IIFT Reading Comprehension MCQ - 1 - CAT MCQ

16 Questions MCQ Test - IIFT Reading Comprehension MCQ - 1

Group Question

The passage given below is followed by a set of questions. Choose the most appropriate answer to each question.

The critics who denigrate advertising attack not only advertising but also by logical necessity capitalism, ethical egoism, and reason. As an institution in the division of labor and an instrument of capitalistic production, advertising communicates to many people at one time, the availability and nature of need- and want-satisfying products. In essence, advertising is salesmanship via the mass media; as such, it is the capitalist’s largest sales force and most effective means of delivering information to the market. In addition, advertising by its essential nature blatantly and unapologetically appeals to the self-interest of consumers for the blatant and selfish gain of capitalists. To criticize advertising is to criticize capitalism and ethical egoism. At the most fundamental level, the attacks on advertising are an assault on reason on man’s ability to form concepts and to think in principles because advertising is a conceptual communication to many people at one time about the conceptual achievements of others. It is attacked for precisely this aspect of its nature. The goal of advertising is to sell products to consumers, and the means by which this goal is achieved is to communicate what advertisers call the “product concept.” An advertisement is itself an abstraction, a concept of what the capitalist has produced. Thus, advertising is a conceptual communication in a market economy to self-interested buyers about the self-interested, conceptual achievements of capitalists. To criticize advertising at the most fundamental level - is to assault man’s consciousness.

From its earliest days, critics attacked capitalism for its dependence on the profit motive and the pursuit of self-interest. As the most visible manifestation, or “point man” of capitalism, advertising can be called the capitalist’s “tool of selfishness.” In a world culture based on altruism and self-sacrifice, it is amazing that advertising has lasted as long as it has. Indeed, its growth was stunted in Great Britain and Ireland for 141 years by a tax on newspapers and newspaper advertising. If selfishness is the original sin of man, according to Judeo-Christian ethics, then surely advertising is the original sin of capitalism. More accurately, advertising is the serpent that encourages man to pursue selfish gain and, in subtler form, to disobey authority. In contemporary economics, pure and perfect competition is the Garden of Eden in which the lion lies down beside the lamb and this “dirty, filthy” advertising is entirely absent-because consumers allegedly have perfect information. Small wonder that advertising does not have a good press. At the level of fundamental ideas, three attacks on advertising constitute the assault on consciousness. One attack attributes to advertising the coercive power to force consumers to buy products they do not need or want. At the level of metaphysics, this attack denies the volitional nature of reason, that is, free will; consequently, it denies, either explicitly or implicitly, the validity of human consciousness as such. A second attack derides advertising for how offensive it allegedly is; ultimately, critics advocate regulation to control the allegedly offensive advertising. At root - that is, at the level of ethics this attack denies that values are objective, that values are a product of the relation between material objects and a volitional consciousness that evaluates them. Consequently, it denies the existence of rational options.

A third attack, which derives from contemporary economics, views advertising as a tool of monopoly power. At the level of epistemology, however, this attack denies the possibility of truth and certainty, because reason allegedly is impotent to know reality; all man can do is emulate the methods of physics, by conducting statistically controlled experiments, and attempt to establish an uncertain, probabilistic knowledge. These three assaults on consciousness form the philosophic foundations of what are commonly known as the “social” and “economic” criticisms of advertising, the first two forming the foundation of the “social” criticisms, the third the foundation of the economic criticisms. The quantity of literature that attacks advertising approaches the infinite. The list of complaints is long, and each one has many variations. Explicitly or implicitly, all attacks attribute to advertising the power to initiate physical force against both consumers and competitors. The “social” criticisms assert that advertising adds no value to the products it promotes; therefore, it is superfluous, inherently dishonest, immoral, and fraudulent. The economic criticisms assert that advertising increases prices and wastes society’s valuable resources; therefore, advertising contributes to the establishment of monopoly power.

In essence, there are two “social” criticisms. The first explicitly charges advertising with the power to force consumers to buy products they do not need or want; the second implicitly charges advertising with this power. According to the first, advertising changes the tastes and preferences of consumers by coercing them to conform to the desires of producers. For example, consumers may want safer auto-mobiles, but what they get, according to the critics, are racing stripes and aluminum hubcaps. Forcing consumers to conform to the desires of producers, the critics point out, is the opposite of what advocates of capitalism claim about a free- market economy-namely, that producers conform to the tastes and preferences of consumers. Within the first criticism there are two forms. The more serious claims that advertising, by its very nature, is inherently deceptive, because it manipulates consumers into buying products they do not need or want. The most specific example of this criticism is the charge of subliminal advertising. Thus, when looking at a place mat in front of you at a Howard Johnson’s restaurant, with its picture of the fried clam special, you might be deceived and manipulated into changing your taste. The other form claims that advertising is “merely” coercive, by creating needs and wants that otherwise would not exist without it. That is, highly emotional, persuasive, combative advertising - as opposed to rational, informative, and constructive advertising - is claimed to be a kind of physical force that destroys consumer sovereignty over the free market. This is Galbraith’s “dependence effect,” so called because our wants, he claims, are dependent on or created by the process by which they are satisfied- the process of production, especially advertising and salesmanship. Our wants for breakfast cereal and laundry detergent, says Galbraith, are contrived and artificial. The psychology of behaviorism has strongly influenced this second form of the first “social” criticism.

Both forms of the “coercive power” charge refer repeatedly to the advertising of cigarettes, liquor, drugs, sports cars, deodorant, Gucci shoes, and color television sets as evidence of advertising’s alleged power to force unneeded and unwanted products on the poor, helpless consumer. The charge of manipulation and deception is more serious than “mere” coercion because manipulation is more devious; a manipulator can make consumers buy products they think are good for them when, in fact, that is not the case. The charge of manipulation, in effect, views advertising as a pack of lies. The charge of “mere” coercion, on the other hand, claims that advertising is just brute force; advertising in this view, in effect, is excessively pushy. According to the second “social” criticism, advertising offends the consumer’s sense of good taste by insulting and degrading his intelligence, by promoting morally offensive products, and by encouraging harmful and immoral behavior. Prime targets of this “offensiveness” criticism are Mr. Whipple and his Charmin bathroom tissue commercials, as well as the “ring around the collar” commercials of Wisk liquid detergent and the Noxzema “take it all off’ shaving cream ads. But worse, the critics allege, advertising promotes products that have no redeeming moral value, such as cigarettes, beer, and pornographic literature. Advertising encourages harmful and immoral behavior and therefore is itself immoral. Although this criticism does not begin by attributing coercive power to advertising, it usually ends by supporting one or both forms of the first “social” criticism, thus calling for the regulation or banishment of a certain type of offensive-meaning coercive-advertising.

Q. Which of the following statements is incorrect according to the passage?

The critics who denigrate advertising attack not only advertising but also by logical necessity capitalism, ethical egoism, and reason. As an institution in the division of labor and an instrument of capitalistic production, advertising communicates to many people at one time, the availability and nature of need- and want-satisfying products. In essence, advertising is salesmanship via the mass media; as such, it is the capitalist’s largest sales force and most effective means of delivering information to the market. In addition, advertising by its essential nature blatantly and unapologetically appeals to the self-interest of consumers for the blatant and selfish gain of capitalists. To criticize advertising is to criticize capitalism and ethical egoism. At the most fundamental level, the attacks on advertising are an assault on reason on man’s ability to form concepts and to think in principles because advertising is a conceptual communication to many people at one time about the conceptual achievements of others. It is attacked for precisely this aspect of its nature. The goal of advertising is to sell products to consumers, and the means by which this goal is achieved is to communicate what advertisers call the “product concept.” An advertisement is itself an abstraction, a concept of what the capitalist has produced. Thus, advertising is a conceptual communication in a market economy to self-interested buyers about the self-interested, conceptual achievements of capitalists. To criticize advertising at the most fundamental level - is to assault man’s consciousness.

The critics who denigrate advertising attack not only advertising but also by logical necessity capitalism, ethical egoism, and reason. As an institution in the division of labor and an instrument of capitalistic production, advertising communicates to many people at one time, the availability and nature of need- and want-satisfying products. In essence, advertising is salesmanship via the mass media; as such, it is the capitalist’s largest sales force and most effective means of delivering information to the market. In addition, advertising by its essential nature blatantly and unapologetically appeals to the self-interest of consumers for the blatant and selfish gain of capitalists. To criticize advertising is to criticize capitalism and ethical egoism. At the most fundamental level, the attacks on advertising are an assault on reason on man’s ability to form concepts and to think in principles because advertising is a conceptual communication to many people at one time about the conceptual achievements of others. It is attacked for precisely this aspect of its nature. The goal of advertising is to sell products to consumers, and the means by which this goal is achieved is to communicate what advertisers call the “product concept.” An advertisement is itself an abstraction, a concept of what the capitalist has produced. Thus, advertising is a conceptual communication in a market economy to self-interested buyers about the self-interested, conceptual achievements of capitalists. To criticize advertising at the most fundamental level - is to assault man’s consciousness.

From its earliest days, critics attacked capitalism for its dependence on the profit motive and the pursuit of self-interest. As the most visible manifestation, or “point man” of capitalism, advertising can be called the capitalist’s “tool of selfishness.” In a world culture based on altruism and self-sacrifice, it is amazing that advertising has lasted as long as it has. Indeed, its growth was stunted in Great Britain and Ireland for 141 years by a tax on newspapers and newspaper advertising. If selfishness is the original sin of man, according to Judeo-Christian ethics, then surely advertising is the original sin of capitalism. More accurately, advertising is the serpent that encourages man to pursue selfish gain and, in subtler form, to disobey authority. In contemporary economics, pure and perfect competition is the Garden of Eden in which the lion lies down beside the lamb and this “dirty, filthy” advertising is entirely absent-because consumers allegedly have perfect information. Small wonder that advertising does not have a good press. At the level of fundamental ideas, three attacks on advertising constitute the assault on consciousness. One attack attributes to advertising the coercive power to force consumers to buy products they do not need or want. At the level of metaphysics, this attack denies the volitional nature of reason, that is, free will; consequently, it denies, either explicitly or implicitly, the validity of human consciousness as such. A second attack derides advertising for how offensive it allegedly is; ultimately, critics advocate regulation to control the allegedly offensive advertising. At root - that is, at the level of ethics this attack denies that values are objective, that values are a product of the relation between material objects and a volitional consciousness that evaluates them. Consequently, it denies the existence of rational options.

A third attack, which derives from contemporary economics, views advertising as a tool of monopoly power. At the level of epistemology, however, this attack denies the possibility of truth and certainty, because reason allegedly is impotent to know reality; all man can do is emulate the methods of physics, by conducting statistically controlled experiments, and attempt to establish an uncertain, probabilistic knowledge. These three assaults on consciousness form the philosophic foundations of what are commonly known as the “social” and “economic” criticisms of advertising, the first two forming the foundation of the “social” criticisms, the third the foundation of the economic criticisms. The quantity of literature that attacks advertising approaches the infinite. The list of complaints is long, and each one has many variations. Explicitly or implicitly, all attacks attribute to advertising the power to initiate physical force against both consumers and competitors. The “social” criticisms assert that advertising adds no value to the products it promotes; therefore, it is superfluous, inherently dishonest, immoral, and fraudulent. The economic criticisms assert that advertising increases prices and wastes society’s valuable resources; therefore, advertising contributes to the establishment of monopoly power.

In essence, there are two “social” criticisms. The first explicitly charges advertising with the power to force consumers to buy products they do not need or want; the second implicitly charges advertising with this power. According to the first, advertising changes the tastes and preferences of consumers by coercing them to conform to the desires of producers. For example, consumers may want safer auto-mobiles, but what they get, according to the critics, are racing stripes and aluminum hubcaps. Forcing consumers to conform to the desires of producers, the critics point out, is the opposite of what advocates of capitalism claim about a free- market economy-namely, that producers conform to the tastes and preferences of consumers. Within the first criticism there are two forms. The more serious claims that advertising, by its very nature, is inherently deceptive, because it manipulates consumers into buying products they do not need or want. The most specific example of this criticism is the charge of subliminal advertising. Thus, when looking at a place mat in front of you at a Howard Johnson’s restaurant, with its picture of the fried clam special, you might be deceived and manipulated into changing your taste. The other form claims that advertising is “merely” coercive, by creating needs and wants that otherwise would not exist without it. That is, highly emotional, persuasive, combative advertising - as opposed to rational, informative, and constructive advertising - is claimed to be a kind of physical force that destroys consumer sovereignty over the free market. This is Galbraith’s “dependence effect,” so called because our wants, he claims, are dependent on or created by the process by which they are satisfied- the process of production, especially advertising and salesmanship. Our wants for breakfast cereal and laundry detergent, says Galbraith, are contrived and artificial. The psychology of behaviorism has strongly influenced this second form of the first “social” criticism.

Both forms of the “coercive power” charge refer repeatedly to the advertising of cigarettes, liquor, drugs, sports cars, deodorant, Gucci shoes, and color television sets as evidence of advertising’s alleged power to force unneeded and unwanted products on the poor, helpless consumer. The charge of manipulation and deception is more serious than “mere” coercion because manipulation is more devious; a manipulator can make consumers buy products they think are good for them when, in fact, that is not the case. The charge of manipulation, in effect, views advertising as a pack of lies. The charge of “mere” coercion, on the other hand, claims that advertising is just brute force; advertising in this view, in effect, is excessively pushy. According to the second “social” criticism, advertising offends the consumer’s sense of good taste by insulting and degrading his intelligence, by promoting morally offensive products, and by encouraging harmful and immoral behavior. Prime targets of this “offensiveness” criticism are Mr. Whipple and his Charmin bathroom tissue commercials, as well as the “ring around the collar” commercials of Wisk liquid detergent and the Noxzema “take it all off’ shaving cream ads. But worse, the critics allege, advertising promotes products that have no redeeming moral value, such as cigarettes, beer, and pornographic literature. Advertising encourages harmful and immoral behavior and therefore is itself immoral. Although this criticism does not begin by attributing coercive power to advertising, it usually ends by supporting one or both forms of the first “social” criticism, thus calling for the regulation or banishment of a certain type of offensive-meaning coercive-advertising.

Q. Which of the following statements justify the claim that advertising is a coercive power?

| 1 Crore+ students have signed up on EduRev. Have you? Download the App |

The critics who denigrate advertising attack not only advertising but also by logical necessity capitalism, ethical egoism, and reason. As an institution in the division of labor and an instrument of capitalistic production, advertising communicates to many people at one time, the availability and nature of need- and want-satisfying products. In essence, advertising is salesmanship via the mass media; as such, it is the capitalist’s largest sales force and most effective means of delivering information to the market. In addition, advertising by its essential nature blatantly and unapologetically appeals to the self-interest of consumers for the blatant and selfish gain of capitalists. To criticize advertising is to criticize capitalism and ethical egoism. At the most fundamental level, the attacks on advertising are an assault on reason on man’s ability to form concepts and to think in principles because advertising is a conceptual communication to many people at one time about the conceptual achievements of others. It is attacked for precisely this aspect of its nature. The goal of advertising is to sell products to consumers, and the means by which this goal is achieved is to communicate what advertisers call the “product concept.” An advertisement is itself an abstraction, a concept of what the capitalist has produced. Thus, advertising is a conceptual communication in a market economy to self-interested buyers about the self-interested, conceptual achievements of capitalists. To criticize advertising at the most fundamental level - is to assault man’s consciousness.

From its earliest days, critics attacked capitalism for its dependence on the profit motive and the pursuit of self-interest. As the most visible manifestation, or “point man” of capitalism, advertising can be called the capitalist’s “tool of selfishness.” In a world culture based on altruism and self-sacrifice, it is amazing that advertising has lasted as long as it has. Indeed, its growth was stunted in Great Britain and Ireland for 141 years by a tax on newspapers and newspaper advertising. If selfishness is the original sin of man, according to Judeo-Christian ethics, then surely advertising is the original sin of capitalism. More accurately, advertising is the serpent that encourages man to pursue selfish gain and, in subtler form, to disobey authority. In contemporary economics, pure and perfect competition is the Garden of Eden in which the lion lies down beside the lamb and this “dirty, filthy” advertising is entirely absent-because consumers allegedly have perfect information. Small wonder that advertising does not have a good press. At the level of fundamental ideas, three attacks on advertising constitute the assault on consciousness. One attack attributes to advertising the coercive power to force consumers to buy products they do not need or want. At the level of metaphysics, this attack denies the volitional nature of reason, that is, free will; consequently, it denies, either explicitly or implicitly, the validity of human consciousness as such. A second attack derides advertising for how offensive it allegedly is; ultimately, critics advocate regulation to control the allegedly offensive advertising. At root - that is, at the level of ethics this attack denies that values are objective, that values are a product of the relation between material objects and a volitional consciousness that evaluates them. Consequently, it denies the existence of rational options.

A third attack, which derives from contemporary economics, views advertising as a tool of monopoly power. At the level of epistemology, however, this attack denies the possibility of truth and certainty, because reason allegedly is impotent to know reality; all man can do is emulate the methods of physics, by conducting statistically controlled experiments, and attempt to establish an uncertain, probabilistic knowledge. These three assaults on consciousness form the philosophic foundations of what are commonly known as the “social” and “economic” criticisms of advertising, the first two forming the foundation of the “social” criticisms, the third the foundation of the economic criticisms. The quantity of literature that attacks advertising approaches the infinite. The list of complaints is long, and each one has many variations. Explicitly or implicitly, all attacks attribute to advertising the power to initiate physical force against both consumers and competitors. The “social” criticisms assert that advertising adds no value to the products it promotes; therefore, it is superfluous, inherently dishonest, immoral, and fraudulent. The economic criticisms assert that advertising increases prices and wastes society’s valuable resources; therefore, advertising contributes to the establishment of monopoly power.

In essence, there are two “social” criticisms. The first explicitly charges advertising with the power to force consumers to buy products they do not need or want; the second implicitly charges advertising with this power. According to the first, advertising changes the tastes and preferences of consumers by coercing them to conform to the desires of producers. For example, consumers may want safer auto-mobiles, but what they get, according to the critics, are racing stripes and aluminum hubcaps. Forcing consumers to conform to the desires of producers, the critics point out, is the opposite of what advocates of capitalism claim about a free- market economy-namely, that producers conform to the tastes and preferences of consumers. Within the first criticism there are two forms. The more serious claims that advertising, by its very nature, is inherently deceptive, because it manipulates consumers into buying products they do not need or want. The most specific example of this criticism is the charge of subliminal advertising. Thus, when looking at a place mat in front of you at a Howard Johnson’s restaurant, with its picture of the fried clam special, you might be deceived and manipulated into changing your taste. The other form claims that advertising is “merely” coercive, by creating needs and wants that otherwise would not exist without it. That is, highly emotional, persuasive, combative advertising - as opposed to rational, informative, and constructive advertising - is claimed to be a kind of physical force that destroys consumer sovereignty over the free market. This is Galbraith’s “dependence effect,” so called because our wants, he claims, are dependent on or created by the process by which they are satisfied- the process of production, especially advertising and salesmanship. Our wants for breakfast cereal and laundry detergent, says Galbraith, are contrived and artificial. The psychology of behaviorism has strongly influenced this second form of the first “social” criticism.

Both forms of the “coercive power” charge refer repeatedly to the advertising of cigarettes, liquor, drugs, sports cars, deodorant, Gucci shoes, and color television sets as evidence of advertising’s alleged power to force unneeded and unwanted products on the poor, helpless consumer. The charge of manipulation and deception is more serious than “mere” coercion because manipulation is more devious; a manipulator can make consumers buy products they think are good for them when, in fact, that is not the case. The charge of manipulation, in effect, views advertising as a pack of lies. The charge of “mere” coercion, on the other hand, claims that advertising is just brute force; advertising in this view, in effect, is excessively pushy. According to the second “social” criticism, advertising offends the consumer’s sense of good taste by insulting and degrading his intelligence, by promoting morally offensive products, and by encouraging harmful and immoral behavior. Prime targets of this “offensiveness” criticism are Mr. Whipple and his Charmin bathroom tissue commercials, as well as the “ring around the collar” commercials of Wisk liquid detergent and the Noxzema “take it all off’ shaving cream ads. But worse, the critics allege, advertising promotes products that have no redeeming moral value, such as cigarettes, beer, and pornographic literature. Advertising encourages harmful and immoral behavior and therefore is itself immoral. Although this criticism does not begin by attributing coercive power to advertising, it usually ends by supporting one or both forms of the first “social” criticism, thus calling for the regulation or banishment of a certain type of offensive-meaning coercive-advertising.

Q. Which of the following statements does not agree with the idea of social criticism?

The critics who denigrate advertising attack not only advertising but also by logical necessity capitalism, ethical egoism, and reason. As an institution in the division of labor and an instrument of capitalistic production, advertising communicates to many people at one time, the availability and nature of need- and want-satisfying products. In essence, advertising is salesmanship via the mass media; as such, it is the capitalist’s largest sales force and most effective means of delivering information to the market. In addition, advertising by its essential nature blatantly and unapologetically appeals to the self-interest of consumers for the blatant and selfish gain of capitalists. To criticize advertising is to criticize capitalism and ethical egoism. At the most fundamental level, the attacks on advertising are an assault on reason on man’s ability to form concepts and to think in principles because advertising is a conceptual communication to many people at one time about the conceptual achievements of others. It is attacked for precisely this aspect of its nature. The goal of advertising is to sell products to consumers, and the means by which this goal is achieved is to communicate what advertisers call the “product concept.” An advertisement is itself an abstraction, a concept of what the capitalist has produced. Thus, advertising is a conceptual communication in a market economy to self-interested buyers about the self-interested, conceptual achievements of capitalists. To criticize advertising at the most fundamental level - is to assault man’s consciousness.

From its earliest days, critics attacked capitalism for its dependence on the profit motive and the pursuit of self-interest. As the most visible manifestation, or “point man” of capitalism, advertising can be called the capitalist’s “tool of selfishness.” In a world culture based on altruism and self-sacrifice, it is amazing that advertising has lasted as long as it has. Indeed, its growth was stunted in Great Britain and Ireland for 141 years by a tax on newspapers and newspaper advertising. If selfishness is the original sin of man, according to Judeo-Christian ethics, then surely advertising is the original sin of capitalism. More accurately, advertising is the serpent that encourages man to pursue selfish gain and, in subtler form, to disobey authority. In contemporary economics, pure and perfect competition is the Garden of Eden in which the lion lies down beside the lamb and this “dirty, filthy” advertising is entirely absent-because consumers allegedly have perfect information. Small wonder that advertising does not have a good press. At the level of fundamental ideas, three attacks on advertising constitute the assault on consciousness. One attack attributes to advertising the coercive power to force consumers to buy products they do not need or want. At the level of metaphysics, this attack denies the volitional nature of reason, that is, free will; consequently, it denies, either explicitly or implicitly, the validity of human consciousness as such. A second attack derides advertising for how offensive it allegedly is; ultimately, critics advocate regulation to control the allegedly offensive advertising. At root - that is, at the level of ethics this attack denies that values are objective, that values are a product of the relation between material objects and a volitional consciousness that evaluates them. Consequently, it denies the existence of rational options.

A third attack, which derives from contemporary economics, views advertising as a tool of monopoly power. At the level of epistemology, however, this attack denies the possibility of truth and certainty, because reason allegedly is impotent to know reality; all man can do is emulate the methods of physics, by conducting statistically controlled experiments, and attempt to establish an uncertain, probabilistic knowledge. These three assaults on consciousness form the philosophic foundations of what are commonly known as the “social” and “economic” criticisms of advertising, the first two forming the foundation of the “social” criticisms, the third the foundation of the economic criticisms. The quantity of literature that attacks advertising approaches the infinite. The list of complaints is long, and each one has many variations. Explicitly or implicitly, all attacks attribute to advertising the power to initiate physical force against both consumers and competitors. The “social” criticisms assert that advertising adds no value to the products it promotes; therefore, it is superfluous, inherently dishonest, immoral, and fraudulent. The economic criticisms assert that advertising increases prices and wastes society’s valuable resources; therefore, advertising contributes to the establishment of monopoly power.

In essence, there are two “social” criticisms. The first explicitly charges advertising with the power to force consumers to buy products they do not need or want; the second implicitly charges advertising with this power. According to the first, advertising changes the tastes and preferences of consumers by coercing them to conform to the desires of producers. For example, consumers may want safer auto-mobiles, but what they get, according to the critics, are racing stripes and aluminum hubcaps. Forcing consumers to conform to the desires of producers, the critics point out, is the opposite of what advocates of capitalism claim about a free- market economy-namely, that producers conform to the tastes and preferences of consumers. Within the first criticism there are two forms. The more serious claims that advertising, by its very nature, is inherently deceptive, because it manipulates consumers into buying products they do not need or want. The most specific example of this criticism is the charge of subliminal advertising. Thus, when looking at a place mat in front of you at a Howard Johnson’s restaurant, with its picture of the fried clam special, you might be deceived and manipulated into changing your taste. The other form claims that advertising is “merely” coercive, by creating needs and wants that otherwise would not exist without it. That is, highly emotional, persuasive, combative advertising - as opposed to rational, informative, and constructive advertising - is claimed to be a kind of physical force that destroys consumer sovereignty over the free market. This is Galbraith’s “dependence effect,” so called because our wants, he claims, are dependent on or created by the process by which they are satisfied- the process of production, especially advertising and salesmanship. Our wants for breakfast cereal and laundry detergent, says Galbraith, are contrived and artificial. The psychology of behaviorism has strongly influenced this second form of the first “social” criticism.

Both forms of the “coercive power” charge refer repeatedly to the advertising of cigarettes, liquor, drugs, sports cars, deodorant, Gucci shoes, and color television sets as evidence of advertising’s alleged power to force unneeded and unwanted products on the poor, helpless consumer. The charge of manipulation and deception is more serious than “mere” coercion because manipulation is more devious; a manipulator can make consumers buy products they think are good for them when, in fact, that is not the case. The charge of manipulation, in effect, views advertising as a pack of lies. The charge of “mere” coercion, on the other hand, claims that advertising is just brute force; advertising in this view, in effect, is excessively pushy. According to the second “social” criticism, advertising offends the consumer’s sense of good taste by insulting and degrading his intelligence, by promoting morally offensive products, and by encouraging harmful and immoral behavior. Prime targets of this “offensiveness” criticism are Mr. Whipple and his Charmin bathroom tissue commercials, as well as the “ring around the collar” commercials of Wisk liquid detergent and the Noxzema “take it all off’ shaving cream ads. But worse, the critics allege, advertising promotes products that have no redeeming moral value, such as cigarettes, beer, and pornographic literature. Advertising encourages harmful and immoral behavior and therefore is itself immoral. Although this criticism does not begin by attributing coercive power to advertising, it usually ends by supporting one or both forms of the first “social” criticism, thus calling for the regulation or banishment of a certain type of offensive-meaning coercive-advertising.

Q. Find the correct statement.

Group Question

Read the passage carefully and answer the questions that follow.

Investors, even professionals, fall prey to important logical fallacies and psychological failings. These psychological pressures impact our decisions under conditions of uncertainty in a very predictable manner, not only in the marketplace, but in virtually every aspect of our lives. The bottom line is that these powerful forces lead most people to make the same mistakes time and again. Understanding them is your best protection against stampeding with the crowd, and may help you to profit from their mistakes instead. But as you read on you’ll see it’s much easier said than done.

Despite what many economists and financial theorists assume, people are not good intuitive statisticians, particularly under difficult conditions. They do not calculate odds properly when making investment decisions, which causes consistent errors. Let us first look at one of the most common of the cognitive biases that Daniel Kahneman of Princeton and the late Amos Tversky of Stanford call ‘representativeness’. The two professors show it’s a natural human tendency to draw analogies and see identical situations where in fact there are important differences. In the market, this means labelling two companies, or two market environments, as the same when the actual resemblance is superficial. Give people a little information and, click!, they pull out a picture they’re familiar with, though it may only remotely represent the current situation. An example: the aftermath of the 1987 stock market crash. In five trading days the Dow fell 742 points, culminating with the 508 point decline on Black Monday, October 19. This wiped out almost $1 trillion of value. ‘Is this 1929?’ asked the media in bold headlines. Many investors taking this heuristical shortcut cowered in cash. They were caught up in the false parallel between 1987 and 1929. Why? At the time, the situations seemed eerily similar. We had not had a stock market crash for 58 years. Generations grew up believing that because a Depression followed the 1929 Crash it would always happen this way. A large part of Wall Street’s experts, the media, and the investing public agreed.

Overlooked was that the two crashes had only the remotest similarity. In the first place, 1929 was a special case. The nation has had numerous panics and crashes in the nineteenth and early twentieth centuries without a depression. Crashes or no, the thriving American economy always bounded back in short order. More important, it was apparent even then that the economic and investment climate was entirely different. Although market savants and publications were presenting charts showing the breathtaking similarity between the market postcrash in 1988 with that of 1929, there was far less to it than met the eye. It was hard for even the most fervent gloom-and-doomer to argue that a parallel situation existed after the 1987 crash. The economy was rolling along at a rate above most estimates pre-crash and sharply above the recession levels projected in the weeks following the October 19 debacle.

The representativeness heuristic covers a number of common decision-making errors. Kahneman and Tversky defined this heuristic as a subjective judgment of the extent to which the event in question ‘is similar in essential properties to its parent population’ or ‘reflects the salient features of the process by which it is generated’. Because the definition of representativeness is abstract and a little hard to understand, let’s look at some more concrete examples of how this heuristic works, and how it can lead to major mistakes in many situations. First, it may give too much emphasis to the similarities between events (or samples), but not to the probability that they will occur. Again looking at the 1987 crash, it appeared similar to 1929 in its stunning decline, but this by itself did not mean that a Great Depression would follow. In fact, as we have seen, there have been many crashes, but only one Great Depression.

Second, representativeness may reduce the importance of variables that are critical in determining the event’s probability. Again using the crash as an illustration, the major differences between the situations in 1987 and 1929 were downplayed, with the focus solely on the market’s plunge. This type of representativeness bias occurs time and again in the marketplace. As I’m sure you have guessed, the representativeness heuristic can apply just as forcefully to a company or an industry as to the market as a whole. Here is one such an example: In 1993 Dell Computer collapsed on Wall Street, losing 50% of its value in months. One day it had a market capitalization of $4.6 billion; six months later, it was just over $2.2 billion. What caused the drop? Earnings were weak, as the company took some major charges while repositioning its personal computer lines and restructuring its marketing.

What probably happened was this: two other industry leaders, IBM and Digital Equipment Corporation (DEC), were weak, and investors lumped the three companies together. IBM was in temporary trouble, while DEC’S was more serious. Dell was not. It was a very different kind of company with different products. Its repositioning was fabulously successful and it went on to become a major player in the personal computer industry.

Kahneman and Tversky’s findings, which have been repeatedly confirmed, are particularly important to our understanding of stock market errors.

Q. Which statements do not reflect the true essence of the passage?

I. Daniel Kahneman and Amos Tversky have identified a cognitive bias they call ‘representativeness’ which is particularly useful in understanding the mistakes people make in the stock market.

II. People are led astray by similarities between two things, and fail to spot the differences, especially in the context of the stock market.

III. People wrongly assumed that the stock market crash of 1987 was similar to that of 1929, and therefore expected it to be followed by an economic depression.

IV. Stock market crashes are not necessarily as bad as the one in 1929, but people are bad at calculating probabilities, so they assume the worst.

Investors, even professionals, fall prey to important logical fallacies and psychological failings. These psychological pressures impact our decisions under conditions of uncertainty in a very predictable manner, not only in the marketplace but in virtually every aspect of our lives. The bottom line is that these powerful forces lead most people to make the same mistakes time and again. Understanding them is your best protection against stampeding with the crowd, and may help you to profit from their mistakes instead. But as you read on you’ll see it’s much easier said than done.

Despite what many economists and financial theorists assume, people are not good intuitive statisticians, particularly under difficult conditions. They do not calculate odds properly when making investment decisions, which causes consistent errors. Let us first look at one of the most common of the cognitive biases that Daniel Kahneman of Princeton and the late Amos Tversky of Stanford call ‘representativeness’. The two professors show it’s a natural human tendency to draw analogies and see identical situations where in fact there are important differences. In the market, this means labeling two companies, or two market environments, as the same when the actual resemblance is superficial. Give people a little information and, click! they pull out a picture they’re familiar with, though it may only remotely represent the current situation. An example: the aftermath of the 1987 stock market crash. In five trading days, the Dow fell 742 points, culminating with the 508 point decline on Black Monday, October 19. This wiped out almost $1 trillion of value. ‘Is this 1929?’ asked the media in bold headlines. Many investors taking this heuristical shortcut cowered in cash. They were caught up in the false parallel between 1987 and 1929. Why? At the time, the situations seemed eerily similar. We had not had a stock market crash for 58 years. Generations grew up believing that because a Depression followed the 1929 Crash it would always happen this way. A large part of Wall Street’s experts, the media, and the investing public agreed.

Overlooked was that the two crashes had only the remotest similarity. In the first place, 1929 was a special case. The nation has had numerous panics and crashes in the nineteenth and early twentieth centuries without a depression. Crashes or no, the thriving American economy always bounded back in short order. More important, it was apparent even then that the economic and investment climate was entirely different. Although market savants and publications were presenting charts showing the breathtaking similarity between the market postcrash in 1988 with that of 1929, there was far less to it than met the eye. It was hard for even the most fervent gloom-and-doomer to argue that a parallel situation existed after the 1987 crash. The economy was rolling along at a rate above most estimates pre-crash and sharply above the recession levels projected in the weeks following the October 19 debacle.

The representativeness heuristic covers a number of common decision-making errors. Kahneman and Tversky defined this heuristic as a subjective judgment of the extent to which the event in question ‘is similar in essential properties to its parent population’ or ‘reflects the salient features of the process by which it is generated’. Because the definition of representativeness is abstract and a little hard to understand, let’s look at some more concrete examples of how this heuristic works, and how it can lead to major mistakes in many situations. First, it may give too much emphasis on the similarities between events (or samples), but not to the probability that they will occur. Again looking at the 1987 crash, it appeared similar to 1929 in its stunning decline, but this by itself did not mean that a Great Depression would follow. In fact, as we have seen, there have been many crashes, but only one Great Depression.

Second, representativeness may reduce the importance of variables that are critical in determining the event’s probability. Again using the crash, as an illustration, the major differences between the situations in 1987 and 1929 were downplayed, with the focus solely on the market’s plunge. This type of representativeness bias occurs time and again in the marketplace. As I’m sure you have guessed, the representativeness heuristic can apply just as forcefully to a company or an industry as to the market as a whole. Here is one such an example: In 1993 Dell Computer collapsed on Wall Street, losing 50% of its value in months. One day it had a market capitalization of $4.6 billion; six months later, it was just over $2.2 billion. What caused the drop? Earnings were weak, as the company took some major charges while repositioning its personal computer lines and restructuring its marketing.

What probably happened was this: two other industry leaders, IBM and Digital Equipment Corporation (DEC), were weak, and investors lumped the three companies together. IBM was in temporary trouble, while DEC’S was more serious. Dell was not. It was a very different kind of company with different products. Its repositioning was fabulously successful and it went on to become a major player in the personal computer industry.

Kahneman and Tversky’s findings, which have been repeatedly confirmed, are particularly important to our understanding of stock market errors.

Q. Which of the following does not define the cognitive bias that Daniel Kahneman and Amos Tversky call ‘representativeness’?

I. People are not good intuitive statisticians and do not calculate the odds correctly when making investment decisions.

II. People tend to see similarities between two situations and ignore the differences, even when the differences are important ones.

III. People often make incorrect assumptions about stock market crashes based on the events following the 1929 Crash.

IV. People often judge the probability of an event by the extent to which the event in question is similar in essential properties to its parent population.

Investors, even professionals, fall prey to important logical fallacies and psychological failings. These psychological pressures impact our decisions under conditions of uncertainty in a very predictable manner, not only in the marketplace, but in virtually every aspect of our lives. The bottom line is that these powerful forces lead most people to make the same mistakes time and again. Understanding them is your best protection against stampeding with the crowd, and may help you to profit from their mistakes instead. But as you read on you’ll see it’s much easier said than done.

Despite what many economists and financial theorists assume, people are not good intuitive statisticians, particularly under difficult conditions. They do not calculate odds properly when making investment decisions, which causes consistent errors. Let us first look at one of the most common of the cognitive biases that Daniel Kahneman of Princeton and the late Amos Tversky of Stanford call ‘representativeness’. The two professors show it’s a natural human tendency to draw analogies and see identical situations where in fact there are important differences. In the market, this means labelling two companies, or two market environments, as the same when the actual resemblance is superficial. Give people a little information and, click!, they pull out a picture they’re familiar with, though it may only remotely represent the current situation. An example: the aftermath of the 1987 stock market crash. In five trading days the Dow fell 742 points, culminating with the 508 point decline on Black Monday, October 19. This wiped out almost $1 trillion of value. ‘Is this 1929?’ asked the media in bold headlines. Many investors taking this heuristical shortcut cowered in cash. They were caught up in the false parallel between 1987 and 1929. Why? At the time, the situations seemed eerily similar. We had not had a stock market crash for 58 years. Generations grew up believing that because a Depression followed the 1929 Crash it would always happen this way. A large part of Wall Street’s experts, the media, and the investing public agreed.

Overlooked was that the two crashes had only the remotest similarity. In the first place, 1929 was a special case. The nation has had numerous panics and crashes in the nineteenth and early twentieth centuries without a depression. Crashes or no, the thriving American economy always bounded back in short order. More important, it was apparent even then that the economic and investment climate was entirely different. Although market savants and publications were presenting charts showing the breathtaking similarity between the market postcrash in 1988 with that of 1929, there was far less to it than met the eye. It was hard for even the most fervent gloom-and-doomer to argue that a parallel situation existed after the 1987 crash. The economy was rolling along at a rate above most estimates pre-crash and sharply above the recession levels projected in the weeks following the October 19 debacle.

The representativeness heuristic covers a number of common decision-making errors. Kahneman and Tversky defined this heuristic as a subjective judgment of the extent to which the event in question ‘is similar in essential properties to its parent population’ or ‘reflects the salient features of the process by which it is generated’. Because the definition of representativeness is abstract and a little hard to understand, let’s look at some more concrete examples of how this heuristic works, and how it can lead to major mistakes in many situations. First, it may give too much emphasis to the similarities between events (or samples), but not to the probability that they will occur. Again looking at the 1987 crash, it appeared similar to 1929 in its stunning decline, but this by itself did not mean that a Great Depression would follow. In fact, as we have seen, there have been many crashes, but only one Great Depression.

Second, representativeness may reduce the importance of variables that are critical in determining the event’s probability. Again using the crash as an illustration, the major differences between the situations in 1987 and 1929 were downplayed, with the focus solely on the market’s plunge. This type of representativeness bias occurs time and again in the marketplace. As I’m sure you have guessed, the representativeness heuristic can apply just as forcefully to a company or an industry as to the market as a whole. Here is one such an example: In 1993 Dell Computer collapsed on Wall Street, losing 50% of its value in months. One day it had a market capitalization of $4.6 billion; six months later, it was just over $2.2 billion. What caused the drop? Earnings were weak, as the company took some major charges while repositioning its personal computer lines and restructuring its marketing.

What probably happened was this: two other industry leaders, IBM and Digital Equipment Corporation (DEC), were weak, and investors lumped the three companies together. IBM was in temporary trouble, while DEC’S was more serious. Dell was not. It was a very different kind of company with different products. Its repositioning was fabulously successful and it went on to become a major player in the personal computer industry.

Kahneman and Tversky’s findings, which have been repeatedly confirmed, are particularly important to our understanding of stock market errors.

Q. What does the example of Dell Computer illustrate?

I. That the representativeness heuristic can apply to individual companies as well as the whole market.

II. That Dell, unlike IBM and DEC, was not an industry leader at the time (1993), though it went on to become very successful by late 1997.

III. That the company lost half its value because it was making some major charges while repositioning its personal computer lines and restructuring its marketing.

IV. That Dell lost its market value because people wrongly lumped it with the other two industry leaders, IBM and DEC, which were in trouble, though Dell was not.

Investors, even professionals, fall prey to important logical fallacies and psychological failings. These psychological pressures impact our decisions under conditions of uncertainty in a very predictable manner, not only in the marketplace, but in virtually every aspect of our lives. The bottom line is that these powerful forces lead most people to make the same mistakes time and again. Understanding them is your best protection against stampeding with the crowd, and may help you to profit from their mistakes instead. But as you read on you’ll see it’s much easier said than done.

Despite what many economists and financial theorists assume, people are not good intuitive statisticians, particularly under difficult conditions. They do not calculate odds properly when making investment decisions, which causes consistent errors. Let us first look at one of the most common of the cognitive biases that Daniel Kahneman of Princeton and the late Amos Tversky of Stanford call ‘representativeness’. The two professors show it’s a natural human tendency to draw analogies and see identical situations where in fact there are important differences. In the market, this means labelling two companies, or two market environments, as the same when the actual resemblance is superficial. Give people a little information and, click!, they pull out a picture they’re familiar with, though it may only remotely represent the current situation. An example: the aftermath of the 1987 stock market crash. In five trading days the Dow fell 742 points, culminating with the 508 point decline on Black Monday, October 19. This wiped out almost $1 trillion of value. ‘Is this 1929?’ asked the media in bold headlines. Many investors taking this heuristical shortcut cowered in cash. They were caught up in the false parallel between 1987 and 1929. Why? At the time, the situations seemed eerily similar. We had not had a stock market crash for 58 years. Generations grew up believing that because a Depression followed the 1929 Crash it would always happen this way. A large part of Wall Street’s experts, the media, and the investing public agreed.

Overlooked was that the two crashes had only the remotest similarity. In the first place, 1929 was a special case. The nation has had numerous panics and crashes in the nineteenth and early twentieth centuries without a depression. Crashes or no, the thriving American economy always bounded back in short order. More important, it was apparent even then that the economic and investment climate was entirely different. Although market savants and publications were presenting charts showing the breathtaking similarity between the market postcrash in 1988 with that of 1929, there was far less to it than met the eye. It was hard for even the most fervent gloom-and-doomer to argue that a parallel situation existed after the 1987 crash. The economy was rolling along at a rate above most estimates pre-crash and sharply above the recession levels projected in the weeks following the October 19 debacle.

The representativeness heuristic covers a number of common decision-making errors. Kahneman and Tversky defined this heuristic as a subjective judgment of the extent to which the event in question ‘is similar in essential properties to its parent population’ or ‘reflects the salient features of the process by which it is generated’. Because the definition of representativeness is abstract and a little hard to understand, let’s look at some more concrete examples of how this heuristic works, and how it can lead to major mistakes in many situations. First, it may give too much emphasis to the similarities between events (or samples), but not to the probability that they will occur. Again looking at the 1987 crash, it appeared similar to 1929 in its stunning decline, but this by itself did not mean that a Great Depression would follow. In fact, as we have seen, there have been many crashes, but only one Great Depression.

Second, representativeness may reduce the importance of variables that are critical in determining the event’s probability. Again using the crash as an illustration, the major differences between the situations in 1987 and 1929 were downplayed, with the focus solely on the market’s plunge. This type of representativeness bias occurs time and again in the marketplace. As I’m sure you have guessed, the representativeness heuristic can apply just as forcefully to a company or an industry as to the market as a whole. Here is one such an example: In 1993 Dell Computer collapsed on Wall Street, losing 50% of its value in months. One day it had a market capitalization of $4.6 billion; six months later, it was just over $2.2 billion. What caused the drop? Earnings were weak, as the company took some major charges while repositioning its personal computer lines and restructuring its marketing.

What probably happened was this: two other industry leaders, IBM and Digital Equipment Corporation (DEC), were weak, and investors lumped the three companies together. IBM was in temporary trouble, while DEC’S was more serious. Dell was not. It was a very different kind of company with different products. Its repositioning was fabulously successful and it went on to become a major player in the personal computer industry.

Kahneman and Tversky’s findings, which have been repeatedly confirmed, are particularly important to our understanding of stock market errors.

Q. “Kahneman and Tversky’s findings ... are particularly important to our understanding of stock market errors.” Why is this?

I. We are particularly vulnerable to cognitive biases under conditions of uncertainty like those prevailing in the stock market.

II. The cognitive biases that Kahneman and Tversky mention are found only when calculating odds in making investments.

III. People are good intuitive statisticians, especially when they make investment decisions based on their instincts rather than intellect.

IV. None of the above.

Group Question

The passage given below is followed by a set of questions. Choose the most appropriate answer to each question.

It’s rare to come across a realistic and readable book about personal finance. Most are laden with rosy promises, followed by acronyms and turgid advice. Helaine Olen, a freelance journalist, offers an exception with “Pound Foolish: Exposing the Dark Side of the Personal F in ance Industry” . It’s a take-no-prisoners examination of the ways she says we have been scared, misled or bambooz led by those purporting to help us achieve financial security. Ms. Olen writes that the “financial therapy movement,” for all of its flaws, “has hit on one universal truth: When it comes to money, the vast majority of us are nuts. Bonkers.” She counts some of the ways: “We don’t open our 401 (k) statements. We ‘forget’ to pay our bills or file our taxes until the last minute.” Financial literacy is alarmingly low. Many of us don’t budget at all. With a flood of financial advice available on the Internet and on television, and through books and newspapers, what’s the disconnect? Aren’t we listening?

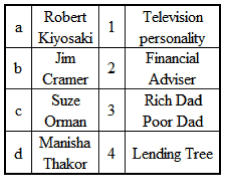

The problem, Ms. Olen writes, is that “most of the financial advice published and dished out by the truckload is useless” - that it is simply “oblivious to the messiness of the human condition.” What most advice fails to factor in - and what we often choose to overlook ourselves - are the costly realities of things like job loss, protracted unemployment, medical bankruptcy and high-interest debt. Even when we do save, plummeting interest rates, falling home prices and other economic events imperil our best efforts. A former personal finance columnist for The Los Angeles Times, Ms. Olen uses as examples people who are desperate for help with managing their money. These include a real estate investor whose combination of bad luck, unemployment and poor decision-making left her in foreclosure. There is also a commercial pilot whose pension was cut and who invested in real estate that ended up plummeting in value. Desperation, fear and insecurity can be a salesperson’s best friend. Ms. Olen learns how lucrative it is to sell financial services to the elderly, many of them terrified of outliving their savings. A 2009 AARP survey found that nearly one in 10 people over 55, or about 5.9 million Americans, had attended a free financial seminar in the last three years. At the World MoneyShow, an annual event in Orlando, 80 percent of attendees were over 55. The author writes that “a panicked baby boomer is their best customer.” And while Ms. Olen roundly attacks the myth that women are too emotional or ignorant to handle money well, she notes that they often lack confidence in their money management skills. Women also live longer than men and earn less. Saving more money, as women are exhorted to do, isn’t the issue, Ms. Olen says: “How they should do this with a lesser income that’s expected to do more goes unsaid.” Unusual, and refreshing, is her inclusion of so many women’s voices throughout the book, such as the writer Jane Bryant Quinn; the financial adviser Manisha Thakor, the labor economist Teresa Ghilarducci, and Elizabeth Warren, recently elected to the Senate from Massachusetts.

One woman who comes in for some scathing treatment is the best-selling financial adviser Suze Orman, whom Ms. Olen criticizes as offering “financial platitudes” and making huge amounts of money by telling others to be frugal. Ms. Olen writes that “Orman’s supposed wisdom often contradicts itself,” and that her affiliations with companies like FICO and Lending Tree raise questions about the impartiality of her advice. She criticizes many other financial gurus, saying they have provided unhelpful or confusing advice. These include Robert Kiyosaki, who in “Rich Dad, Poor Dad” referred to investments that “may have returns of 100 percent to infinity,” and the television personality Jim Cramer, whom the author describes as “a sweating and howling man” and who once declared that “Bear Steams is not in trouble!” shortly before it collapsed. Even good investing advice is often unhelpful, Ms. Olen says, because millions of Americans have saved so little money. For people who do have enough money to invest, the ability of financial services firms to charge high fees, unchallenged, is abetted by low rates of financial literacy. Many investors are unwilling to question glowing promises of double-digit returns or to read carefully the small print on a mutual fund statement. Our overly optimistic expectations of investment performance too often meet the reality of little professional oversight for all but the wealthiest.

While we know intellectually that we need to save and invest for our future, our ability to do so varies enormously, Ms. Olen points out. “Between 1979 and 2007, the average after-tax income for the top 1 percent of earners in the economy soared by 281 percent,” she writes. “The top 20 percent would see their incomes increase by 95 percent. The middle fifth? A mere 25 percent.” The solutions offered by the personal finance world have been unrealistic, she says, contending that “the increasing problem Americans were having keeping up financially was not viewed as a social justice problem, but as a knowledge and smarts problem that could be solved on an individual basis, one investor at a time.” She’s clear-eyed about the challenge of saving and investing when you simply have nothing to work with, and when decisions about spending are a daily quandary as prices rise and wages remain stagnant or fall. Ms. Olen describes playing Spent, an online role-playing game in which players are asked to make decisions while earning minimum wages, like those often found in retailing, the nation’s largest source of new jobs. The goal is to get to the next pay cycle without debt. “I’ve played Spent dozens of times,” she writes, “and I’ve never, ever made it to the end of the month.”

Q. Which statement reflects the true essence of the passage?

I. Most financial information does not connect well with the public because they do not take into account the financial difficulties that people are going through.

II. Most advice fails to factor in the costly realities of things like job loss, protracted unemployment, medical bankruptcy and high-interest debt.

III. Even good investing advice is often unhelpful, because millions of Americans have saved such little money.

IV. Most financial experts deliberately mislead people in order to make money.

It’s rare to come across a realistic and readable book about personal finance. Most are laden with rosy promises, followed by acronyms and turgid advice. Helaine Olen, a freelance journalist, offers an exception with “Pound Foolish: Exposing the Dark Side of the Personal F in ance Industry” . It’s a take-no-prisoners examination of the ways she says we have been scared, misled or bambooz led by those purporting to help us achieve financial security. Ms. Olen writes that the “financial therapy movement,” for all of its flaws, “has hit on one universal truth: When it comes to money, the vast majority of us are nuts. Bonkers.” She counts some of the ways: “We don’t open our 401 (k) statements. We ‘forget’ to pay our bills or file our taxes until the last minute.” Financial literacy is alarmingly low. Many of us don’t budget at all. With a flood of financial advice available on the Internet and on television, and through books and newspapers, what’s the disconnect? Aren’t we listening?

The problem, Ms. Olen writes, is that “most of the financial advice published and dished out by the truckload is useless” - that it is simply “oblivious to the messiness of the human condition.” What most advice fails to factor in - and what we often choose to overlook ourselves - are the costly realities of things like job loss, protracted unemployment, medical bankruptcy and high-interest debt. Even when we do save, plummeting interest rates, falling home prices and other economic events imperil our best efforts. A former personal finance columnist for The Los Angeles Times, Ms. Olen uses as examples people who are desperate for help with managing their money. These include a real estate investor whose combination of bad luck, unemployment and poor decision-making left her in foreclosure. There is also a commercial pilot whose pension was cut and who invested in real estate that ended up plummeting in value. Desperation, fear and insecurity can be a salesperson’s best friend. Ms. Olen learns how lucrative it is to sell financial services to the elderly, many of them terrified of outliving their savings. A 2009 AARP survey found that nearly one in 10 people over 55, or about 5.9 million Americans, had attended a free financial seminar in the last three years. At the World MoneyShow, an annual event in Orlando, 80 percent of attendees were over 55. The author writes that “a panicked baby boomer is their best customer.” And while Ms. Olen roundly attacks the myth that women are too emotional or ignorant to handle money well, she notes that they often lack confidence in their money management skills. Women also live longer than men and earn less. Saving more money, as women are exhorted to do, isn’t the issue, Ms. Olen says: “How they should do this with a lesser income that’s expected to do more goes unsaid.” Unusual, and refreshing, is her inclusion of so many women’s voices throughout the book, such as the writer Jane Bryant Quinn; the financial adviser Manisha Thakor, the labor economist Teresa Ghilarducci, and Elizabeth Warren, recently elected to the Senate from Massachusetts.

One woman who comes in for some scathing treatment is the best-selling financial adviser Suze Orman, whom Ms. Olen criticizes as offering “financial platitudes” and making huge amounts of money by telling others to be frugal. Ms. Olen writes that “Orman’s supposed wisdom often contradicts itself,” and that her affiliations with companies like FICO and Lending Tree raise questions about the impartiality of her advice. She criticizes many other financial gurus, saying they have provided unhelpful or confusing advice. These include Robert Kiyosaki, who in “Rich Dad, Poor Dad” referred to investments that “may have returns of 100 percent to infinity,” and the television personality Jim Cramer, whom the author describes as “a sweating and howling man” and who once declared that “Bear Steams is not in trouble!” shortly before it collapsed. Even good investing advice is often unhelpful, Ms. Olen says, because millions of Americans have saved so little money. For people who do have enough money to invest, the ability of financial services firms to charge high fees, unchallenged, is abetted by low rates of financial literacy. Many investors are unwilling to question glowing promises of double-digit returns or to read carefully the small print on a mutual fund statement. Our overly optimistic expectations of investment performance too often meet the reality of little professional oversight for all but the wealthiest.

While we know intellectually that we need to save and invest for our future, our ability to do so varies enormously, Ms. Olen points out. “Between 1979 and 2007, the average after-tax income for the top 1 percent of earners in the economy soared by 281 percent,” she writes. “The top 20 percent would see their incomes increase by 95 percent. The middle fifth? A mere 25 percent.” The solutions offered by the personal finance world have been unrealistic, she says, contending that “the increasing problem Americans were having keeping up financially was not viewed as a social justice problem, but as a knowledge and smarts problem that could be solved on an individual basis, one investor at a time.” She’s clear-eyed about the challenge of saving and investing when you simply have nothing to work with, and when decisions about spending are a daily quandary as prices rise and wages remain stagnant or fall. Ms. Olen describes playing Spent, an online role-playing game in which players are asked to make decisions while earning minimum wages, like those often found in retailing, the nation’s largest source of new jobs. The goal is to get to the next pay cycle without debt. “I’ve played Spent dozens of times,” she writes, “and I’ve never, ever made it to the end of the month.”

Q. According to the passage why is personal finance investing advice unhelpful?

I. There appears to be too much of accessible information which confuses people as to what strategy to follow.

II. Most people are not financially literate.

III. Many people have little to no savings. Therefore, they are in no position to invest.

IV. Personal finance does not take into account the financial difficulties that most people are going through.

It’s rare to come across a realistic and readable book about personal finance. Most are laden with rosy promises, followed by acronyms and turgid advice. Helaine Olen, a freelance journalist, offers an exception with “Pound Foolish: Exposing the Dark Side of the Personal F in ance Industry” . It’s a take-no-prisoners examination of the ways she says we have been scared, misled or bambooz led by those purporting to help us achieve financial security. Ms. Olen writes that the “financial therapy movement,” for all of its flaws, “has hit on one universal truth: When it comes to money, the vast majority of us are nuts. Bonkers.” She counts some of the ways: “We don’t open our 401 (k) statements. We ‘forget’ to pay our bills or file our taxes until the last minute.” Financial literacy is alarmingly low. Many of us don’t budget at all. With a flood of financial advice available on the Internet and on television, and through books and newspapers, what’s the disconnect? Aren’t we listening?

The problem, Ms. Olen writes, is that “most of the financial advice published and dished out by the truckload is useless” - that it is simply “oblivious to the messiness of the human condition.” What most advice fails to factor in - and what we often choose to overlook ourselves - are the costly realities of things like job loss, protracted unemployment, medical bankruptcy and high-interest debt. Even when we do save, plummeting interest rates, falling home prices and other economic events imperil our best efforts. A former personal finance columnist for The Los Angeles Times, Ms. Olen uses as examples people who are desperate for help with managing their money. These include a real estate investor whose combination of bad luck, unemployment and poor decision-making left her in foreclosure. There is also a commercial pilot whose pension was cut and who invested in real estate that ended up plummeting in value. Desperation, fear and insecurity can be a salesperson’s best friend. Ms. Olen learns how lucrative it is to sell financial services to the elderly, many of them terrified of outliving their savings. A 2009 AARP survey found that nearly one in 10 people over 55, or about 5.9 million Americans, had attended a free financial seminar in the last three years. At the World MoneyShow, an annual event in Orlando, 80 percent of attendees were over 55. The author writes that “a panicked baby boomer is their best customer.” And while Ms. Olen roundly attacks the myth that women are too emotional or ignorant to handle money well, she notes that they often lack confidence in their money management skills. Women also live longer than men and earn less. Saving more money, as women are exhorted to do, isn’t the issue, Ms. Olen says: “How they should do this with a lesser income that’s expected to do more goes unsaid.” Unusual, and refreshing, is her inclusion of so many women’s voices throughout the book, such as the writer Jane Bryant Quinn; the financial adviser Manisha Thakor, the labor economist Teresa Ghilarducci, and Elizabeth Warren, recently elected to the Senate from Massachusetts.

One woman who comes in for some scathing treatment is the best-selling financial adviser Suze Orman, whom Ms. Olen criticizes as offering “financial platitudes” and making huge amounts of money by telling others to be frugal. Ms. Olen writes that “Orman’s supposed wisdom often contradicts itself,” and that her affiliations with companies like FICO and Lending Tree raise questions about the impartiality of her advice. She criticizes many other financial gurus, saying they have provided unhelpful or confusing advice. These include Robert Kiyosaki, who in “Rich Dad, Poor Dad” referred to investments that “may have returns of 100 percent to infinity,” and the television personality Jim Cramer, whom the author describes as “a sweating and howling man” and who once declared that “Bear Steams is not in trouble!” shortly before it collapsed. Even good investing advice is often unhelpful, Ms. Olen says, because millions of Americans have saved so little money. For people who do have enough money to invest, the ability of financial services firms to charge high fees, unchallenged, is abetted by low rates of financial literacy. Many investors are unwilling to question glowing promises of double-digit returns or to read carefully the small print on a mutual fund statement. Our overly optimistic expectations of investment performance too often meet the reality of little professional oversight for all but the wealthiest.