ICAI Notes 1 - Introduction to Microeconomics - CA Foundation PDF Download

Learning Objectives

- know what Economics is about.

- know about the nature of Economics.

- understand the various methods of studying Economics.

- understand the basic problems of an economy.

- understand how different economies solve their basic problems.

- get an insight into the tool of Production Possibilities Curve.

1.0 WHAT IS ECONOMICS ABOUT?

Consider the following situation. It is your birthday and your mother gives you Rs. 500 as birthday gift. You are free to spend the money as you like. What will you do? You have many options before you, like :

Option 1 : You can give a party to your friends and spend the whole money on them.

Option 2 : You can buy yourself a dress for Rs. 500.

Option 3 : You can go for a movie and eat in some restaurant.

Option 4 : You can buy yourself a book and save some money.

What do you notice? You have so many options before you. You will have to go for one option or a combination of one or more options. But why can’t you have everything? Given the choice you would like to spend not only on your friends, but would also like to see movie, eat in the restaurant, buy a dress and a book and save some money. But you cannot. Why? Because you have only 500 Rupees with you. Had your mother given you Rs. 1,500, you might have satisfied more of your demands. Thus you are in dilemma. Similar dilemma is faced by every individual, every society and every country in this world. Life is like that. Because we cannot have every thing all at once, we are forever forced to make choices. We can use our resources to satisfy only some of our wants, leaving many others unsatisfied.

These two fundamental facts that

(i) Human beings have unlimited wants; and

(ii) The means of satisfying these wants are relatively scarce form the subject matter of Economics. Economics is, thus, the study of how we work together to transform scarce resources into goods and services to satisfy the most pressing of our infinite wants and how we distribute these goods and services among ourselves. The term ‘Economics’ owes its origin to the Greek word ‘Oikonomia’ meaning ‘household’.

This definition of Economics, in terms of using scarce resources to satisfy human wants, is correct but it is incomplete. It brings to our mind the picture of a society with fixed resources, skills and productive capacity deciding what specific kinds of goods it ought to produce and how they ought to be distributed. Yet two of the most important concerns of modern economies are not fully covered by this concept.

On the one hand, the productive capacity of modern economies has grown tremendously. Population and labour force have increased, new sources of raw materials have been discovered, and new and better plant and equipment have been made available on farms and in factories and mines. Not only has the quantity of available productive resources increased, their quality has also been greatly improved. Education and newly acquired skills have raised the productivity of the labour force, and led to the discovery of completely new kinds of natural resources like petroleum and atomic energy. On the other hand, the resulting growth in production and income has not been smooth. There have been periods in which output not only failed to grow but also actually declined sharply. During such periods factories and workers remained idle due to insufficient demand.

Economics, therefore, concerns itself not just with how a nation allocates to various uses its scarce productive resources, important as that may be. It also deals with the process by which the productive capacity of these resources is increased and with the factors which in the past have led to sharp fluctuations in the rate of utilisation of resources.

In the day-to-day events we come across several economic problems like changes in price of individual commodities as well as general price level changes; the economic prosperity and higher standards of living of some people despite general poverty of the masses in India; the problems of unemployment of certain class of persons or in some areas are some of the matters connected with economic analysis. The study of Economics will help in analysing the possible causes contributory to these problems and might suggest a number of alternative courses, which could be adopted for tackling these problems. However, it is necessary to remember that most economic problems are of complex nature which are affected by several forces, some of which are rooted in Economics and some in political set up, social norms, etc. The study of Economics cannot ensure that all the problems will be tackled but surely it would enable a student to examine a problem in its right perspective and would help him in finding suitable measures to tackle those problems.

1.1 DEFINITIONS AND SCOPE OF ECONOMICS

Several definitions of Economics have been given. For the sake of convenience let us classify the various definitions into four groups :

1. Science of wealth

2. Science of material well-being

3. Science of choice making and

4. Science of dynamic growth and development We shall examine each one of these briefly.

1. Science of wealth : Some earlier economists defined Economics as follows : The classical economists defined Economics in terms of “The Science of Wealth”. Adam Smith, also known as the father of modern Economics, published his masterpiece “An Enquiry into the Nature and Causes of Wealth of Nations” in the year 1776. He defined Economics as: “An inquiry into the nature and causes of the wealth of the nations” by Adam Smith. “Science which deals with wealth” by J.B. Say. In the above definitions wealth becomes the main focus of the study of Economics. The definition of Economics, as science of wealth, had some merits. The important ones are :

(i) It highlighted an important problem faced by each and every nation of the world, namely creation of wealth.

(ii) Since the problems of poverty, unemployment etc. can be solved to a greater extent when wealth is produced and is distributed equitably; it goes to the credit of Adam Smith (called the father of Economics) and his followers to have addressed to the problems of economic growth and increase in the production of wealth. (iii) By considering the problems of production, distribution and exchange of wealth, classical economists focused attention on the important issues with which Economics is concerned.

The study of Economics as a ‘Science of Wealth’ has been criticised on several grounds. The main criticisms levelled against this definition are;

(i) Adam Smith and other classical economists concentrated only on material wealth. They totally ignored creation of immaterial wealth like services of doctors, chartered accountants etc.

(ii) The advocates of Economics as ‘science of wealth’ concentrated too much on the production of wealth and ignored social welfare. This makes their definition incomplete and inadequate.

2. Science of material well-being : Under this group of definitions the emphasis is on welfare as compared with wealth in the earlier group. Alfred Marshall, the neo-classicist, raised Economics from its ignoble position to a noble one. It was he who shifted the emphasis from wealth to welfare. According to him, “Economics is a study of mankind in the ordinary business of life. It examines that part of individual and social action which is most closely connected with the attainment and with the use of the material requisites of well-being. Thus, it is on the one side a study of wealth and on the other and more important side a part of the study of the man” Alfred Marshall.

Another definition: “The range of our inquiry becomes restricted to that part of social welfare that can be brought directly or indirectly into relation with the measuring rod of money” A.C. Pigou.

In the first definition Economics has been indicated to be a study of mankind in the ordinary business of life. By ordinary business we mean those activities which occupy considerable part of human effort. The fulfillment of economic needs is a very important business which every man ordinarily does. Professor Marshall has clearly pointed that Economics is the study of wealth but more important is the study of man. Thus, man gets precedence over wealth. There is also emphasis on material requisites of well-being. Obviously, the material things like food, clothing and shelter, are very important economic objectives.

The second definition by Pigou emphasises social welfare but only that part of it which can be related with the measuring rod of money. Money is general measure of purchasing power by the use of which the science of Economics can be rendered more precise. Marshall’s and Pigou’s definitions of Economics are wider and more comprehensive as they take into account the aspect of social welfare. But their definitions have their share of criticism.

Their definitions are criticised on the following grounds.

(i) Economics is concerned with not only material things but also with immaterial things like services of singes, teachers, actors etc. Marshall and Pigou chose to ignore them.

(ii) Robbins criticised the welfare definition on the ground that it is very difficult to state which things would lead to welfare and which will not. He is of the view that we would study in Economics all those goods and services which carry a price whether they promote welfare or not.

3. Science of choice making : Prof. Lionel Robbins of the London School of Economics gave a new definition to Economics in his famous book “Nature and significance of Economics” which he brought out in 1931. According to Robbins, Economics studies the problems which have arisen because of the scarcity of resources. Nature has not provided mankind sufficient resources to satisfy all its wants. Therefore, people have to choose for which ends or for which wants the resources are to be utilized. Robbins gave a more scientific definition of Economics. His definition is as follows : “Economics is the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses”.

The definition deals with the following four aspects :

(i) Economics is a science : Economics studies economic human behaviour scientifically. It studies how humans try to optimise (maximize or minimize) certain objective under given constraints. For example, it studies how consumers, with given income and prices of the commodities, try to maximize their satisfaction.

(ii) Unlimited ends : Ends refer to wants. Human wants are unlimited. When one want is satisfied, other wants crop up. If man’s wants were limited, then there would be no economic problem.

(iii) Scarce means : Means refer to resources. Since resources (natural productive resources, man-made capital goods, consumer goods, money and time etc.) are limited economic problem arises. If the resources were unlimited, people would be able to satisfy all their wants and there would be no problem.

(iv) Alternative uses : Not only resources are scarce, they have alternative uses. For example, coal can be used as a fuel for the production of industrial goods, it can be used for running trains, it can also be used for domestic cooking purposes and for so many purposes.

Similarly, financial resources can be used for many purposes. The man or society has, therefore, to choose the uses for which resources would be used. If there was only a single use of the resource then the economic problem would not arise.

It follows from the definition of Robbins that Economics is a science of choice. An important thing about Robbin’s definition is that it does not distinguish between material and non-material, between welfare and non-welfare. Anything which satisfies the wants of the people would be studied in Economics. Even if a good is harmful to a person it would be studied in Economics if it satisfies his wants.

No doubt, Robbins has made Economics a scientific study and his definition has become popular among some economists. But his definition has also been criticised on several grounds. Important ones are :

(i) Robbins has made Economics quite impersonal and colourless. By making it a complete positive science and excluding normative aspects he has narrowed down its scope.

(ii) Robbins’ definition is totally silent about certain macro-economic aspects such as determination of national income and employment. (iii) His definition does not cover the theory of economic growth and development. While Robbins takes resources as given and talks about their allocation, it is totally silent about the measures to be taken to raise these resources i.e. national income and wealth.

4. Science of dynamic growth and development : Although the fundamental economic problem of scarcity in relation to needs is undisputed, it would not be proper to think that economic resources - physical, human, financial are fixed and cannot be increased by human ingenuity, exploration, exploitation and development. A modern and somewhat modified definition is as follows :

“Economics is the study of how men and society choose, with or without the use of money, to employ scarce productive resources which could have alternative uses, to produce various commodities over time and distribute them for consumption now and in the future amongst various people and groups of society”.

Paul A. Samuelson

The above definition is very comprehensive because it does not restrict to material well-being or money measure as a limiting factor. But it considers economic growth over time.

Prof Henry Smith also gave an all inclusive definition of Economics. According to him, Economics, is the “the study of how in a civilized society one obtains the share of what other people have produced and of how the total product of society changes and is determined”. By civilized society it is meant that there are some legal institutions as well as rights of property and other things in the society.

Jacob Viner has given a pragmatic definition of Economics. According to him, “Economics is what Economists do”. In other words, what economists do and what they have been doing.

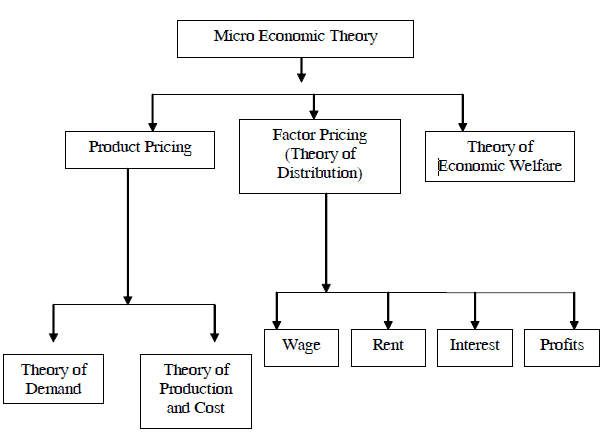

Micro and Macro-Economics: The subject-matter of Economics has been divided into two parts - Micro-Economics and Macro Economics. In Micro-Economics we study the economic behaviour of an individual, firm or industry in the national economy. It is thus a study of a particular unit rather than all the units combined. It is basically concerned with the mechanism of allocation of given resources. Further, it is a partial equilibrium analysis as it seeks to determine price and output in an industry independent of those in other industries. The term Micro Economics is derived from the Greek word mikros, meaning “small”. We mainly study the following in Micro-Economics :

(i) product pricing; |

(ii) consumer behaviour;

(iii) factor pricing;

(iv) economic conditions of a section of the people;

(v) study of firms; and

(vi) location of a industry.

Thus, when we are studying how a producer fixes the prices of his products, we are studying Micro-Economics. Similarly, when we are studying why an industry is located at a particular place, we are studying Micro-Economics. The whole content of micro Economics theory is presented in the following chart;

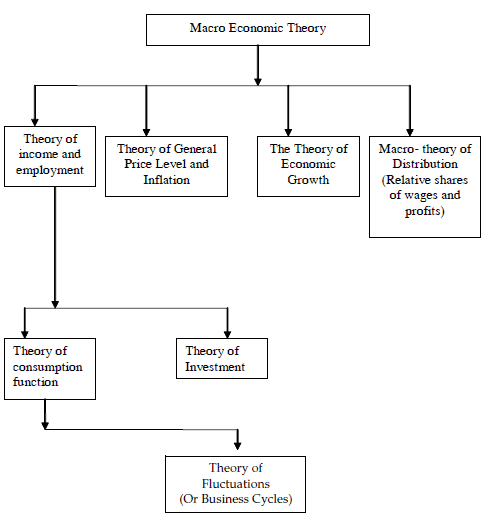

The term Macro Economics is derived from the Greek word makros, meaning “large”.

In Macro-Economics, we study the economic behaviour of the large aggregates such as the overall conditions of the economy such as total production, total consumption, total saving and total investment in it. It is the study of overall economic phenomena as a whole rather than its individual parts. It includes :

(i) national income and output;

(ii) general price level;

(iii) balance of trade and payments;

(iv) external value of money;

(v) saving and investment; and

(vi) employment and economic growth. Thus, when we study why we continue to have balance of payments deficits, or why the value of rupee vis-à-vis dollar is falling or why saving rates are high or low in a particular country we are studying Macro-Economics. The various aspects of macro economic theory are shown in the following chart:

1.2 NATURE OF ECONOMICS

Under this, we generally discuss whether Economics is science or art or both and if it is a science whether it is a positive science or a normative science or both. Economics – As a science and as an art :

Often a question arises – whether Economics is a science or an art or both.

(a) Economics is a science : A subject is considered science if

1. It is a systematised body of knowledge which studies the relationship between cause and effect.

2. It is capable of measurement.

3. It has its own methodological apparatus.

4. It should have the ability to forecast.

If we analyse Economics, we find that it has all the features of science. Like science it studies cause and effect relationship between economic phenomena. To understand, let us take the law of demand. It explains the cause and effect relationship between price and demand for a commodity. It says, given other things constant, as price rises, the demand for a commodity falls and vice versa. Here the cause is price and the effect is fall in quantity demanded. Similarly like science it is capable of being measured, the measurement is in terms of money. It has its own methodology of study (induction and deduction) and it forecasts the future market condition with the help of various statistical and non-statistical tools.

But it is to be noted that Economics is not a perfect science. This is because

1. Economists do not have uniform opinion about a particular event.

2. The subject matter of Economics is the economic behaviour of man which is highly unpredictable.

3. Money which is used to measure outcomes in Economics is itself a dependent variable.

4. It is not possible to make correct predictions about the behaviour of economic variables.

(b) Economics is an art : Art is nothing but practice of knowledge. Whereas science teaches us to know art teaches us to do. Unlike science which is theoretical, art is practical. If we analyse Economics, we find that it has the features of an art also. Its various branches, consumption, production and public finance etc. provide practical solutions to various economic problems. It helps in solving various economic problems which we face in our day-to-day life.

Thus, Economics is both a science and an art. It is science in its methodology and art in its application. Study of unemployment problem is science but framing suitable policies for reducing the extent of unemployment is an art.

Economics as Positive Science and Economics as Normative Science

(i) Positive Science : As stated above, Economics is a science. But the question arises whether it is a positive science or a normative science. A positive or pure science analyses cause and effect relationship between variables but it does not pass value judgment. In other words, it states what is and not what ought to be. Professor Robbins emphasised the positive aspects of science but Marshall and Pigou have considered the ethical aspects of science which obviously are normative.

Positive Economics is the one that simply states facts and uses empirical evidence. An example of positive statement is: “According to the law of demand, a lower price will yield more quantity sold”.

According to Robbins, Economics is concerned only with the study of the economic decisions of individuals and the society as positive facts but not with the ethics of these decisions. Economics should be neutral between ends. It is not for economists to pass value judgments and make pronouncements on the goodness or otherwise of human decisions. An individual with a limited amount of money may use it for buying liquor and not milk, but that is entirely his business. A community may use its limited resources for making guns rather than butter, but it is no concern of the economists to condemn or appreciate this policy. Economics only studies facts and makes generalisations from them. It is a pure and positive science, which excludes from its scope the normative aspect of human behaviour.

Complete neutrality between ends is, however, neither feasible nor desirable. It is because in many matters the economist has to suggest measures for achieving certain socially desirable ends. For example, when he suggests the adoption of certain policies for increasing employment and raising the rates of wages, he is making value judgments; or that the exploitation of labour and the state of unemployment are bad and steps should be taken to remove them. Similarly, when he states that the limited resources of the economy should not be used in the way they are being used and should be used in a different way; that the choice between ends is wrong and should be altered, etc. he is making value judgments.

(ii) Normative Science : As normative science, Economics involves value judgments. It is prescriptive in nature and describes ‘what should be the things’. Normative Economics is the one that takes values into account, and results in statements like: “This tax should be reduced.” For example, the questions like what should be the level of national income, what should be the wage rate, how the fruits of national product be distributed among people - all fall within the scope of normative science. Thus, normative economics is concerned with welfare propositions. Some economists are of the view that value judgments by different individuals will be different and thus for deriving laws or theories, it should not be used.

To conclude, we may say that while laying down laws or theories, Economics may be treated as pure and positive Economics, but as a tool of practical application it must have some normative goals in view.

1.3 METHODS OF STUDY

In Economics, there are two methods of deriving generalisations or laws. These are deductive method and inductive method.

Deductive method : This method is also called abstract, analytical and priori method. Under this method laws are deduced logically. On the basis of certain fundamental assumptions or accepted axioms or truths which have been established and handed down from generation to generation, conclusions and generalisations are drawn. The logic proceeds from general to particular. This method is called abstract or a priori because it is based on abstract reasoning and not on actual facts. However, actual situation may differ from what deductive logic suggests For example, it is assumed that man is rational and on the basis of this it is deduced that he will buy cheap and sell dear. But in actual situation this may not happen, say, because of absence of proper knowledge and market conditions.

The principal steps in the process of deriving economic generalizations through deductive logic are (a) perception of the problem (b) defining the technical terms and making appropriate assumptions (c) deducing hypothesis and (d) testing of hypothesis deduced.

Many theories and generalisation have been established in Economics with the help of deductive method such as inverse relationship between price and quantity demanded, the direct relationship between price and quantity supplied etc. But this method also suffers from certain handicaps such as

(i) assumptions generally turn out to be untrue or partially true

(ii) valid conclusions cannot be drawn in the absence of proper knowledge of the whole situation and

(iii) it is dangerous to claim universal validity for the economic generalisations so deduced.

Inductive Method : Under this method conclusions are drawn on the basis of collection and analysis of facts relevant to the inquiry. The logic in this case proceeds from the particular to the general. The generalisations are based on observation of individual examples.

The principal steps in this method are

(i) perception of the problem

(ii) collection, classification and analysis of data by using appropriate statistical techniques

(iii) finding out the reasons for the relationship established through statistical analysis and to set rules for the verification of the principles. Many researches in macro-economics have been obtained through inductive method such as principle of acceleration describing the factors which determine investment in an economy, the nature of consumption function describing the relationship between income and consumption etc.

Inductive method is increasingly being used because

(i) statistical induction leads to precise, exact and measurable conclusions

(ii) it underlines the importance of relativity of economic laws

(iii) it shows that generalisations are valid only under certain conditions.

But this method suffers from

(i) risk of hurried conclusions having being drawn from an insufficient number of facts

(ii) difficulties involved in the collection of facts

(iii) the fact that observation and experimentation have very limited application in a science that deals with human activities.

However, the two methods are not mutually exclusive and are used side by side in any scientific inquiry. Conclusions drawn from the deductive method of reasoning and are verified by inductive method of observing concrete facts of life.

For example, the hypothesis of rationality may be tested and verified by the observation of the behaviour of people.

Marshall rightly pointed out, “induction and deduction are both needed for scientific thought as the right and left foot are both needed for walking”.

1.4 CENTRAL ECONOMIC PROBLEMS

As discussed before, human wants are unlimited and productive resources such as land and other natural resources, raw materials, capital equipments etc. with which goods and services are produced to satisfy those wants are scarce. The problem of scarcity of resources is felt not only by individuals but also by the society as a whole. This gives rise to the problem of how to use scarce resources to attain maximum satisfaction. This is generally called ‘the economic problem’. Every economic system, be it capitalist, socialist or mixed, has to deal with this central problem of scarcity of resources relative to wants for them. The central economic problem is further divided into four basic economic problems.

These are :

(i) What to produce?

(ii) How to produce?

(iii) For whom to produce?

(iv) What provisions (if any) are to be made for economic growth?

(i) What to produce? : Every society has to decide which goods are to be produced and in what quantities. Whether more guns should be produced or more butter should be produced; or whether more capital goods like machines, equipments, dams etc., will be produced or more consumer goods such as bread will be produced. Not only the society has to decide about what goods are to be produced it has also to decide in what quantities these goods would be produced. In nutshell, a society must decide how much wheat, how many hospitals, how many schools, how many machines, how many meters of cloths etc. have to be produced.

(ii) How to produce? : There are various alternative techniques of producing a commodity. For example, cotton cloth can be produced with either handlooms or power looms or automatic looms. Production with handlooms involves use of more labour and production with automatic loom involves use of more machines and capital. A society has to decide whether it will produce cotton cloth using labour intensive techniques or capital intensive techniques. Likewise for all goods and services it has to decide whether to use labour intensive techniques or capital intensive techniques. Obviously, the choice would depend on the availability of different factors of production (i.e. labour and capital) and their relative prices. It is in the society’s interest to use those techniques of production that make best use of the available resources.

(iii) For whom to produce? : Another important decision which a society has to take is for whom to produce. The society can not satisfy all wants of all the people. Therefore, it has to decide who should get how much of the total output of goods and services. In other words, it has to decide about the shares of different people in the national cake of goods and services.

(iv) What provision should be made for economic growth? : A society would not like to use all its scarce resources for current consumption only. This is because if it uses all the resources for current consumption and no provision is made for future production, the society’s production capacity would not increase. This implies that incomes or standards of living of the people would remain stagnant and in future, the levels of living may decline. Therefore, a society has to decide how much saving and investment (i.e. how much sacrifice of current consumption) should be made for future progress.

1.5 PRODUCTION POSSIBILITIES CURVE

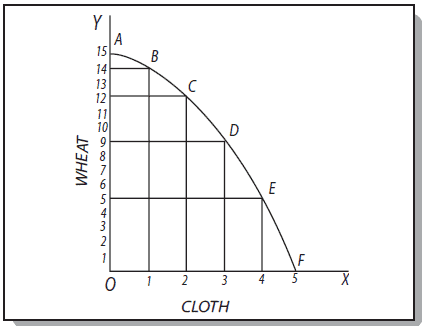

The nature of basic problems explained above can be better understood with the help of an important tool of Economics known as Production Possibilities Curve (PPC). Production possibilities curve graphically represents the alternative production possibilities facing an economy.

In Economics, a production-possibility curve (PPC) or “transformation curve” is a graph that shows the different rates of production of two goods that an individual or group can efficiently produce with limited productive resources. The PPF shows the maximum obtainable amount of one commodity for any given amount of another commodity or composite of all other commodities, given the society’s technology and the amount of factors of production available.

In order to understand PPC, let us assume that there are two types of goods – wheat and cloth which are to be produced. We also assume that

(1) there is a given amount of productive resources and they remain fixed;

(2) resources are neither unemployed nor underemployed; and (3) technology does not change. Now consider the following table :

Table : 1

Alternative Production Possibilities

| Production possibilities | Cloth (in thousand metres) | Wheat (in thousand quintals) | Opportunity cost |

A | 0 | 15 | |

| B | 1 | 14 | 1 |

| C | 2 | 12 | 2 |

| D | 3 | 9 | 3 |

| E | 4 | 5 | 4 |

| F | 5 | 0 | 5 |

The above table shows various production possibilities between wheat and cloth. If all the given resources are employed for the production of wheat, 15 thousand quintals of wheat are produced. On the other hand, if all the resources are employed for the production of cloth, 5 thousand meters of cloth are made. But these two are extreme production possibilities. In between these two there will be many other production possibilities such as B, C, D and E. With production possibility B, the economy can produce with given resources one thousand meter of cloth and 14 thousand quintals of wheat and with production possibility C, it can produce 2 thousand meters of cloth and 12 thousand quintals of wheat. Thus, as the economy is moving from one possibility to another, it takes away some resources from wheat and put them in the production of cloth. Since resources are limited and we have assumed that they are fully employed, the economy has to give up something of one good to obtain some more of the other.

The production possibilities shown above can be illustrated diagrammatically also as is shown in the Figure 1.

Fig. 1 : Production Possibilities Curve

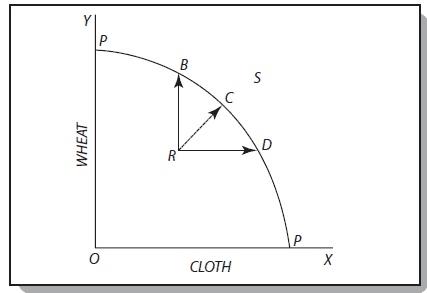

The curve AF is called Production Possibilities Curve (PPC) or Production Possibilities Frontier (PPF). This curve shows the various combinations of two goods which the economy can produce with a given amount of resources. Since the given resources are fully employed and utilized, the combination of two goods produce can lie anywhere on the production possibilities curve AF but not inside or outside it. For example, the combined output of two goods can neither lie at R nor at S (Figure 2). This is because at point R the economy would not be utilising its resources fully and at point S, the economy would not have capability to produce with the given technology.

Fig. 2 : Production Possibilities Curve

Opportunity Cost and Production Possibilities Curve

Suppose after completing your chartered accountancy course, you have two options open to you. One, to join a company which gives you Rs. 8 lakh annually and second, to start your practice and earn Rs. 6 lakh. Now, if you join the company, you will earn Rs. 8 lakh annually but you will not get Rs. 6 lakh. This Rs. 6 lakh is your opportunity cost for serving in the company and not starting your practice. Most generally, the opportunity cost of a given activity is defined as the value of the next best activity.

In the context of PPC, since there are only two goods, therefore opportunity cost of producing one good is in terms of sacrifice made of the other good. In table 1, we have found opportunity cost of producing additional units of cloth in terms of wheat. Thus, as the economy moves from possibility A to possibility B, it has to give up one thousand quintal of wheat in order to have one thousand meters of cloth. Thus, first thousand meters of cloth have the opportunity cost of one thousand quintals wheat to the economy. But as we step up the production of cloth and move further from B to C, extra two thousand quintals of wheat have to be foregone for producing extra one thousand meters of cloth. In other words, opportunity cost goes on increasing as we have more of cloth and less of wheat. It is this principle of increasing opportunity cost that makes the PPC concave to the origin. If opportunity costs were constant, PPC would be a straight line. But generally, we get increasing opportunity costs. This is because a given resource is suitable more for the production of one good than another. Thus, in our example, land is more suitable for the production of wheat than cloth. As we increase the production of cloth, resources which are less productive in the production of cloth would have to be pushed in it. Thus, more units of that resource would be required to produce cloth. In other words, greater sacrifice would have to be made in terms of production of wheat for every extra production of cloth. This law holds good if we move from A to F or from F to A on the PPC.

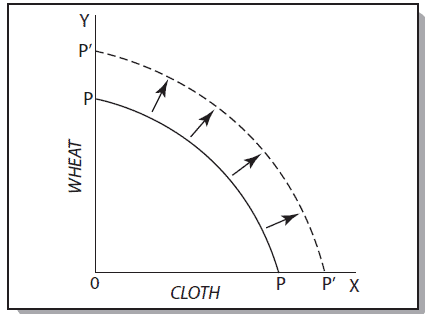

Economic growth and shift in Production Possibility Curve

All points on PPC curve show that goods and services are produced at least cost and no resource is wasted i.e. an economy is productively efficient. But that does not mean there is no scope of progress. When the economy makes progress in technology, that is, when scientists and engineers discover new and better ways of doing things, the production possibilities curve will shift outward and to the right showing that more of both goods can be produced than before (see Fig. 3)

Fig. 3 : Shift in PPC due to economic growth

Figure 3 shows that technological progress allows the society to produce more of both goods with a given and fixed amount of resources. Thus, with P’ P’, more amount of wheat and cloth can be produced than before with the given amount of inputs. It is to be noted that if the economy is producing at point R (in Fig. 2), then it is not using its resources fully i.e. its resources are unemployed. A Shift from inside the PPC (Say R) to anywhere on the PPC (Say to B) indicates that the resources which were lying unutilised are now being utilised fully. But a movement from one PPC to another PPC on the right indicates economic growth of the economy. This movement becomes possible because of an improvement in the overall technology, greater capital formation, an increase in the population growth etc.

1.6 HOW DIFFERENT ECONOMIES SOLVE THEIR CENTRAL ECONOMIC PROBLEMS?

An economic system refers to the sum total of the arrangements for the production and distribution of goods and services in a society. You must be wondering how different economies of the world would be solving their central problems. In order to understand this, we divide all the economies into three broad classifications based on their mode of production, exchange, distribution and the role which government plays in economic activity. These are :

- Capitalist economy

- Socialist economy

- Mixed economy

Capitalist economy : Capitalism is an economic system in which all the means of production are owned and controlled by private individuals for profit. In short, private property is the mainstay of capitalism and profit motive is its driving force. The government is not supposed to interfere in the management of economic affairs under this system. An economy is called capitalist or a free market economy if it has the following characteristics :

(1) The right of private property : The right of private property means that productive factors such as land, factories, machinery, mines etc. are under private ownership. The owners of these factors are free to use them in the manner in which they like. The government may, however, put some restrictions for the benefit of the society in general.

(2) Freedom of enterprise : This means that everybody engages in any economic activity he likes. More specifically he is free to set up any firm to produce goods.

(3) Freedom to choice by the consumers : This means people in a capitalist economy are free to spend their income as they like. This is known as consumer sovereignty. Consumers are sovereign in the sense producers produce only those goods which consumers wish to buy.

(4) Profit motive : In a capitalist economy it is the profit motive which forces or induces people to work and produce.

(5) Competition : Competition prevails among sellers to sell their goods and among buyers to obtain goods to satisfy their wants. Advertisement, price-cutting, discounts etc. are very common methods of competition in a capitalist economy.

(6) Inequalities of incomes : There is generally a wide gap of income between the rich and the poor in the economy which mainly arises due to unequal distribution of property in such economies.

How capitalist economies solve their central problems?

A capitalist economy has no central planning authority to decide what, how and for whom to produce. In absence of any central authority it looks like a miracle as to how such an economy functions. If the consumers want cars, producers choose to make cloth and workers choose to work for the furniture industry, there will be total confusion and chaos in the country. But this is not so. Such an economy uses the impersonal forces of the market demand and supply or the price mechanism to solve its central problems.

Deciding what to produce : The aim of an entrepreneur is to earn as much profits as possible. This causes businessmen to compete with one another to produce those goods which consumers wish to buy. Thus, if consumers want more cars, there will be an increase in the demand for cars and as a result their prices will increase. A rise in the price of cars, cost remaining the same, will lead to more profits. This will induce producers to produce more cars. On the other hand, if the consumers’ demand for cloth decreases, its price would fall and profits would go down and hence its production would also go down. Thus, more of cars and less of cloth will be produced in such an economy. Thus, in a capitalist economy (like the USA, UK, and Germany) the question regarding what to produce is ultimately decided by consumers who show their preferences by spending on the goods which they want.

Deciding how to produce : An entrepreneur will produce his goods with that technique of production which renders his cost of production minimum. If labour is relatively cheap he will use labour intensive method and if labour is relatively costlier he will use capital intensive method. Thus, the relative prices of factors of production help in deciding how to produce.

Deciding for whom to produce : Goods and services in a capitalist economy will be produced for those who have the buying capacity. The buying capacity of an individual depends upon his income. How much income he will be able to make depends not only on the amount of work he does and the prices of the factors he owns but also on how much property he owns. Higher the income, higher will be his buying capacity and higher generally will be his demand for goods in general.

Deciding about consumption, saving and investment : Consumption and savings are done by consumers and investments are done by entrepreneurs. Consumers savings, among other factors, are governed by the rate of interest prevailing in the market. Higher the interest rate, higher are the savings. Investment decisions depend upon the rate of return on capital. The greater the profit expectation (i.e. the return on capital), the greater will be the investment in a capitalist economy. The rate of interest on savings and the rate of return on capital are nothing but the prices of capital. Thus, we see above what goods are produced, by which methods they are produced, for whom they are produced and what provisions should be made for economic growth are all decided by price mechanism or market mechanism.

Merits of Capitalist economy:

1. To attract the consumer the producer will bring out newer and finer varieties of goods.

2. The existence of private property and the driving force of profit motive results in high standard of living.

3. Capitalism works automatically through the price mechanism.

4. The freedom of enterprise results in maximum efficiency in production.

5. All activities under capitalism enjoy the maximum amount of liberty and freedom.

6. Under capitalism freedom of choice brings maximum satisfaction to consumers

7. Capitalism preserves fundamental rights such as right to freedom and right to private property.

8. It rewards men of initiative and enterprise.

9. Country as a whole benefits through growth of business talents, development of research, etc.

Demerits of Capitalism

1. In capitalism the enormous wealth produced is apportioned by a few. This causes rich, richer and poor, poorer.

2. Welfare is not protected under capitalism, because here the aim is profit and not the welfare of the people.

3. Economic instability in terms of over production, economic depression, unemployment, etc. is very common under capitalism.

4. The producer spends huge amounts of money on advertisement and sale promotion activities like fair, exhibitions etc.

5. Class conflict arises between employer and employee. They will be paid low wages and this leads to strikes and lock-outs.

6. Productive resources are misused under capitalism. They are used for the production of luxuries as they will bring high profits.

7. Capitalism leads to the formation of monopolies.

8. There is no security of employment under capitalism.

Socialist economy : In this economy, the material means of production i.e. factories, capital, mines etc. are owned by the whole community represented by the State. All members are entitled to get benefit from the fruits of such socialised planned production on the basis of equal rights. Some important characteristics of this economy are :

Here, production and distribution of goods are aimed at maximizing the welfare of the community as a whole.

(i) There is collective ownership of all means of production except small farms, workshops and trading firms which may remain in private hands. As a result of social ownership, profit-motive and self- interest are not the driving force of economic activity as it is in the case of a market economy. The resources here are used to achieve certain socio-economic objectives.

(ii) There is a central authority to set and accomplish socio-economic goals; that is why it is called a centrally planned economy. Major economic decisions, such as what to produce, when and how much to produce, etc., are taken by the central authority.

(iii) Freedom from hunger is guaranteed but consumers’ sovereignty gets restricted by selective production of goods. The range of choice is limited by planned production. However, within that range an individual is free to choose what he likes most. The right to work is guaranteed but the choice of occupation gets restricted because these are determined by some authority on the basis of certain socio-economic goals before the nation.

(iv) A relative equality of income is an important feature. Among other things, differences are narrowed down by lack of opportunities to accumulate private capital. Educational and other facilities are enjoyed more or less equally; thus the basic causes of inequalities are removed.

(v) Price mechanism exists in a socialist economy but it has only a secondary role, e.g., to secure disposal of accumulated stocks. Since allocation of productive resources is done according to a predetermined plan, the price mechanism as such does not influence these decisions. In the absence of the profit motive, price mechanism loses its predominant role in economic decisions. The erstwhile U.S.S.R. is an example of socialist economy. In today’s world there is no country which is purely socialist.

Merits of Socialism

1. Equitable distribution of wealth and income and provision of equal opportunities for all help to maintain social justice.

2. In socialistic economy there will be better utilization of resources and it ensures the maximum production. Socialist economy means planned economy.

3. Waste of all kinds is avoided through strict economic planning.

4. In planned economy unemployment is removed, business fluctuation are eliminated and stability is brought about and maintained.

5. The absence of profit motive helps the community to develop a co-operative mentality and avoids classwar.

6. Socialism ensures right to work and minimum standard of living to people.

7. Under socialisms the labourers and consumers are protected from the exploitation by the employer and monopolies respectively.

Demerits of Socialism

1. Socialism involves the predominance of bureaucracy. Moreover, there may also be corruption, red-tapism, favouritism, etc.

2. It restricts the freedom of individuals as there is state ownership of the material means of production and state direction and control of economic activity.

3. Socialism takes away such right as the right of private property.

4. It will not provide necessary incentive to hard work in the form of profit.

5. There is no proper basis for cost calculation. In the absence of such practice, the most economic and scientific allocation of resources and the efficient functioning of the economic system are impossible.

6. State monopolies created by socialism will sometime become uncontrollable. This will be more dangerous than the private monopolies under capitalism.

7. Under socialism the consumers have no freedom of choice. Therefore, what state produces has to be accepted by the consumers.

8. The extreme form of socialism is not at all practicable.

The Mixed Economy : In a mixed economy the aim is to develop a system which tries to include the best features of both the controlled economy and the market economy while excluding the demerits of both. It appreciates the advantages of private enterprise and private property with their emphasis on self-interest and profit motive. Vast economic development of England, the USA etc. is due to private enterprise. At the same time, it is noticed that private property, profit motive and self interest of the market economy may not promote the interests of the community as a whole and as such the government should remove these defects of private enterprise. For this purpose, the government itself must run important and selected industries and eliminate the free play of the profit motive and self-interest. Private enterprise which has its own significance is also allowed to play the positive role in a mixed economy.

The concept of mixed economy is of recent origin. J.M. Keynes, one of the greatest economists of the 20th century favoured the idea of a mixed economy as a compromise between socialism and capitalism.

Features of a mixed economy

The first important feature of a mixed economy is the co-existence of both private and public enterprise. In fact, in a mixed economy, there are three sectors of industries:

(a) Private sector

Production and distribution are managed and controlled by private individuals and groups. Industries in this sector are based on self-interest and profit motive. The system of private property exists and personal initiative is given full scope. However private enterprise may be regulated by the government directly and or indirectly by a number of policy instruments.

(b) Public sector

Industries in this sector are not primarily profit-oriented but are set up by the State for the welfare of the community.

(c) Combined sector

A sector in which both the government and the private enterprises have equal access, and join hands to produce a commodity, leading to the establishment of joint sectors.

Secondly, a mixed economy is a planned economy, i.e. an economy in which the government has a clear and definite economic plan. Public sector enterprises have to work according to a plan and to achieve the objectives laid down. The government has also to create necessary atmosphere for the private sector to develop on its own. Thus it must prepare plans of development for both the private and the public sector enterprises. Allocation of resources in a mixed economy should be better since it attempts to combine the productive efficiency of capitalism and distributive justice of socialism.

Thirdly, in a mixed economy balanced regional development is expected. Public sector enterprises may be located in the backward regions so as to ensure its development. Further by way of subsidies and other incentives private sector may be lured to establish and develop industries in backward regions.

Fourthly, in a mixed economy, a dual system of pricing exists. In private sector, prices of goods and factors of production are determined through the free play of market forces of demand and supply. In public sector, the state determines prices of various products. The state reserves itself the right to keep different prices for public sector units and private sector units. The state may also fix the prices of certain essential commodities which are used by the common man.

For example, in India, the prices of essential commodities like diesel, LPG, are fixed by government. Overall planning is done by the State Authority called Planning Commission in countries like India who have adopted mixed economy.

Merits of Mixed Economy

1. Mixed economy secures the merits of both capitalism and socialism while avoiding the evils of both.

2. Mixed economy protects individual freedom. Under the system, individuals have the freedom of consumption, choice of occupation, freedom of enterprise and freedom of expression.

3. Price mechanism is allowed to operate under mixed economy.

4. Reducing the inequalities of wealth and class struggle is one of the aims of mixed economy.

5. Economic fluctuations can be avoided due to centrally planned economy. 6. Mixed economy helps under-developed countries to have rapid and balanced economic development.

Demerits of Mixed Economy

1. Mixed economy is difficult to operate. Balancing and adjusting the public and private sector is often difficult.

2. Excessive controls and heavy taxes are likely to prevail under mixed economy. These will discourage production in the private sector.

3. Problems of red-tapism, nepotism, favouritism, officialdom, etc. are also found in this type of economic system.

4. Mixed economy is described by Schumpeter as “Capitalism in the oxygen tent”. According to him it is only a trick of the capitalists to cheat the working class by offering them some temporary advantage like social security, uplift of the depressed classes, etc.

SUMMARY

Economics deals with the laws and principles which govern the functioning of an economy and its various parts. An economy exists because of two basic facts. Firstly, human wants for goods and services are unlimited and secondly, productive resources with which to produce goods and services are scarce. Therefore, an economy has to decide how to use its scarce resources to obtain the maximum possible satisfaction of the members of the society. It is this basic problem of scarcity which gives rise to many of the economic problems. There has been a lot of controversy among economists about the true content of economic theory or its subject matter.

The subject-matter and scope of economics has been variously defined. Each definition is incomplete and inadequate and because of various conflicting definitions, some confusion has been created about the nature and scope of economics.

The subject matter of economics has been divided into two parts : - Micro-economics and Macro-economics. Micro-economics deals with the analysis of small individual units of the economy such as individual consumers, firms, industries and markets. On the other hand, macro-economics concerns itself with the analysis of the economy as a whole and its large aggregates such as total national income, output, employment etc.

The problems of scarcity and choice-making can be depicted using the tool of production possibilities curve. The basic economic problems of what, how and for whom to produce can be solved in many ways by an economy. If it gives the whole charge of the economy, to private ownership we get capitalist economy, to public ownership we get socialist economy and jointly to private and public ownership we get mixed economy.

FAQs on ICAI Notes 1 - Introduction to Microeconomics - CA Foundation

| 1. What is microeconomics? |  |

| 2. What are the key concepts of microeconomics? | |

| 3. What is the difference between microeconomics and macroeconomics? | |

| 4. What are the applications of microeconomics? | |

| 5. What is the importance of microeconomics in the CA Foundation exam? | |

|

20.2K Views |

|

4.84/5 Rating |

|

Nov 15, 2024 Last updated |

|

Explore Courses for CA Foundation exam

|

|

shortcuts and tricks

,mock tests for examination

,Free

,Viva Questions

,Exam

,Previous Year Questions with Solutions

,Extra Questions

,past year papers

,ICAI Notes 1 - Introduction to Microeconomics - CA Foundation

,Summary

,Objective type Questions

,practice quizzes

,Important questions

,ICAI Notes 1 - Introduction to Microeconomics - CA Foundation

,Sample Paper

,Semester Notes

,video lectures

,ICAI Notes 1 - Introduction to Microeconomics - CA Foundation

,ppt

,study material

,MCQs

;

ICAI Notes 1 - Introduction to Microeconomics Free PDF Download

Importance of ICAI Notes 1 - Introduction to Microeconomics

ICAI Notes 1 - Introduction to Microeconomics

ICAI Notes 1 - Introduction to Microeconomics CA Foundation Questions

Study ICAI Notes 1 - Introduction to Microeconomics on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|