Class 12 Exam > Class 12 Questions > Why is the equality between marginal cost and...

Start Learning for Free

Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.?

Verified Answer

Why is the equality between marginal cost and marginal revenue necessa...

Equilibrium refers to a state of rest when no change is required. A firm (producer) is said to be in equilibrium when it has no inclination to expand or to contract its output. This state either reflects maximum profits or minimum losses.

According to MC=MR approach, As long as MC is less than MR, it is profitable for the producer to go on producing more because it adds to its profits. He stops producing more only when MC becomes equal to MR.

When MC is greater than MR after equilibrium, it means producing more will lead to decline

in profits.

Both the conditions are needed for Firm’s Equilibrium:

1. MC = MR:

MR is the addition to TR from sale of one more unit of output and MC is addition to TC for increasing production by one unit. Every producer aims to maximize the total profits. For this, a firm compares it’s MR with its MC. Profits will increase as long as MR exceeds MC and profits will fall if MR is less than MC. So, equilibrium is not achieved when MC < MR as it is possible to add to profits by producing more. Producer is also not in equilibrium when MC > MR because benefit is less than the cost. It means, the firm will be at

equilibrium when MC = MR.

2. MC is greater than MR after MC = MR output level:

MC = MR is a necessary condition, but not sufficient enough to ensure equilibrium. Only that output level is the equilibrium output when MC becomes greater than MR after the equilibrium.

It is because if MC is greater than MR, then producing beyond MC = MR output will reduce profits. On the other hand, if MC is less than MR beyond MC = MR output, it is possible to add to profits by producing more. So, first condition must be supplemented with the second condition to attain the producer’s equilibrium.

This question is part of UPSC exam. View all Class 12 courses

This question is part of UPSC exam. View all Class 12 courses

Most Upvoted Answer

Why is the equality between marginal cost and marginal revenue necessa...

The Equality between Marginal Cost and Marginal Revenue in Firm Equilibrium

An Introduction to Equilibrium

Equilibrium in a firm occurs when it maximizes its profits by producing and selling a certain quantity of goods or services. This equilibrium point is where the firm's marginal cost (MC) is equal to its marginal revenue (MR). Marginal cost represents the additional cost incurred by the firm when producing one more unit of output, while marginal revenue indicates the additional revenue generated by selling one more unit of output.

The Importance of Equality

The equality between marginal cost and marginal revenue is crucial for a firm to achieve equilibrium due to the following reasons:

1. Profit Maximization: In order to maximize profits, a firm needs to produce the quantity of goods or services where its marginal cost equals its marginal revenue. At this point, the firm is neither overproducing nor underproducing, ensuring that it is efficiently allocating its resources.

2. Cost and Revenue Optimization: When marginal cost is greater than marginal revenue, it implies that the cost of producing one more unit exceeds the revenue generated from selling it. This would result in a decrease in profits. On the other hand, if marginal revenue exceeds marginal cost, the firm can increase its profits by producing more units until the equality between the two is achieved.

3. Market Competition: In a perfectly competitive market, firms are price takers and face a horizontal demand curve. The market price is equal to the marginal revenue for each unit sold. Therefore, for a firm to maximize profits, it must produce the quantity where marginal cost equals the market price (which is also equal to marginal revenue).

Equilibrium Diagram and Schedule

To illustrate the equilibrium condition, let's consider a diagram and schedule:

Diagram:

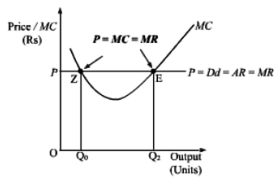

In the diagram, the x-axis represents the quantity of output produced, while the y-axis represents the cost and revenue. The marginal cost (MC) curve is upward sloping, indicating that as more units are produced, the cost of production increases. The marginal revenue (MR) curve is horizontal and coincides with the demand curve in a perfectly competitive market.

At the equilibrium point, the MC curve intersects the MR curve. This intersection represents the quantity of output where marginal cost is equal to marginal revenue, indicating that the firm is in equilibrium.

[Insert diagram here]

Schedule:

Let's consider a hypothetical schedule to further understand the equilibrium condition.

Quantity | Total Cost | Marginal Cost | Total Revenue | Marginal Revenue

----------------------------------------------------------------------

1 | $10 | $10 | $20 | $20

2 | $20 | $10 | $40 | $20

3 | $30 | $10 | $60 | $20

4 | $40 | $10 | $80 | $20

In this schedule, as the firm increases its output from 1 unit to 4 units, the marginal cost remains constant at $10, while the marginal revenue remains constant at $20. The equality between marginal cost and marginal revenue is maintained throughout, indicating equilibrium.

Conclusion

The equality between marginal cost and marginal revenue is necessary for a firm to be in equilibrium as it allows for profit maximization and cost optimization. When the equality is achieved, the firm is producing

An Introduction to Equilibrium

Equilibrium in a firm occurs when it maximizes its profits by producing and selling a certain quantity of goods or services. This equilibrium point is where the firm's marginal cost (MC) is equal to its marginal revenue (MR). Marginal cost represents the additional cost incurred by the firm when producing one more unit of output, while marginal revenue indicates the additional revenue generated by selling one more unit of output.

The Importance of Equality

The equality between marginal cost and marginal revenue is crucial for a firm to achieve equilibrium due to the following reasons:

1. Profit Maximization: In order to maximize profits, a firm needs to produce the quantity of goods or services where its marginal cost equals its marginal revenue. At this point, the firm is neither overproducing nor underproducing, ensuring that it is efficiently allocating its resources.

2. Cost and Revenue Optimization: When marginal cost is greater than marginal revenue, it implies that the cost of producing one more unit exceeds the revenue generated from selling it. This would result in a decrease in profits. On the other hand, if marginal revenue exceeds marginal cost, the firm can increase its profits by producing more units until the equality between the two is achieved.

3. Market Competition: In a perfectly competitive market, firms are price takers and face a horizontal demand curve. The market price is equal to the marginal revenue for each unit sold. Therefore, for a firm to maximize profits, it must produce the quantity where marginal cost equals the market price (which is also equal to marginal revenue).

Equilibrium Diagram and Schedule

To illustrate the equilibrium condition, let's consider a diagram and schedule:

Diagram:

In the diagram, the x-axis represents the quantity of output produced, while the y-axis represents the cost and revenue. The marginal cost (MC) curve is upward sloping, indicating that as more units are produced, the cost of production increases. The marginal revenue (MR) curve is horizontal and coincides with the demand curve in a perfectly competitive market.

At the equilibrium point, the MC curve intersects the MR curve. This intersection represents the quantity of output where marginal cost is equal to marginal revenue, indicating that the firm is in equilibrium.

[Insert diagram here]

Schedule:

Let's consider a hypothetical schedule to further understand the equilibrium condition.

Quantity | Total Cost | Marginal Cost | Total Revenue | Marginal Revenue

----------------------------------------------------------------------

1 | $10 | $10 | $20 | $20

2 | $20 | $10 | $40 | $20

3 | $30 | $10 | $60 | $20

4 | $40 | $10 | $80 | $20

In this schedule, as the firm increases its output from 1 unit to 4 units, the marginal cost remains constant at $10, while the marginal revenue remains constant at $20. The equality between marginal cost and marginal revenue is maintained throughout, indicating equilibrium.

Conclusion

The equality between marginal cost and marginal revenue is necessary for a firm to be in equilibrium as it allows for profit maximization and cost optimization. When the equality is achieved, the firm is producing

|

|

Explore Courses for Class 12 exam

|

|

Similar Class 12 Doubts

Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.?

Question Description

Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.? for Class 12 2024 is part of Class 12 preparation. The Question and answers have been prepared according to the Class 12 exam syllabus. Information about Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.? covers all topics & solutions for Class 12 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.?.

Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.? for Class 12 2024 is part of Class 12 preparation. The Question and answers have been prepared according to the Class 12 exam syllabus. Information about Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.? covers all topics & solutions for Class 12 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.?.

Solutions for Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.? in English & in Hindi are available as part of our courses for Class 12.

Download more important topics, notes, lectures and mock test series for Class 12 Exam by signing up for free.

Here you can find the meaning of Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.? defined & explained in the simplest way possible. Besides giving the explanation of

Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.?, a detailed solution for Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.? has been provided alongside types of Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.? theory, EduRev gives you an

ample number of questions to practice Why is the equality between marginal cost and marginal revenue necessary for the firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain with diagram and schedule.? tests, examples and also practice Class 12 tests.

|

|

Explore Courses for Class 12 exam

|

|

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup