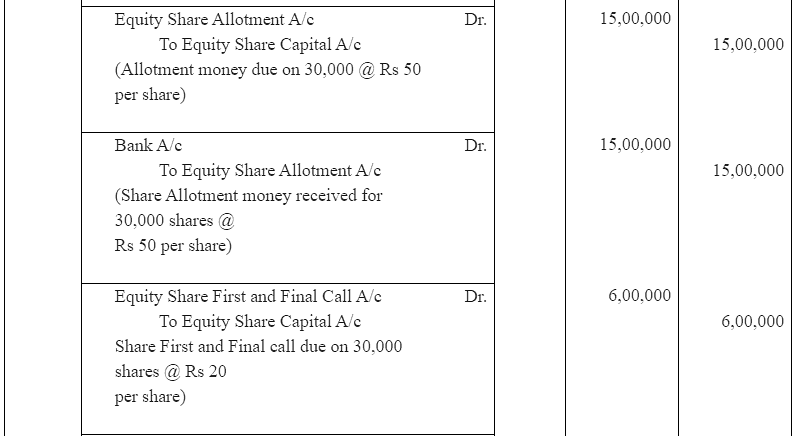

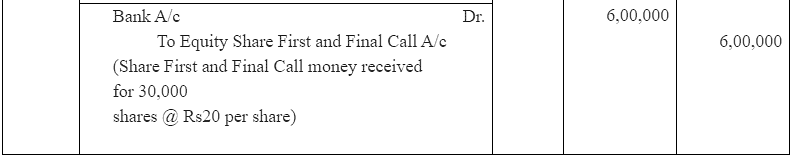

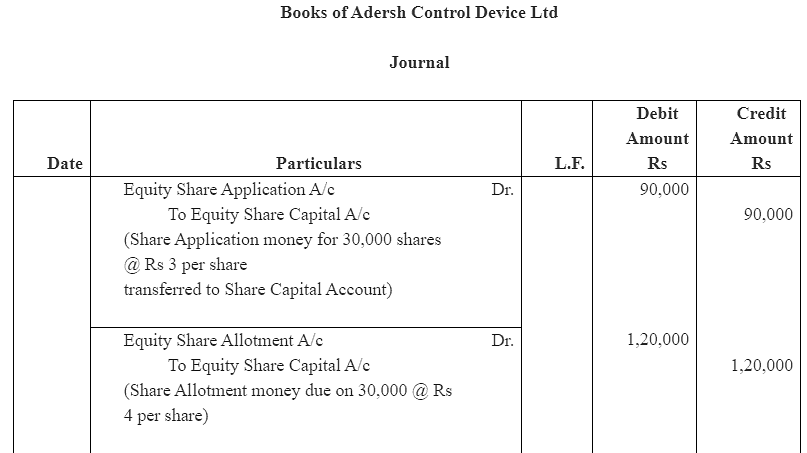

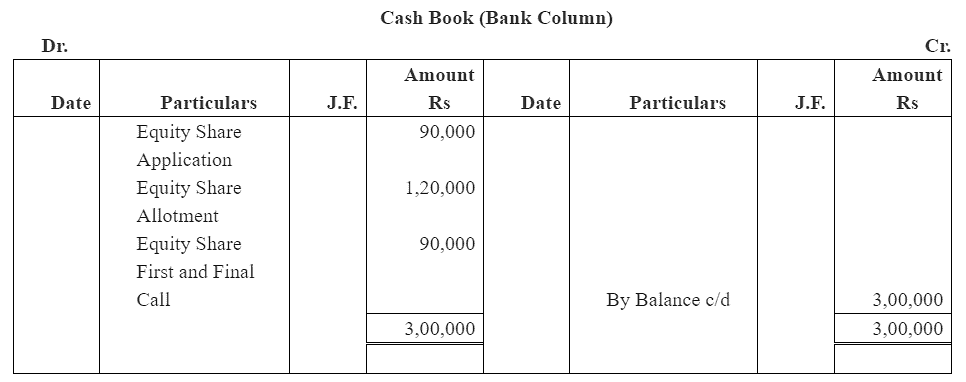

Q2: The Adersh Control Device Ltd was registered with the authorised capital of Rs 3,00,000 divided into 30,000 shares of Rs 10 each, which were offered to the public. Amount payable as Rs. 3 per share on application, Rs 4 per share on allotment and Rs 3 per share on first and final call. These share were fully subscribed and all money was dully received. Prepare journal and Cash Book.

Ans:

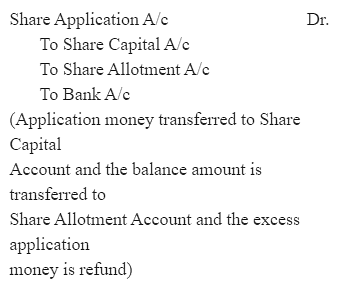

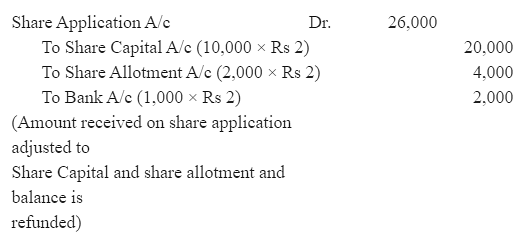

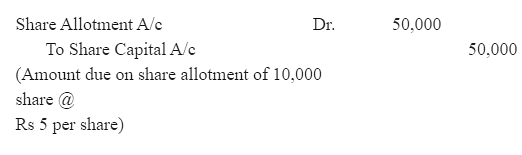

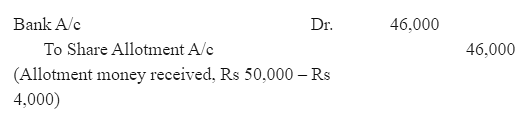

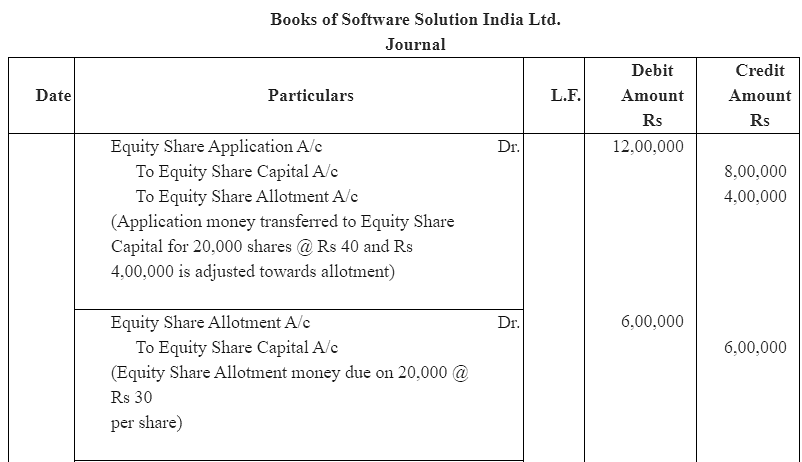

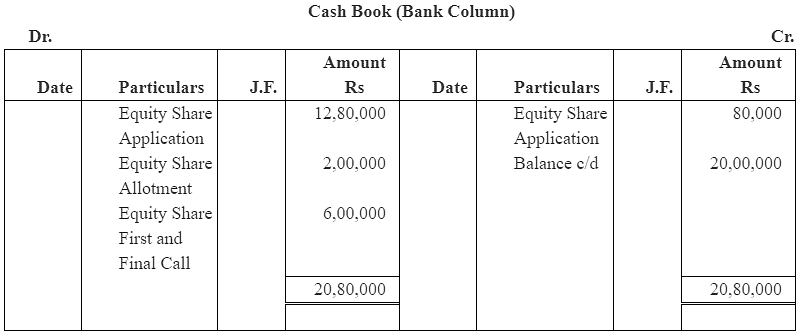

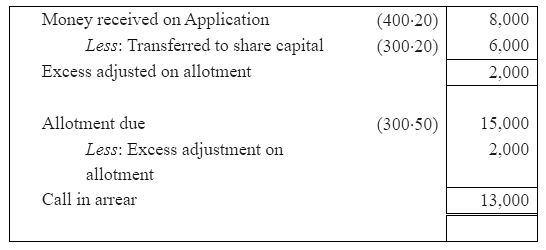

Q3: Software solution India Ltd inviting application for 20,000 equity share of Rs 100 each, payable Rs 40 on application, Rs 30 on allotment and Rs 30 on call. The company received applications for 32,000 shares. Application for 2,000 shares were rejected and money returned to Applicants. Applications for 10,000 shares were accepted in full and applicants for 20,000 share allotted half of the number of share applied and excess application money adjusted into allotment. All money received due on allotment and call. Prepare journal and cash book.

Ans:

Working Note:

Working Note:

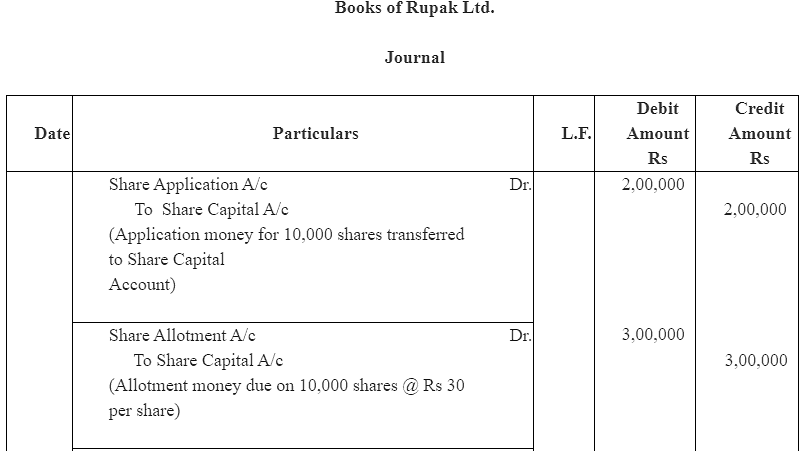

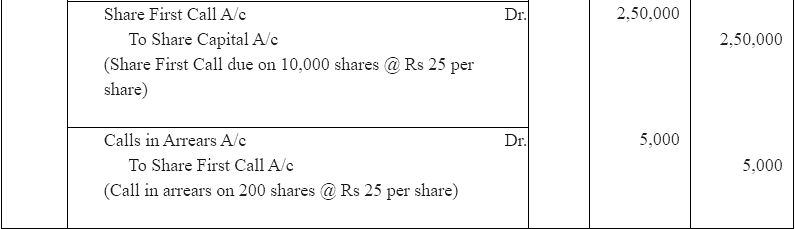

Q4: Rupak Ltd. issued 10,000 shares of Rs 100 each payable Rs 20 per share on application, Rs 30 per share on allotment and balance in two calls of Rs 25 per share. The application and allotment money were duly received. On first call all member pays their dues except one member holding 200 shares, while another member holding 500 shares paid for the balance due in full. Final call was not made. Give journal entries and prepare cash book.

Ans:

Working Note:

Working Note:

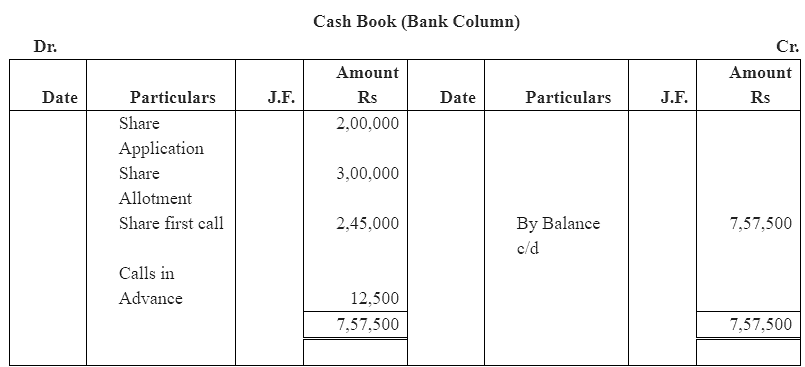

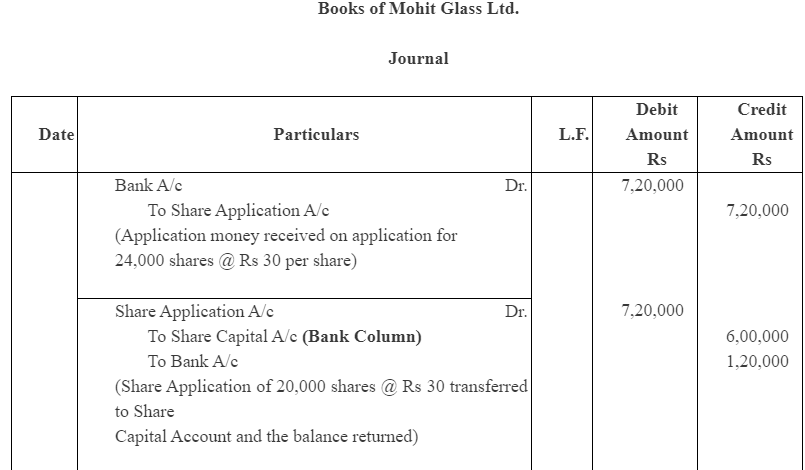

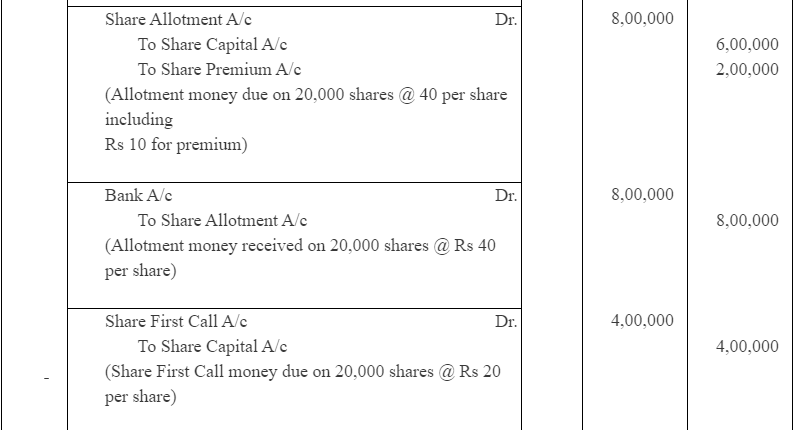

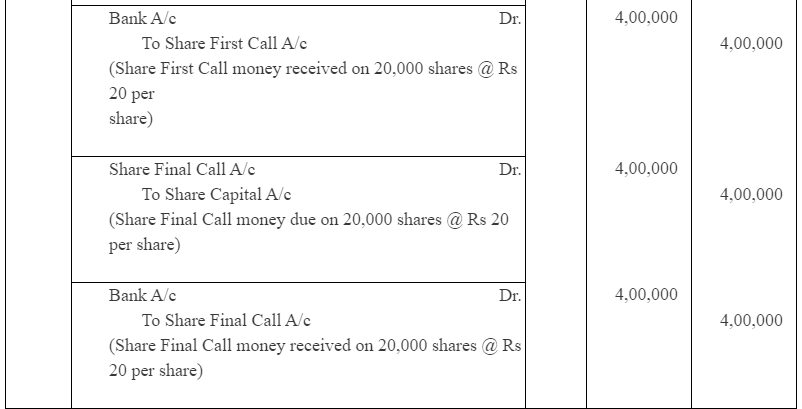

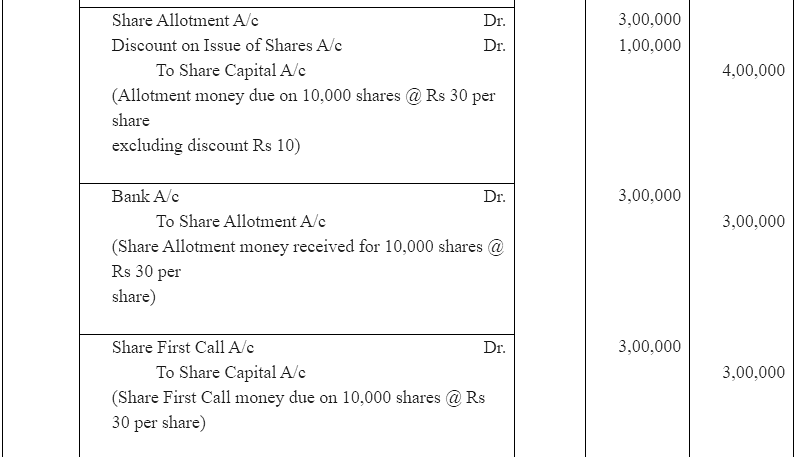

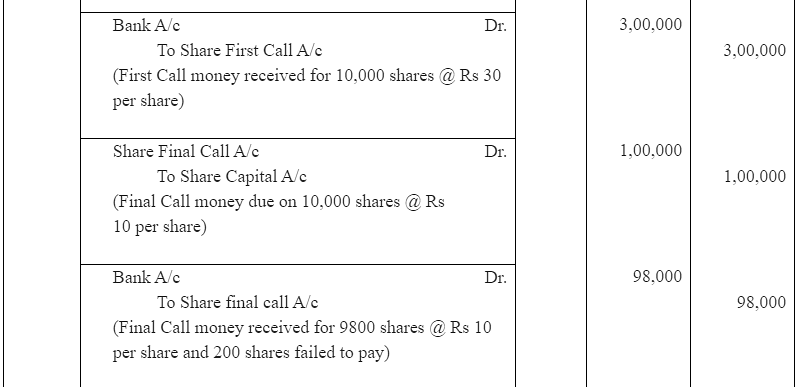

Q5: Mohit Glass Ltd. issued 20,000 shares of Rs 100 each at Rs 110 per share, payable Rs 30 on application, Rs 40 on allotment (including Premium), Rs 20 on first call and Rs 20 on final call. The applications were received for 24,000 shares and allotted 20,000 shares and reject 4,000 shares and amount returned thereon. The money was duly received. Give journal entries.

Ans:

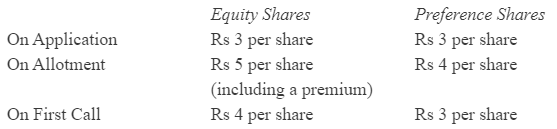

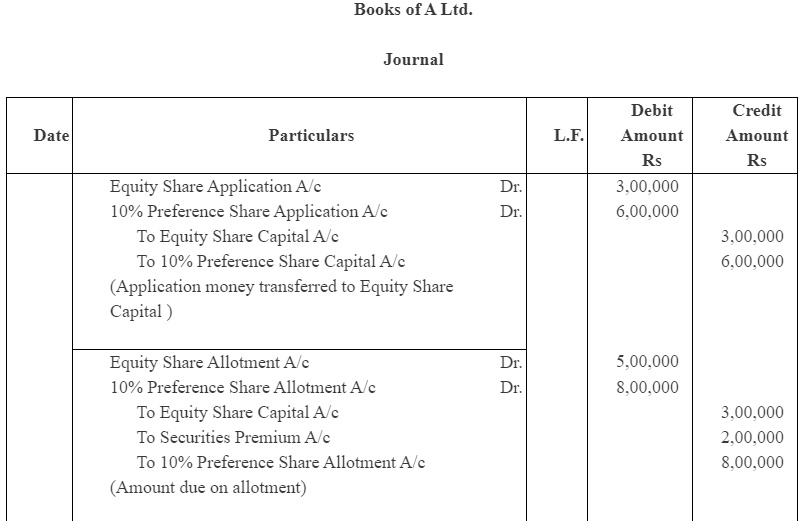

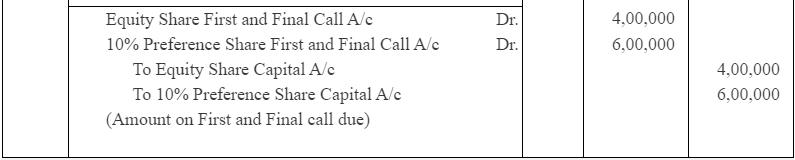

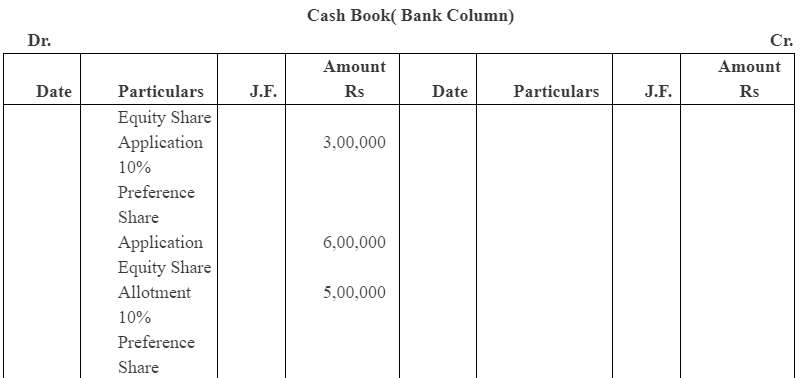

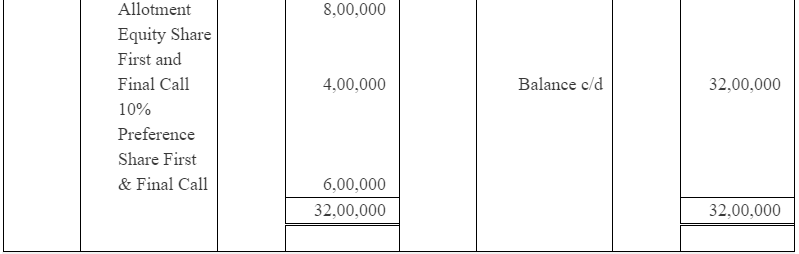

Q6: A limited company offered for subscription of 1,00,000 equity shares of Rs 10 each at a premium of Rs 2 per share. 2,00,000. 10% Preference shares of Rs 10 each at par.

The amount on share was payable as under :

All the shares were fully subscribed, called-up and paid.

Record these transactions in the journal and cash book of the company:

Ans:

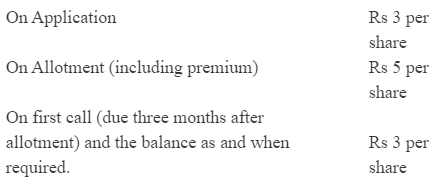

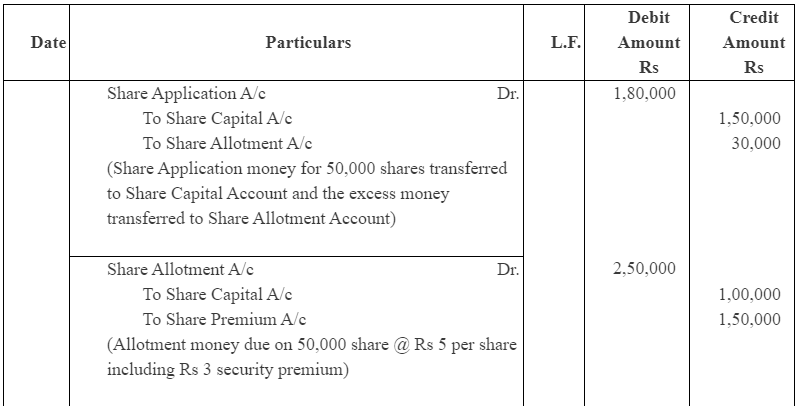

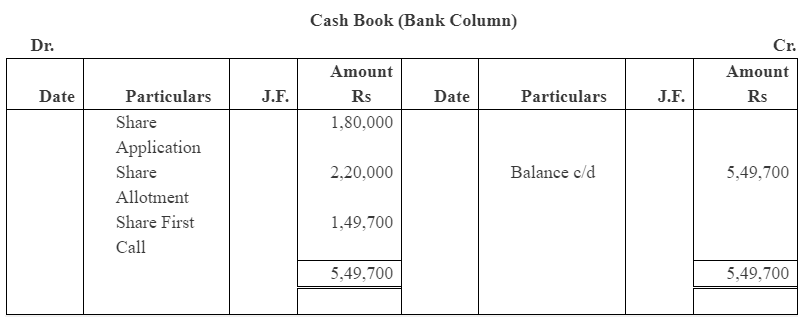

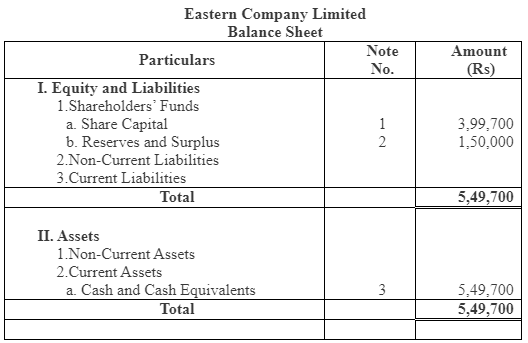

Q7: Eastern Company Limited, having an authorised capital of Rs 10,00,000 in shares of Rs 10 each, issued 50,000 shares at a premium of Rs 3 per share payable as follows :

Applications were received for 60,000 shares and the directors allotted the shares as follows:

(a) Applicants for 40,000 shares received shares, in full.

(b) Applicants for 15,000 shares received an allotment of 8,000 shares.

(c) Applicants for 500 shares received 200 shares on the allotment, with excess money being returned.

All amounts due on allotment were received.

The first call was duly made and the money was received with the exception of the call due on 100 shares.

Give journal and cash book entries to record these transactions of the company. Also, prepare the Balance Sheet of the company.

Ans:

To solve this question, applicants of category C have been assumed as 5000 instead of 500 and allotment to the applicants of this category has been taken as 2000 in place of 200.

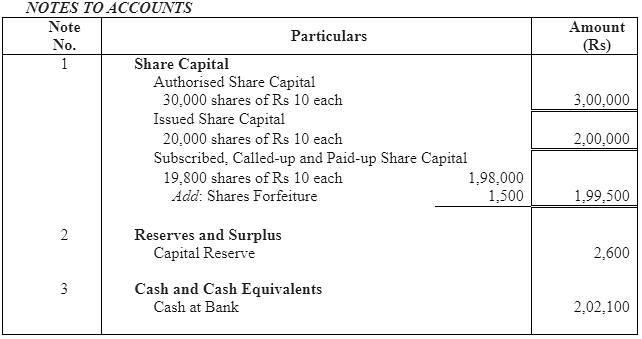

Notes To Accounts

Notes To Accounts

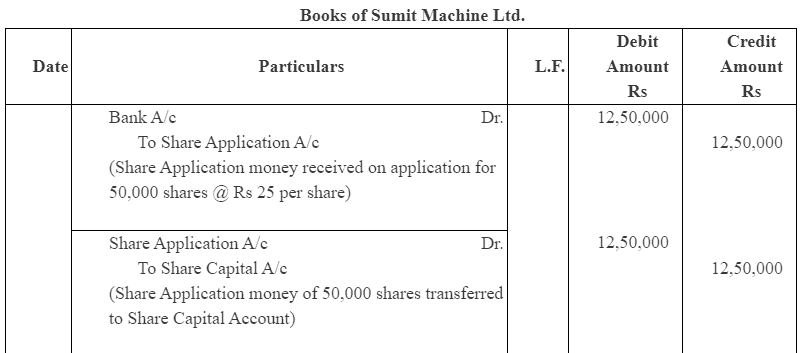

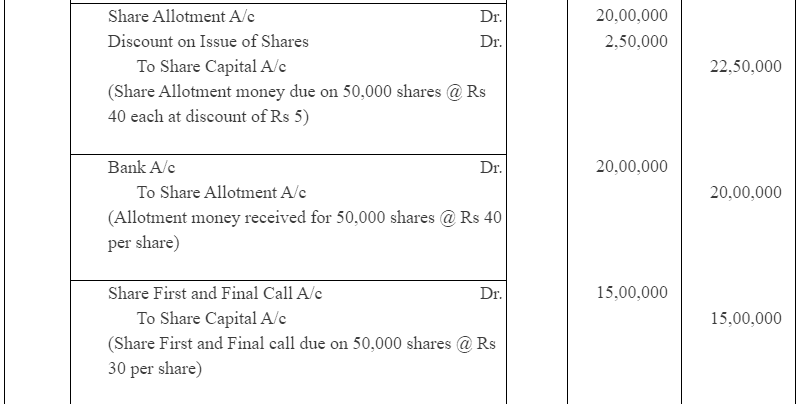

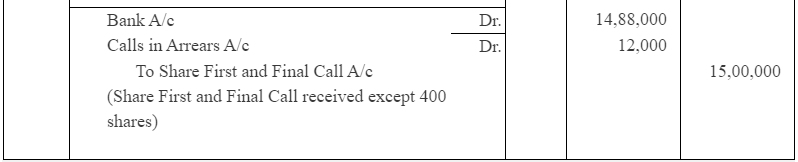

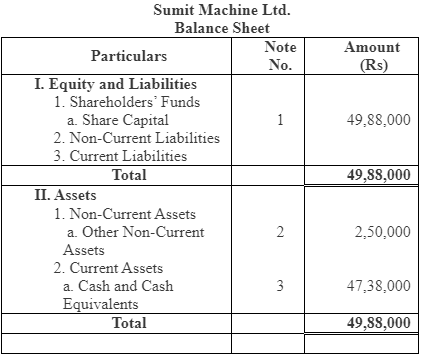

Q8: Sumit Machine Ltd issued 50,000 shares of Rs 100 each at discount of 5%. The shares were payable Rs 25 on application, Rs 40 on allotment and Rs 30 on first and final call. The issue were fully subscribed and money were duly received except the final call on 400 shares. The discount was adjusted on allotment. Give journal entries and prepare balance sheet.

Ans:

Notes to Accounts

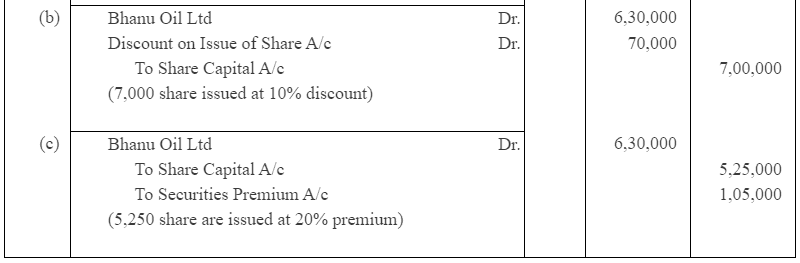

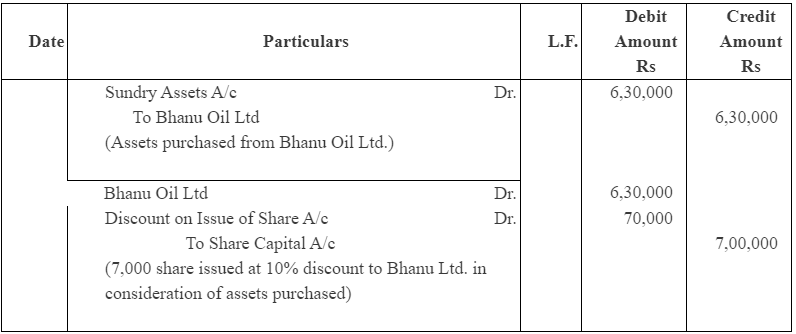

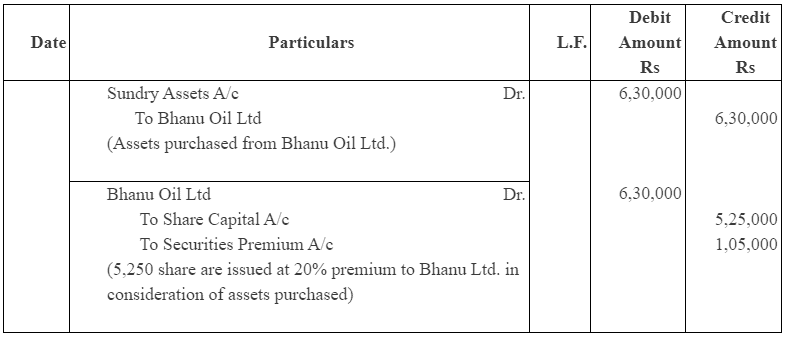

Q9: Kumar Ltd purchases assets of Rs 6,30,000 from Bhanu Oil Ltd. Kumar Ltd. issued equity share of Rs 100 each fully paid in consideration. What journal entries will be made, if the share are issued,

(a) at par,

(b) at discount of 10 % and

(c) at premium of 20%.

Ans:

Case (a)

No. of Shares issued of at par = (Amount payable over /Face Value)

6,300 Shares= {6,30,000/ 100})

Case (b)

No. of Shares issued of at par =

7,000 Shares = ;

Case (c)

No. of Shares issued of at par =

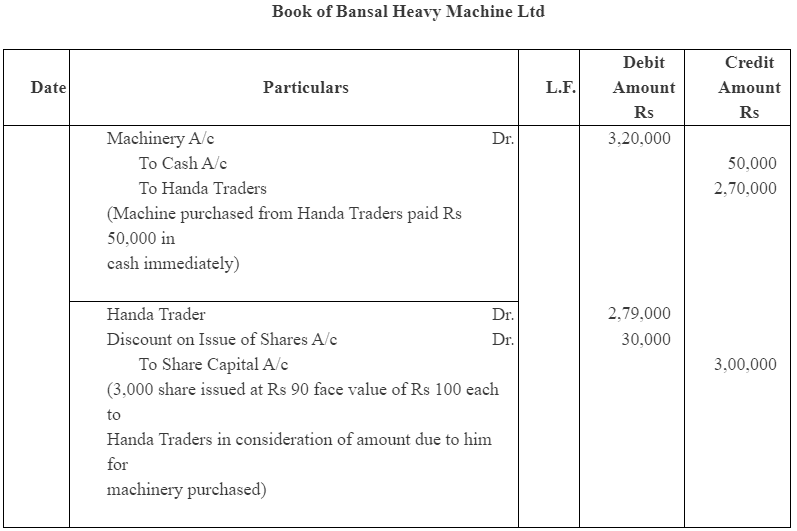

Q10: Bansal Heavy machine Ltd purchased machine worth Rs 3,20,000 from Handa Trader. Payment was made as Rs 50,000 cash and remaining amount by issue of equity share of the face value of Rs 100 each fully paid at an issue price of Rs 90 each. Give journal entries to record the above transaction.

Ans:

Working Notes:-

1. Number of shares issued

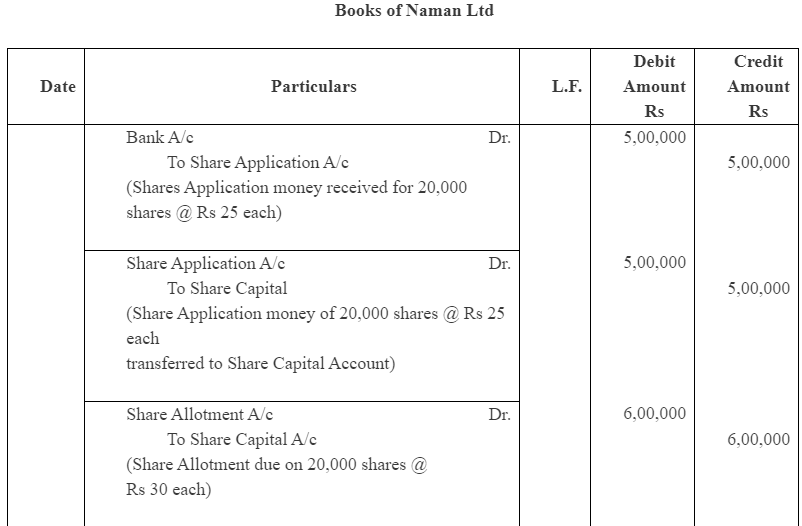

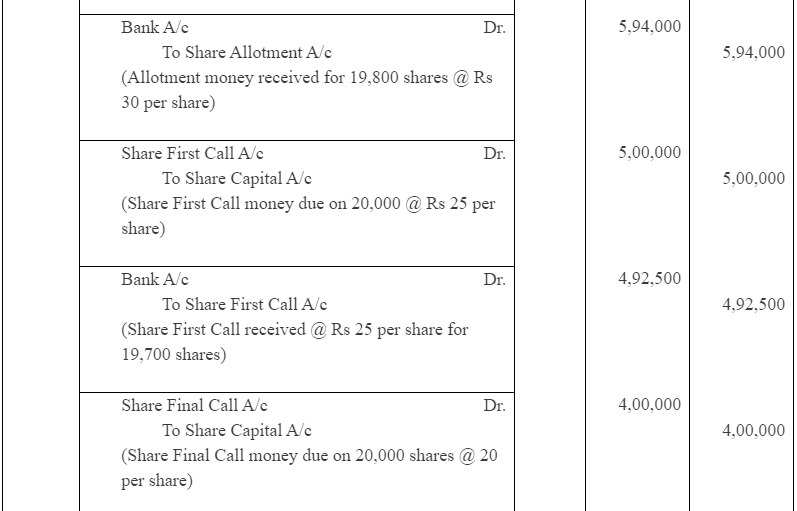

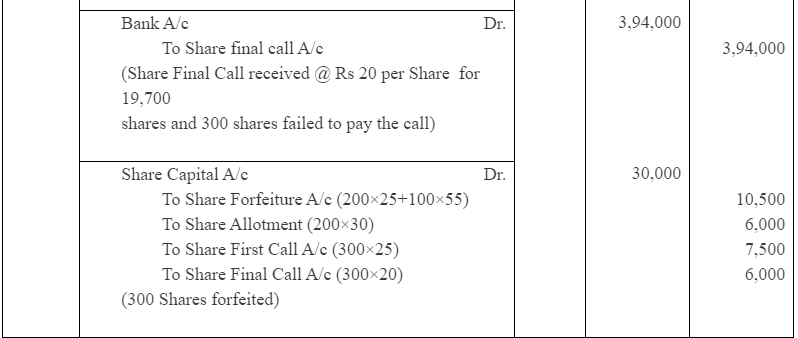

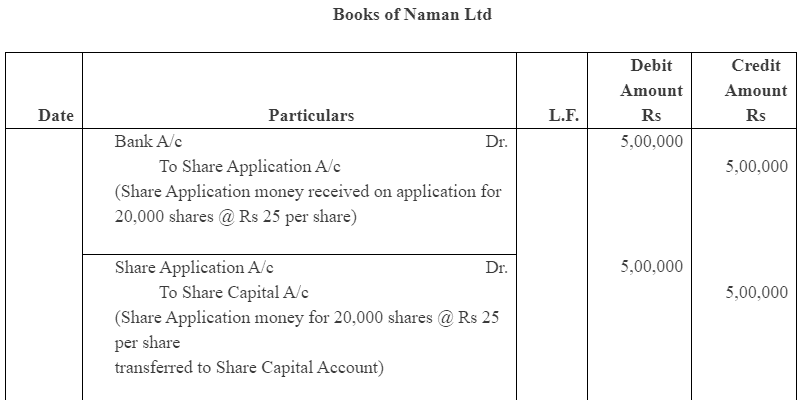

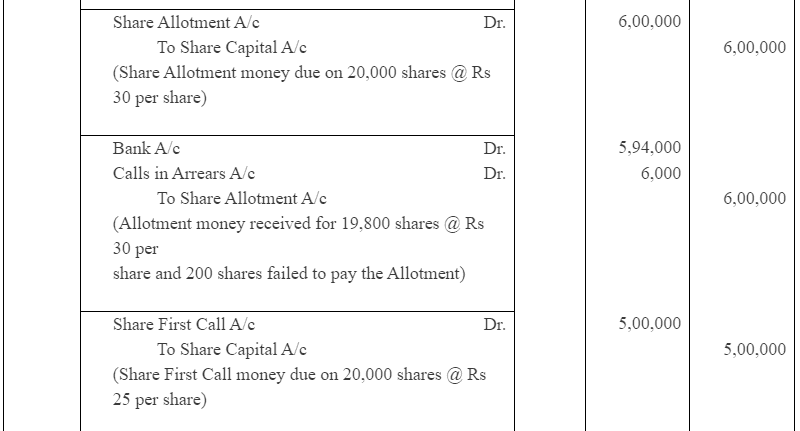

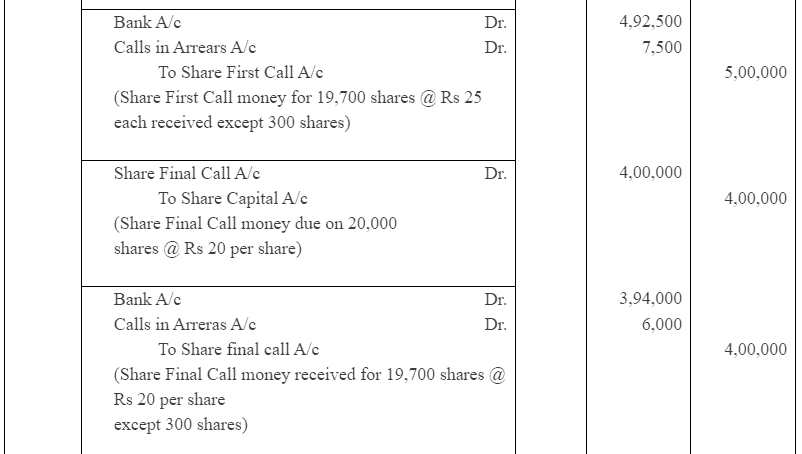

Q11: Naman Ltd issued 20,000 shares of Rs 100 each, payable Rs 25 on application, Rs 30 on allotment , Rs 25 on first call and The balance on final call. All money duly received except Anubha, who holding 200 shares did not pay allotment and calls money and Kumkum, who holding 100 shares did not pay both the calls. The directors forfeited shares of Anubha and kumkum.

Give journal entries.

Ans:

Alternatively, this question can be solved by debiting Calls in Arrears Account.

Working Note:

1. Forfeited Amount

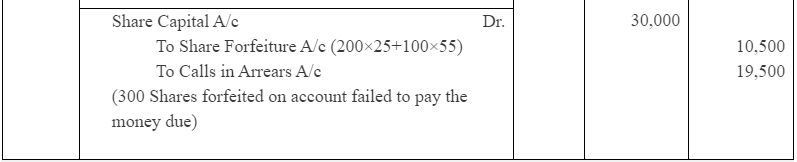

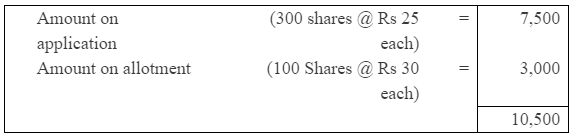

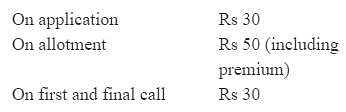

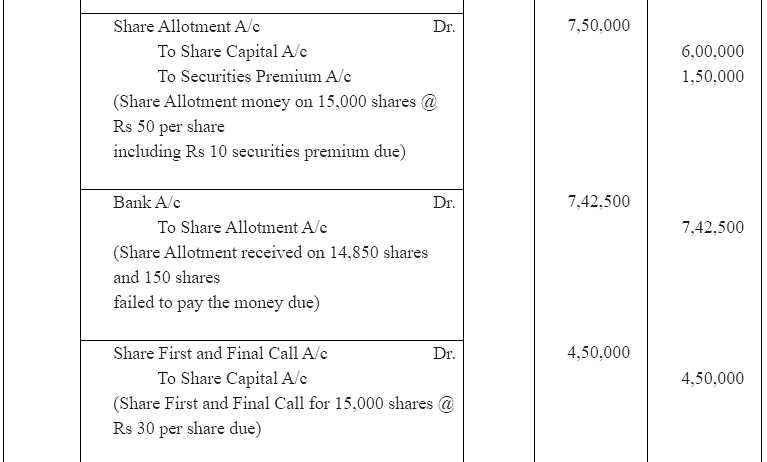

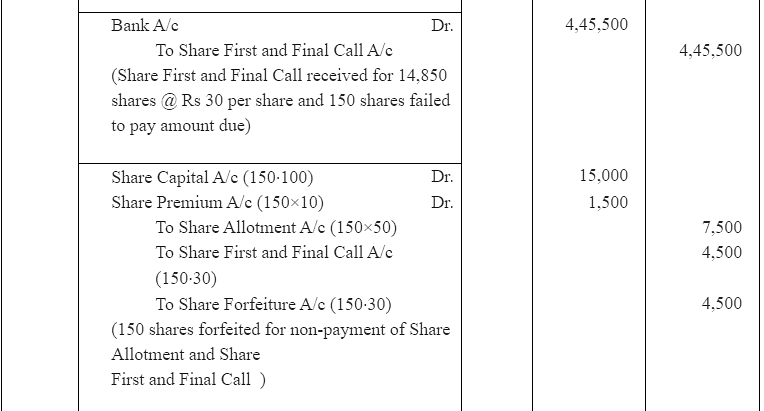

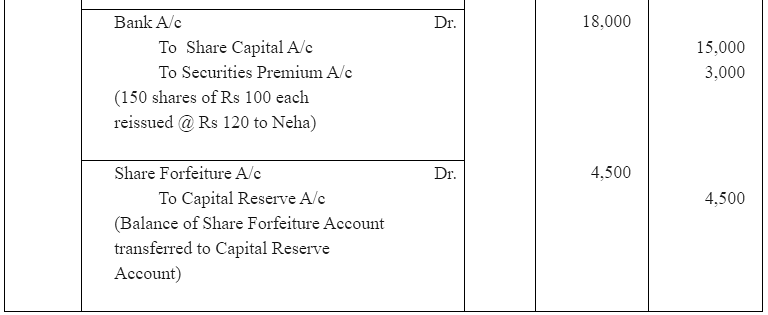

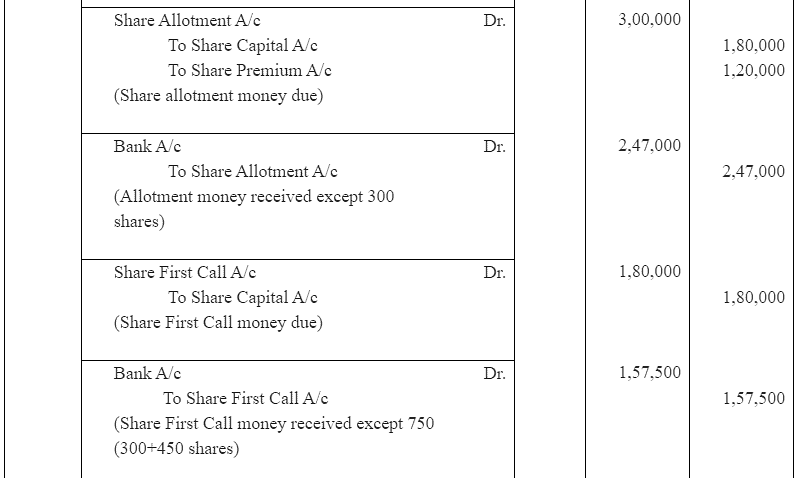

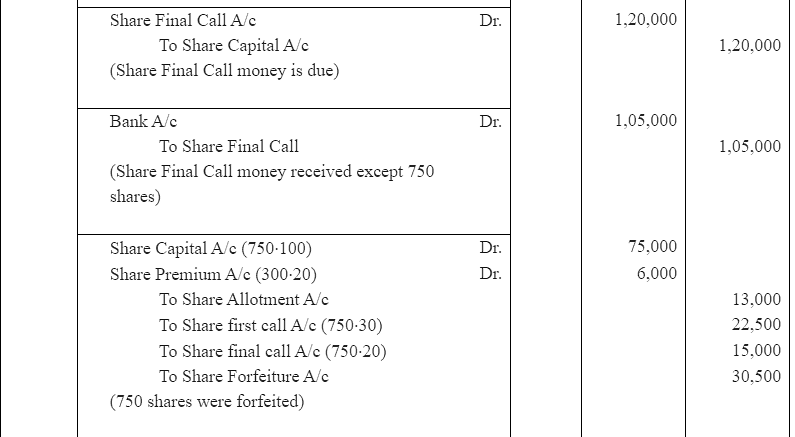

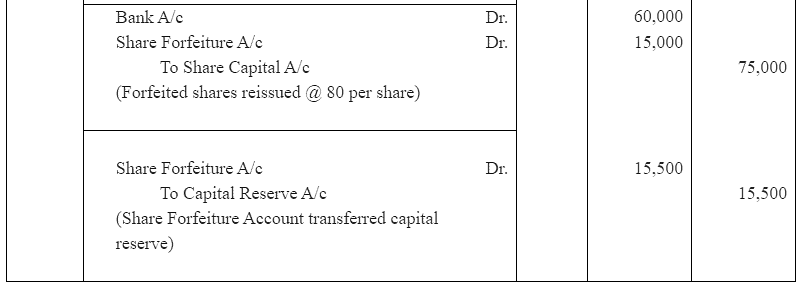

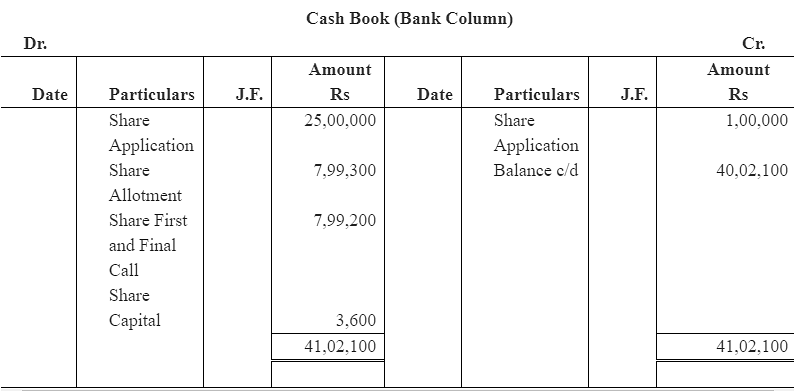

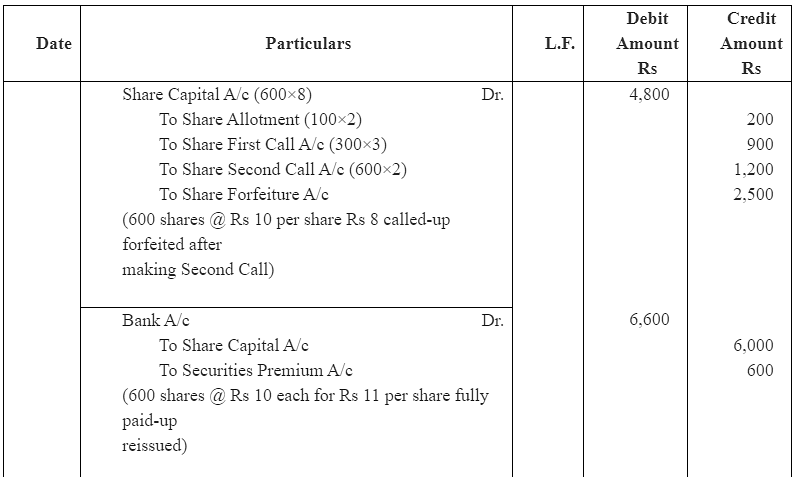

Q 12: Kishna Ltd issued 15,000 shares of Rs 100 each at a premium of Rs 10 per share, payable as follows:

All the shares subscribed and the company received all the money due, With the exception of the allotment and call money on 150 shares. These shares were forfeited and reissued to Neha as fully paid share of Rs 12 each.

Give journal entries in the books of the company.

Ans:

Note: In the solution, the reissued price of Rs 12 has been assumed as Rs 120 per share.

Note: In the solution, the reissued price of Rs 12 has been assumed as Rs 120 per share.

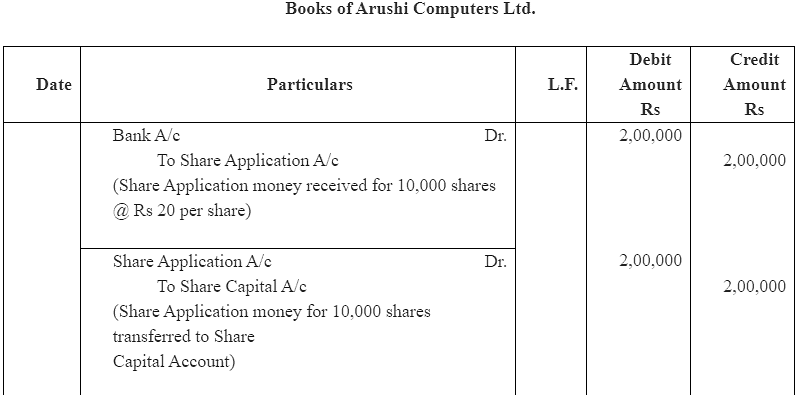

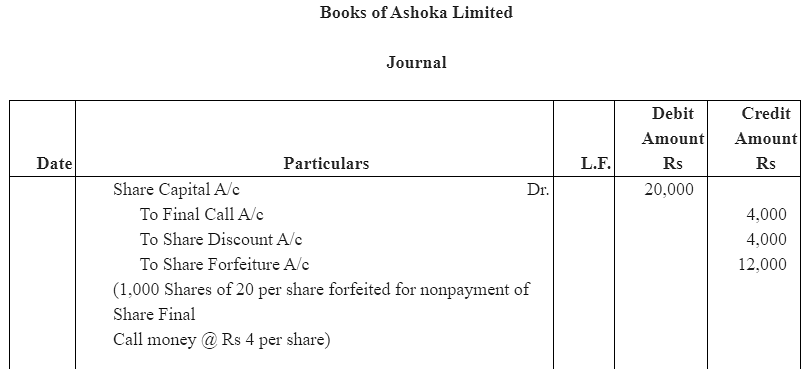

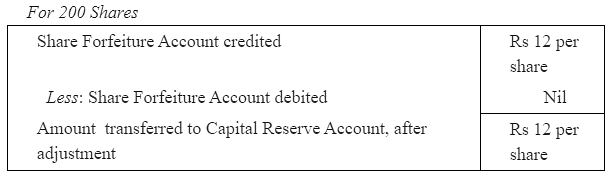

Q13: Arushi Computers Ltd issued 10,000 equity shares of Rs 100 each at 10% discount. The net amount payable as follows:

A shareholder holding 200 shares did not pay final call. His shares were forfeited. Out of these 150 shares were reissued to Ms. Sonia at Rs 75 per shares. Give Journal entries in the books of the company.

Ans:

Working Notes:

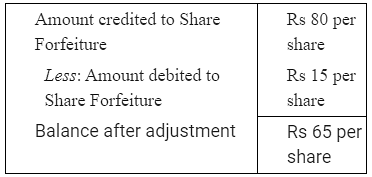

Working Notes:

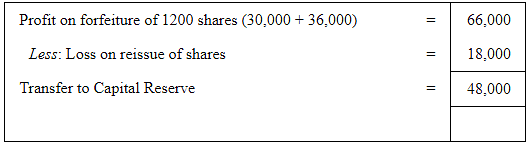

Amount Transferred to Capital Reserve A/c

Amount transferred to Capital Reserve Account = Balance per share after adjustment × Number of shares reissued Rs 9,750 = Rs 65 × Rs 150 per share

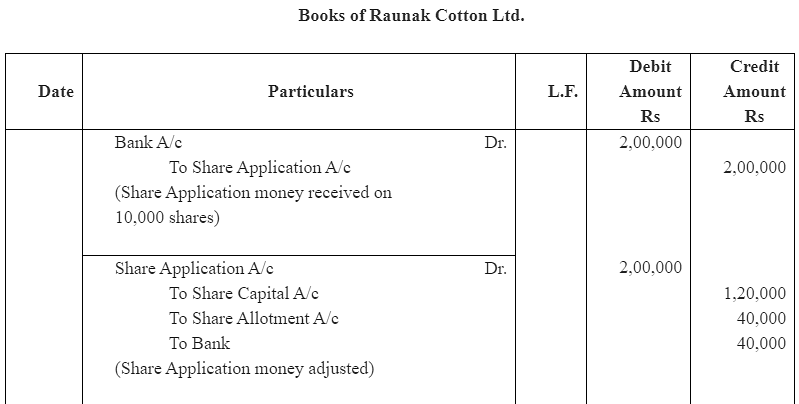

Q14: Raunak Cotton Ltd. issued a prospectus inviting applications for 6,000 equity shares of Rs 100 each at a premium of Rs 20 per shares, payable as follows:

Applications were received for 10,000 shares and allotment was made Pro-rata to the applicants of 8,000 shares, the remaining applications Being refused. Money received in excess on the application was adjusted toward the amount due on allotment.

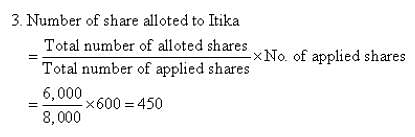

Rohit, to whom 300 shares were allotted failed to pay allotment and calls money, his shares were forfeited. Itika, who applied for 600 shares, failed to pay the two calls and her share were also forfeited. All these shares were sold to Kartika as fully paid for Rs 80 per shares.

Give journal entries in the books of the company.

Ans:

2. Call in arrears by Rohit on allotment

4. Share Forfeiture amount

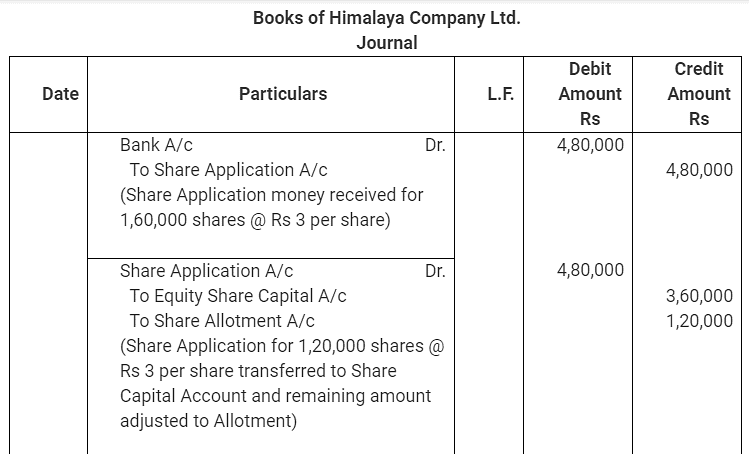

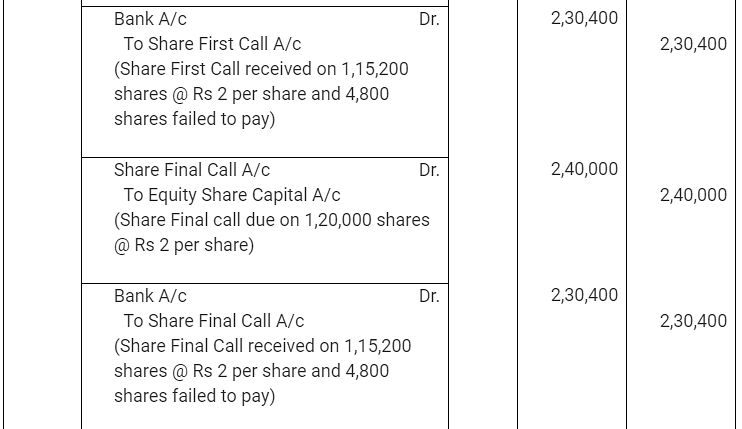

Q15: Himalaya Company Limited issued for public subscription of 1,20,000 equity shares of Rs 10 each at a premium of Rs 2 per share payable as under :

Applications were received for 1,60,000 shares. Allotment was made on pro-rata basis. Excess money on application was adjusted against the amount due on allotment.

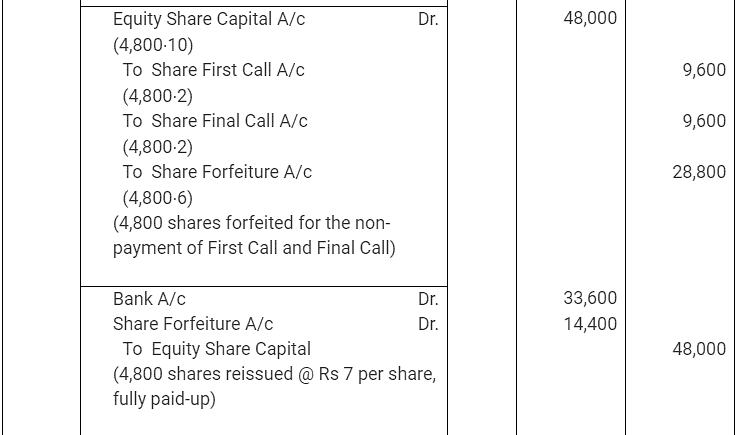

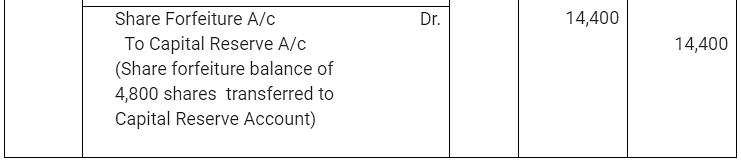

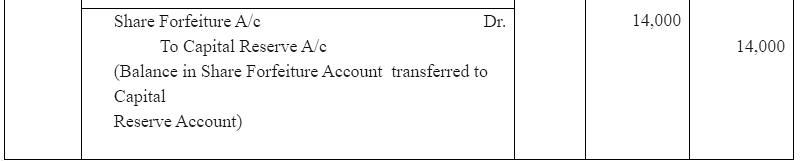

Rohan, whom 4,800 shares were allotted, failed to pay for the two calls. These shares were subsequently forfeited after the second call was made. All the shares forfeited were reissued to Teena as fully paid at Rs 7 per share.

Record journal entries in the books of the company to record these transactions relating to share capital. Also show the company’s balance sheet.

Ans:

Notes to Account

Notes to Account

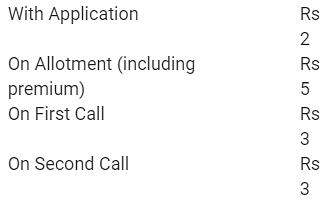

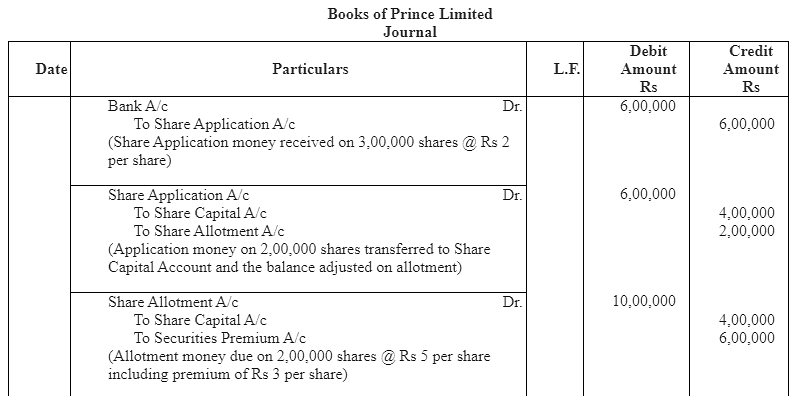

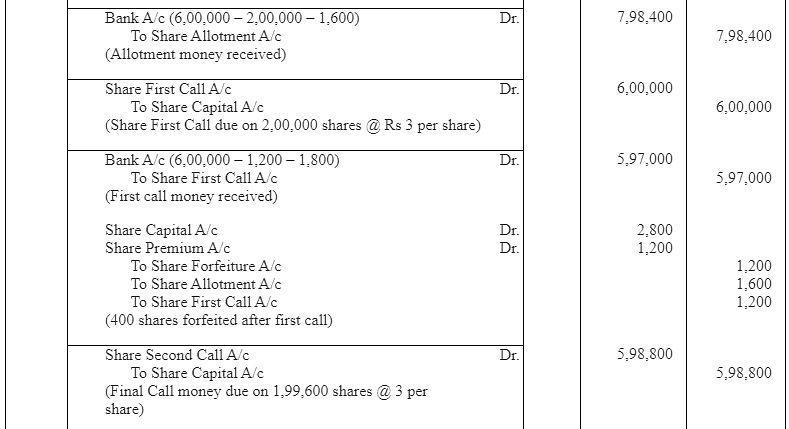

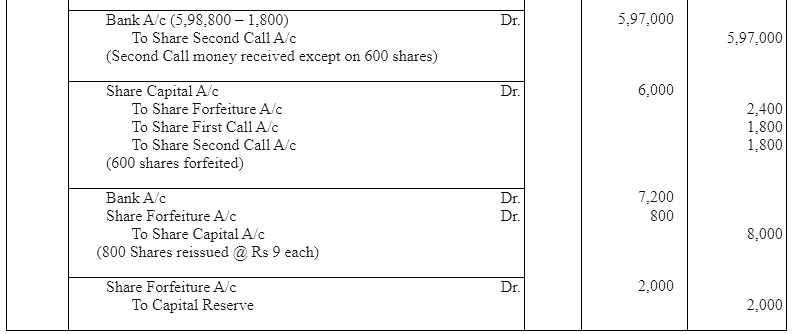

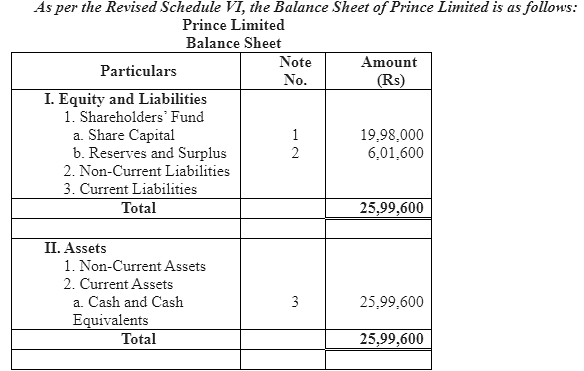

Q16: Prince Limited issued a prospectus inviting applications for 2,00,000 equity shares of Rs 10 each at a premium of Rs 3 per share payable as follows : Applications were received for 30,000 shares and allotment was made on pro-rata basis. Money overpaid on applications was adjusted to the amount due on allotment.

Applications were received for 30,000 shares and allotment was made on pro-rata basis. Money overpaid on applications was adjusted to the amount due on allotment.

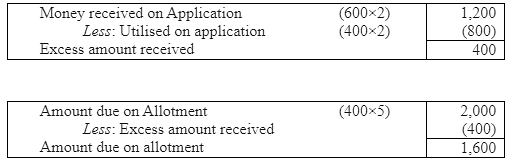

Mr. ‘Mohit’ whom 400 shares were allotted, failed to pay the allotment money and the first call, and her shares were forfeited after the first call. Mr. ‘Joly’, whom 600 shares were allotted, failed to pay for the two calls and hence, his shares were forfeited.

Of the shares forfeited, 800 shares were reissued to Supriya as fully paid for Rs 9 per share, the whole of Mr. Mohit’s shares being included.

Record journal entries in the books of the Company and prepare the Balance Sheet.

Ans:

Notes to Account

Notes to Account Working Note:

Working Note:

1. Number of shares applied by Mohit = (Total number of applied shares/Total number of allotted shares) x Number of shares allotted = (300000/200000) x 400 = 600 shares

2. Amount to be transferred to capital Reserve

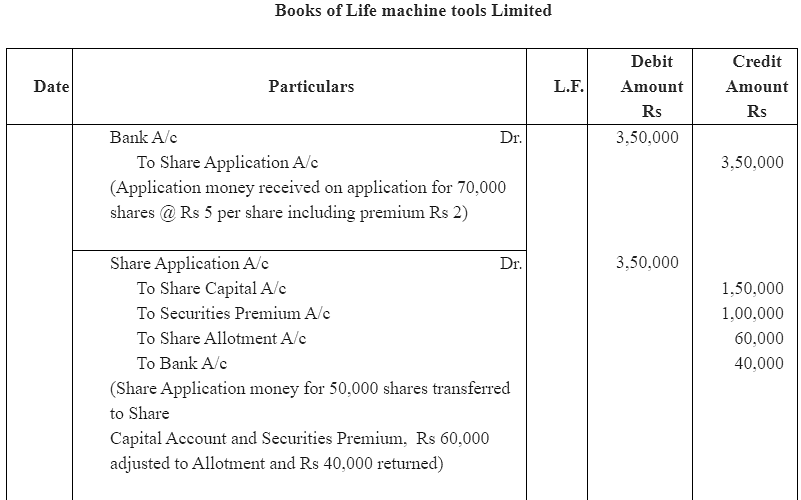

Q17: Life Machine Tools Limited, issued 50,000 equity shares of Rs. 10 each at Rs. 12 per share, payable at to Rs. 5 on application (including premium), Rs. 4 on allotment and the balance on the first and final call.

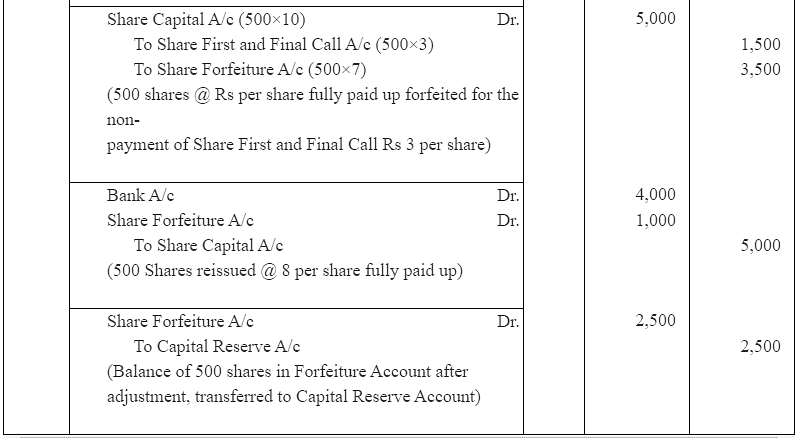

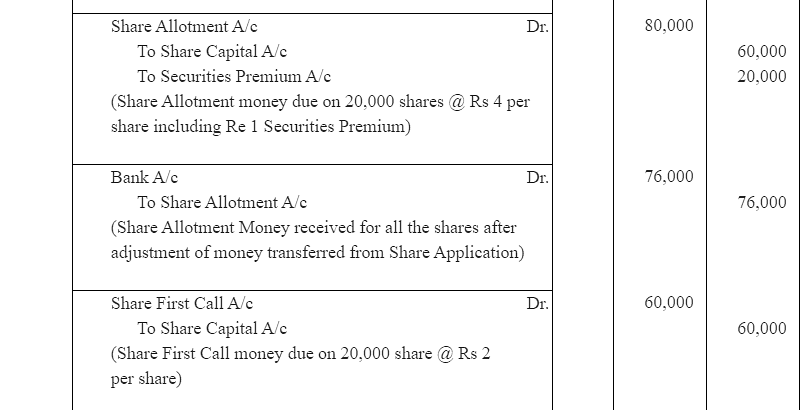

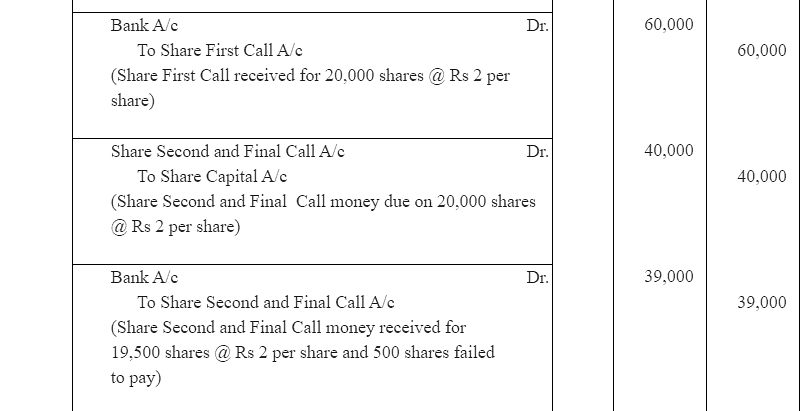

Applications for 70,000 shares had been received. Of the cash received, Rs 40,000 was returned and Rs 60,000 was applied to the amount due on allotment, the balance of which was paid. All shareholders paid the call due, with the exception of one shareholder of 500 shares. These shares were forfeited and reissued as fully paid at Rs 8 per share. Journalise the transactions.

Ans:

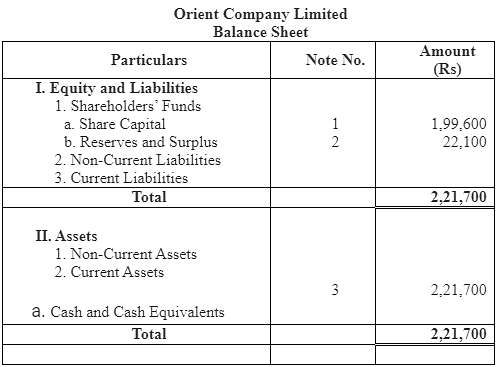

Q18: The Orient Company Limited offered for public subscription 20,000 equity shares of Rs 10 each at a premium of 10% payable at Rs 2 on application; Rs 4 on allotment including premium; Rs 3 on First Call and Rs 2 on Second and Final call. Applications for 26,000 shares were received. Applications for 4,000 shares were rejected. Pro-rata allotment was made to the remaining applicants. Both the calls were made and all the money were received except the final call on 500 shares which were forfeited. 300 of the forfeited shares were later on issued as fully paid at Rs 9 per share. Give journal entries and prepare the balance sheet.

Ans:

Working Notes:

The amount transferred to Capital Reserve Account, after adjustment for 300 shares = 300 Shares @ Rs 7 per share = Rs 2,100

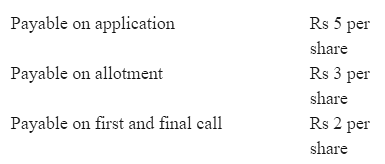

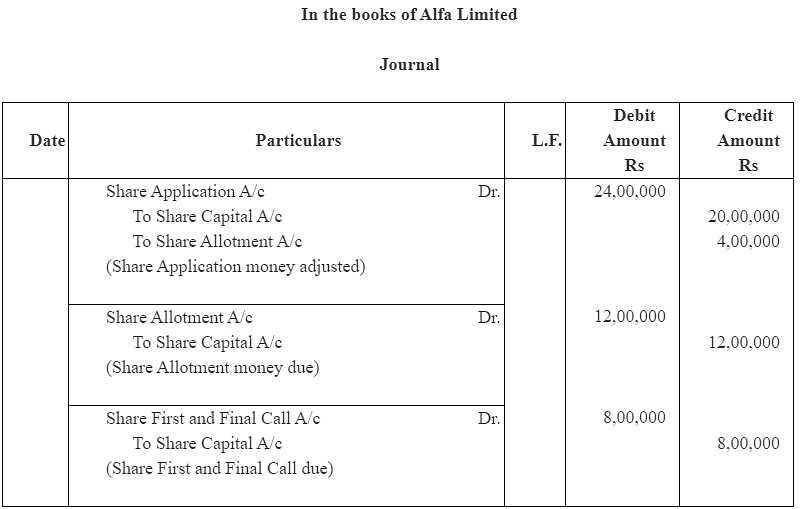

Q19: Alfa Limited invited applications for 4,00,000 of its equity shares of Rs 10 each on the following terms :

Applications for 5,00,000 shares were received. It was decided :

(a) to refuse allotment to the applicants for 20,000 shares;

(b) to allot in full to applicants for 80,000 shares;

(c) to allot the balance of the available shares' pro-rata among the other applicants; and

(d) to utilise excess application money in part as payment of allotment money.

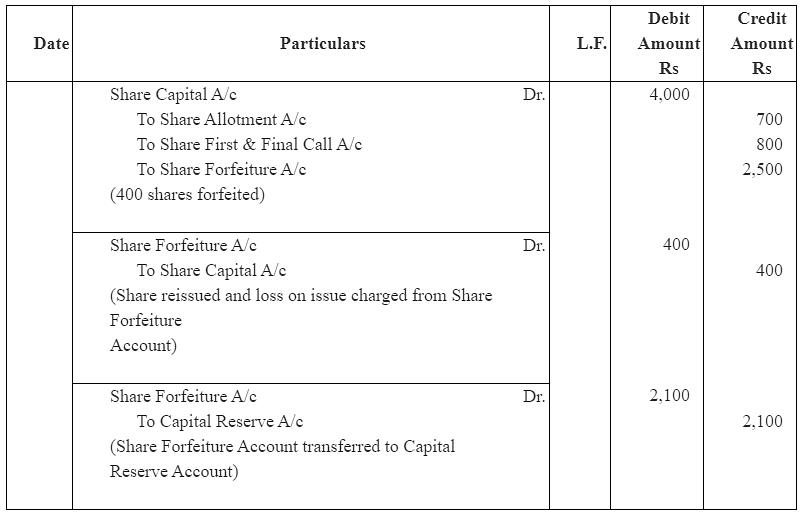

One applicant, whom shares had been allotted on pro-rata basis, did not pay the amount due on allotment and on the call, and his 400 shares were forfeited. The shares were reissued @ Rs 9 per share. Show the journal and prepare Cash book to record the above.

Ans:

Working Note:

1. Number of Share Applied by Applicant = (Total number of Applied Shares/Total number of Allotted Shares) x Number of Shares Allotted = (400000/320000) x 400 = 500 shares

2. Call in arrears by applicant on allotment

3.

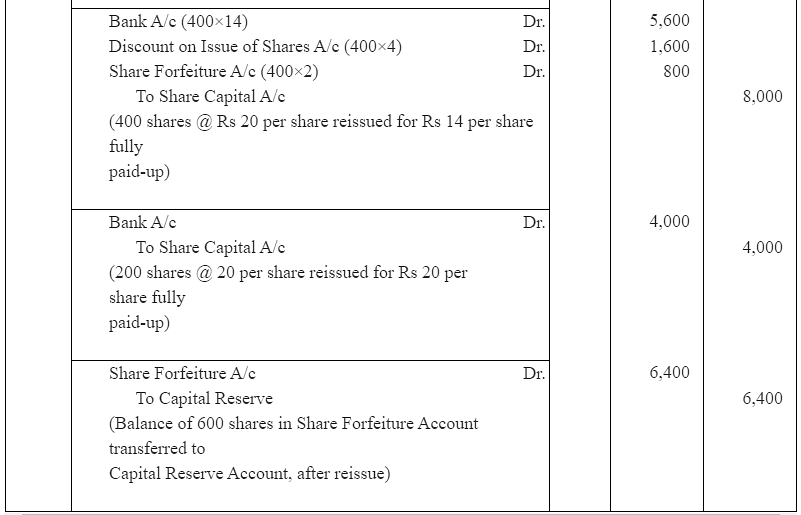

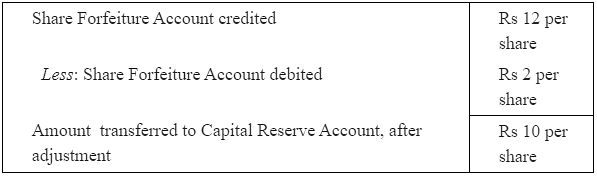

Q20: Ashoka Limited Company which had issued equity shares of Rs 20 each at a discount of Rs 4 per share, forfeited 1,000 shares for non-payment of final call of Rs 4 per share. 400 of the forfeited shares are reissued at Rs 14 per share out of the remaining shares of 200 shares reissued at Rs 20 per share. Give journal entries for the forfeiture and reissue of shares and show the amount transferred to capital reserve and the balance in Share Forfeiture Account.

Ans:

Balance in Share Forfeiture Account (12,000 – 800 – 6,400) = Rs 4,800

Working Notes:

For 400 Shares

Amount of 400 shares transferred to Capital Reserve Account, after reissue = 400 Shares @ Rs 10 per share = Rs 4,000

Amount of 200 shares transferred to Capital Reserve Account, after reissue = 200 Shares @ Rs 12 per share = Rs 2,400

Q21: Amit holds 100 shares of Rs 10 each on which he has paid Re.1 per share as application money. Bimal holds 200 shares of Rs 10 each on which he has paid Re.1 and Rs 2 per share as application and allotment money, respectively. Chetan holds 300 shares of Rs 10 each and has paid Re.1 on application, Rs 2 on allotment and Rs 3 for the first call. They all fail to pay their arrears and the second call of Rs 2 per share and the directors, therefore, forfeited their shares. The shares are reissued subsequently for Rs 11 per share as fully paid. Journalise the transactions.

Ans:

Working Notes:

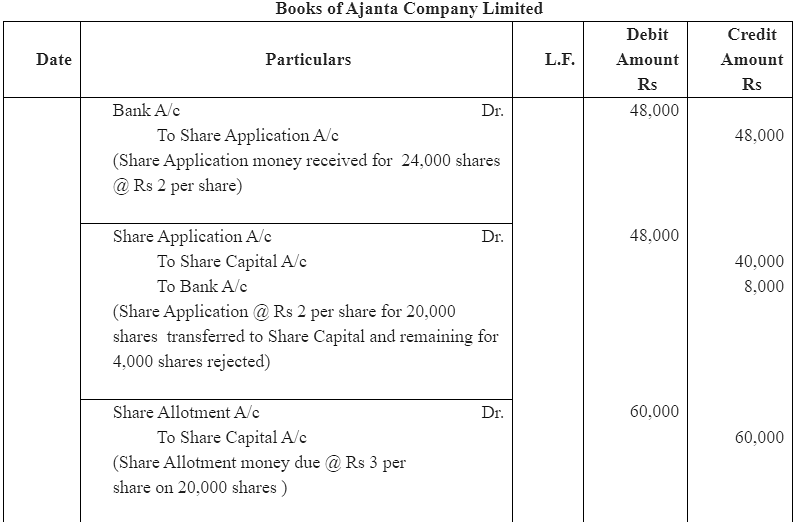

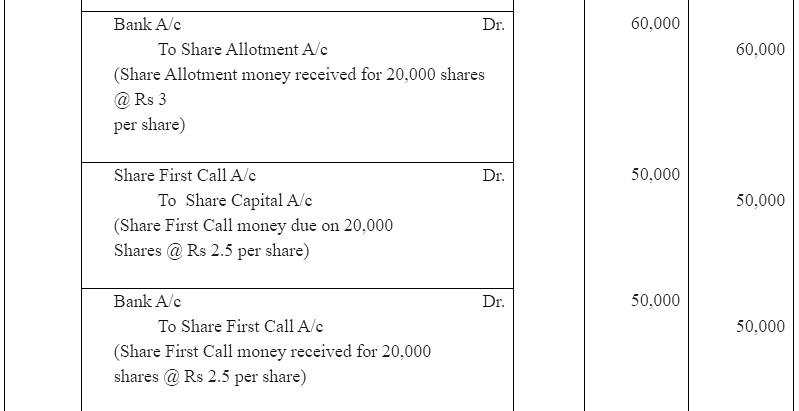

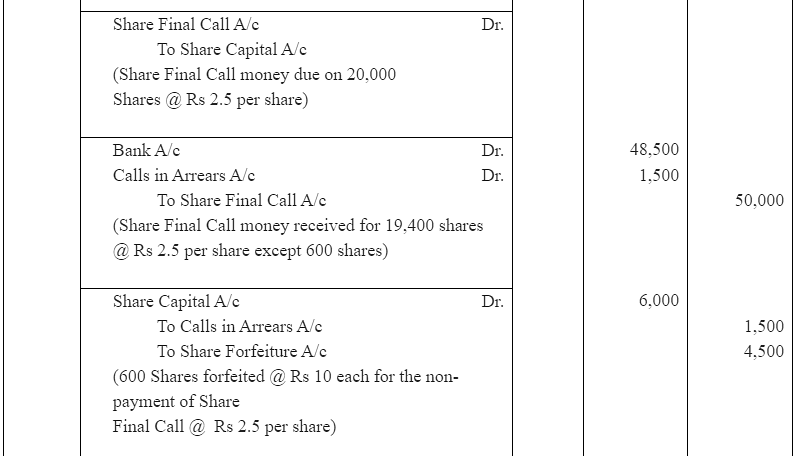

Q22: Ajanta Company Limited having a normal capital of Rs. 3,00,000, divided into shares of Rs. 10 each offered for public subscription of 20,000 shares payable at Rs. 2 on application; Rs. 3 on allotment and the balance in two calls of Rs. 2.50 each. Applications were received by the company for 24,000 shares. Applications for 20,000 shares were accepted in full and the shares allotted. Applications for the remaining shares were rejected and the application money was refunded.

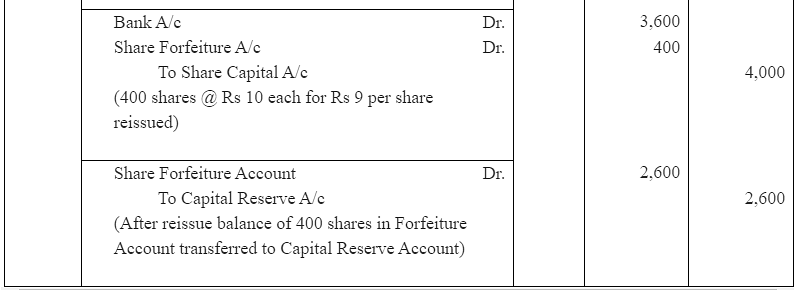

All moneys due were received with the exception of the final call on 600 shares which were forfeited after legal formalities were fulfilled. 400 shares of the forfeited shares were reissued at Rs. 9 per share.

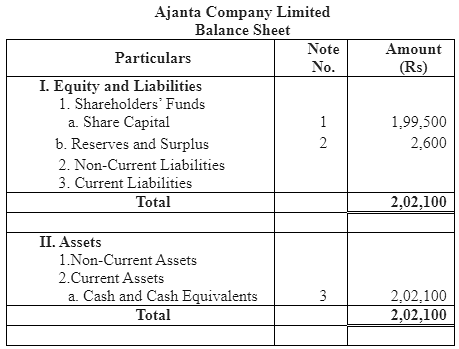

Record necessary journal entries and prepare the balance Sheet showing the amount transferred to capital reserve and the balance in Share forfeiture account.

Ans:

Working Note:

Working Note:

Amount of 400 shares transferred to Capital Reserve Account, after reissue = 400 Shares @ Rs 6.5 per share = Rs 2,600

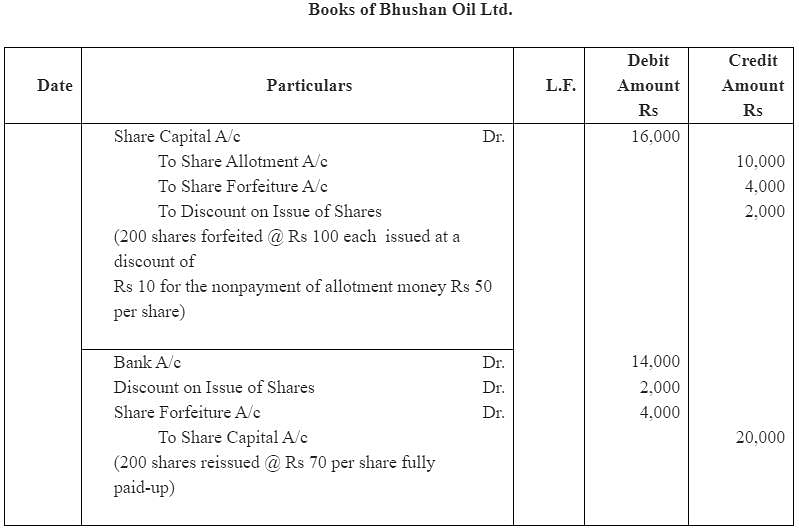

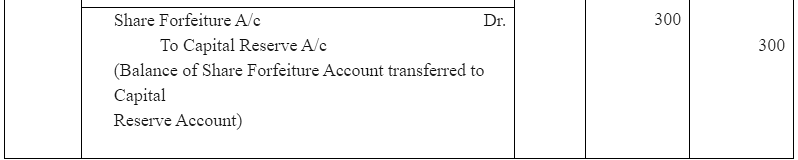

Q23: Journalise the following transaction in the books Bhushan Oil Ltd:

(a) 200 shares of Rs 100 each issued at a discount of Rs 10 were forfeited for the non payment of allotment money of Rs 50 per share. The first and final call of Rs 20 per share on these share were not made. The forfeited share were reissued at Rs 70 per share as fully paid-up.

(b) 150 shares of Rs 10 each issued at a premium of Rs 4 per share payable with allotment were forfeited for non-payment of allotment money of Rs 8 per share including premium. The first and final call of Rs 4 per share were not made. The forfeited share were reissued at Rs 15 per share fully paid-up.

(c) 400 share of Rs 50 each issued at par were forfeited for non-payment of final call of Rs 10 per share. These share were reissued at Rs 45 per share fully paid-up.

Ans:

Case (b)

Case(c)

Case(c)

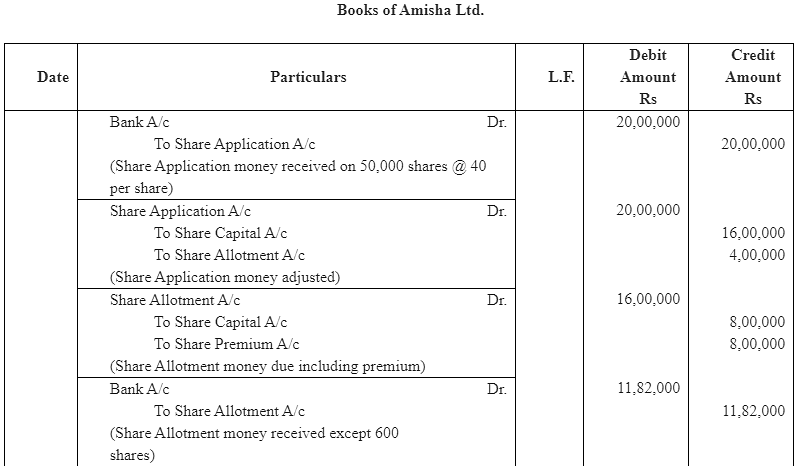

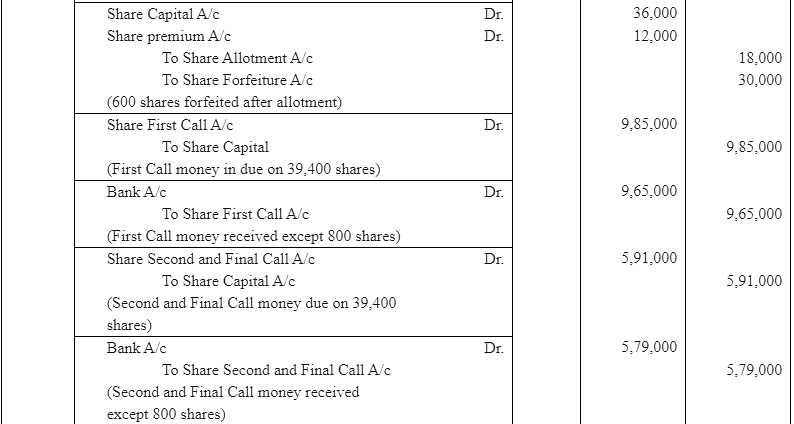

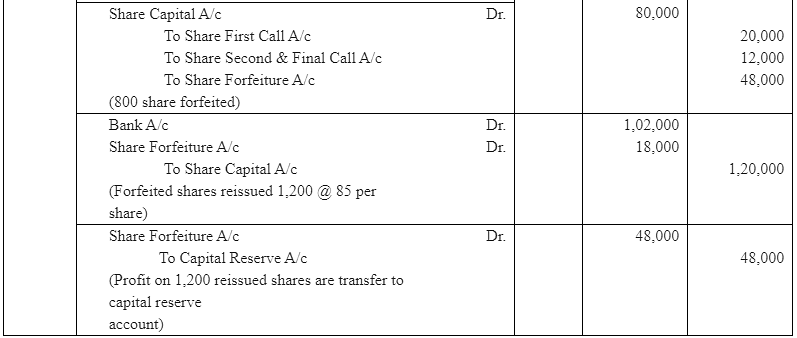

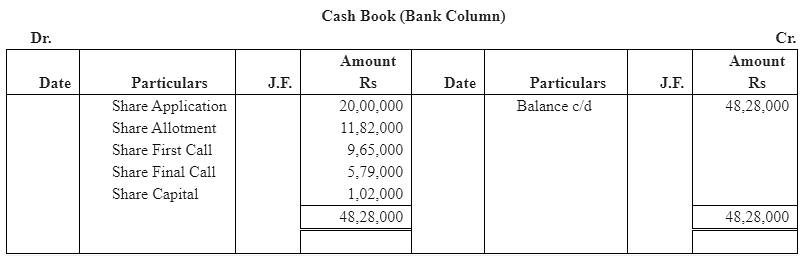

Q24 : Amisha Ltd inviting application for 40,000 shares of Rs 100 each at a premium of Rs 20 per share payable; on application Rs 40; on allotment Rs 40 (Including premium): on first call Rs 25 and Second and final call Rs 15.

Application were received for 50,000 shares and allotment was made on pro-rata basis. Excess money on application was adjusted on sums due on allotment.

Rohit to whom 600 shares were allotted failed to pay the allotment money and his shares were forfeited after allotment. Ashmita, who applied for 1,000 shares failed to pay the Two calls and his shares were forfeited after the second call. Of the shares forfeited, 1,200 shares were sold to Kapil for Rs 85 per share as fully paid, the whole of Rohit's shares being included.

Record necessary journal entries.

Ans:

Working Notes:

Working Notes:

1. Number of Share Applied by Rohit = (Total number of Applied Shares/Total number of Allotted Shares) x Number of Allotted Shares = (50000/40000) x 600 = 750 shares

2. Call in arrears by Rohit on allotment 3.

3.

4. Number of shares allotted to Ashmita = (Total number of Allotted Shares/Total number of Applied Shares) x Number of Applied Shares = (40000/50000) x 1000 = 800 shares

5. Profit on the forfeiture of 600 shares of Rohit = Rs.30000 Profit on the forfeiture of 600 shares of Ashmita = 48000 x (600/800) = Rs.36000

6. Balance in Share Forfeiture Account (48,000 – 36,000) = Rs. 12,000

|

42 videos|168 docs|43 tests

|

FAQs on NCERT Solution: Accounting for Share Capital - Accountancy Class 12 - Commerce

| 1. What is share capital in accounting? |  |

| 2. How is share capital recorded in the financial statements? | |

| 3. What are the different types of shares that a company can issue? | |

| 4. What is the difference between authorized capital and paid-up capital? | |

| 5. What is the significance of share capital in a company's financial health? | |

|

5.9K Views |

|

4.92/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

mock tests for examination

,NCERT Solution: Accounting for Share Capital | Accountancy Class 12 - Commerce

,Viva Questions

,Important questions

,study material

,Semester Notes

,Objective type Questions

,NCERT Solution: Accounting for Share Capital | Accountancy Class 12 - Commerce

,video lectures

,Previous Year Questions with Solutions

,NCERT Solution: Accounting for Share Capital | Accountancy Class 12 - Commerce

,MCQs

,Free

,shortcuts and tricks

,Summary

,practice quizzes

,past year papers

,Sample Paper

,Extra Questions

,Exam

,ppt

;

NCERT Solution: Accounting for Share Capital Free PDF Download

Importance of NCERT Solution: Accounting for Share Capital

NCERT Solution: Accounting for Share Capital Notes

NCERT Solution: Accounting for Share Capital Commerce Questions

Study NCERT Solution: Accounting for Share Capital on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!