NCERT Solution - Financial Statements of a Company

Short Answer Questions

Q1: State the meaning of financial statements?

Ans: Financial statements are the formal records that present the financial performance and financial position of a business for a given period or as at a particular date. They are prepared from the trial balance and other accounting records and provide reliable information to users for decision making. The principal financial statements are:

- Statement of Profit and Loss (Trading and Profit & Loss A/c): shows the revenue, expenses and the resulting profit or loss for an accounting period.

- Balance sheet: shows the financial position by listing the company's assets, liabilities and equity as at a specific date.

- Cash flow statement: shows the cash inflows and outflows during the accounting period, helping assess liquidity.

Together, these statements present a true and fair view of the company's financial affairs and help stakeholders make informed decisions.

Q2: What are limitations of financial statements?

Ans: Limitations of financial statements are given below.

- Ignores changes in price level:

The amounts are usually recorded at historical cost, so financial statements do not show the effects of inflation or changes in purchasing power. Comparisons over time may therefore be distorted. - Possibility of misleading information:

Changes in accounting policies or errors can make figures misleading. If items are not disclosed fully, users may draw incorrect conclusions. - Interim picture:

Financial statements present information for a particular date or period and may not capture future events or the long-term prospects of the business. - Ignores qualitative factors:

Non-monetary aspects such as managerial skill, employee morale, brand value and market reputation are not reflected in monetary terms.

Q3: List any three objectives of financial statements?

Ans: Objectives of Financial Statements

The following are the main objectives for preparing financial statements:

- To enable meaningful comparisons of financial data over different periods and between firms, helping users spot trends and changes.

- To assist management in planning and control by providing financial information used for budgeting, performance measurement and corrective actions.

- To show the earning capacity and profitability of the firm and to measure the efficiency of operations for investors, creditors and other stakeholders.

Q4: State the importance of financial statements to:

(i) shareholders

(ii) creditors

(iii) government

(iv) investors

Ans: Importance of financial statements to various users is given below.

(i) Shareholders: They use financial statements to assess the profitability and the returns on their capital and to judge management's performance and the firm's financial health.

(ii) Creditors: Lenders and suppliers look for information about the company's liquidity and solvency to decide whether the firm can meet short-term and long-term obligations.

(iii) Government: Uses accounting data for macroeconomic statistics, tax assessment and for framing economic policies; it needs reliable figures on income, profits and taxes.

(iv) Investors: Existing and prospective investors rely on financial statements to evaluate the viability and future prospects of their investment and to compare investment alternatives.

Q5: How will you disclose the following items in the Balance Sheet of a company;

(i) Current assets, inventory

(ii) Contigent liabilities in notes to accounts

(iii) Shareholders Funds, Reserve and Surplus

(iv) Fixed Assets, Intangible Assets

(v) Proposed Dividend for the current year

(vi) Non Current Liabilities

(vii) Arrears of Dividend on Cumulative Preference Shares.

Ans: Disclosure of various items in the Balance Sheet of a company is given below.

Long Answer Questions

Q1: Explain the nature of the financial statements.

Ans: The financial statements are the end-products of the accounting process and reflect the combined effect of recorded facts, accepted accounting conventions and the accountant's judgments. Their nature is influenced by the following factors:

1. Recorded facts- Items in financial statements are usually recorded at their historical cost (the amount paid when acquired). As a result, they do not always show current market values and do not automatically reflect inflationary changes.

2. Conventions- The application of conventions and concepts such as prudence, materiality, and matching ensures consistency, comparability and reliability in presentation.

3. Accounting assumptions Basic postulates such as going concern, money measurement and realisation shape how transactions are recognised and measured in the statements.

4. Personal judgments- Decisions such as method of depreciation, valuation of inventory, and provisions for doubtful debts require judgement. Different choices can lead to different reported results, so judgment influences the nature of the statements significantly.

Q2: Explain in detail about the significance of the financial statements.

Ans: The significance of financial statements is explained below.

- Provides information: They supply both internal and external users with financial data needed for evaluation and decision making, for example assessing profitability or tax liabilities.

- Cash flow: Cash flow information from financial statements helps users judge liquidity and the company's ability to meet obligations.

- Effectiveness of management: Comparability of results across periods enables evaluation of managerial performance and helps in policy and strategy formulation.

- Disclosure of accounting policies: Notes to accounts explain methods and changes in accounting policies, improving transparency and comparability.

- Policy formation by government: Aggregated accounting data support macroeconomic analysis and policy-making for employment, taxation and industry regulation.

- Attracts investors: Clear and reliable statements help attract new capital by showing profitability and solvency.

Q3: Explain the limitations of financial statements.

Ans: The following are the limitations of financial statements.

- Historical data: Values are normally recorded at cost, not current market value, so the effect of price changes is ignored.

- Ignorance of qualitative aspects: Qualities such as brand strength, customer goodwill or employee skill are not reflected in monetary terms.

- Biased information: Accounting involves judgement. Different choices of methods (inventory valuation, depreciation) may lead to different results.

- Difficulty in inter-firm comparison: Differences in accounting policies and practices make direct comparisons between firms less reliable.

- Window dressing: Companies may manipulate presentation (legally or otherwise) to present a better financial picture, which can mislead users.

- Difficulty in forecasting: As statements are based on past data, they may not reliably predict future performance without further analysis.

Q4: Prepare the format of statement of profit and loss and explain its items upto the ascertainment of profit before tax.

Ans: Format of Statement of Profit and Loss- As per the REVISED SCHEDULE VI

I. Revenue from operations - income arising from the company's core business activities. For a manufacturing or trading company this is mainly sale of products, sale of services and other operating revenues. For finance companies it includes interest and dividend earned from their financing activities.

II. Other incomes - income not arising from primary activities, e.g. interest received (for a non-financing company), dividend income, profit or loss on sale of investments and other non-operating incomes (net of directly related expenses).

III. Expenses - costs incurred to earn revenue. Major heads include:

- Cost of materials consumed - calculated as Opening stock of raw material + Purchases - Closing stock of raw material.

- Purchase of stock-in-trade - for trading concerns.

- Change in inventories - difference between opening and closing balances of stock and work-in-progress.

All expenses are deducted from total revenue to arrive at Profit before tax.

Q5: Prepare the format of balance sheet and explain the various elements of balance sheet.

Ans: COMPANY'S BALANCE SHEET- As per REVISED SCHEDULE VI

Items under the head Equity and Liabilities

1. Shareholders' Funds

a. Share Capital:

- Authorised Capital-

- Issued Share Capital-

- Subscribed Share Capital-

- Called-up Share Capital-

- Paid-up Share Capital-

- Share Forfeiture Amount

b. Reserves and Surplus: It consists of the following items to be shown separately.

- Capital Reserve

- Capital Redemption Reserve

- Securities Premium

- Debenture Redemption Reserve

- Revaluation Reserve

- Other Reserves (such as General Reserve, Tax Reserve, etc.)

- Proposed Additions to Reserves

- Sinking Fund

- Share Option Outstanding Amount

- Surplus i.e. credit balance in Statement of Profit and Loss. However, in the case of debit balance in Statement of Profit and Loss, it is deducted from the total reserves.

c. Money received against warrants: Amounts received on share warrants are shown under this head.

2. Share Application Money Pending Allotment

Amounts received on applications for shares not yet allotted are shown separately under this head.

3. Non-Current Liabilities

Typical items include:

- Long-term borrowings (debentures, bonds, term loans, deposits)

- Deferred tax liabilities (net)

- Other long-term liabilities and long-term provisions

4. Current Liabilities

Includes items expected to be settled within 12 months:

a. Short-term borrowings (loans and overdrafts), deposits

- Trade payables (creditors)

- Other current liabilities (income received in advance, interest accrued, unpaid dividends, calls-in-advance)

- Short-term provisions (provision for tax, proposed dividend, provision for doubtful debts)

Items under the head Assets

Assets are classified as Non-current and Current.

1. Non-Current Assets

a. Fixed Assets (tangible and intangible) such as buildings, machinery, goodwill, trademarks; capital work-in-progress and intangible assets under development.

- Tangible assets (buildings, machinery, furniture)

- Intangible assets (goodwill, copyrights, trademarks)

- Capital work-in-progress

b. Non-current investments, deferred tax assets, long-term loans and advances and other non-current assets.

2. Current Assets

a. Current investments (held for conversion into cash within 12 months)

- Equity shares, preference shares, government securities, mutual fund investments etc.

b. Inventories (raw materials, work-in-progress, finished goods, stores and spares), trade receivables, cash and cash equivalents (cash on hand, balances with banks, cheques in hand), short-term loans and advances, and other current assets (prepaid expenses, advance tax).

Q6: Explain how financial statements are useful to the various parties who are interested in the affairs of an undertaking?

Ans: The parties interested in financial statements are divided into:

1. Internal parties - those within the organisation who use the statements for managerial purposes.

2. External parties - those outside the organisation who use the statements for assessment and decision making.

Internal Parties

Key internal users and their interests:

- Owner: Interested in profit or loss and the return on capital invested.

- Management: Uses statements for planning, control, and policy formulation; monitors budgets and performance.

- Employees and workers: Concerned with profitability as it affects wages, bonuses and job security.

External Parties

External users and their needs:

- Banks and financial institutions: Need information on liquidity, solvency and profitability before sanctioning loans.

- Creditors: Assess the firm's ability to meet short-term obligations.

- Investors and potential investors: Evaluate profitability, growth prospects and risk before investing.

- Tax authorities: Use reported income and revenue figures to determine tax liabilities.

- Government: Relies on aggregate accounting information for policy making and economic analysis.

- Researchers and public: Use statements for industry studies, consumer protection and social responsibility assessment.

Q7: `Financial statements reflect a combination of recorded facts, accounting conventions and personal judgments' discuss.

Ans: The statement is correct. Financial statements are influenced by:

- Recorded facts: Transactions recorded at historical cost form the factual base of the statements.

- Conventions: Accepted accounting conventions (prudence, matching, materiality) guide recognition and measurement.

- Assumptions and judgements: Going concern and other assumptions, plus personal judgements about valuation and provisions, shape the final reported figures.

Q8: Explain the process of preparing income statement and balance sheet.

Ans: The process for preparing the income statement and the Balance Sheet is given below in chronological order.

- Prepare a trial balance from ledger balances to ensure that debits equal credits.

- Record revenue from operations (sales less sales returns) and add other incomes to arrive at total revenue.

- Classify and deduct operating and non-operating expenses (cost of materials, finance cost, depreciation etc.) to determine Profit before tax.

- Deduct tax to arrive at profit or loss for the period and transfer appropriate amounts to reserves and retained earnings.

- Prepare the Balance Sheet in vertical format (as per Revised Schedule VI) with two main sections: Equity and Liabilities and Assets.

- Under Equity and Liabilities, present Shareholders' funds, Share application money pending allotment, Non-current liabilities and Current liabilities.

- Under Assets, present Non-current assets (fixed assets, investments, deferred tax assets etc.) and Current assets (inventories, trade receivables, cash and equivalents etc.).

- Ensure that totals of Equity and Liabilities and Assets are equal before finalising the statements.

Numerical Questions

Q1: Show the following items in the balance sheet as per the provisions of the Companies Act, 2013 in Schedule III:

Ans:

Notes to Accounts

Q2: On April 1 , 2017, Jumbo Ltd., issued 10,000; 12% debentures of Rs. 100 each a discount of 20%, redeemable after 5 years. The company decided to write-off discount on issue of such debentures on March 31, 2018.

Show the items in the balance sheet of the company immediately after the issue of these debentures.

Ans:

Notes to Accounts

Q3: From the following information prepare the balance sheet of Gitanjali Ltd., as per the (Revised) Schedule VI:

Inventories Rs. 14,00,000; Equity Share Capital Rs. 20,00,000; Plant and Machinery Rs. 10,00,000; Preference Share Capital Rs. 12,00,000; Debenture Redemption Reserve Rs. 6,00,000; Outstanding Expenses Rs. 3,00,000; Proposed Dividend Rs. 5,00,000; Land and Building Rs. 20,00,000; Current Investments Rs. 8,00,000; Cash Equivalent Rs. 10,00,000; Short term loan from Zaveri Ltd. (A Subsidiary Company of Twilight Ltd.) Rs. 4,00,000; Public Deposits Rs. 12,00,000.

Ans:

Q4: From the following information prepare the balance sheet of Jam Ltd. as per the (revised) Schedule VI:

Inventories Rs. 7,00,000; Equity Share Capital Rs. 16,00,000; Plant and Machinery Rs. 8,00,000; Preference Share Capital Rs. 6,00,000; General Reserves Rs. 6,00,000; Bills payable Rs. 1,50,000; Provision for taxation Rs. 2,50,000; Land and Building Rs. 16,00,000; Noncurrent Investments Rs. 10,00,000; Cash at Bank Rs. 5,00,000;Creditors Rs. 2,00,000; 12% Debentures Rs. 12,00,000.

Ans:

Q5: Prepare the balance sheet of Jyoti Ltd. as at March 31, 2017 from the following information:

Building Rs. 10,00,000; Investments in the shares of Metro Tyers Rs. 3,00,000; Stores & Spares Rs. 1,00,000; Discount on issue of 10% debentures Rs. 10,000; Statement of Profit and Loss (Dr.) Rs. 90,000; 5,00,000 Equity Shares of Rs. 20 each fully paid-up; Capital Redemption Reserve Rs. 1,00,000; 10% Debentures Rs. 3,00,000; Unpaid dividends Rs. 90,000; Share options outstanding account Rs. 10,000.

Ans:

*Note: There is a misprint in the book. The number of equity shares issued must be 50,000 so that both sides of the Balance Sheet stand equal.

Q6: Brinda Ltd. has furnished the following information:

(a) 25,000, 10% debentures of Rs. 100 each;

(b) Bank Loan of Rs. 10,00,000 repayable after 5 years;

(c) Interest on debentures is yet to be paid.

Show the above items in the balance sheet of the company as at March 31, 2017.

Ans:

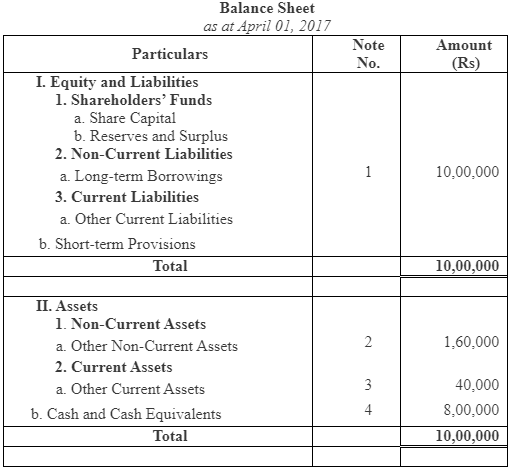

Question 7: Prepare a balance sheet of Black Swan Ltd., as at March 31, 2017 from the following information:

Ans:

FAQs on NCERT Solution - Financial Statements of a Company

| 1. What are the key components of a financial statement for a company? |  |

| 2. How do financial statements help in analyzing a company's performance? | |

| 3. What is the difference between cash flow and profit in financial statements? | |

| 4. Why is it important for companies to prepare financial statements regularly? | |

| 5. What role do auditors play in the financial statement process? | |