5. Monetary Policy of India, Indian Economy, Civil Services Exam | RAS RPSC Prelims Preparation - Notes, Study Material & Tests - RPSC RAS (Rajasthan) PDF Download

Monetary Policy of India:

Topics

- MP background

- Evolution of monetary policy in India: Different phases

- Transmission Mechanism

- Goals of MP

- Instruments of MP

- Determinants of MP

- Role of RBI: Pre and post-reforms

- MP: pre and post reforms

- Committees on Monetary Management in India

- MP and Money Market

- MP and Fiscal Policy

- MP and the external sector

- MP and the banking sector

- MP and Economic growth

- MP and Inflation

- Financial Stability: New Challenge

- Challenges before monetary policy

- Criticisms of India’s MP

Some background information

- An important factor that determines the effectiveness of MP is its transmission – a process through which changes in the policy achieve the objectives of controlling inflation and achieving growth

- MP transmission mechanism describes how MP action affects output and inflation, the final objectives of MP

- Various MP transmission channels

- Quantum Channel relating to money supply and credit

- Interest Rate Channel –this has become important in the post reform period

- Exchange Rate Channel

- Asset Price Channel

- How these channels function in an economy depends on its stage of development and its underlying financial structure.

- These channels, however, are not mutually exclusive. There could be considerable feedback and interaction among them.

Evolution of MP

- 1935: Proportional Reserve System

- 1954: Minimum Reserve System

- 1973-76: Minimum and maximum lending rates for bank loans prescribed

- 1985: Flexible monetary targeting with feedback

- 1998: Multiple indicator approach adopted

Divide MP into phases and study

Functions of RBI

- Monetary functions

- Conduct of monetary policy

- Bank of issue

- Banker to the government

- Banker’s Bank and Lender of the Last Resort

- Controller of credit

- Custodian of foreign exchange reserves

- Foreign exchange management – current and capital account management

- Oversight of the payment and settlement systems

- Non-monetary functions

- Regulation and supervision of the banking and non-banking financial institutions, including credit information companies

- Regulation of money, forex and government securities markets as also certain financial derivatives

- Promotional functions: promotion of IFCI, SFC etc

- Developmental role

- Research and statistics

Objective of MP

- To catalyse economic growth: by ensuring adequate flow of credit to productive sectors

- Price stability

- After the financial crisis, achieving Financial Stability has emerged as an important objective. Exchange rate management can be yet another objective

Tools of MP

- General Credit Control (Quantitative Control)

- Bank Rate

- Open Market Operations

- Cash Reserve Ratio

- Specific and direct credit control (Qualitative Control)

- Lending margins

- Purpose specific credit ceiling

- Discriminatory interest rates

- Eg: Credit Authorisation Scheme, Credit Monitoring Arrangement.

MP pre-reforms

- MP in India was conducted under the monetary targeting framework till 1997-98 with M3 as an intermediate target. This amounted to regulating money supply consistent with the expected growth in real income and a projected level of inflation.

- During the monetary targeting phase (1985-1998), while M3 growth provided the nominal anchor, reserve money was used as the operating target and cash reserve ratio (CRR) was used as the principal operating instrument. Besides CRR, in the pre-reform period prior to 1991, given the command and control nature of the economy, the Reserve Bank had to resort to direct instruments like interest rate regulations and selective credit control. These instruments were used intermittently to neutralize the expansionary impact of large fiscal deficits which were partly monetised. The administered interest rate regime kept the yield rate of the government securities artificially low. The demand for them was created through periodic hikes in the Statutory Liquidity Ratio (SLR) for banks. The task before the Reserve Bank was, therefore, to develop the financial markets to prepare the ground for indirect operations.

MP post-reform

- In the wake of the financial reforms, questions were raised about the appropriateness of this framework.

- Working Group on Money Supply (1998)

- Highlighted that the interest rate channel of transmission mechanism was gaining importance

- On the recommendation of this working group, RBI shifted over to a multiple-indicator approach from 1998-9

- Multiple Indicator Approach: Interest rates or rates of return in different markets (money, capital and g-sec), along with such data as on currency, credit extended by banks and financial institutions, fiscal position, trade, capital flows, inflation rate, exchange rate, refinancing and transactions in foreign exchange available on high-frequency basis, are juxtaposed with output data for drawing policy perspectives.

- LAF: Another important feature post reform is the increased use of LAF. It has enabled RBI to modulate short-term liquidity under varied financial market conditions, including large capital inflows from abroad.

- CRR: Reduced

- 1992-93: market borrowing programme of the government was put through the auction process

- SLR was brought down to its statutory minimum of 25 pc by Oct 1997 and 24 pc in 2010

- CRR was brought down from 15 pc of NDTL of banks to 9.5 pc in Nov 1997 which has stabilised at 6 pc for a long time. Not bound by its statutory limit (lower) of 3 pc now.

- Narsimhan Committee (1998) recommended reforms in the money market

- RBI introduced LAF in 2000 to manage market liquidity on a daily basis and also to transmit interest rate signals to the market. In the post-reform period, LAF, with OMO, has emerged as the dominant instrument of MP, though CRR continued to be used as an additional instrument of policy.

- Call money market was transformed into a pure inter-bank market by 2005.

- With the introduction of prudential limits on borrowing and lending by banks in the call money market, the collateralized money market segments developed rapidly

- To absorb the capital inflows in excess of the absorptive capacity of the economy MSS was introduced in 2004. Interestingly, in the face of reversal of capital flows during the recent crisis, unwinding of the sterilised liquidity under the MSS helped to ease liquidity conditions.

- Increased Micro-finance: To strengthen rural finance RBI has focused on SHGs.

- Fiscal Monetary Separation: Automatic monetization of deficit faced out since 1994. Thus it has separated the monetary policy from the fiscal policy.

- Changed interest rate structure: Phased deregulation of lending rates in the credit market. Minimum lending rates had been abolished and lending rates above Rs. 2 lakh were freed. In 2010, the base rate mechanism was adopted. Savings rate was deregulated in 2011

- Higher market orientation for banking: the banking sector got more autonomy and operational flexibility.

Challenges in the post-reform period

- A major challenge is the conduct of monetary policy in surplus liquidity conditions.

- Increased capital inflows

- To deal with this, RBI initiated the Market Stabilization Scheme (MSS) in 2004

- Under the scheme RBI issues Treasury Bills and dated government securities. The money generated from sale of these bills is kept in a different account held by the government and maintained and operated by RBI. This money is not available for government’s expenditure. Thus, liquidity in the market is mopped.

- The operationalization of the MSS to absorb liquidity of more enduring nature has considerably reduced the burden of sterilization on the LAF window.

- Financial stability is an emerging concern

- The ongoing modernisation of the payments system with the introduction of RTGS would have a significant impact on MP.

- The transmission of policy signals to banks’ lending rates has been rather slow. <base rate system introduced to correct this?>

- Central bank independence

Criticisms/Limitations

- In case of high fiscal deficit, monetary expansion has continued to happen

- Limited coverage: The MP covers only commercial banking system and leaves out the non-bank institutions. This limits the effectiveness of MP

- Unorganised money market: It’s pretty large and does not come under the control of the RBI. Hence, MP does not affect them.

- Predominance of cash transaction (?):<check out the current situation> In India, still there is huge dominance of cash in total money supply. It is one of the main obstacles in the effective implementation of MP. Because MP operates on the bank credit rather than cash.

- Increase volatility: As MP has adopted changes in accordance to the changes in the external sector as well, it could lead to a high amount of volatility.

Evaluation of the changes in MP and Money Market

- In response to the reforms, over the years the turnover in various market segments increased significantly

- The reforms have also led to improvement in liquidity management operations by the RBI as is evident from the stability in call money rates, which also helped improve integration of various money market segments and thereby effective transmission of policy signals

- The rule based fiscal policy pursued under the FRBM Act, by easing fiscal dominance, contributed to overall improvement in monetary management.

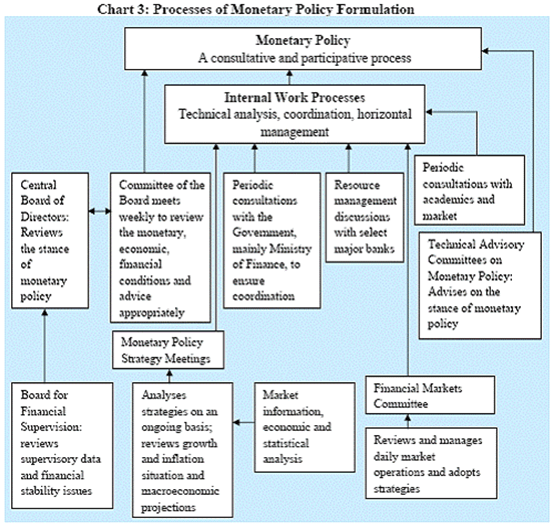

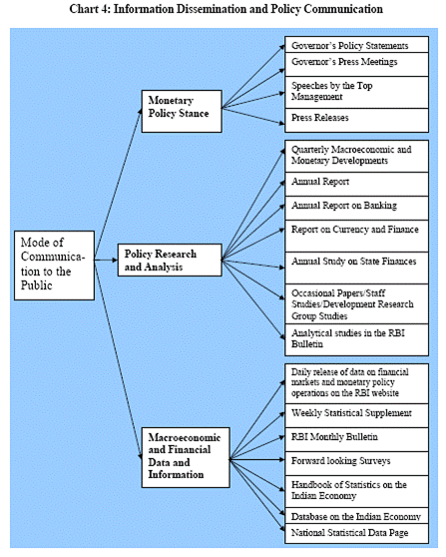

- With the changing framework of monetary policy in India from monetary targeting to an augmented multiple indictors approach, the operating targets and processes have also undergone a change. There has been a shift from quantitative intermediate targets to interest rates, as the development of financial markets enabled transmission of policy signals through the interest rate channel. At the same time, availability of multiple instruments such as CRR, OMO including LAF and MSS has provided necessary flexibility to monetary operations. While monetary policy formulation is a technical process, it has become more consultative and participative with the involvement of market participant, academics and experts. The internal process has also been re-engineered with more technical analysis and market orientation. In order to enhance transparency in communication the focus has been on dissemination of information and analysis to the public through the Governor’s monetary policy statements and also through regular sharing of policy research and macroeconomic and financial information.

- The availability of multiple instruments and their flexible use in the implementation of monetary policy have enabled the RBI to successfully influence the liquidity and interest rate conditions in the economy.

Changes in MP

|

|

Pre-reform |

Post-reform |

|

Operating Target |

Reserve Money was used as the operating target in the monetary targeting framework until mid-1990s |

Multiple Indicator Approach |

|

Monetary Policy Instruments |

CRR and SLR was heavily used |

Reliance on direct instruments has been reduced and liquidity management in the system is carried out through OMOs in the form of outright purchases of g-secs and daily repo and reverse repo operations under LAF. MSS also introduced. |

|

|

|

Large capital inflows witnessed in recent years have posed a major challenge in the conduct of monetary and exchange rate management. |

|

|

|

Phased deregulation of the interest rates |

|

|

High SLR and CRR |

Low SLR and CRR |

|

|

|

|

Money Market

- RBI operationalizes its monetary policy through its operations in government securities, foreign exchange and money markets

- 1985: Money Market reforms begin

- 1992: Introduction of auction system for government securities

- 1996: Primary Dealer System initiated

- 2002: Electronic trading and guaranteed settlement through CCIL for G-Sec starts

- 2006: RBI expressly empowered to regulate money, forex, G-sec and gold related securities markets

Role of RBI

|

Pre-reform |

Post-reform |

|

|

Developmental Role: the developmental role has increased in view of the changing structure of the economy with a focus on SMEs and financial inclusion |

Priority Sector Lending: Introduced from 1974 with public sector banks. Extended to all commercial banks by 1992 |

In the revised guidelines for PSL the thrust is on ensuring adequate flow of bank credit to those sectors that impact large segments of the population and weaker sections, and to the sectors which are employment intensive such as agriculture and small enterprises |

|

Lead Bank Scheme |

Special Agricultural Credit Plan introduced. |

|

|

Kisan Credit Card scheme (1998-99) |

||

|

Focus on credit flow to micro, small and medium enterprises development |

||

|

Financial Inclusion |

||

|

Monetary Policy: the role of RBI has changed from regulating credit and money flow directly to using market mechanisms for achieving policy targets. MP framework has changed to promote financial deregulations and market development. Role as a facilitator rather than as principal actor. |

M3 as an intermediary target |

Multiple Indicator Approach |

|

Regulation of foreign exchange |

Management of foreign exchange |

|

|

Direct credit control |

Open Market Operations, MSS, LAF |

|

|

Rupee convertability highly managed |

Full current ac convertability and some capital account convertability |

|

|

Banker to the government |

Monetary policy was linked to the fiscal policy due to automatic monetisation of the deficit |

Delinking of monetary policy from the fiscal policy. From 2006, under FRBM, RBI ceased to participate in the primary market auctions of the central government’s securities. |

|

As regulator of financial sector: As regulator of the financial sector, RBI has faced the challenge of regulating the increasing financial sector in India. Credit flows have increased. RBI had to make sure that financial institutions are regulated in a way to protect the consumers while not impeding economic growth. |

Reduction in SLR |

|

|

Custodian of FOREX reserves |

Forex reserves have increased drastically. Need to manage it adequately and avoid inflationary impact |

|

|

Inflation |

Direct instruments were used |

Multiple indicators |

|

Financial Stability |

Closed economy |

Increased FDI and FII has made financial stability one of the policy objectives. |

|

Money Market |

Narsimhan Committee (1998) recommended reforms in the money market

|

The term Sustainable growth became prominent after the World Conservation Strategy Presented in 1980 by the International Union for the Conservation of Nature and Natural Resources. BrundlandReport (1987) define sustainable development as the process which seek to meet the needs and aspirations of the present generation without compromising the ability of the future generation to meet their own demands.

Natural resources are limited and thus sustainable development promotes their judicious use and put emphasis on conservation and protection of environment.Global warming and Climate change has brought the issue of Sustainable development in prominence.

Inclusive Growth is economic growth that creates opportunity for all segments of the population and distributes the dividends of increased prosperity, both in monetary and non-monetary terms, fairly across society.Indian Plans after the independence were based on the downward infiltration theory, which failed to bring equitable growth to all the sections of the Indian society.

Approach paper of 11th five year plan talked about “Inclusive and more faster growth” through bridging divides by including those in growth process who were excluded. Divide between above and Below Poverty Line, between those with productive jobs and those who are unemployed or grossly unemployed is at alarming stage.

Liberalization and Privatization after 1990’s have brought the nation out of the Hindu growth rate syndrome but the share of growth has not been equitably distributed amongst different sections of Indian Society.

Various dimensions of Inclusive growth are:-

- economic

- social

- financial

- environmental

Important issues that are needed to be addressed to achieve the inclusive growth are:-

- Poverty

- Unemployment

- Rural Infrastructure

- Financial Inclusion

- Balanced regional development

- Gender equality

- Human Resource Development (Health, Education, Skill Development)

- Basic Human Resources like sanitation, drinking water, housing etc.

Government has launched several programs and policies for Inclusive growth such as:-

- MNREGA

- Jan DhanYojna

- Atal Pension Yojna

- Skill India Mission

- DeenDayalUpadhyaya Gram JyotiYojana

- Pradhan MantriSurakshaBimaYojana

- Pradhan MantriJeevanJyotiBimaYojana

- SukanyaSamridhiYojana

- Pradhan Mantri GaribKalyanYojana

- Jan AushadhiYojana (JAY)

- NaiManzil Scheme for minority students

The Pradhan MantriAwasYojana (PMAY) or Housing for all by 2022

FAQs on 5. Monetary Policy of India, Indian Economy, Civil Services Exam - RAS RPSC Prelims Preparation - Notes, Study Material & Tests - RPSC RAS (Rajasthan)

| 1. What is monetary policy and how does it impact the Indian economy? |  |

| 2. What are the tools used by the Reserve Bank of India to implement monetary policy? | |

| 3. What is the current monetary policy stance of the Reserve Bank of India? | |

| 4. How does monetary policy affect inflation in India? | |

| 5. How does the Reserve Bank of India's monetary policy impact the exchange rate of the Indian rupee? | |

|

4.69/5 Rating |

|

Dec 19, 2024 Last updated |

|

109 docs|21 tests

|

|

Explore Courses for RPSC RAS (Rajasthan) exam

|

|

shortcuts and tricks

,Indian Economy

,Civil Services Exam | RAS RPSC Prelims Preparation - Notes

,Indian Economy

,Exam

,Sample Paper

,Free

,Study Material & Tests - RPSC RAS (Rajasthan)

,Civil Services Exam | RAS RPSC Prelims Preparation - Notes

,Study Material & Tests - RPSC RAS (Rajasthan)

,practice quizzes

,past year papers

,Important questions

,Extra Questions

,Study Material & Tests - RPSC RAS (Rajasthan)

,MCQs

,Summary

,ppt

,Previous Year Questions with Solutions

,5. Monetary Policy of India

,mock tests for examination

,Indian Economy

,5. Monetary Policy of India

,study material

,Semester Notes

,Viva Questions

,Objective type Questions

,Civil Services Exam | RAS RPSC Prelims Preparation - Notes

,video lectures

,5. Monetary Policy of India

,

5. Monetary Policy of India, Indian Economy, Civil Services Exam Free PDF Download

Importance of 5. Monetary Policy of India, Indian Economy, Civil Services Exam

5. Monetary Policy of India, Indian Economy, Civil Services Exam Notes

5. Monetary Policy of India, Indian Economy, Civil Services Exam RPSC RAS (Rajasthan) Questions

Study 5. Monetary Policy of India, Indian Economy, Civil Services Exam on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|