Residential Status (Section 5 to 9) | Fast Track Quick Revision Income Tax - Taxation PDF Download

| Section 6 : Determination of Residential Status | |||||

| (1) | (2) | (3) | (4) | (5) | (6) |

| Ind | HUF, Firm, AOP/ BOI | Company | Local Auth. / AJP | Ind / HUF | |

| Basic Condition | Additional condition | ||||

| Satisfies | Do not satisfiy | x | Satisfies | Do not satisfy | |

| Resident | Non - Resident | R-OR | R-NOR | ||

| S 6(1) & 6(6). Determination of Residential Status of Individual. | |||

| S 6(1) : Basic Condition | |||

| If an Individual is present in India | |||

| (a) | for period or periods of atleast 182 days in the relevant PY; or | Satisfies any one basic condition | Resident in India. |

| for atleast 60 days in the relevant PY & atleast 365 days in last 4 years immediately preceding the relevant PY | |||

| (b) | Do not satisfies any basic condition | Non - Resident in India. | |

| Exceptions to the basic condition -check only 182 days | |

| (a) | If an Indian Citizen leaves India for the purpose of employment or leaves India as a crew member of Indian Ship. |

| (b) | If an Indian Citizen or Person of Indian Origin comes to India on a visit from outside India. |

| As per explanation to S 115C(e) A Person is said to be of Indian Origin if he himself or his Parents / Grandparents are borne in undivided India. Check date of birth should be before 15-8-1947 and place of birth is in India, Pakistan or Bangladesh. | |

| S 6(6) : Additional Condition | |||

| (a) | Resident in India for atleast 2 years in last 10 years immediately preceding the relevant PY; and | } | If satisfies both the Additional Condition then RS is R-OR otherwise R-NOR. |

| (b) |

Present in India for atleast 730 days in last 7 years immediately preceding the relevant PY. |

||

| Residential Status of other person | Control & Management of the affairs of the business (POEM) | |||

| S 6(2) | HUF / Firm / AOP / BOI | In India | Outside India | |

| S 6(3) | Foreign Company | Wholly / Partially | Wholly | |

| S 6(4) | Local authority / AJP | |||

| Resident | Non - Resident | |||

Note : Residential Status of Indian Company is always resident irrespective of control and management of affairs of the business.

Note : Place of effective management to mean a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are, in substance made. It simply means the place where board meetings are held or that person to whom board of directors have delegated the entire policy decision of company. E.g. Managing Director, Manager who has control and management.

| S 5. Incidence of tax | ||||||

| R - OR | R - NOR | NR | ||||

| 1. | Income which accrues or arise in India. (Indian Income) | Taxable | Texable | Texable | ||

|

2

|

Income which accrues or arise outside India. (Foreign Income) | Taxable | Not Taxable. However in case of | Not Taxable but if income is received in India then taxable. | ||

| Business Income | Professional Income | |||||

| Taxable if business is controlled from India | Taxable if Profession is set up in India | |||||

| Taxable if any income is received in India. | ||||||

| S 9(1). Income deemed to accrue or arise in India | |||

| 1. | • Income from Business Connection. Business outside India and part activity of business carried out in India. Also called permanent establishment or territorial nexus. |

Exceptions to the Business Connection. | |

| a. | All operation not carried out in India. | ||

| b. | Purchase for export. | ||

| c. | Collection of news. | ||

| d. | Shooting of film in India by foreign citizen. | ||

| • Assets located in India. | |||

| 2. | Services rendered in India by any person. | ||

| 3. |

Services rendered outside India by Indian Citizen. Employer is Govt. of India. However as per S 10(7) allowances and perquisites are exempt from tax. Only basic salary is taxable. |

||

| 4. | Dividend from Indian Company. However it is exempt from tax u/s 10(34) | ||

| 5. | Interest on Loan which is used in India. | If interest, royalty or FTS is payable by Govt. of India then such income deemed to accrue or arise in India whether there is business connection or not. | |

| 6. | Royalty from knowledge which is used in India. | ||

| 7. | Fees from technical services where technical agreement is implemented in India. | ||

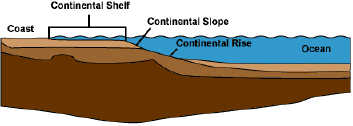

| Section 2(25A). India includes territorial waters of India, its continental shelf, air space above territorial waters and exclusive economic zone. | Oil Rig |

|

|

|

|

|

24 videos|28 docs

|

FAQs on Residential Status (Section 5 to 9) - Fast Track Quick Revision Income Tax - Taxation

| 1. What is residential status for taxation purposes? |  |

| 2. How is residential status determined for taxation? | |

| 3. What are the tax implications for residents and non-residents? | |

| 4. Can an individual be a resident for tax purposes in multiple countries? | |

| 5. Are there any tax benefits or exemptions available to non-residents? | |

Important questions

,Viva Questions

,Residential Status (Section 5 to 9) | Fast Track Quick Revision Income Tax - Taxation

,past year papers

,Exam

,video lectures

,Residential Status (Section 5 to 9) | Fast Track Quick Revision Income Tax - Taxation

,MCQs

,Summary

,Semester Notes

,Previous Year Questions with Solutions

,Extra Questions

,Free

,Residential Status (Section 5 to 9) | Fast Track Quick Revision Income Tax - Taxation

,shortcuts and tricks

,Sample Paper

,study material

,mock tests for examination

,ppt

,practice quizzes

,Objective type Questions

;

Residential Status (Section 5 to 9) Free PDF Download

Importance of Residential Status (Section 5 to 9)

Residential Status (Section 5 to 9) Notes

Residential Status (Section 5 to 9) Taxation Questions

Study Residential Status (Section 5 to 9) on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!