B Com Exam > B Com Questions > Define production possibility curve?

Start Learning for Free

Define production possibility curve?

Most Upvoted Answer

Define production possibility curve?

Community Answer

Define production possibility curve?

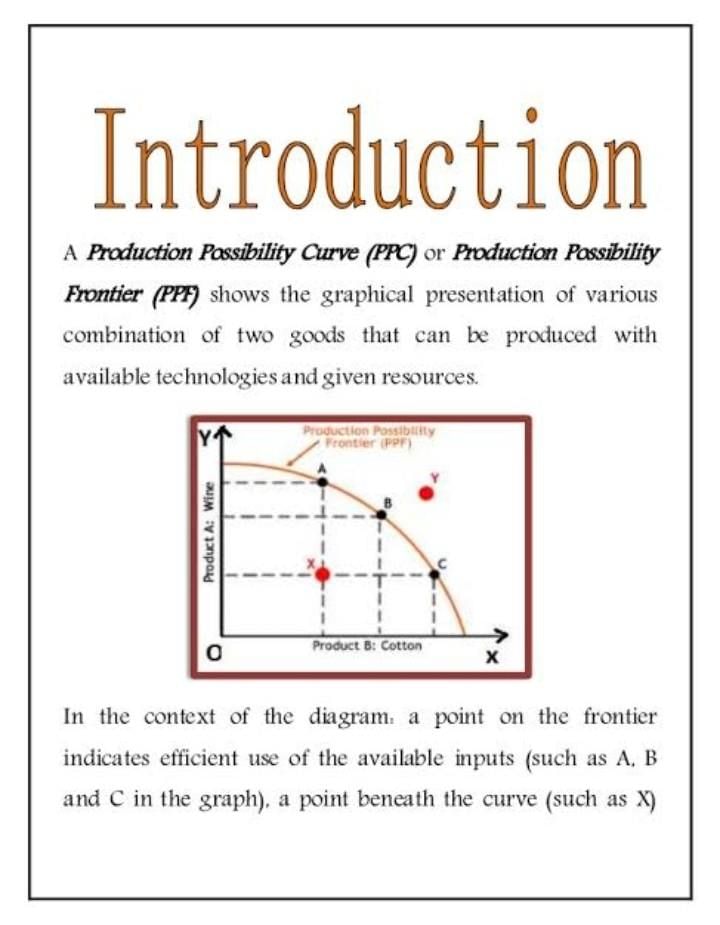

Production Possibility Curve

The production possibility curve (PPC), also known as the production possibility frontier (PPF), is a graphical representation that shows the different combinations of two goods or services that an economy can produce efficiently using its given resources and technology. It illustrates the concept of trade-offs and opportunity costs in an economy.

Key Points:

- The PPC is a downward-sloping curve that demonstrates the maximum potential production levels of two goods or services in an economy. It is based on the assumption that resources are fully utilized and allocated efficiently.

- The PPC is typically depicted on a graph with one good or service on the x-axis and the other on the y-axis. Each point on the curve represents a combination of the two goods or services that can be produced using all available resources.

- The shape of the PPC is concave, indicating increasing opportunity costs. This means that as more of one good is produced, the opportunity cost of producing an additional unit of that good increases in terms of the other good that must be given up.

- The points along the PPC are considered efficient because they represent the maximum output achievable with the given resources. Points inside the curve are inefficient, while points outside the curve are unattainable with the current level of resources and technology.

- Factors that can shift the PPC include changes in available resources, technological advancements, and improvements in productivity. If there is an increase in resources or technology, the PPC can shift outward, allowing for higher levels of production.

- The PPC also serves as a tool to illustrate the concept of economic growth. When an economy experiences growth, the PPC expands, indicating an increase in the potential production levels of both goods or services.

Summary:

The production possibility curve is a graphical representation of the different combinations of two goods or services that an economy can efficiently produce using its available resources and technology. It shows the trade-offs and opportunity costs involved in production. The curve is concave, indicating increasing opportunity costs, and can shift outward with changes in resources or technology. The PPC helps illustrate the concept of efficiency, inefficiency, and economic growth in an economy.

The production possibility curve (PPC), also known as the production possibility frontier (PPF), is a graphical representation that shows the different combinations of two goods or services that an economy can produce efficiently using its given resources and technology. It illustrates the concept of trade-offs and opportunity costs in an economy.

Key Points:

- The PPC is a downward-sloping curve that demonstrates the maximum potential production levels of two goods or services in an economy. It is based on the assumption that resources are fully utilized and allocated efficiently.

- The PPC is typically depicted on a graph with one good or service on the x-axis and the other on the y-axis. Each point on the curve represents a combination of the two goods or services that can be produced using all available resources.

- The shape of the PPC is concave, indicating increasing opportunity costs. This means that as more of one good is produced, the opportunity cost of producing an additional unit of that good increases in terms of the other good that must be given up.

- The points along the PPC are considered efficient because they represent the maximum output achievable with the given resources. Points inside the curve are inefficient, while points outside the curve are unattainable with the current level of resources and technology.

- Factors that can shift the PPC include changes in available resources, technological advancements, and improvements in productivity. If there is an increase in resources or technology, the PPC can shift outward, allowing for higher levels of production.

- The PPC also serves as a tool to illustrate the concept of economic growth. When an economy experiences growth, the PPC expands, indicating an increase in the potential production levels of both goods or services.

Summary:

The production possibility curve is a graphical representation of the different combinations of two goods or services that an economy can efficiently produce using its available resources and technology. It shows the trade-offs and opportunity costs involved in production. The curve is concave, indicating increasing opportunity costs, and can shift outward with changes in resources or technology. The PPC helps illustrate the concept of efficiency, inefficiency, and economic growth in an economy.

|

Explore Courses for B Com exam

|

|

Similar B Com Doubts

Define production possibility curve?

Question Description

Define production possibility curve? for B Com 2024 is part of B Com preparation. The Question and answers have been prepared according to the B Com exam syllabus. Information about Define production possibility curve? covers all topics & solutions for B Com 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Define production possibility curve?.

Define production possibility curve? for B Com 2024 is part of B Com preparation. The Question and answers have been prepared according to the B Com exam syllabus. Information about Define production possibility curve? covers all topics & solutions for B Com 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Define production possibility curve?.

Solutions for Define production possibility curve? in English & in Hindi are available as part of our courses for B Com.

Download more important topics, notes, lectures and mock test series for B Com Exam by signing up for free.

Here you can find the meaning of Define production possibility curve? defined & explained in the simplest way possible. Besides giving the explanation of

Define production possibility curve?, a detailed solution for Define production possibility curve? has been provided alongside types of Define production possibility curve? theory, EduRev gives you an

ample number of questions to practice Define production possibility curve? tests, examples and also practice B Com tests.

|

|

Explore Courses for B Com exam

|

|

Suggested Free Tests

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

Follow Us

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup