Scanner - Cost of Production

N. .C. E. R. T Questions

(Q1) Classify following into fixed and variable cost

(a) Rent for shed (b) Minimum telephone bill

(c) Cost of raw material (d) Wages to permanent staff

(e) Interest on capital (f) Payment for transportation of goods

(g) Telephone charges beyond the minimum (h) Daily Wages.

(i) Expenditure on raw material (j) Excise duty and Sales Tax

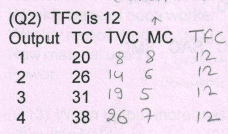

(Q2) How does TFC changes when output changes

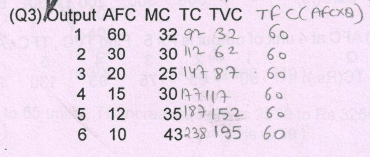

(Q3) How is total variable cost derived from marginal cost schedule ?

(Q4) What is the general shape of AFC, MC , AC curves?

(Q5) What will happen to ATC when MC > ATC ?

(Q6) Distinguish between fixed and variable cost ?

(Q7) With the help of a suitable diagram , explain the relationship between TC, TFC, and TVC

(Q8) DO ATC and AVC curves intersect? Give reason

(Q9) Why is the MC curve in the short run U - shaped ?

(Q10) Explain the relationship between ATC, AVC and MC with a suitable illustration.

(Q11) During market period all cost are fixed cost . How ?

C. B. S. E. Questions

(Q1) Meaning of Marginal Cost, Fixed Cost / supplementary cost, variable cost ?

(Q4) Why does average fixed cost falls as output rises ?

(Q5) Distinguish between fixed and variable costs ? Give two example of each ?

(Q6) Explain the relationship between MC and AC with the help of cost schedule ?

CBSE + Sample Paper Questions

(Q1) Distinguish between (i) fixed cost and variable cost giving examples and (ii) average cost and marginal cost giving an example. (4M)

(Q2) A firm's Average Fixed Cost of producing 2 units of a good is Rs. 9 and given below is its total cost schedule. Calculate its Average Variable Cost and Marginal Cost for each of the given level of output : (3M)

(Q3) Define opportunity cost.(1M)

(Q4) Define cost.(1M)

(Q5) Draw average total cost, average variable cost, and marginal cost curves in a single diagram. Also explain the relationship between ATC and AVC.(6M)

(Q6) Explain the relation between (i) ATC and AVC and (ii) MC and AVC.(6M)

CBSE

(Q1) Why is average total cost greater than average variable cost ?(1M)

(Q2) Define fixed costs.(1M)

(Q3) Define marginal cost.(1M)

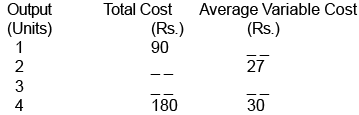

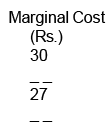

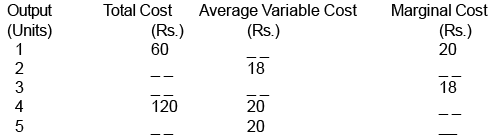

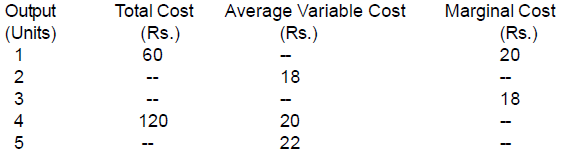

(Q4) Complete the following table :

(Q5) Complete the following table :

(Q6) Complete the following table :

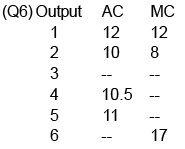

(Q7) Given below is cost schedule of a firm . Its AFC is 20 rupees when it produces 3 units. Calculate MC and ATC

(Q8) State true or false with reason (6M)

(i) As output is increased, the difference between average total cost and average variable falls and utimately becomes zero

(ii) Average cost falls only when marginal cost falls.

(iii) The difference between average total cost and average variable cost is constant.

(Q9) State true or false with reason (a) AVC can fall when MC is rising (b) The difference between TC and TVC fall with increase in output (CBSE {D})

CBSE + Sample Paper Questions

(Q1) State true or false. Give reasons for your answer : As soon as marginal cost starts rising,average variable cost also starts rising.(2M)

(Q2) A firm's average fixed cost, when it produces 2 units, is Rs. 30. Its average total cost schedule is given below. Calculate its marginal cost and average variable cost at each level of output. (3M)

(Q3) Given below is the cost shedule of a firm. Its total fixed cost is Rs. 120. Calculate of a firm. Calculate the marginal cost and average variable cost at each level of output.

(Q4) From the following cost schedule of a firm, calculate marginal cost and average variable cost at each level of output.

(Q5) Give the meaning of marginal cost.(1 M)

(Q6) What is meant by cost in economics ?(1 M)

(Q7) State the distinction between explicit cost and implicit cost. Give an example of each.(3 M)

(Q8) Why does the difference between Average Total Cost and Average Variable Cost decrease with an increase in the level of output ? Can these two be equal at some level of output

CBSE Questions

(Q1) Distinguish between explicit cost and implicit cost and give examples.(3 marks)

(Q2) Define marginal cost. Explain its relation with average cost.(4 marks)

OR

Define variable cost. Explain the behaviour of total variable cost as output increases.(4 marks)

(Q3) Distinguish between explicit cost and implicit cost and give examples.(3 marks)

(Q4) An individual is both the owner and manager of a shop taken on rent . Identify implicit and explicit costs from this information . Explain

(Q5) A producer borrows money and opens a shop . The shop premises is owned by him . Identify Identify implicit and explicit costs from this information . Explain

(Q6) A producer starts a business by investing his own saving . He employs a manager to look after it .Identify implicit and explicit costs from this information . Explain

(Q7) What is the behaviour of Total Variable Cost, as output increases? (1 mark)

(Q8) A farmer takes a farm on rent and carries on farming with the help of family members. Identify explicit and implicit costs from this information. Explain.(3 marks)

(Q9) Draw Total Variable Cost, Total Cost, and Total Fixed Cost curves in a single diagram. or Explain the behaviour of total cost as output increases. (3 marks)

(Q10) A producer starts a business by investing his own savings and hiring the labour. Identify implicit costs from this information. Explain. (3 marks)

(Q11) What is Opportunity Cost ? Explain with the help of an example. (3 marks)

(Q12) A producer borrows money and starts a business. He himself looks after the business. Identify implicit and explicit costs from this information. Explain. (3 marks)

CBSE Questions

(Q1) Define Marginal Cost

Ans: Addition to total cost on producing one more unit.

(Q2) Give two examples of fixed costs

Ans: Rent , Salary of permanent employee, etc. (any two) ½×2

(Q3 ) Give two examples of variable costs

Ans: Expenditure on raw materials, casual labour, etc (any two)

(Q4) State the behavior of Total Variable Cost. Draw Total Variable Cost, Total Cost and Total Fixed Cost curves in a single diagram. (4 marks)

(Q5) Show with the help of numerical example that AC is constant when MC is equal to it

Sample Paper

(Q1) If it is given that the total variable cost for producing 15 units of output is Rs. 3000 and for 16 units is Rs. 3,500. Find the value of Marginal Cost.

Ans: Rs. 500

Sol: Marginal Cost = TVC(16) - TVC(15) = Rs. 3,500 - Rs. 3,000 = Rs. 500.

(Q2) If a firm's production department data says that the total variable cost for producing 8 units and 10 units of output is 2,500 and 3,000 respectively, marginal cost of 10th unit will be

a. 100 b. 150 c. 500 d. 250

Ans: (d)

Explanation: The increase in TVC from 8 to 10 units = Rs. 3,000 - Rs. 2,500 = Rs. 500. This increase is for two units (9th and 10th). So, marginal cost of the 10th unit = Rs. 500 ÷ 2 = Rs. 250.

(Q3) The total cost at 5 units of output is Rs 30. The fixed cost is Rs 5. The average variable cost at 5 units of output is :

(a) Rs 25 (b) Rs 6 (c) Rs 5 (d) Re 1

Ans: (c)

Explanation: Variable cost = Total cost - Fixed cost = Rs. 30 - Rs. 5 = Rs. 25. Average variable cost = Variable cost ÷ Quantity = Rs. 25 ÷ 5 = Rs. 5.

(Q4) State true or false

(a) AFC curve is a rectangular hyperbola curve.

(b) Total cost rises only when marginal cost rises

(c) With increase in level of output, average fixed cost goes on falling till it reaches zero.

Ans:

Part (a) - Ans: True

Explanation: Average fixed cost (AFC) = TFC/Q. Since total fixed cost (TFC) is constant, AFC falls continuously as Q increases and its graph is a rectangular hyperbola.

Part (b) - Ans: False

Explanation: Total cost (TC) rises whenever marginal cost (MC) is positive. If MC falls but remains positive, TC still rises, though at a diminishing rate. Thus TC does not rise only when MC rises; it can rise even when MC is falling (provided MC > 0).

Part (c) - Ans: False

Explanation: TFC is positive and constant. AFC = TFC/Q falls as Q increases but never becomes zero for any finite Q.

(Q5) Justify the statement, 'In economics, normal profits are always a part of total cost'. (3)

Ans: The statement is correct. Normal profit is the minimum reward required to keep the entrepreneur supplying his services in that activity. Since total cost includes payments to all primary inputs - land, labour, capital and enterprise - it includes rent, wages, interest and normal profit. Hence normal profit forms part of total cost.

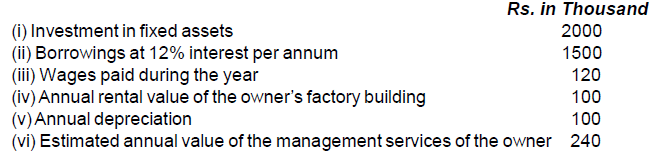

(Q6) Find out (a) explicit cost and (b) implicit cost from the following :(4 marks)

Ans: (a) Explicit cost: Rs. 400; (b) Implicit cost: Rs. 400.

C.B.S.E Paper

(Q1) Define variable cost. (1 mark)

Ans: The cost which changes with change in output is called variable cost.

(Q2) What is cost in economics ? (1 mark)

Ans: Cost in economics refers to the sum of actual money expenditure on inputs and the estimated value of inputs supplied free by the owner (imputed cost).

(Q3) Draw a total variable cost curve and a total cost curve in a single diagram.(3M)

(Q4) Explain behaviour of Average Fixed Cost (AFC). Use diagram.(3M)

Ans: AFC falls continuously as output is increased. This is because total fixed cost (TFC) remains unchanged while output rises, so AFC = TFC/output declines with each additional unit.

(Q5) Explain the relation between total Cost and Marginal cost

Ans: When total cost (TC) rises at a decreasing rate, marginal cost (MC) falls. When TC rises at an increasing rate, MC rises. When TC rises at a constant rate, MC remains constant. In short, MC indicates the slope or rate of change of TC.

Sample Paper

(Q1) The total cost at 5 units of output is Rs. 30. The fixed cost is Rs. 5. The average variable cost at 5 units of output is :(1 M)

(a) Rs. 25 (b) Rs. 6 (c) Rs. 5 (d) Rs.1

(Q2) State True or False. Justify your answer.(3 M)

(a) Total cost rises only when marginal cost rises.

C.B.S.E Paper

(Q1) What is the behaviour of (a) Average Fixed Cost and (b) Average Variable Cost as more and more units of a good are produced ?(4 M)

Ans: (a) AFC falls continuously as more output is produced because total fixed cost remains unchanged while quantity increases.

(b) AVC falls initially due to increasing marginal returns and, after a certain level of output, starts rising because of diminishing marginal returns.

(Q2) The average fixed cost at 4 units of output is Rs.20. Average variable cost at 5 units of output is Rs.40. Average cost of producing 5 units is :[AI (C)]

(a) Rs.20 (b) Rs.40 (c) Rs. 56 (d) Rs. 60

Ans: (c)

(Q3) Giving reasons, state whether the following statements are true or false?[AI (C)]

(a) The difference between AC and AVC is always constant. (b) When MC rises, AVC must rise. (c) Average cost will rise only when marginal cost rises.

(Q4) State the relationship between :[AI (C)]

(a) Marginal cost and average variable cost (b) Total cost and marginal costExplain the

(Q5) Define cost. State the relation between marginal cost and average variable cost.(1M)

Ans: Cost in economics refers to the sum of actual money expenditure on inputs and the imputed expenditure in the form of inputs supplied by the owners including normal profit.

If MC < AVC , then AVC falls.

If MC = AVC, then AVC is constant.

If MC > AVC, then AVC rises.

(Q6) The average fixed cost at 4 units of output is Rs 20. Average variable cost at 5 units of output is Rs 40. Average cost of producing 5 units is rupees : (1)

(a) 20 (b) 40 (c) 56 (d) 60

Ans: (c)

(Q7)Giving reasons, state whether the following statements are true or false : The difference between average cost and average variable cost is always constant

Ans: False. The difference between AC and AVC equals AFC. As output increases, AFC falls; therefore the difference between AC and AVC falls.

FAQs on Scanner - Cost of Production

| 1. What factors contribute to the cost of production for scanners? |  |

| 2. How does the scale of production impact the cost of scanners? | |

| 3. What role does technology play in determining the cost of producing scanners? | |

| 4. How do changes in raw material prices affect the cost of producing scanners? | |

| 5. How do competition and market demand influence the cost of production for scanners? | |