B Com Exam > B Com Questions > Transport company purchased a truck from a ak...

Start Learning for Free

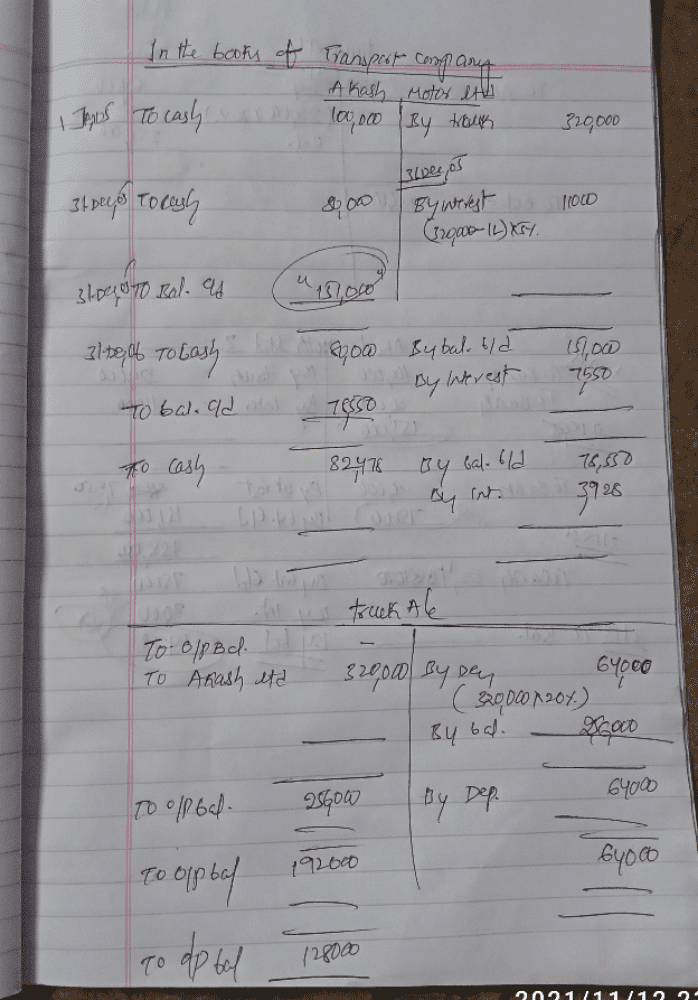

Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company?

Most Upvoted Answer

Transport company purchased a truck from a akash motors ltd.on instalm...

Accounts for Truck Purchased on Instalment Payment System

Cash Payment Schedule

- Rs 100,000 on delivery on 1st January 2005

- Rs 80,000 on 31st Dec. 2005

- Rs 80,000 on 31st Dec. 2006

- Rs 82,478 on 31st Dec. 2007

Interest Calculation

- Balance amount after each payment:

- 31st Dec. 2005: Rs 220,000 (Rs 320,000 - Rs 100,000)

- 31st Dec. 2006: Rs 140,000 (Rs 220,000 - Rs 80,000)

- 31st Dec. 2007: Rs 60,000 (Rs 140,000 - Rs 80,000)

- Interest charged at 5% p.a on balance amount:

- 31st Dec. 2005: Rs 11,000 (Rs 220,000 x 5%)

- 31st Dec. 2006: Rs 7,000 (Rs 140,000 x 5%)

- 31st Dec. 2007: Rs 3,000 (Rs 60,000 x 5%)

- Total Interest: Rs 21,000

Depreciation Calculation

- 20% depreciation charged on cost price of Rs 320,000:

- 2005: Rs 64,000 (Rs 320,000 x 20%)

- 2006: Rs 64,000 (Rs 320,000 x 20%)

- 2007: Rs 64,000 (Rs 320,000 x 20%)

Accounts in Books of Transport Company

- Purchase of Truck Account: Debit Rs 320,000

- Cash Account: Credit Rs 100,000, Rs 80,000, Rs 80,000, Rs 82,478

- Interest on Instalments Account: Debit Rs 21,000

- Depreciation on Truck Account: Debit Rs 192,000 (Rs 64,000 x 3)

- Truck Account: Balance of Rs 47,522 (Rs 320,000 - Rs 100,000 - Rs 80,000 - Rs 80,000 - Rs 82,478 - Rs 21,000 - Rs 192,000)

Explanation

The purchase of the truck is recorded in the Purchase of Truck Account, while the cash payments are recorded in the Cash Account. Interest charged by Akash Motors Ltd. is recorded in the Interest on Instalments Account, while depreciation charged by the transport company is recorded in the Depreciation on Truck Account. The Truck Account reflects the balance amount of the truck after all the transactions and adjustments.

Cash Payment Schedule

- Rs 100,000 on delivery on 1st January 2005

- Rs 80,000 on 31st Dec. 2005

- Rs 80,000 on 31st Dec. 2006

- Rs 82,478 on 31st Dec. 2007

Interest Calculation

- Balance amount after each payment:

- 31st Dec. 2005: Rs 220,000 (Rs 320,000 - Rs 100,000)

- 31st Dec. 2006: Rs 140,000 (Rs 220,000 - Rs 80,000)

- 31st Dec. 2007: Rs 60,000 (Rs 140,000 - Rs 80,000)

- Interest charged at 5% p.a on balance amount:

- 31st Dec. 2005: Rs 11,000 (Rs 220,000 x 5%)

- 31st Dec. 2006: Rs 7,000 (Rs 140,000 x 5%)

- 31st Dec. 2007: Rs 3,000 (Rs 60,000 x 5%)

- Total Interest: Rs 21,000

Depreciation Calculation

- 20% depreciation charged on cost price of Rs 320,000:

- 2005: Rs 64,000 (Rs 320,000 x 20%)

- 2006: Rs 64,000 (Rs 320,000 x 20%)

- 2007: Rs 64,000 (Rs 320,000 x 20%)

Accounts in Books of Transport Company

- Purchase of Truck Account: Debit Rs 320,000

- Cash Account: Credit Rs 100,000, Rs 80,000, Rs 80,000, Rs 82,478

- Interest on Instalments Account: Debit Rs 21,000

- Depreciation on Truck Account: Debit Rs 192,000 (Rs 64,000 x 3)

- Truck Account: Balance of Rs 47,522 (Rs 320,000 - Rs 100,000 - Rs 80,000 - Rs 80,000 - Rs 82,478 - Rs 21,000 - Rs 192,000)

Explanation

The purchase of the truck is recorded in the Purchase of Truck Account, while the cash payments are recorded in the Cash Account. Interest charged by Akash Motors Ltd. is recorded in the Interest on Instalments Account, while depreciation charged by the transport company is recorded in the Depreciation on Truck Account. The Truck Account reflects the balance amount of the truck after all the transactions and adjustments.

Community Answer

Transport company purchased a truck from a akash motors ltd.on instalm...

|

Explore Courses for B Com exam

|

|

Similar B Com Doubts

Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company?

Question Description

Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company? for B Com 2024 is part of B Com preparation. The Question and answers have been prepared according to the B Com exam syllabus. Information about Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company? covers all topics & solutions for B Com 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company?.

Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company? for B Com 2024 is part of B Com preparation. The Question and answers have been prepared according to the B Com exam syllabus. Information about Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company? covers all topics & solutions for B Com 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company?.

Solutions for Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company? in English & in Hindi are available as part of our courses for B Com.

Download more important topics, notes, lectures and mock test series for B Com Exam by signing up for free.

Here you can find the meaning of Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company? defined & explained in the simplest way possible. Besides giving the explanation of

Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company?, a detailed solution for Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company? has been provided alongside types of Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company? theory, EduRev gives you an

ample number of questions to practice Transport company purchased a truck from a akash motors ltd.on instalment payment system. Cash price of truck was Rs 320000 which was paid as follow :Rs 100000 on delivery on1st January 2005; Rs 80000 on 31st Dec.2005, Rs 80000 on 31st Dec. 2006 and Rs 82 478 on 31st Dec. 2007.akash motors charged 5% Interest p.a on balance. Purchaser company charged 20% depreciation on cost price. Prepare necessary accounts in the books of transport company? tests, examples and also practice B Com tests.

|

|

Explore Courses for B Com exam

|

|

Suggested Free Tests

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup