Important Questions - Retirement (Accounting for Partnership Firms and Companies) | Accountancy Class 12 - Commerce PDF Download

Chapter - Retirement

Important Questions

Q1. A, B and C are the partners sharing profits and losses in the ratio of 5:3:2. C retired and his capital balance after adjustments regarding Reserves, Accumulated profits/ losses and gain/loss on revaluation was 2,50,000. C was paid 3,00,000 in full settlement. Afterwards D was admitted for 1/4th share . Calculate the amount of goodwill premium brought by D.

(1)

Q2. MM, KK and PP are partners in a firm. PP retired from the firm. After making adjustments for Reserves and Revaluation of Assets and Liabilities the balance in PP’s capital account was Rs.1,20,000. MM and KK paid Rs.1,80,000 in full settlement to PP. Identify the item for which MM and KK paid Rs.60,000 more to PP and pass the entry for the same.

(1)

Q3. X, Y and Z are partners in a firm sharing profits in the ratio of 3: 2 : 1. X retires from the firm. Y and Z agree that the capital of the new firm shall be fixed at Rs. 2,10,000 in the profit-sharing ratio. The capital accounts of Y and Z after all adjustments on the date of retirement showed balances of Rs. 1,45,000 and Rs. 63,000 respectively. State the amount of actual cash to be brought in or to be paid to the partners. Pass the necessary journal entries.

(3)

Q4. A, B, C and D were partners sharing profits in the ratio of 3: 3: 2 : 2 respectively. On 1st April, 2014, D retired owing to ill health. It was decided by A, Band C that in future their profit-sharing ratio would be 3 : 2 : 1. Goodwill of the firm is valued at Rs. 6,00,000. Goodwill already appeared in the Balance Sheet at Rs. 50,000. Pass the necessary journal entries.

(3)

Q5. A, B, C and D were partners sharing profits in the ratio of 1:2:3:4. D retired and his share was acquired by A and B equally. Goodwill was valued at 3 year’s purchase of average profits of last 4 years, which were 40,000. General Reserve showed a balance of 1,30,000 and D’s Capital in the Balance Sheet was 3,00,000 at the time of D’s retirement. You are required to record necessary Journal entries in the books of the firm and prepare D’s capital account on his retirement.

(4)

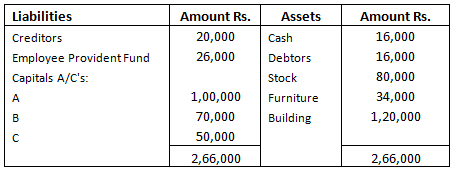

Q6. A, B and C were partners sharing profits in the ratio of 3:5:2. Their Balance Sheet as on 1st April, 2011 was as follows:

B retires on the above date and it was agreed that:

a. B’s share of Goodwill was 8,000.

b. 5% provision for doubtful debts was to be made on debtors.

c. Sundry creditors were valued 4,000 more than the book value.

Pass necessary journal entries for the above transactions on B’s retirement.

(4)

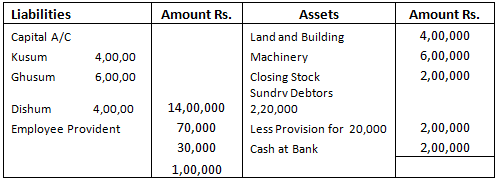

Q7. Following is the Balance Sheet of kusum, ghusum and dishum who have agreed to share profits and losses in proportion of their capitals.

On 31st March, 2014, Kusum desired to retire from the firm and the remaining partners decided to carry on the business. It was agreed to revalue the assets and reassess the liabilities on that date, on the following basis:

(i) Land and Building to be appreciated by 30%.

(ii) Machinery be depreciated by 30%.

(iii) There were Bad Debts of Rs. 35,000.

(iv) The claim on account of Workmen Compensation Reserve was estimated at Rs. 15,000.

(v) Goodwill of the firm was valued at Rs. 2,80,000

(vi) remaining partners decided to pay off cash immediately to the Retiring partners by bringing in cash in the new profit sharing ratio and also to leave a balance of Rs1,00,000 in their bank account.

(vii) they will also adjust their capitals in their new ratio which was 3:4 Prepare Revaluation Account & Capital Accounts of Partners only

(6)

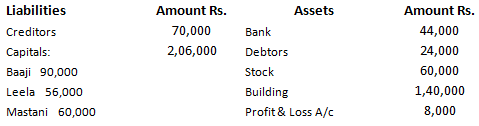

Q8. Baaji, Leela and Mastani were partners in a firm sharing profits in the ratio of 5:3:2. Their Balance Sheet on March 31, 2015 was as follows:

On April 1,2015 Leela retired on the following terms:

i. Building was to be depreciated by 10,000.

ii. A Provision of 5% was to be made on Debtors for doubtful debts.

iii. Salary outstanding was 4,800.

iv. Goodwill of the firm was valued at 1,40,000.

v. Leela was to be paid 20,800 through cheque and the balance was to be paid in two equal quarterly

installments (starting from June 30, 2015) along with interest @ 10% p.a.

Prepare Revaluation Account, partners’s Capital Account and leela Loan Account till it is finally paid.

(8)

|

42 videos|168 docs|43 tests

|

FAQs on Important Questions - Retirement (Accounting for Partnership Firms and Companies) - Accountancy Class 12 - Commerce

| 1. What are the benefits of retirement accounting for partnership firms and companies? |  |

| 2. How is retirement accounting different for partnership firms and companies? | |

| 3. What are the different types of retirement benefits provided by partnership firms and companies? | |

| 4. How can retirement accounting help in financial planning? | |

| 5. What are the legal obligations of partnership firms and companies towards retirement benefits? | |

|

16.2K Views |

|

4.70/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

Summary

,Exam

,MCQs

,ppt

,Free

,Important Questions - Retirement (Accounting for Partnership Firms and Companies) | Accountancy Class 12 - Commerce

,Viva Questions

,Previous Year Questions with Solutions

,Important questions

,Sample Paper

,practice quizzes

,Objective type Questions

,shortcuts and tricks

,Important Questions - Retirement (Accounting for Partnership Firms and Companies) | Accountancy Class 12 - Commerce

,study material

,past year papers

,video lectures

,Semester Notes

,Extra Questions

,mock tests for examination

,Important Questions - Retirement (Accounting for Partnership Firms and Companies) | Accountancy Class 12 - Commerce

;

Important Questions - Retirement (Accounting for Partnership Firms and Companies) Free PDF Download

Importance of Important Questions - Retirement (Accounting for Partnership Firms and Companies)

Important Questions - Retirement (Accounting for Partnership Firms and Companies) Notes

Important Questions - Retirement (Accounting for Partnership Firms and Companies) Commerce

Study Important Questions - Retirement (Accounting for Partnership Firms and Companies) on the App

|

© EduRev

|

Education Revolution

|

|