All Exams >

Commerce >

Economics CUET Preparation >

All Questions

All questions of The Theory of the Firm under Perfect Competition for Commerce Exam

A firm can sell as much as it wants at the market price. The situation is related to?- a)Monopoly

- b)Monopolistic competition

- c)Perfect competition

- d)Oligopoly

Correct answer is option 'C'. Can you explain this answer?

A firm can sell as much as it wants at the market price. The situation is related to?

a)

Monopoly

b)

Monopolistic competition

c)

Perfect competition

d)

Oligopoly

|

Sushil Kumar answered |

Pure or perfect competition is a theoretical market structure in which the following criteria are met:

- All firms sell an identical product (the product is a "commodity" or "homogeneous").

- All firms are price takers (they cannot influence the market price of their product). Market share has no influence on prices.

When AR=Rs. 10 and AC=Rs. 8, the firm makes?- a)Gross profit

- b)Supernormal profit

- c)Normal profit

- d)Net profit

Correct answer is option 'B'. Can you explain this answer?

When AR=Rs. 10 and AC=Rs. 8, the firm makes?

a)

Gross profit

b)

Supernormal profit

c)

Normal profit

d)

Net profit

|

|

Ishan Choudhury answered |

Supernormal profit is defined as extra profit above that level of normal profit.

Here the firm earns profit of Rs. 2 over the cost occurred.

Here the firm earns profit of Rs. 2 over the cost occurred.

____________ is an ideal market?- a)Monopolistic competition

- b)Oligopoly

- c)Perfect competition

- d)Monopoly

Correct answer is option 'C'. Can you explain this answer?

____________ is an ideal market?

a)

Monopolistic competition

b)

Oligopoly

c)

Perfect competition

d)

Monopoly

|

|

Vikas Kapoor answered |

Pure or perfect competition is a theoretical market structure in which the following criteria are met: All firms sell an identical product (the product is a "commodity" or "homogeneous"). All firms are price takers (they cannot influence the market price of their product). Market share has no influence on prices.

This a MCQ (Multiple Choice Question) based practice test of Chapter 4 - Theory of Firm Under Perfect Competition of Economics of Class XII (12) for the quick revision/preparation of School Board examinationsQ Condition for producer equilibrium is:- a)TC=TSC

- b)MC=MR

- c)TR=TVC

- d)None of above

Correct answer is 'B'. Can you explain this answer?

This a MCQ (Multiple Choice Question) based practice test of Chapter 4 - Theory of Firm Under Perfect Competition of Economics of Class XII (12) for the quick revision/preparation of School Board examinations

Q Condition for producer equilibrium is:

a)

TC=TSC

b)

MC=MR

c)

TR=TVC

d)

None of above

|

Puja Nambiar answered |

Condition for Producer Equilibrium

The producer equilibrium is a situation where a firm is maximizing its profits by producing a level of output where marginal cost (MC) is equal to marginal revenue (MR). In other words, the producer equilibrium is reached when a firm is producing at the point where it is making the highest possible economic profit.

The condition for producer equilibrium is as follows:

MC = MR

Explanation

Marginal cost (MC) is the additional cost of producing one more unit of output. Marginal revenue (MR) is the additional revenue earned by selling one more unit of output. In perfect competition, a firm is a price taker, meaning it cannot influence the market price of the product it sells. Therefore, the price of the product remains constant for the firm.

In perfect competition, the firm's marginal revenue (MR) is equal to the price of the product. Therefore, the condition for producer equilibrium can be rephrased as:

MC = P

where P is the price of the product.

If a firm produces at a level where MC is less than MR, it means that the firm can increase its profits by producing more units of output. Similarly, if a firm produces at a level where MC is greater than MR, it means that the firm can increase its profits by producing fewer units of output. So, the producer equilibrium is reached only when MC is equal to MR, where the firm is producing the level of output that maximizes its profits.

Conclusion

The condition for producer equilibrium is MC = MR, where a firm is producing the level of output that maximizes its profits. In perfect competition, where a firm is a price taker, the condition can be rephrased as MC = P.

The producer equilibrium is a situation where a firm is maximizing its profits by producing a level of output where marginal cost (MC) is equal to marginal revenue (MR). In other words, the producer equilibrium is reached when a firm is producing at the point where it is making the highest possible economic profit.

The condition for producer equilibrium is as follows:

MC = MR

Explanation

Marginal cost (MC) is the additional cost of producing one more unit of output. Marginal revenue (MR) is the additional revenue earned by selling one more unit of output. In perfect competition, a firm is a price taker, meaning it cannot influence the market price of the product it sells. Therefore, the price of the product remains constant for the firm.

In perfect competition, the firm's marginal revenue (MR) is equal to the price of the product. Therefore, the condition for producer equilibrium can be rephrased as:

MC = P

where P is the price of the product.

If a firm produces at a level where MC is less than MR, it means that the firm can increase its profits by producing more units of output. Similarly, if a firm produces at a level where MC is greater than MR, it means that the firm can increase its profits by producing fewer units of output. So, the producer equilibrium is reached only when MC is equal to MR, where the firm is producing the level of output that maximizes its profits.

Conclusion

The condition for producer equilibrium is MC = MR, where a firm is producing the level of output that maximizes its profits. In perfect competition, where a firm is a price taker, the condition can be rephrased as MC = P.

Under which market condition firms make only Normal Profit in the long run?- a)Oligopoly

- b)Monopoly

- c)Monopolistic competition

- d)Duopoly

Correct answer is option 'C'. Can you explain this answer?

Under which market condition firms make only Normal Profit in the long run?

a)

Oligopoly

b)

Monopoly

c)

Monopolistic competition

d)

Duopoly

|

|

Nandini Iyer answered |

In the long-run, the demand curve of a firm in a monopolistic competitive

Other name by which average revenue curve known:- a)Indifference curve

- b)Profit curve

- c)Average cost curve

- d)Demand curve

Correct answer is option 'D'. Can you explain this answer?

Other name by which average revenue curve known:

a)

Indifference curve

b)

Profit curve

c)

Average cost curve

d)

Demand curve

|

|

Aryan Khanna answered |

Average revenue curve is often called the demand curve due to its representation of the product's demand in the market. Each point on the curve represents the price of the product in the market. Price determines the demand for a product, hence Average revenue curve is also demand curve.

Assuming it is a perfect competitive market.

Assuming it is a perfect competitive market.

In perfect competition, since the firm is a price taker, the ________ curve is straight line- a)Total cost

- b)Marginal cost

- c)Total revenue

- d)Marginal revenue

Correct answer is option 'D'. Can you explain this answer?

In perfect competition, since the firm is a price taker, the ________ curve is straight line

a)

Total cost

b)

Marginal cost

c)

Total revenue

d)

Marginal revenue

|

|

Aryan Khanna answered |

Marginal revenue is the extra revenue generated when a perfectly competitive firm sells one more unit of output. The marginal revenue received by a firm is the change in total revenue divided by the change in quantity.

Perfect competition is a market structure with a large number of small firms, each selling identical goods. Perfectly competitive firms have perfect knowledge and perfect mobility into and out of the market. These conditions mean perfectly competitive firms are price takers, they have no market control and receive the going market price for all output sold.

Since they are the price takers and have no control over price but just the production, so even if they increase their quantity of production, still the price will remain constant and so does the marginal revenue.

In the long run the market price of a commodity is equal to its minimum average cost of production under the___________?- a)Monopolist competition

- b)Perfect competition

- c)Oligopoly

- d)Monopoly

Correct answer is option 'B'. Can you explain this answer?

In the long run the market price of a commodity is equal to its minimum average cost of production under the___________?

a)

Monopolist competition

b)

Perfect competition

c)

Oligopoly

d)

Monopoly

|

|

Kiran Mehta answered |

Perfect competition is an industry structure in which there are many firms producing homogeneous products.

None of the firms are large enough to influence the industry. In the long-run, companies that are engaged in a perfectly competitive market earn zero economic profits.

The long-run equilibrium point for a perfectly competitive market occurs where the demand curve (price) intersects the marginal cost (MC) curve and the minimum point of the average cost (AC) curve.

Since they are the price takers and the price remains constant so does the AC of production.

When ___________, the firms are earning just normal profit:- a)AC=AR

- b)MC=AC

- c)AR=MR

- d)MC=MR

Correct answer is option 'A'. Can you explain this answer?

When ___________, the firms are earning just normal profit:

a)

AC=AR

b)

MC=AC

c)

AR=MR

d)

MC=MR

|

|

Vikas Kapoor answered |

AC = AR means the firm’s cost and revenue are equal which means the firm does not earn any profit or no loss, which means the firm is earning normal profit.

Which of the following is the condition for equilibrium of a firm?- a)MC curve must cut MR curve from above

- b)MR = MC

- c)None of above

- d)Both of these

Correct answer is option 'B'. Can you explain this answer?

Which of the following is the condition for equilibrium of a firm?

a)

MC curve must cut MR curve from above

b)

MR = MC

c)

None of above

d)

Both of these

|

Rahul Chaudhary answered |

Equilibrium of a Firm:

Equilibrium of a firm refers to a situation where the firm is earning maximum profits or where there is no incentive to change the level of output. In other words, the firm is producing the level of output where its marginal cost equals its marginal revenue.

Condition for Equilibrium:

The condition for equilibrium of a firm is that its marginal revenue (MR) should be equal to its marginal cost (MC). This condition can be explained as follows:

- Marginal Revenue (MR): Marginal revenue is the additional revenue earned by the firm by selling one additional unit of output. It is also the slope of the total revenue curve.

- Marginal Cost (MC): Marginal cost is the additional cost incurred by the firm by producing one additional unit of output. It is also the slope of the total cost curve.

When the firm produces one additional unit of output, it incurs an additional cost (MC) and earns an additional revenue (MR). If MR is greater than MC, the firm should produce more output as it will earn more revenue than the cost incurred. On the other hand, if MC is greater than MR, the firm should produce less output as it will incur more cost than the revenue earned. Therefore, the firm should produce the level of output where MR equals MC, as at this level of output, the firm is earning maximum profits.

Conclusion:

Hence, the condition for equilibrium of a firm is that MR should be equal to MC. If the firm produces any other level of output, it will not be in equilibrium, as it will either earn less profit or incur losses.

Equilibrium of a firm refers to a situation where the firm is earning maximum profits or where there is no incentive to change the level of output. In other words, the firm is producing the level of output where its marginal cost equals its marginal revenue.

Condition for Equilibrium:

The condition for equilibrium of a firm is that its marginal revenue (MR) should be equal to its marginal cost (MC). This condition can be explained as follows:

- Marginal Revenue (MR): Marginal revenue is the additional revenue earned by the firm by selling one additional unit of output. It is also the slope of the total revenue curve.

- Marginal Cost (MC): Marginal cost is the additional cost incurred by the firm by producing one additional unit of output. It is also the slope of the total cost curve.

When the firm produces one additional unit of output, it incurs an additional cost (MC) and earns an additional revenue (MR). If MR is greater than MC, the firm should produce more output as it will earn more revenue than the cost incurred. On the other hand, if MC is greater than MR, the firm should produce less output as it will incur more cost than the revenue earned. Therefore, the firm should produce the level of output where MR equals MC, as at this level of output, the firm is earning maximum profits.

Conclusion:

Hence, the condition for equilibrium of a firm is that MR should be equal to MC. If the firm produces any other level of output, it will not be in equilibrium, as it will either earn less profit or incur losses.

What are the conditions for the long run equilibrium of the competitive firm?- a)SMC=SAC=LMC

- b)P=MR

- c)LMC=LAC=P

- d)All of the above

Correct answer is option 'C'. Can you explain this answer?

What are the conditions for the long run equilibrium of the competitive firm?

a)

SMC=SAC=LMC

b)

P=MR

c)

LMC=LAC=P

d)

All of the above

|

Anjana Desai answered |

Conditions for Long Run Equilibrium of Competitive Firm

In a perfectly competitive market, there are certain conditions that must be met for a firm to achieve long-run equilibrium. These conditions are as follows:

LMC = LAC = P

In the long run, a firm in a perfectly competitive market will produce at the point where its long-run marginal cost (LMC) is equal to its long-run average cost (LAC). At this point, the firm is producing at the minimum efficient scale, which means that it is producing at the lowest possible cost.

At the same time, the price of the good or service that the firm is selling (P) must be equal to its long-run marginal cost (LMC) and its long-run average cost (LAC). This condition ensures that the firm is earning zero economic profit in the long run.

Implications of these Conditions

When a firm is in long-run equilibrium, it is operating at maximum efficiency. It is producing at the lowest possible cost and selling its output at a price that is just enough to cover its costs. As a result, there is no incentive for new firms to enter the market, and existing firms have no reason to leave.

In this state of equilibrium, the market is perfectly competitive, with many firms producing the same good or service. Consumers benefit from the low prices that result from the firms' efficient production, and the firms themselves are able to earn a reasonable rate of return on their investments.

Conclusion

In conclusion, the conditions for long-run equilibrium of a competitive firm are that its long-run marginal cost (LMC) must be equal to its long-run average cost (LAC), and both these costs must be equal to the price (P) of the good or service. When these conditions are met, the firm is operating at maximum efficiency and the market is perfectly competitive.

In a perfectly competitive market, there are certain conditions that must be met for a firm to achieve long-run equilibrium. These conditions are as follows:

LMC = LAC = P

In the long run, a firm in a perfectly competitive market will produce at the point where its long-run marginal cost (LMC) is equal to its long-run average cost (LAC). At this point, the firm is producing at the minimum efficient scale, which means that it is producing at the lowest possible cost.

At the same time, the price of the good or service that the firm is selling (P) must be equal to its long-run marginal cost (LMC) and its long-run average cost (LAC). This condition ensures that the firm is earning zero economic profit in the long run.

Implications of these Conditions

When a firm is in long-run equilibrium, it is operating at maximum efficiency. It is producing at the lowest possible cost and selling its output at a price that is just enough to cover its costs. As a result, there is no incentive for new firms to enter the market, and existing firms have no reason to leave.

In this state of equilibrium, the market is perfectly competitive, with many firms producing the same good or service. Consumers benefit from the low prices that result from the firms' efficient production, and the firms themselves are able to earn a reasonable rate of return on their investments.

Conclusion

In conclusion, the conditions for long-run equilibrium of a competitive firm are that its long-run marginal cost (LMC) must be equal to its long-run average cost (LAC), and both these costs must be equal to the price (P) of the good or service. When these conditions are met, the firm is operating at maximum efficiency and the market is perfectly competitive.

Before producer’s equilibrium when MR>MC, the firm earns only- a)Normal Profit

- b)Normal loss

- c)Abnormal loss

- d)Abnormal profit

Correct answer is option 'D'. Can you explain this answer?

Before producer’s equilibrium when MR>MC, the firm earns only

a)

Normal Profit

b)

Normal loss

c)

Abnormal loss

d)

Abnormal profit

|

|

Vikas Kapoor answered |

If a firm makes more than normal profit it is called super-normal profit. Supernormal profit is also called economic profit, and abnormal profit, and is earned when total revenue is greater than the total costs.

Total profits = total revenue (TR) – total costs (TC)

Abnormal Profit = MR > MC

Total profits = total revenue (TR) – total costs (TC)

Abnormal Profit = MR > MC

For maximum profit, the condition is:- a)MC=AC

- b)MR=MC

- c)AR=AC

- d)MR=AR

Correct answer is option 'B'. Can you explain this answer?

For maximum profit, the condition is:

a)

MC=AC

b)

MR=MC

c)

AR=AC

d)

MR=AR

|

|

Rajat Patel answered |

This strategy is based on the fact that the total profit reaches its maximum point where marginal revenue equals marginal profit. This is the case because the firm will continue to produce until marginal profit is equal to zero, and marginal profit equals the marginal revenue (MR) minus the marginal cost (MC).

The elasticity at a point on a straight line supply curve passing through the origin making an angle of 45°will be- a)4

- b)2

- c)3

- d)1.0

Correct answer is option 'D'. Can you explain this answer?

The elasticity at a point on a straight line supply curve passing through the origin making an angle of 45°will be

a)

4

b)

2

c)

3

d)

1.0

|

|

Sahil Khanna answered |

Degrees with the horizontal axis is equal to 1.

Explanation:

The elasticity of supply is defined as the percentage change in quantity supplied divided by the percentage change in price. Mathematically, it can be represented as:

Elasticity of Supply = (% Change in Quantity Supplied) / (% Change in Price)

For a linear supply curve passing through the origin, the slope of the curve represents the change in quantity supplied for a given change in price. This slope is constant along the curve, and equals the tangent of the angle made by the curve with the horizontal axis.

In this case, the angle is 45 degrees, which means the slope is 1. Therefore, for a given change in price, the quantity supplied changes by the same percentage. This implies that the elasticity of supply is 1, which means that supply is unit elastic at every point along the curve.

Explanation:

The elasticity of supply is defined as the percentage change in quantity supplied divided by the percentage change in price. Mathematically, it can be represented as:

Elasticity of Supply = (% Change in Quantity Supplied) / (% Change in Price)

For a linear supply curve passing through the origin, the slope of the curve represents the change in quantity supplied for a given change in price. This slope is constant along the curve, and equals the tangent of the angle made by the curve with the horizontal axis.

In this case, the angle is 45 degrees, which means the slope is 1. Therefore, for a given change in price, the quantity supplied changes by the same percentage. This implies that the elasticity of supply is 1, which means that supply is unit elastic at every point along the curve.

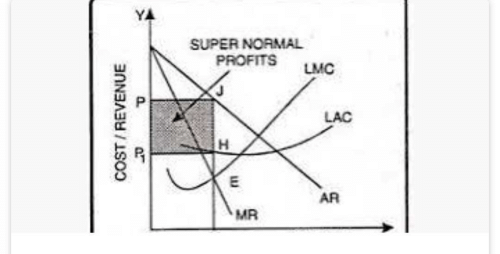

Supernormal profit occur, when?- a)Total revenue is equal to variable cost

- b)Average revenue is more than average cost

- c)Average revenue is equal to average cost

- d)Total revenue is equal to total cost

Correct answer is option 'B'. Can you explain this answer?

Supernormal profit occur, when?

a)

Total revenue is equal to variable cost

b)

Average revenue is more than average cost

c)

Average revenue is equal to average cost

d)

Total revenue is equal to total cost

|

|

Poonam Reddy answered |

Supernormal profit is defined as extra profit above that level of normal profit. Supernormal profit is also known as abnormal profit. Abnormal profit means there is an incentive for other firms to enter the industry.

In which of the following types of market structures, are resources, assumed to be mobile?- a)Oligopoly

- b)Perfect competition

- c)Monopolistic competition

- d)Monopoly

Correct answer is option 'B'. Can you explain this answer?

In which of the following types of market structures, are resources, assumed to be mobile?

a)

Oligopoly

b)

Perfect competition

c)

Monopolistic competition

d)

Monopoly

|

|

Ishan Choudhury answered |

Pure or perfect competition is a theoretical market structure in which the following criteria are met:

1. All firms sell an identical product (the product is a "commodity" or "homogeneous").

2. All firms are price takers (they cannot influence the market price of their product).

3. Market share has no influence on prices.

4. Buyers have complete or "perfect" information—in the past, present and future—about the product being sold and the prices charged by each firm.

5. Resources for such a labor are perfectly mobile.

6. Firms can enter or exit the market without cost.

1. All firms sell an identical product (the product is a "commodity" or "homogeneous").

2. All firms are price takers (they cannot influence the market price of their product).

3. Market share has no influence on prices.

4. Buyers have complete or "perfect" information—in the past, present and future—about the product being sold and the prices charged by each firm.

5. Resources for such a labor are perfectly mobile.

6. Firms can enter or exit the market without cost.

A rational consumer is a person who?- a)Has perfect knowledge of the market

- b)Is not influenced by persuasive advertising

- c)Behaves at all times, other things being equal, in a judicious manner

- d)Knows the prices of goods in different market and buys the cheapest

Correct answer is option 'A'. Can you explain this answer?

A rational consumer is a person who?

a)

Has perfect knowledge of the market

b)

Is not influenced by persuasive advertising

c)

Behaves at all times, other things being equal, in a judicious manner

d)

Knows the prices of goods in different market and buys the cheapest

|

|

Alok Verma answered |

A rational consumer is considered to be that person who makes rational consumption decisions.

In other words, the consumer who makes his choices after considering all the other alternative goods (and services) available in the market is called a rational consumer.

Beyond producer’s equilibrium when MR<MC, the firm earns only- a)Abnormal profit

- b)Normal loss

- c)Abnormal loss

- d)Normal Profit

Correct answer is option 'C'. Can you explain this answer?

Beyond producer’s equilibrium when MR<MC, the firm earns only

a)

Abnormal profit

b)

Normal loss

c)

Abnormal loss

d)

Normal Profit

|

Aravind Saha answered |

Marginal Cost < Marginal Revenue means abnormal loss situation, where the total revenue of a business does not cover total cost incurred for the business, due to which the profits of the business are below normal limits.

While a seller under perfect competition equates price and MC to maximize profits a monopolist should equate?- a)MR and MC

- b)AR and MR

- c)AR and MC

- d)TC and TR

Correct answer is option 'A'. Can you explain this answer?

While a seller under perfect competition equates price and MC to maximize profits a monopolist should equate?

a)

MR and MC

b)

AR and MR

c)

AR and MC

d)

TC and TR

|

|

Vikas Kapoor answered |

In a monopolistic market, there is only one firm that produces a product. There is absolute product differentiation because there is no substitute.

The marginal cost of production is the change in the total cost that arises when there is a change in the quantity produced.

The marginal revenue is the change in the total revenue that arises when there is a change in the quantity produced a firm maximizes its total profit by equating marginal cost to marginal revenue and solving for the price of one product and the quantity it must produce.

The elasticity at a point on a straight line supply curve passing through the origin will be- a)3

- b)1.0

- c)4

- d)2

Correct answer is option 'B'. Can you explain this answer?

The elasticity at a point on a straight line supply curve passing through the origin will be

a)

3

b)

1.0

c)

4

d)

2

|

|

Arun Yadav answered |

Regardless of the gradient of the linear supply curve or its position on the supply curve, the PES of a linear supply curve that passes through the origin is always equal to 1. Therefore, if the supply curve originates with P=0 and Q=0, the elasticity will always be 1.

Formula-

%Change in quantity

%change in price.

Formula-

%Change in quantity

%change in price.

A competitive firm in the short run incurs losses. The firm continues production, if?- a)P=AVC

- b)P>AVC

- c)P<AVC

- d)P>=AVC

Correct answer is option 'D'. Can you explain this answer?

A competitive firm in the short run incurs losses. The firm continues production, if?

a)

P=AVC

b)

P>AVC

c)

P<AVC

d)

P>=AVC

|

|

Om Desai answered |

With loss minimization, price exceeds average variable cost but is less than average total cost at the quantity that equates marginal revenue and marginal cost. In this case, the firm incurs a smaller loss by producing some output than by not producing any output.

Globalization has made Indian Market as?- a)Seller market

- b)Buyer market

- c)Monopsony market

- d)Monopoly market

Correct answer is option 'B'. Can you explain this answer?

Globalization has made Indian Market as?

a)

Seller market

b)

Buyer market

c)

Monopsony market

d)

Monopoly market

|

|

Nandini Iyer answered |

Globalisation is the rapid integration or interconnection between countries mostly on the economic plane. In other words Globalisation means integrating our economy with the world economy.Movement of people between countries increases due to globalisation. CORRECT OPTION IS (B).

At producer’s equilibrium when MR=MC, the firm earns only- a)Abnormal loss

- b)Abnormal profit

- c)Normal Profit

- d)Normal loss

Correct answer is option 'C'. Can you explain this answer?

At producer’s equilibrium when MR=MC, the firm earns only

a)

Abnormal loss

b)

Abnormal profit

c)

Normal Profit

d)

Normal loss

|

|

Anjali Sharma answered |

Producer’s equilibrium refers to the state in which a producer earns his maximum profit or minimises its losses. According to the MR-MC approach, the producer is at equilibrium when the Marginal Revenue (MR) is equal to the Marginal Cost (MC), and the Marginal Cost curve must cut the Marginal Revenue curve from below.

Two conditions under this approach are:

(i) MR = MC

(ii) MC curve should cut the MR curve from below, or MC should be rising.

Marginal revenue in any competitive situation is?- a)Trn-Pn-1

- b)TRn-TRn-1

- c)TRn/Qn-1

- d)None of above

Correct answer is option 'B'. Can you explain this answer?

Marginal revenue in any competitive situation is?

a)

Trn-Pn-1

b)

TRn-TRn-1

c)

TRn/Qn-1

d)

None of above

|

Neha Choudhury answered |

Marginal revenue (MR) can be defined as additional revenue gained from the additional unit of output. Marginal revenue is the change in total revenue which results from the sale of one more or one less unit of output.

Formula:

Total revenue=TR

Total Unit = n

Total Unit less one unit = n-1

MR= TRn-TRn-1.

Formula:

Total revenue=TR

Total Unit = n

Total Unit less one unit = n-1

MR= TRn-TRn-1.

MR curve=AR=Demand curve is a feature of which kind of market?- a)Perfect competition

- b)Oligopoly

- c)Monopolistic competition

- d)Monopoly

Correct answer is option 'A'. Can you explain this answer?

MR curve=AR=Demand curve is a feature of which kind of market?

a)

Perfect competition

b)

Oligopoly

c)

Monopolistic competition

d)

Monopoly

|

|

Pj Commerce Academy answered |

MR curve=AR=Demand curve is a feature of which kind of market?

The feature of MR curve=AR=Demand curve is characteristic of a perfect competition market. In a perfect competition market, there are numerous buyers and sellers of homogeneous products. Here is a detailed explanation:

1. Perfect competition:

- Perfect competition is a market structure where there are many buyers and sellers.

- The products sold in this market are identical or homogeneous, meaning they are indistinguishable from each other.

- There is free entry and exit of firms in the market, allowing for easy competition.

- The information is perfect, and all participants have full knowledge of prices and market conditions.

- In perfect competition, firms are price takers, meaning they cannot influence the market price.

- The demand curve faced by a firm in perfect competition is perfectly elastic, i.e., horizontal.

- Marginal revenue (MR) is equal to average revenue (AR), which is equal to the demand curve.

2. MR curve=AR=Demand curve:

- In perfect competition, since the firm is a price taker, it can only sell its output at the prevailing market price.

- The demand curve faced by the firm is perfectly elastic, meaning any change in quantity will not affect the price.

- Consequently, the average revenue (AR) curve, which represents the price at which the firm sells its output, is a horizontal line.

- Since the firm can sell additional units only at the prevailing market price, the marginal revenue (MR) curve is also horizontal and coincides with the AR curve.

- Therefore, in perfect competition, the MR curve, AR curve, and demand curve are all the same.

Conclusion:

- The feature of MR curve=AR=Demand curve is unique to perfect competition.

- In other market structures like oligopoly, monopolistic competition, and monopoly, the MR curve, AR curve, and demand curve are not equal.

- Thus, the correct answer to the question is A: Perfect competition.

The feature of MR curve=AR=Demand curve is characteristic of a perfect competition market. In a perfect competition market, there are numerous buyers and sellers of homogeneous products. Here is a detailed explanation:

1. Perfect competition:

- Perfect competition is a market structure where there are many buyers and sellers.

- The products sold in this market are identical or homogeneous, meaning they are indistinguishable from each other.

- There is free entry and exit of firms in the market, allowing for easy competition.

- The information is perfect, and all participants have full knowledge of prices and market conditions.

- In perfect competition, firms are price takers, meaning they cannot influence the market price.

- The demand curve faced by a firm in perfect competition is perfectly elastic, i.e., horizontal.

- Marginal revenue (MR) is equal to average revenue (AR), which is equal to the demand curve.

2. MR curve=AR=Demand curve:

- In perfect competition, since the firm is a price taker, it can only sell its output at the prevailing market price.

- The demand curve faced by the firm is perfectly elastic, meaning any change in quantity will not affect the price.

- Consequently, the average revenue (AR) curve, which represents the price at which the firm sells its output, is a horizontal line.

- Since the firm can sell additional units only at the prevailing market price, the marginal revenue (MR) curve is also horizontal and coincides with the AR curve.

- Therefore, in perfect competition, the MR curve, AR curve, and demand curve are all the same.

Conclusion:

- The feature of MR curve=AR=Demand curve is unique to perfect competition.

- In other market structures like oligopoly, monopolistic competition, and monopoly, the MR curve, AR curve, and demand curve are not equal.

- Thus, the correct answer to the question is A: Perfect competition.

Under which market situation demand curve is linear and parallel to X-axis?- a)Monopoly

- b)Oligopoly

- c)Perfect competition

- d)Monopolistic competition

Correct answer is option 'C'. Can you explain this answer?

Under which market situation demand curve is linear and parallel to X-axis?

a)

Monopoly

b)

Oligopoly

c)

Perfect competition

d)

Monopolistic competition

|

BT Educators answered |

Answer:

Market situation: Perfect competition

Explanation:

1. Characteristics of perfect competition:

- A large number of buyers and sellers

- Homogeneous products

- Perfect knowledge and information

- No barriers to entry or exit

- Price takers - firms have no control over the price

2. Demand curve in perfect competition:

- Perfectly competitive firms face a perfectly elastic demand curve.

- The demand curve is horizontal or parallel to the X-axis because the firm can sell as much as it wants at the market price.

- The price is determined by the market forces of supply and demand, and individual firms have no influence on it.

- If a firm tries to charge a higher price, buyers will shift their demand to other firms in the market.

- If a firm tries to charge a lower price, it will not be able to sell any additional quantity because buyers can already purchase as much as they want at the market price.

3. Linear demand curve:

- A linear demand curve is a straight line on a graph, indicating a constant rate of change in quantity demanded for each unit change in price.

- In perfect competition, the demand curve is linear because the price remains constant regardless of the quantity demanded by the firm.

- As the firm increases its output, it can sell all the additional units at the market price.

Therefore, in a market situation of perfect competition, the demand curve is linear and parallel to the X-axis.

Under perfect competition the number of firms- a)Is about 10

- b)Are many but limited

- c)Is large

- d)Is limited

Correct answer is option 'C'. Can you explain this answer?

Under perfect competition the number of firms

a)

Is about 10

b)

Are many but limited

c)

Is large

d)

Is limited

|

|

Anjali Sharma answered |

Perfect competition is a type of market where there are many buyers and sellers, and all of them initiate the buying and selling mechanism. There are no restrictions and no direct competition in the market. It is assumed that all the sellers are selling identical or homogenous products.

If under perfect competition, the price lies below the average cost curve, the firm would?- a)Make only normal profits

- b)Profit cannot be determined

- c)Make abnormal profits

- d)Incur losses

Correct answer is option 'D'. Can you explain this answer?

If under perfect competition, the price lies below the average cost curve, the firm would?

a)

Make only normal profits

b)

Profit cannot be determined

c)

Make abnormal profits

d)

Incur losses

|

|

Rohini Desai answered |

Under perfect competition, the price is determined by the market forces of demand and supply. If the price lies below the average cost curve, it means that the firm is selling its product at a price that is lower than the average cost of production. In such a scenario, the firm would incur losses because its costs of production would be higher than the revenue it earns from selling the product.

Here is a detailed explanation of why the firm would incur losses:

1. Price determination under perfect competition:

- In perfect competition, the price is determined by the equilibrium point of demand and supply in the market.

- The firm is a price taker and has no control over the price.

- It can only adjust its quantity of output to maximize its profits.

2. Average cost curve and profit:

- The average cost curve represents the average cost of production per unit of output.

- It is U-shaped, with economies of scale in the beginning and diseconomies of scale at higher levels of output.

- The average cost curve intersects with the marginal cost curve at its minimum point.

- If the price is below the average cost curve, it means that the firm is unable to cover its costs of production.

3. Losses in the short run:

- In the short run, the firm has fixed costs that it cannot change.

- It can only adjust its variable costs by changing the quantity of output.

- If the price is below the average cost curve, the firm's total revenue will be less than its total costs, resulting in losses.

4. Shutdown point:

- If the price falls below the average variable cost curve, the firm should shut down in the short run.

- By shutting down, the firm avoids incurring any further losses.

- However, it still incurs its fixed costs.

In conclusion, if the price lies below the average cost curve under perfect competition, the firm would incur losses in the short run. It is important for the firm to assess its costs and the prevailing market price to make informed decisions about its production and profitability.

Chapter doubts & questions for The Theory of the Firm under Perfect Competition - Economics CUET Preparation 2025 is part of Commerce exam preparation. The chapters have been prepared according to the Commerce exam syllabus. The Chapter doubts & questions, notes, tests & MCQs are made for Commerce 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises, MCQs and online tests here.

Chapter doubts & questions of The Theory of the Firm under Perfect Competition - Economics CUET Preparation in English & Hindi are available as part of Commerce exam.

Download more important topics, notes, lectures and mock test series for Commerce Exam by signing up for free.

Economics CUET Preparation

142 videos|21 docs|75 tests

|

|

© EduRev

|

Education Revolution

|

|

Signup on EduRev and stay on top of your study goals

10M+ students crushing their study goals daily