Taxation Exam > Taxation Notes > Fast Track Quick Revision Income Tax > Income from Other Sources (Section 56 to 59)

Income from Other Sources (Section 56 to 59) | Fast Track Quick Revision Income Tax - Taxation PDF Download

| Sections | Particulars | Provisions | ||||

| 56. | Charge | 56(1) | Any income which is not charged under the first 4 head is charged under the head ‘Income from Other Sources‘. E.g. |

|||

| Director’s, MP’s, MLA’s, salary |

Rent from vacant land. |

Income from sub letting. |

Interest | |||

| Royalty | ||||||

| 56(2) | Following incomes are always charged under the ‘OS‘ | |||||

| Gifts | Dividend | Lottery income |

Rent of Plant |

|||

| 57. | Amount expressly allowed as deduction. |

Expenditure should be incurred wholly and exclusively for earning S 56 income. E.g. (a) Interest on loan taken for purchase of bond. (b) Collection charges. (c) Contribution towards PF |

||||

| 58. | Restriction on deduction. |

Following deductions are not allowed. E.g. Expenses incurred in earning lottery income. | ||||

| 59. | Deemed income |

As per S 41. (Refer PGBP) | ||||

| S 56(2). GIFTS | |||||

| Part A | Part B | Part C | |||

| Nature of gift | Cash Gift | Land & Building on or after 1-10-2009 |

JAD PB SAS on or after 1-10-2009 |

||

| Donor / Seller | Any Person | Any person | Any person | ||

| Donee / Buyer | Ind / HUF | Ind / HUF | Ind / HUF | ||

| Consideration | Nil | Nil or inadequate consideration |

Nil or inadequate consideration |

||

| In excess of certain amount taxable in the year of receipt |

Cash in excess of Rs. 50,000 in aggregate is taxed u/h OS |

a. | Stamp duty value exceeds Rs.50,000 taxed |

a. | FMV in excess of aggregate ₹ 50,000 taxed |

| b. | Difference = (SDV – PP) in excess of Rs. 50,000 taxed |

b. | Difference = (FMV – PP) in excess of aggregate Rs. 50,000 taxed |

||

| Exceptions to Part A, B & C | |||

| 1. | Gifts received from any relative | 4. | Gifts received on the marriage of the individual |

| 2. | Gifts received under a will or inheritance. | 5. | Gifts received in contemplation of death of the payer |

| 3. | Money received from local authority. | 7. | Money received from a registered charitable institute |

| 7. | Money received from any fund, foundation, university, other educational institution, medical institution. | ||

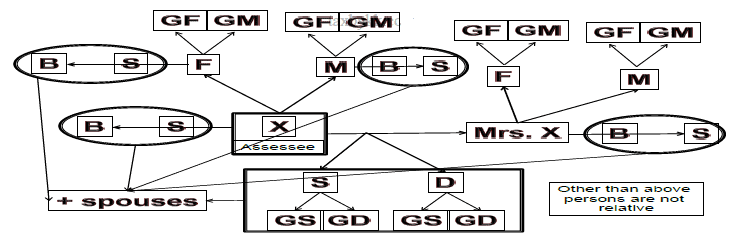

| S 56(2). Relative | |||

| Other Incomes charged under the head other sources | |||||||||||

| 1. | Life insurance maturity proceeds if premium for any year exceeds 10% of assured amount. |

4. | Family pension less (1/3rd or ₹ 15,000 whichever is lower). |

||||||||

| 2. | Owning & maintaining race horses. | 5. | Letting of plant & machinery. | ||||||||

| 3. | Composite letting of building + P & M. | 6. | Lottery income. No deduction. | ||||||||

| 7. | Maturity proceeds of keyman insurance policy. |

|

|||||||||

| Interest on Securities | |||

| Securities held as |

Stock in Trade | Interest charged under the head Business. S 28 to 44D. | S 37. Interest on loan & collection charges to run business is allowed as deduction. |

| Investment | Interest charged under the head Other Sources. S 56 to 59. | S 57. Interest on loan & collection charges allowed as deduction. | |

| S 10(15). Following interest exempt from tax. | |||||

| Post office scheme |

Full exemption |

(a) Cash Certificates (b) Fixed deposit (c) Cumulative time deposit account (CTD). |

Note : Interest on Monthly scheme is not exempt interest is fully taxable. | ||

| Partial exemption |

(d) Saving account |

Single | upto Rs. 3,500 exempt | ||

| Joint | upto Rs. 7,000 exempt | ||||

| Interest on Govt. Securities |

a. | Interest on RBI Relief bonds | Interest on other Govt. Securities are fully taxable under the head Other Sources | ||

| b. | Interest on Gold Bonds. | ||||

| S 10(4) | Interest on Non Resident External Account is fully exempt from tax | ||||

| Dividend | ||||

| Securities held as |

Stock in Trade |

Dividend always charged under the head Other Sources. S 56 to 59. |

from Indian Company |

from foreign Company |

| Investment | Exempt u/s 10(34) |

Texable | ||

| S 57. Interest on loan & collection charges allowed as deduction if dividend is taxable. | ||||

| Interim Dividend : Taxable in the year of receipt. | Final Dividend : Taxable in the year of declaration. | |||

| S 10(35). Income from units of mutual fund is exempt from tax. | ||||

The document Income from Other Sources (Section 56 to 59) | Fast Track Quick Revision Income Tax - Taxation is a part of the Taxation Course Fast Track Quick Revision Income Tax.

All you need of Taxation at this link: Taxation

|

24 videos|28 docs

|

FAQs on Income from Other Sources (Section 56 to 59) - Fast Track Quick Revision Income Tax - Taxation

| 1. What are the different types of income that fall under the category of "Income from Other Sources"? |  |

Ans. Income from Other Sources includes income that is not classified under any other specific category of income, such as salary, business profits, or capital gains. Examples include interest on savings accounts, rental income, income from royalty, income from letting out machinery, and gifts received exceeding Rs. 50,000.

| 2. Is income from winnings in lotteries, crossword puzzles, or game shows also considered as "Income from Other Sources"? | |

Ans. Yes, income from winnings in lotteries, crossword puzzles, or game shows is considered as "Income from Other Sources." Such income is taxable under Section 56 of the Income Tax Act. The income is taxable at a flat rate of 30% without any deductions.

| 3. Are gifts received from relatives taxable under "Income from Other Sources"? | |

Ans. No, gifts received from relatives are not taxable under "Income from Other Sources." According to the Income Tax Act, gifts received from specified relatives, including parents, siblings, and grandparents, are exempt from tax. However, if the gift received exceeds Rs. 50,000 in value, it would be taxable.

| 4. How is rental income taxed under "Income from Other Sources"? | |

Ans. Rental income is taxed under "Income from Other Sources" as per the provisions of the Income Tax Act. The rental income received is added to your total income and taxed at the applicable slab rates. However, you can claim deductions for certain expenses related to the property, such as municipal taxes, repairs, and maintenance.

| 5. Can income from interest on fixed deposits be considered as "Income from Other Sources"? | |

Ans. Yes, income from interest on fixed deposits is considered as "Income from Other Sources." Any interest earned on fixed deposits, whether with banks or other financial institutions, is taxable as per the income tax slab rates applicable to the individual. It is important to mention this income while filing your income tax return to ensure compliance with tax laws.

About this Document

1.6K Views

4.66/5

Rating

Oct 17, 2025

Last updated

Related Exams

Document Description: Income from Other Sources (Section 56 to 59) for Taxation 2025 is part of Fast Track Quick Revision Income Tax preparation.

The notes and questions for Income from Other Sources (Section 56 to 59) have been prepared according to the Taxation exam syllabus. Information about Income from Other Sources (Section 56 to 59) covers topics

like and Income from Other Sources (Section 56 to 59) Example, for Taxation 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Income from Other Sources (Section 56 to 59).

Introduction of Income from Other Sources (Section 56 to 59) in English is available as part of our Fast Track Quick Revision Income Tax

for Taxation & Income from Other Sources (Section 56 to 59) in Hindi for Fast Track Quick Revision Income Tax course.

Download more important topics related with notes, lectures and mock test series for Taxation

Exam by signing up for free. Taxation: Income from Other Sources (Section 56 to 59) | Fast Track Quick Revision Income Tax - Taxation

Description

Full syllabus notes, lecture & questions for Income from Other Sources (Section 56 to 59) | Fast Track Quick Revision Income Tax - Taxation - Taxation | Plus excerises question with solution to help you revise complete syllabus for Fast Track Quick Revision Income Tax | Best notes, free PDF download

Information about Income from Other Sources (Section 56 to 59)

In this doc you can find the meaning of Income from Other Sources (Section 56 to 59) defined & explained in the simplest way possible. Besides explaining types of

Income from Other Sources (Section 56 to 59) theory, EduRev gives you an ample number of questions to practice Income from Other Sources (Section 56 to 59) tests, examples and also practice Taxation

tests

Related Searches

ppt

,mock tests for examination

,Sample Paper

,Extra Questions

,Free

,shortcuts and tricks

,past year papers

,Semester Notes

,Income from Other Sources (Section 56 to 59) | Fast Track Quick Revision Income Tax - Taxation

,Income from Other Sources (Section 56 to 59) | Fast Track Quick Revision Income Tax - Taxation

,Income from Other Sources (Section 56 to 59) | Fast Track Quick Revision Income Tax - Taxation

,Important questions

,study material

,Summary

,Previous Year Questions with Solutions

,Objective type Questions

,practice quizzes

,MCQs

,Exam

,video lectures

,Viva Questions

;

Additional Information about Income from Other Sources (Section 56 to 59) for Taxation Preparation

Income from Other Sources (Section 56 to 59) Free PDF Download

The Income from Other Sources (Section 56 to 59) is an invaluable resource that delves deep into the core of the Taxation exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Income from Other Sources (Section 56 to 59) now and kickstart your journey towards success in the Taxation exam.

Importance of Income from Other Sources (Section 56 to 59)

The importance of Income from Other Sources (Section 56 to 59) cannot be overstated, especially for Taxation aspirants.

This document holds the key to success in the Taxation exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Income from Other Sources (Section 56 to 59) Notes

Income from Other Sources (Section 56 to 59) Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Income from Other Sources (Section 56 to 59).

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Income from Other Sources (Section 56 to 59) Notes on EduRev are your ultimate resource for success.

Income from Other Sources (Section 56 to 59) Taxation Questions

The "Income from Other Sources (Section 56 to 59) Taxation Questions" guide is a valuable resource for all aspiring students preparing for the

Taxation exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Income from Other Sources (Section 56 to 59) on the App

Students of Taxation can study Income from Other Sources (Section 56 to 59) alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Income from Other Sources (Section 56 to 59),

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Income from Other Sources (Section 56 to 59) is prepared as per the latest Taxation syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up

within 7 days!

within 7 days!

Takes less than 10 seconds to signup