Test: Introduction To Partnership Accounts - 2 - Commerce MCQ

15 Questions MCQ Test Accountancy Class 12 - Test: Introduction To Partnership Accounts - 2

Ram and Mohan are partners. They draw Rs. 6,000 and Rs. 4,000 for private use, respectively. Interest is charged at 6 percent per annum on their drawings. What is the interest on their drawings?

A and B are partners sharing profits and losses in the ratio of 4:1. C was a manager who received the salary of Rs. 2000 p.m. in addition to a commission of 5% on net profits after charging such commission. Profits for the year is Rs. 3,39,000 before charging salary. Find total remuneration of C:

Ram is a partner. He made drawings as follows:

July 1 Rs. 200

August 1 Rs. 200

September 1 Rs. 300

November 1 Rs. 50

February 1 Rs. 100

If the rate of interest on drawings is 6% and accounts are closed on March 31 the interest on drawing is:

July 1 Rs. 200

August 1 Rs. 200

September 1 Rs. 300

November 1 Rs. 50

February 1 Rs. 100

Profit or loss on revaluation is shared among the old partners in _______ ratio.

Subject to contract between the partners, interest on capital is to be provided out of profits only. In case of insufficient profits (i.e. net profit less than the amount of interest on capital), the amount of profit is distributed:

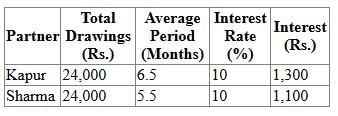

Kapur and Sharma are partners in a partnership firm. Calculate the interest on drawings made by Kapur and Sharma @ 10% p.a. for the year ending 31st December 2013. If, Kapur withdrew Rs. 2,000 per month in the beginning whereas Sharma withdrew same amount at the end of every month.

Aryan and Gauri were partner in a firm sharing profits and losses in the ratio of 2:1. Their capital was R.s. 90,000 and Rs. 60,000 respectively. They were entitled for interest on capital @ 12% p.a. The firm earned a profit of Rs. 84,000 after allowing interest on capitals. Profits will be distributed among them will be:

If there is no partnership deed then interest on capital will be charged at ……….p.a.

Partners are suppose to pay interest on drawings only when ……………..by the ………

In the absence of an agreement, partners are entitled to

What balance does a Partner’s Current Account has?

What time would be taken into consideration if equal monthly amount is drawn as drawings at the beginning of each month?

Features of a partnership firm are:

How would you close the Partner’s Drawings Account?

|

42 videos|168 docs|43 tests

|

Important Questions for Introduction To Partnership Accounts - 2

Introduction To Partnership Accounts - 2 MCQs with Answers

Online Tests for Introduction To Partnership Accounts - 2 Accountancy Class 12

|

© EduRev

|

Education Revolution

|

|