Taxation Exam > Taxation Notes > Fast Track Quick Revision Income Tax > Mixed Topics - Part - 1

Mixed Topics - Part - 1

| Salary for different purpose | |

| Entertainment allowance | Basic Salary |

| Gratuity covered | Basic salary + 100% of DA |

| Gratuity others | SAS. Average of last 10 months preceding the month of retiring |

| Leave Salary | SAS Average of last 10 month preceding the date of retirement |

| HRA | SAS |

| Accommodation | Basic Salary+ DA () + Any commission + taxable allowances |

| 80CCD | SAS |

| Members of household | Family Members | Relative |

| Both the above words are used in Chapter Salary. | Relative word is used in 3 chapters. PGBP, Other Sources & Clubbing of Income | |

| Section 2(41). Meaning of Relative | |||

| Box 1 | Box 2 | Box 3 | |

| Self, Spouse & children | Brother & Sister | Lineal ascendent | Father, mother, grandfather, grandmother |

| Lineal descendent | Son, Daughter, Grandson, Granddaughter | ||

| The above definition of relative is used in following 2 places | |||

| PGBP | Section 40A(2) | Payment made to relatives | |

| Clubbing of income | Section 64(1) (ii) | Remuneration to spouse from a concern in which such individual has substantial interest. | |

| Meaning of relative at different places | ||||

| Income from Salaries | Medical facilities | Spouse, children (dependant or not dependant), Parents, brothers, sisters wholly and mainly dependent on such individual | ||

| Leave Travel Concession. | ||||

| Other Perquisites. Rule 3 | Members of Household | Self, spouse, children and their spouses, parents, servants and dependants | ||

| PGBP | Payment to specified persons. S 2(41) | Relative, partner, director, or person having a substantial interest or relative of any such person. Relative means spouse, brother, sister or any lineal ascendant or descendant of such individual. | ||

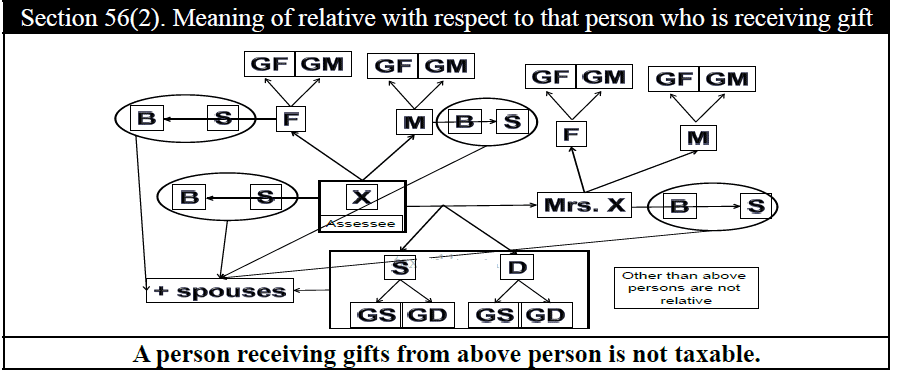

| Other Sources | Gifts, S 56(2) | (i) Spouse of the individual, | ||

| (ii) Brother or sister of the individual, | ||||

| (iii) Brother or sister of the spouse of the individual, | ||||

| (iv) Brother or sister of either of the parents of the individual, | ||||

| (v) Any lineal ascendant or descendant of the individual, | ||||

| (vi) Any lineal ascendant or descendant of the spouse of individual. | ||||

| (vii) Spouse of a person referred to in items (ii) to (vi) | ||||

| Clubbing of Income | Substantial interest. | S 2(41). Relative means spouse, brother, sister or any lineal ascendant or descendant of such individual. | ||

| Dedn u/s 80C to 80U | 80C | Ind : LIP on life of self, spouse and children | HUF : any member of HUF | |

| 80D | Ind : Self, Spouse & dependant children. | Parents (dependant or not dependant) | HUF : any member of HUF | |

| 80DD, 80DDB | Ind, Spouse & children | Parents, brothers and sisters wholly and mainly dependent on such individual | HUF : any member of HUF | |

| 80 E | Self, Spouse, children of individual | |||

| Charitable Trusts | S11 | Interested person. Relative is as defined in S 56(2). | ||

The document Mixed Topics - Part - 1 is a part of the Taxation Course Fast Track Quick Revision Income Tax.

All you need of Taxation at this link: Taxation

FAQs on Mixed Topics - Part - 1

| 1. What is taxation? |  |

Ans. Taxation is the practice of imposing mandatory charges on individuals or entities by the government in order to fund public expenses and services. These charges, known as taxes, are levied on income, property, goods and services, and various financial transactions.

| 2. What are the different types of taxes? | |

Ans. There are several types of taxes imposed by governments, including income tax, property tax, sales tax, value-added tax (VAT), excise tax, estate tax, and corporate tax. Each type of tax serves a specific purpose and is collected through different methods.

| 3. How is income tax calculated? | |

Ans. Income tax is calculated based on the individual's or business's taxable income, which is the total income earned minus any deductions or exemptions. The tax rates vary depending on the income brackets set by the government, with higher income earners generally facing higher tax rates.

| 4. What is the difference between tax evasion and tax avoidance? | |

Ans. Tax evasion refers to the illegal act of deliberately evading taxes by underreporting income, inflating deductions, or hiding assets to avoid paying the full amount owed. On the other hand, tax avoidance is the legal practice of minimizing tax liability by taking advantage of available deductions, credits, and exemptions within the bounds of the law.

| 5. What are some common tax deductions and credits available to individuals? | |

Ans. Common tax deductions and credits available to individuals include the standard deduction, itemized deductions (such as mortgage interest, medical expenses, and charitable contributions), child tax credit, earned income credit, and education-related credits (such as the American Opportunity Credit and Lifetime Learning Credit). These deductions and credits can help reduce the amount of tax owed or increase the taxpayer's refund.

About this Document

4.68/5 Rating

Apr 21, 2026 Last updated

Related Exams

Document Description: Mixed Topics - Part - 1 for Taxation 2026 is part of Fast Track Quick Revision Income Tax preparation. The notes and questions for Mixed Topics - Part - 1 have been prepared according to the Taxation exam syllabus. Information about Mixed Topics - Part - 1 covers topics like and Mixed Topics - Part - 1 Example, for Taxation 2026 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Mixed Topics - Part - 1.

Introduction of Mixed Topics - Part - 1 in English is available as part of our Fast Track Quick Revision Income Tax for Taxation & Mixed Topics - Part - 1 in Hindi for Fast Track Quick Revision Income Tax course. Download more important topics related with notes, lectures and mock test series for Taxation Exam by signing up for free. Taxation: Mixed Topics - Part - 1

Description

Mixed Topics of Fast Track Quick Revision Income Tax covers all the important topics, helping you prepare for the Taxation exam on EduRev. Start for free!

Information about Mixed Topics - Part - 1

In this doc you can find the meaning of Mixed Topics - Part - 1 defined & explained in the simplest way possible. Besides explaining types of Mixed Topics - Part - 1 theory, EduRev gives you an ample number of questions to practice Mixed Topics - Part - 1 tests, examples and also practice Taxation tests

Related Searches

Extra Questions, MCQs, pdf , study material, video lectures, Mixed Topics - Part - 1, Sample Paper, Previous Year Questions with Solutions, ppt, Semester Notes, practice quizzes, Important questions, Exam, Summary, Objective type Questions, past year papers, Mixed Topics - Part - 1, mock tests for examination, Mixed Topics - Part - 1, Free, Viva Questions, shortcuts and tricks;