Class 11 Exam > Class 11 Questions > Qualitative characteristics of accounting inf...

Start Learning for Free

Qualitative characteristics of accounting information?

Most Upvoted Answer

Qualitative characteristics of accounting information?

Community Answer

Qualitative characteristics of accounting information?

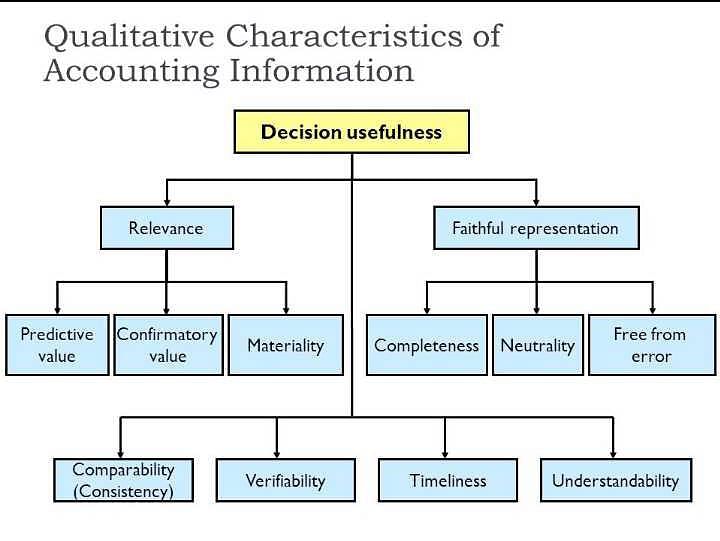

Qualitative Characteristics of Accounting Information

Accounting information is essential for decision-making, and it must be relevant, reliable, comparable, and understandable. These characteristics are known as qualitative characteristics of accounting information. The International Accounting Standards Board (IASB) has identified four primary qualitative characteristics of accounting information. These characteristics are discussed below.

1. Relevance

Relevance is the first and foremost qualitative characteristic of accounting information. Relevant information is capable of making a difference in the decision-making process. To be relevant, accounting information must have predictive value, confirmatory value, and materiality. Predictive value means that the information must be able to predict future events. The confirmatory value means that the information must be able to confirm or refute prior expectations. Additionally, information must be material to be relevant, which means it must be important enough to make a difference in the decision-making process.

2. Reliability

Reliability is another critical qualitative characteristic of accounting information. Reliable information is free from errors and biases and can be depended upon by users to make decisions. To be reliable, accounting information must be verifiable, faithful representation, and neutral. Verifiability means that different users must arrive at the same conclusion after examining the information. Faithful representation means that the information must be complete, accurate, and free from material errors. Neutrality means that the information must be free from bias.

3. Comparability

Comparability means that accounting information must be presented in a way that allows for easy comparison with other information. Comparability is essential for decision-making because it allows users to identify trends and make comparisons across different periods and different entities. To be comparable, accounting information must be presented in a consistent manner over time and across entities.

4. Understandability

Understandability is the final qualitative characteristic of accounting information. Understandability means that the information must be presented in a way that is clear and understandable to users with a reasonable knowledge of business and economic activities. To be understandable, accounting information must be presented in a clear and concise manner and must be free from unnecessary complexity.

Conclusion

In conclusion, the qualitative characteristics of accounting information are essential for decision-making. The information must be relevant, reliable, comparable, and understandable. These characteristics ensure that users can rely on the information to make informed decisions that can impact their businesses positively.

Accounting information is essential for decision-making, and it must be relevant, reliable, comparable, and understandable. These characteristics are known as qualitative characteristics of accounting information. The International Accounting Standards Board (IASB) has identified four primary qualitative characteristics of accounting information. These characteristics are discussed below.

1. Relevance

Relevance is the first and foremost qualitative characteristic of accounting information. Relevant information is capable of making a difference in the decision-making process. To be relevant, accounting information must have predictive value, confirmatory value, and materiality. Predictive value means that the information must be able to predict future events. The confirmatory value means that the information must be able to confirm or refute prior expectations. Additionally, information must be material to be relevant, which means it must be important enough to make a difference in the decision-making process.

2. Reliability

Reliability is another critical qualitative characteristic of accounting information. Reliable information is free from errors and biases and can be depended upon by users to make decisions. To be reliable, accounting information must be verifiable, faithful representation, and neutral. Verifiability means that different users must arrive at the same conclusion after examining the information. Faithful representation means that the information must be complete, accurate, and free from material errors. Neutrality means that the information must be free from bias.

3. Comparability

Comparability means that accounting information must be presented in a way that allows for easy comparison with other information. Comparability is essential for decision-making because it allows users to identify trends and make comparisons across different periods and different entities. To be comparable, accounting information must be presented in a consistent manner over time and across entities.

4. Understandability

Understandability is the final qualitative characteristic of accounting information. Understandability means that the information must be presented in a way that is clear and understandable to users with a reasonable knowledge of business and economic activities. To be understandable, accounting information must be presented in a clear and concise manner and must be free from unnecessary complexity.

Conclusion

In conclusion, the qualitative characteristics of accounting information are essential for decision-making. The information must be relevant, reliable, comparable, and understandable. These characteristics ensure that users can rely on the information to make informed decisions that can impact their businesses positively.

Attention Class 11 Students!

To make sure you are not studying endlessly, EduRev has designed Class 11 study material, with Structured Courses, Videos, & Test Series. Plus get personalized analysis, doubt solving and improvement plans to achieve a great score in Class 11.

|

Explore Courses for Class 11 exam

|

|

Similar Class 11 Doubts

Top Courses for Class 11View all

Qualitative characteristics of accounting information?

Question Description

Qualitative characteristics of accounting information? for Class 11 2024 is part of Class 11 preparation. The Question and answers have been prepared according to the Class 11 exam syllabus. Information about Qualitative characteristics of accounting information? covers all topics & solutions for Class 11 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Qualitative characteristics of accounting information?.

Qualitative characteristics of accounting information? for Class 11 2024 is part of Class 11 preparation. The Question and answers have been prepared according to the Class 11 exam syllabus. Information about Qualitative characteristics of accounting information? covers all topics & solutions for Class 11 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Qualitative characteristics of accounting information?.

Solutions for Qualitative characteristics of accounting information? in English & in Hindi are available as part of our courses for Class 11.

Download more important topics, notes, lectures and mock test series for Class 11 Exam by signing up for free.

Here you can find the meaning of Qualitative characteristics of accounting information? defined & explained in the simplest way possible. Besides giving the explanation of

Qualitative characteristics of accounting information?, a detailed solution for Qualitative characteristics of accounting information? has been provided alongside types of Qualitative characteristics of accounting information? theory, EduRev gives you an

ample number of questions to practice Qualitative characteristics of accounting information? tests, examples and also practice Class 11 tests.

|

|

Explore Courses for Class 11 exam

|

|

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

Follow Us

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup