Important Questions- Admission (Accounting for Partnership Firms and Companies) | Accountancy Class 12 - Commerce PDF Download

Q 1. A and B were partners in a firm. They admitted C as a new partner for a 20% share in the profits. After all adjustments regarding general reserve, goodwill, gain or loss on revaluation, the balances in capital accounts of A and B were 3,85,000 and 4,15,000, respectively. C brought proportionate capital so as to give him a 20% share in the profits. Calculate the amount of capital to be brought by C. (1)

Q2. Jai & Veero are partners sharing profits 3:2. They admitted om has a new partner for 1/5 share in profits one fourth of which he takes in from Jai and remaining from Veero. Ho brings stock of rs.60,000, debtors of rs.80000, land of rs.1,00,000, P&M rs.40,000 as his share of goodwill and capital. On the date of Om’s admission, goodwill was valued at rs.6,00,000. Pass entries. (3)

Q3. (i) A and B were partners in a firm who share profits in the ratio of 5:3. C is admitted for 1/10th share, half of which was gifted by A, and the remaining was taken by c equally from A & B, find the new ratio.

(ii) Rekha, Sunita, and Teena are partners in the firm, sharing profits in the ratio of 3:2:1. Samiksha joins the firm. Rekha surrenders 1/4th of her share; Sunita surrenders 1/3rd of her share and Teena 1/5th of her share in favor of Samiksha. Find the new Profit sharing ratio. (4)

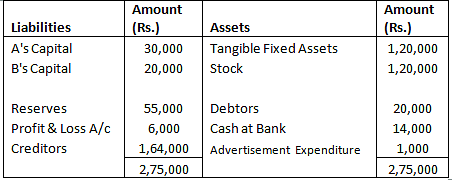

Q5. The Balance Sheet of A & B, who share profits in the ratio of 3:2 as at 31/03/13, was as follows: They admit C as a partner with 1/5 share in the profits of the firm. C brings Rs.40,000 as his capital. Give the necessary Journal entries to record Goodwill and capital. (4)

They admit C as a partner with 1/5 share in the profits of the firm. C brings Rs.40,000 as his capital. Give the necessary Journal entries to record Goodwill and capital. (4)

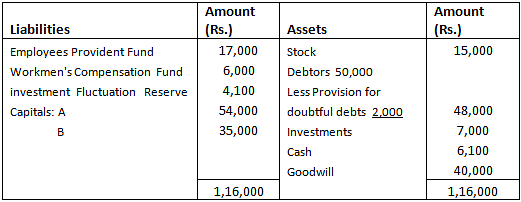

Q6. A and B are partners in the firm, sharing profits and losses in the ratio of 3:1. They admit C for a ¼ share on 31st March 2014 when their Balance Sheet was as follows: The following adjustments were agreed upon:

The following adjustments were agreed upon:

(a) C brings in 16,000 as goodwill and proportionate capital.

(b) Bad debts amounted to 3,000.

(c) Market value of an investment is 4,500.

(d) Liability on account of workmen’s compensation reserve amounted to 2,000.

Prepare Revaluation A/c and Partner’s Capital A/cs. (6)

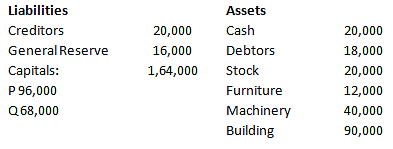

Q7. P and Q were partners in the firm, sharing profits in a 3:2 ratio. R was admitted as a new partner for 1/4th share in the profits on April 1, 2015. The Balance Sheet of the firm on March 31, 2015, was as follows: The terms of the agreement on R’s admission were as follows:

The terms of the agreement on R’s admission were as follows:

a) R brought in cash 60,000 for his capital and 30,000 for his share of goodwill.

b) Building was valued at 1,00,000 and Machinery at 36,000.

c) The capital accounts of P and Q were to be adjusted in the new profit-sharing ratio. Necessary cash was to be brought in or paid off to them as the case may be.

Prepare Revaluation Account, Partner’s Capital Account, and the Balance Sheet of P, Q and R.

Or

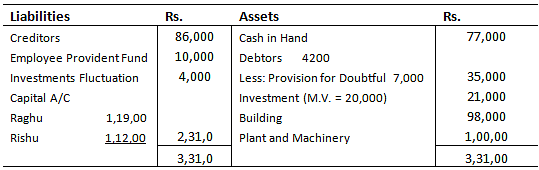

Raghu and Rishu are partners sharing profits in the ratio 3: 2. Their Balance Sheet as at 31st March 2014 was as follows: Rishabh was admitted on that date for 1/4th share of profit on the following terms:

Rishabh was admitted on that date for 1/4th share of profit on the following terms:

(i) Rishabh will bring his capital propionate to the capitals of existing partners.

(ii) Goodwill of the firm is valued at Rs. 42,000, and Rishabh will bring his share of Goodwill in cash.

(iii) Building was appreciated by 20%.

(iv) All Debtors were good.

(v) There was a liability of 10,800 included in creditors which was not likely to arise.

(vi) New profit-sharing ratio will be 2: 1: 1.

(vii) Capital of Raghu and Rishu will be adjusted on the basis of Rishabh's share of capital, and any excess or deficiency will be made by withdrawing or bringing in cash by the partners as the case may be.

Prepare Revaluation Account, Partner’s Capital Account, and the Balance Sheet of Raghu, Rishu and Rishabh. (8)

|

42 videos|168 docs|43 tests

|

FAQs on Important Questions- Admission (Accounting for Partnership Firms and Companies) - Accountancy Class 12 - Commerce

| 1. What is accounting for partnership firms and companies? |  |

| 2. What are the differences between accounting for partnership firms and companies? | |

| 3. What are the different types of financial statements prepared in accounting for partnership firms and companies? | |

| 4. What is the role of an accountant in accounting for partnership firms and companies? | |

| 5. What are some common accounting principles and concepts used in accounting for partnership firms and companies? | |

|

47.6K Views |

|

4.76/5 Rating |

|

Dec 22, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

video lectures

,study material

,ppt

,past year papers

,Exam

,Important Questions- Admission (Accounting for Partnership Firms and Companies) | Accountancy Class 12 - Commerce

,practice quizzes

,Important questions

,Sample Paper

,shortcuts and tricks

,MCQs

,Important Questions- Admission (Accounting for Partnership Firms and Companies) | Accountancy Class 12 - Commerce

,Free

,Summary

,mock tests for examination

,Objective type Questions

,Previous Year Questions with Solutions

,Important Questions- Admission (Accounting for Partnership Firms and Companies) | Accountancy Class 12 - Commerce

,Extra Questions

,Semester Notes

,Viva Questions

;

Important Questions- Admission (Accounting for Partnership Firms and Companies) Free PDF Download

Importance of Important Questions- Admission (Accounting for Partnership Firms and Companies)

Important Questions- Admission (Accounting for Partnership Firms and Companies) Notes

Important Questions- Admission (Accounting for Partnership Firms and Companies) Commerce

Study Important Questions- Admission (Accounting for Partnership Firms and Companies) on the App

|

© EduRev

|

Education Revolution

|

|