Accounting for Partnership Firms-Fundamentals (Part - 4) | Accountancy Class 12 - Commerce PDF Download

Page No 2.83:

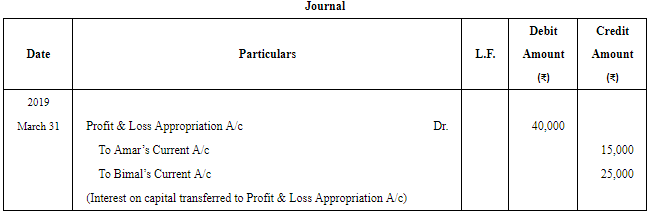

Question 16: Amar and Bimal entered into partnership on 1st April, 2018 contributing ₹ 1,50,000 and ₹ 2,50,000 respectively towards capital. The Partnership Deed provided for interest on capital @ 10% p.a. It also provided that Capital Accounts shall be maintained following Fixed Capital Accounts method. The firm earned net profit of ₹ 1,00,000 for the year ended 31st March 2019.

Pass the Journal entry for interest on capital.

ANSWER:

Working Notes:

WN1: Calculation of Interest on Capital:

Page No 2.83:

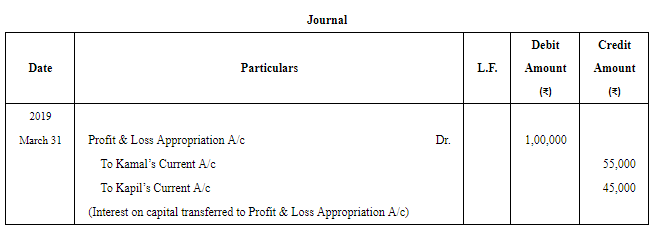

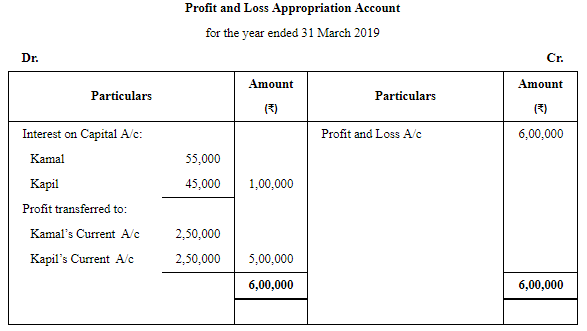

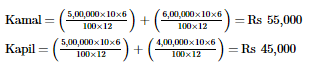

Question 17: Kamal and Kapil are partners having fixed capitals of ₹ 5,00,000 each as on 31st March, 2018. Kamal introduced further capital of ₹ 1,00,000 on 1st October, 2018 whereas Kapil withdrew ₹ 1,00,000 on 1st October, 2018 out of capital.

Interest on capital is to be allowed @ 10% p.a.

The firm earned net profit of ₹ 6,00,000 for the year ended 31st March 2019.

Pass the Journal entry for interest on capital and prepare Profit and Loss Appropriation Account.

ANSWER:

Working Notes:

WN1: Calculation of Interest on Capital:

Page No 2.83:

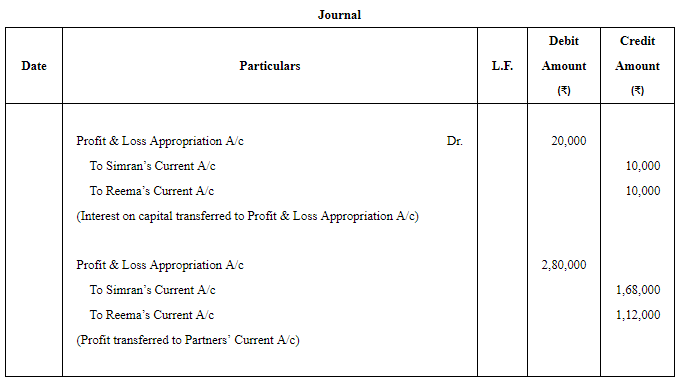

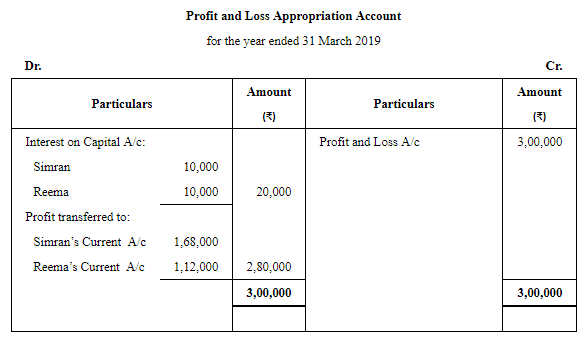

Question 18: Simran and Reema are partners sharing profits in the ratio of 3 : 2. Their capitals as on 31st March, 2018 were ₹ 2,00,000 each whereas Current Accounts had balances of ₹ 50,000 and ₹ 25,000 respectively interest is to be allowed @ 5% p.a. on balances in Capital Accounts. The firm earned net profit of ₹ 3,00,000 for the year ended 31st March 2019.

Pass the Journal entries for interest on capital and distribution of profit. Also prepare Profit and Loss Appropriation Account for the year.

ANSWER:

Working Notes:

WN1: Calculation of Interest on Capital

Page No 2.83:

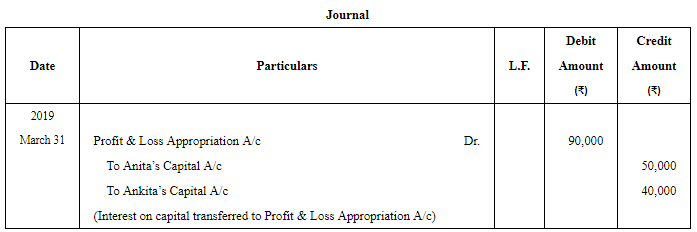

Question 19: Anita and Ankita are partners sharing profits equally. Their capitals, maintained following Fluctuating Capital Accounts Method, as on 31st March, 2018 were ₹ 5,00,000 and ₹ 4,00,000 respectively. Partnership Deed provided to allow interest on capital @ 10% p.a. The firm earned net profit of ₹ 2,00,000 for the year ended 31st March, 2019.

Pass the Journal entry for interest on capital.

ANSWER: Working Notes:

Working Notes:

WN1: Calculation of Interest on Capital

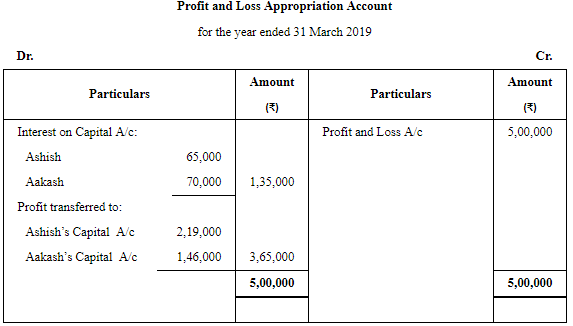

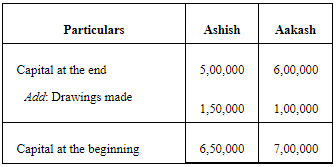

Page No 2.84:

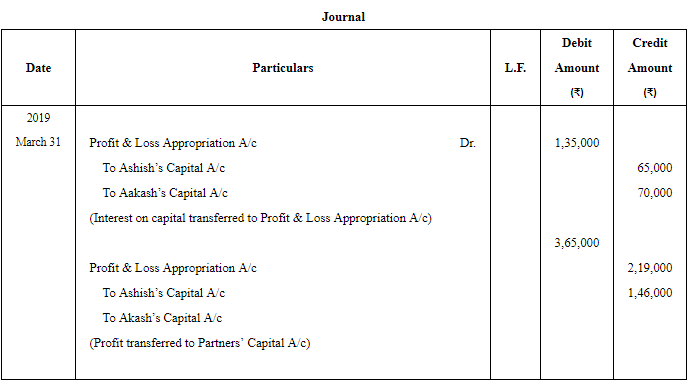

Question 20: Ashish and Aakash are partners sharing profit in the ratio of 3 : 2. Their Capital Accounts showed a credit balance of ₹ 5,00,000 and ₹ 6,00,000 respectively as on 31st March, 2019 after debit of drawings during the year of ₹ 1,50,000 and ₹ 1,00,000 respectively. Net profit for the year ended 31st March, 2019 was ₹ 5,00,000. Interest on capital is to be allowed @ 10% p.a.

Pass the Journal entry for interest on capital and prepare Profit and Loss Appropriation Account.

ANSWER:

Working Notes:

WN1: Calculation of Opening Capital:

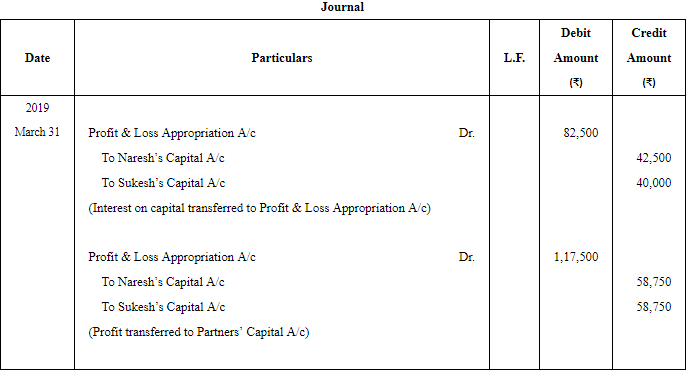

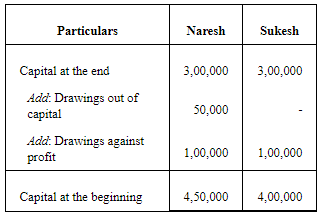

Page No 2.84:

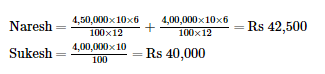

Question 21: Naresh and Sukesh are partners with capitals of ₹ 3,00,000 each as on 31st March, 2019. Naresh had withdrawn ₹ 50,000 against capital on 1st October, 2018 and also ₹ 1,00,000 besides the drawings against capital. Sukesh also had drawings of ₹ 1,00,000.

Interest on capital is to be allowed @ 10% p.a.

Net profit for the year was ₹ 2,00,000, which is yet to be distributed.

Pass the Journal entries for interest on capital and distribution of profit.

ANSWER:

Working Notes:

WN1: Calculation of Opening Capital:

WN2: Calculation of Interest on Capital

Page No 2.84:

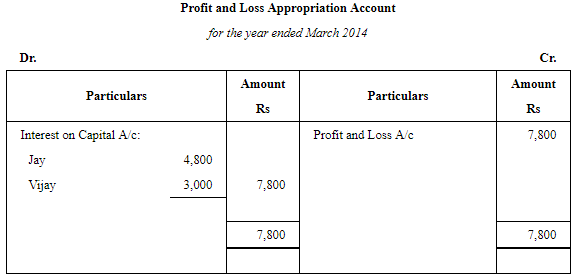

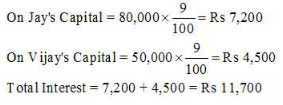

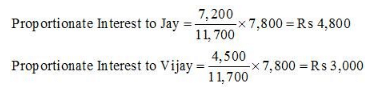

Question 22:On 1st April, 2013, Jay and Vijay entered into partnership for supplying laboratory equipments to government schools situated in remote and backward areas. They contributed capitals of ₹ 80,000 and ₹ 50,000 respectively and agreed to share the profits in the ratio of 3 : 2. The partnership Deed provided that interest on capital shall be allowed at 9% per annum. During the year the firm earned a profit of ₹ 7,800. Showing your calculations cleary, prepare 'Profit and Loss Appropriation Account' of Jay and Vijay for the year ended 31st March, 2014.

ANSWER:

Working Notes:

WN1: Calculation of Interest on Capital

WN2: Calculation of Proportionate Interest on Capital

Note: Interest on capital is to be treated as an appropriation of profits and is to be provided to the extent of available profits i.e. Rs 7,800.

Page No 2.84:

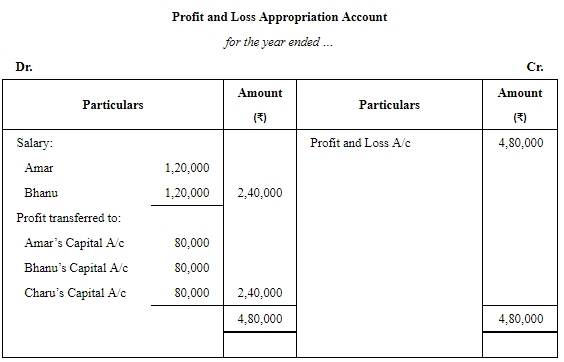

Question 23: Amar, Bhanu, and Charu are partners in a firm. Amar and Bhanu are to get annual salary of ₹ 1,20,000 p.a. each as they are fully involved in the business. Net profit for the year is ₹ 4,80,000. Determine the share of profit to be credited to each partner.

ANSWER:

Page No 2.84:

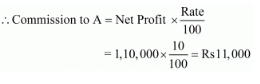

Question 24: A, B and C are partners sharing profits and losses in the ratio of 2 : 2 : 1 respectively. A is entitled to a commission of 10% on the net profit. Net profit for the year is ₹ 1,10,000.

Determine the amount of commission payable to A.

ANSWER:

Net Profit before charging commission = Rs 1,10,000

Commission to A = 10% of on Net Profit before charging such commission

Page No 2.84:

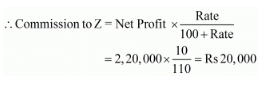

Question 25: X, Y and Z are partners sharing profits and losses equally. As per Partnership Deed, Z is entitled to a commission of 10% on the net profit after charging such commission. The net profit before charging commission is ₹ 2,20,000.

Determine the amount of commission payable to Z.

ANSWER:

Net Profit before charging Commission = Rs 2,20,000

Commission to Z = 10% of on Net Profit after charging such commission

Page No 2.84:

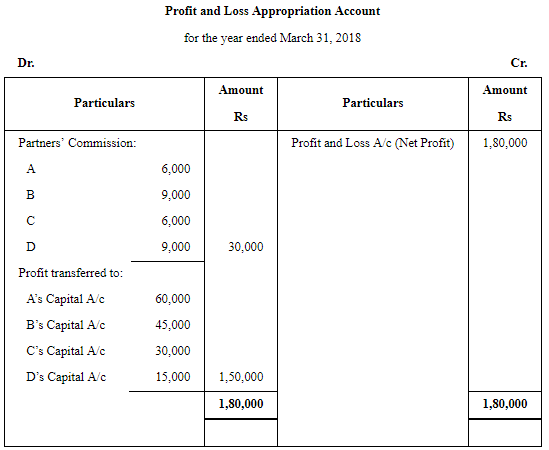

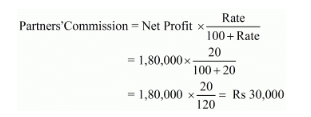

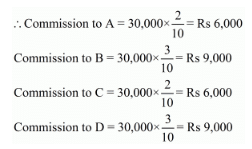

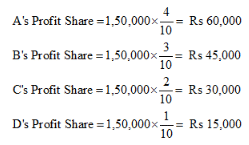

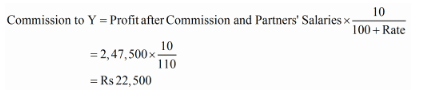

Question 26: A, B, C, and D are partners in a firm sharing profits as 4 : 3 : 2 : 1 respectively. It earned a profit of ₹ 1,80,000 for the year ended 31st March, 2018. As per the Partnership Deed, they are to charge a commission @ 20% of the profit after charging such commission which they will share as 2 : 3 : 2 : 3. You are required to show appropriation of profits among the partners.

ANSWER:

Working Notes:

WN 1 Calculation of Partners’ Commission

Partners’ Commission = 20% on Net Profit after charging such commission

This commission is to be shared by the partners in the ratio of 2 : 3 : 2 : 3

WN 2 Calculation of Profit Share of each Partner

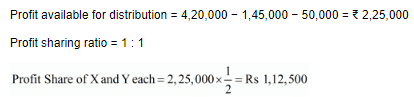

Profit available for Distribution = 1,80,000 − 30,000 = Rs 1,50,000

Profit sharing ratio = 4 : 3 : 2 : 1

Page No 2.85:

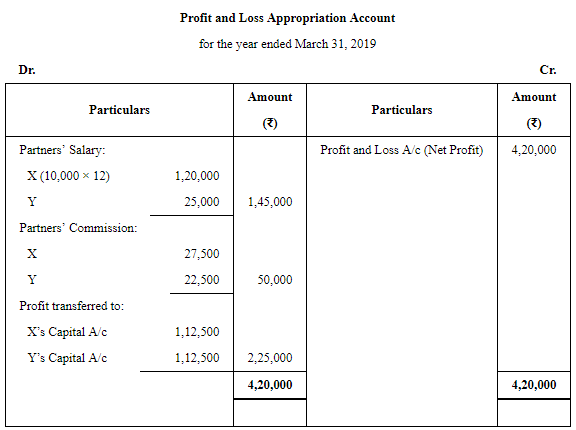

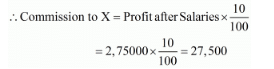

Question 27: X and Y are partners in a firm. X is entitled to a salary of ₹ 10,000 per month and commission of 10% of the net profit after partners' salaries but before charging commission. Y is entitled to a salary of ₹ 25,000 p.a. and commission of 10% of the net profit after charging all commission and partners' salaries. Net profit before providing for partners' salaries and commission for the year ended 31st March, 2019 was ₹ 4,20,000. Show distribution of profit.

ANSWER:

Working Notes:

WN 1 Calculation of Commission

Commission to X = 10% of Net Profit after partners’ salaries but before charging such commission

Profit after Partners’ Salaries = 4,20,000 − 1,45,000 = ₹ 2,75,000

Commission to Y = 10% of Net Profit after charging Commission and Partners’ Salaries

Profit after commission and partners’ salaries = 4,20,000 − 1,45,000 − 27,500 = ₹ 2,47,500

WN 2 Calculation of Profit Share of each Partner

Page No 2.85:

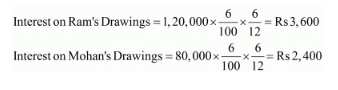

Question 28: Ram and Mohan, two partners, drew for their personal use ₹ 1,20,000 and ₹ 80,000. Interest is chargeable @ 6% p.a. on the drawings. What is the amount of interest chargeable from each partner?

ANSWER: In this question, date of drawings made by the partners is not given. Therefore, interest on drawings is calculated on average basis for a period of six months.

Page No 2.85:

Question 29: Brij and Mohan are partners in a firm. They withdrew ₹ 48,000 and ₹ 36,000 respectively during the year evenly in the middle of every month. According to the partnership agreement, interest on drawings is to be charged @ 10% p.a.

Calculate interest on drawings of the partners using the appropriate formula.

ANSWER:

Since, the drawings are made evenly at the middle of every month, therefore interest on drawings is calculated for a period of six months.

Page No 2.85:

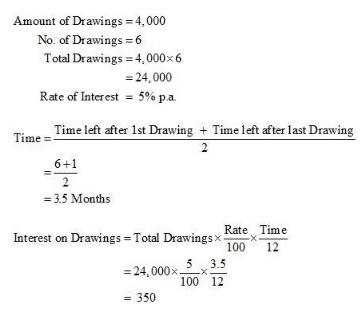

Question 30: A and B are partners sharing profits equally. A drew regularly ₹ 4,000 in the beginning of every month for six months ended 30th September, 2019. Calculate interest on drawings @ 5% p.a. for a period of six months.

ANSWER:

Page No 2.85:

Question 31: One of the partners in a partnership firm has withdrawn ₹ 9,000 at the end of each quarter, throughout the year. Calculate interest on drawings at the rate of 6% per annum.

ANSWER:

Amount of Drawings = ₹ 9,000 per quarter

Annual Drawings= ₹ (9,000 × 4) = ₹ 36,000

Rate of Interest on Drawings = 6% p.a.

Page No 2.85:

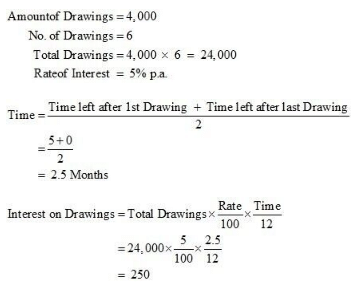

Question 32: A and B are partners sharing profits equally. A drew regularly ₹ 4,000 at the end of every month for six months ended 30th September, 2019. Calculate interest on drawings @ 5% p.a. for a period of six months.

ANSWER:

Page No 2.85:

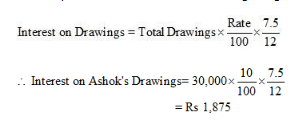

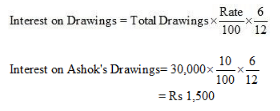

Question 33: Calculate interest on drawings of Ashok @ 10% p.a. for the year ended 31st March, 2019, in each of the following alternative cases:

Case 1. If he withdrew ₹ 7,500 in the beginning of each quarter.

Case 2. If he withdrew ₹ 7,500 at the end of each quarter.

Case 3. If he withdrew ₹ 7,500 during the middle of each quarter.

ANSWER:

Total Drawings = 7,500 × 4 = Rs 30,000

Interest Rate = 10% p.a.

Case (a)

When equal amount is withdrawn in the beginning of each quarter, the interest on drawings is calculated for an average period of 7.5 months

Case (b)

When equal amount is withdrawn at the end of each quarter, the interest on drawings is calculated for an average period of 4.5 months

Case (c)

Page No 2.85:

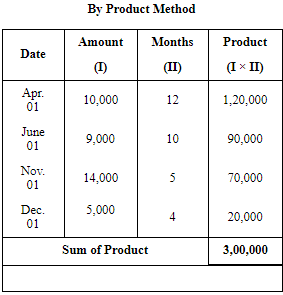

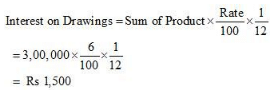

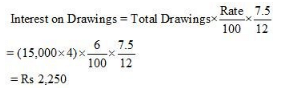

Question 34: Kanika and Gautam are partners doing a dry cleaning business in Lucknow, sharing profits in the ratio 2 : 1 with capitals ₹ 5,00,000 and ₹ 4,00,000 respectively. Kanika withdrew the following amounts during the year to pay the hostel expenses of her son:

Gautam withdrew ₹ 15,000 on the first day of April, July, October and January to pay rent for the accommodation of his family. He also paid ₹ 20,000 per month as rent for the office of partnership which was in a nearby shopping complex.

Calculate interest on drawings @ 6% p.a.

ANSWER:

Interest on Kanika’s Drawings = Rs 1,500

Interest on Gautam’s Drawings = Rs 2,250

Working Notes:

WN1: Calculation of Interest on Kanika’s Drawings

WN2: Calculation of Interest on Gautam’s Drawings

Gautam withdrew Rs 15,000 in the beginning of every quarter.

Page No 2.86:

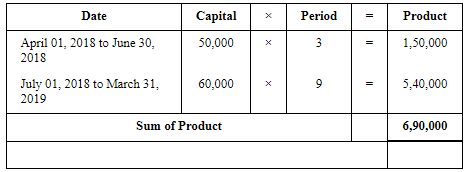

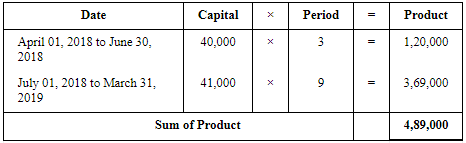

Question 35: A and B are partners sharing Profit and Loss in the ratio 3 : 2 having Capital Account balances of ₹ 50,000 and ₹ 40,000 on 1st April, 2018. On 1st July, 2018, A introduced ₹ 10,000 as his additional capital whereas B introduced only ₹ 1,000. Interest on capital is allowed to partners @ 10% p.a.

Calculate interest on capital for the financial year ended 31st March, 2019.

ANSWER:

Calculation of Interest on A’s Capital

Calculation of Interest on B’s Capital

Page No 2.86:

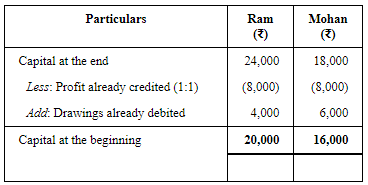

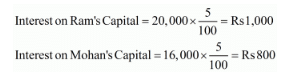

Question 36: Ram and Mohan are partners in a business. Their capitals at the end of the year were ₹ 24,000 and ₹ 18,000 respectively. During the year, Ram's drawings and Mohan's drawings were ₹ 4,000 and ₹ 6,000 respectively. Profit (before charging interest on capital) during the year was ₹ 16,000. Calculate interest on capital @ 5% p.a. for the year ended 31st March, 2019.

ANSWER:

Interest on capital is calculated on the opening balance of partner’s capital.

Calculation of Capital balance at the beginning

Page No 2.86:

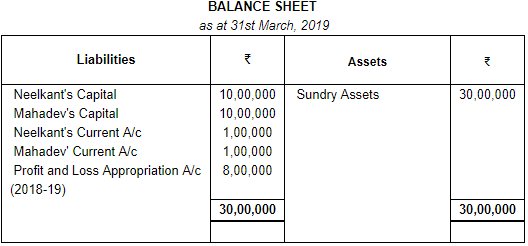

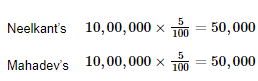

Question 37: Following is the extract of the Balance Sheet of Neelkant and Mahadev as on 31st March, 2019.

During the year, Mahadev's drawings were ₹ 30,000. Profits during the year ended 31st March, 2019 is ₹ 10,00,000. Calculate interest on capital @ 5% p.a. for the year ending 31st March, 2019.

ANSWER:

Interest on Capital

Note: In this question, as the balances of both Partner's Capital Account and of Partner's Current Account are mentioned, so it has been assumed that the capital of the partners is fixed.

As we know, when the capital of the partners is fixed, drawings and interest on capital does not affect the capital balances of the partners. Rather, it would affect their current account balances. Therefore, in this case, capital at the beginning (i.e. opening capital) and capital at the end (i.e. closing capital) of the year would remain same. Thus, the interest on capital is calculated on fixed capital balances (given in the Balance Sheet of the question).

Page No 2.86:

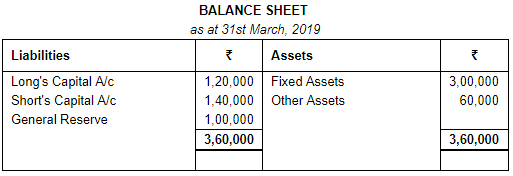

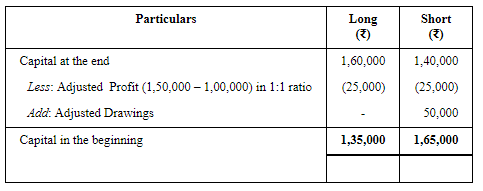

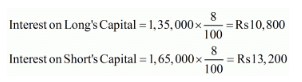

Question 38: From the following Balance Sheet of Long and Short, calculate interest on capital @ 8% p.a. for the year ended 31st March, 2019.

During the year, Long withdrew ₹ 40,000 and Short withdrew ₹ 50,000. Profit for the year was ₹ 1,50,000 out of which ₹ 1,00,000 was transferred to General Reserve.

ANSWER:

Calculation of Capital at the beginning (as on April 01, 2018)

Page No 2.86:

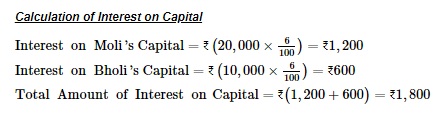

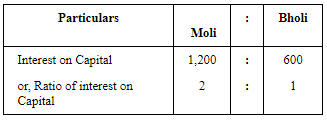

Question 39: Moli and Bholi contribute ₹ 20,000 and ₹ 10,000 respectively towards capital. They decide to allow interest on capital @ 6% p.a. Their respective share of profits is 2 : 3 and the net profit for the year is ₹ 1,500. Show distribution of profits:

(i) where there is no agreement except for interest on capitals; and

(ii) where there is an agreement that the interest on capital as a charge.

ANSWER:

Case (a)

Where there is no clean agreement except for interest on capitals

Profit for the year ended = ₹ 1,500

Total amount of interest = ₹ 1,800

Here, total amount of interest on capital is more than the profit available for distribution. Therefore, profit of Rs 1,500 is distributed between Moli and Bholi in the ratio of their interest on capital.

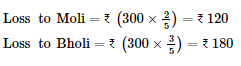

Case (b)

In case, there is a clear agreement that the interest on capital will be allowed even if the firm has incurred loss, then the whole amount of interest on capital is to be allowed to the partners.

Total Profit of the firm = ₹ 1,500

Therefore, loss to the firm amounts to ₹300. This loss is to shared by Moli and Bholi in their profit sharing ratio that is 2 : 3.

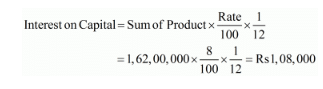

Page No 2.86:

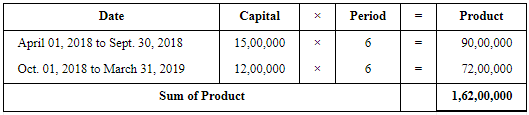

Question 40: Amit and Bramit started business on 1st April, 2018 with capitals of ₹ 15,00,000 and ₹ 9,00,000 respectively. On 1st October, 2018, they decided that their capitals should be ₹ 12,00,000 each. The necessary adjustments in capitals were made by introducing or withdrawing by cheque. Interest on capital is allowed @ 8% p.a. Compute interest on capital for the year ended 31st March, 2019.

ANSWER:

Calculation of Interest on Amit’s Capital

Calculation of Interest on Bramit’s Capital

Page No 2.87:

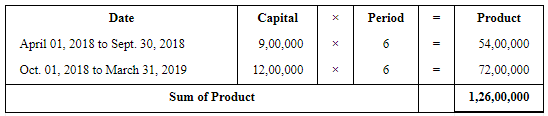

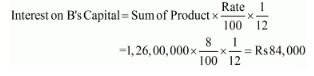

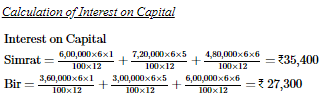

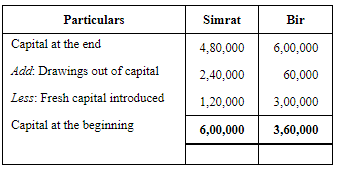

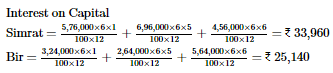

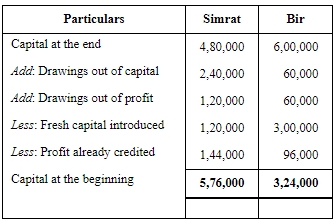

Question 41: Simrat and Bir are partners in a firm sharing profits and losses in the ratio of 3 : 2. On 31st March, 2019 after closing the books of account, their Capital Accounts stood at ₹ 4,80,000 and ₹ 6,00,000 respectively. On 1st May, 2018, Simrat introduced an additional capital of ₹ 1,20,000 and Bir withdrew ₹ 60,000 from his capital.On 1st October, 2018, Simrat withdrew ₹ 2,40,000 from her capital and Bir introduced ₹ 3,00,000. Interest on capital is allowed at 6% p.a. Subsequently, it was noticed that interest on capital @ 6% p.a. had been omitted. Profit for the year ended 31st March, 2019 amounted to ₹ 2,40,000 and the partners' drawings had been: Simrat – ₹ 1,20,000 and Bir – ₹ 60,000. Compute the interest on capital if the capitals are (a) fixed, and (b) fluctuating.

ANSWER:

Case 1: If Capitals are fixed:

Working Notes:

WN1: Calculation of Opening Capital:

Case2: If Capitals are Fluctuating:

Calculation of Interest on Capital

Working Notes:

WN1: Calculation of Opening Capital:

Page No 2.87:

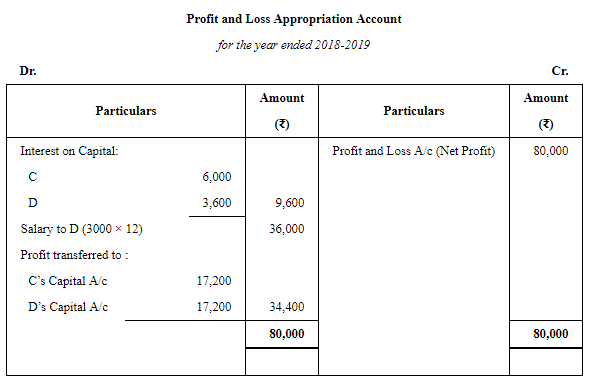

Question 42: C and D are partners in a firm; C has contributed ₹ 1,00,000 and D ₹ 60,000 as capital. Interest in payable @ 6% p.a. and D is entitled to a salary of ₹ 3,000 per month. In the year ended 31st March, 2019, the profit was ₹ 80,000 before interest and salary. Divide the amount between C and D.

ANSWER:

Working Notes:

WN 1 Calculation of Interest on Capital

WN 2 Calculation of Profit Share of each Partner

Profit available for distribution = 80,000 − 9,600 − 36,000 = Rs 34,400

Total amount received by C = Interest on Capital + Profit Share = 6,000 + 17,200 = Rs 23,200

Total amount received by D = Interest on Capital + Salary + Profit Share = 3,600 + 36,000 + 17,200 = Rs 56,800

Page No 2.87:

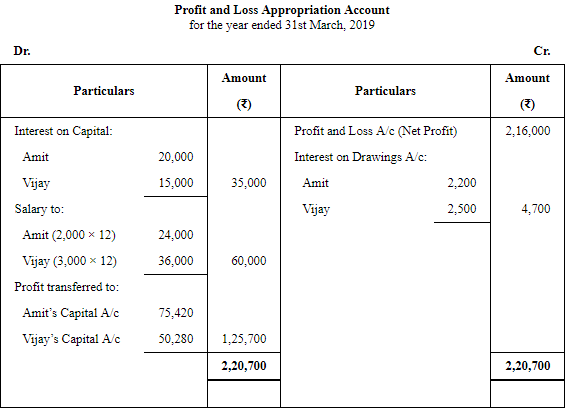

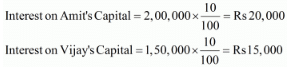

Question 43: Amit and Vijay started a partnership business on 1st April, 2018. Their capital contributions were ₹ 2,00,000 and ₹ 1,50,000 respectively. The Partnership Deed provided as follows:

(a) Interest on capital be allowed @ 10% p.a.

(b) Amit to get a salary of ₹ 2,000 per month and Vijay ₹ 3,000 per month.

(c) Profits are to be shared in the ratio of 3 : 2.

Net profit for the year ended 31st March, 2019 was ₹ 2,16,000. Interest on drawings amounted to ₹ 2,200 for Amit and ₹ 2,500 for Vijay.

Prepare Profit and Loss Appropriation Account.

ANSWER:

Working Notes:

WN 1 Calculation of Interest on Capital

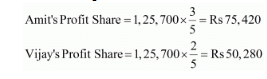

WN 2 Calculation of Profit Share of each Partner

Divisible Profit = 2,16,000 + 4,700 − 35,000 − 60,000 = Rs 1, 25,700

Profit sharing ratio = 3 : 2

Page No 2.87:

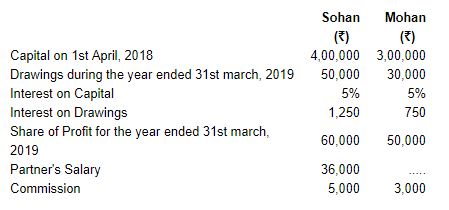

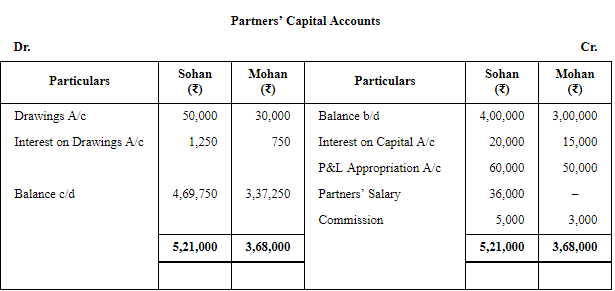

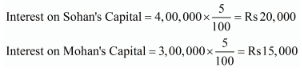

Question 44: Show how the following will be recorded in the Capital Accounts of the Partners Sohan and Mohan when their capitals are fluctuating:

ANSWER:

Working Note:

Calculation of Interest on Capital

Page No 2.87:

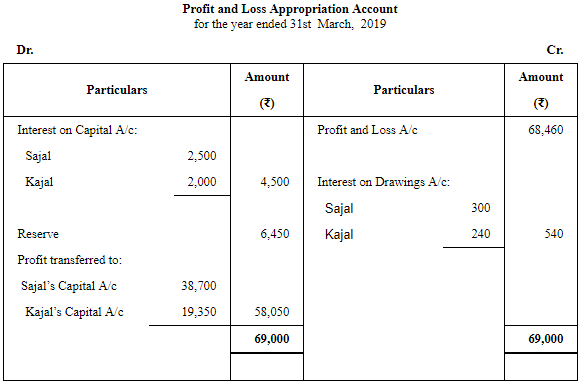

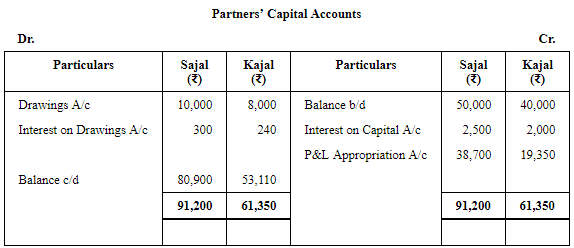

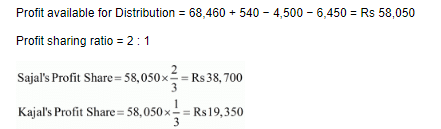

Question 45: Sajal and Kajal are partners sharing profits and losses in the ratio of 2 : 1. On 1st April, 2018 their Capitals were: Sajal – ₹ 50,000 and Kajal – ₹ 40,000.

Prepare Profit and Loss Appropriation Account and the Partners' Capital

Accounts at the end of the year after considering the following items:

(a) Interest on Capital is to be allowed @ 5% p.a.

(b) Interest on the loan advanced by Kajal for the whole year, the amount of loan being ₹ 30,000.

(c) Interest on partners' drawings @ 6% p.a. Drawings: Sajal ₹ 10,000 and Kajal ₹ 8,000.

(d) 10% of the divisible profit is to be transferred to Reserve.

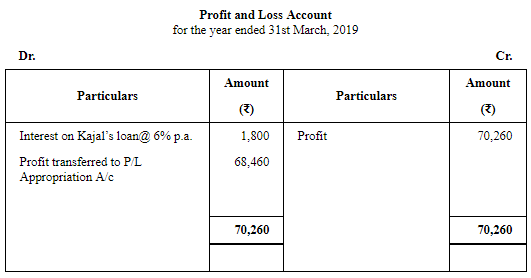

Net profit for the year ended 31st March, 2019 is ₹ 68,460.

Note: Net profit means net profit after debit of interest on loan by the partner.

ANSWER:

Working Notes:

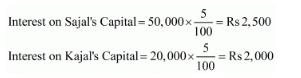

WN 1 Calculation of Interest on Capital

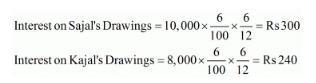

WN 2 Calculation of Interest on Drawings

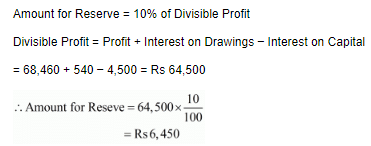

WN 3 Calculation of Amount to be transferred to Reserve

WN 4 Calculation of Profit Share of each Partner

|

42 videos|199 docs|43 tests

|

FAQs on Accounting for Partnership Firms-Fundamentals (Part - 4) - Accountancy Class 12 - Commerce

| 1. What are the fundamentals of accounting for partnership firms? |  |

| 2. How are partnership profits and losses recorded in accounting? | |

| 3. What is the importance of maintaining separate capital accounts for each partner? | |

| 4. What is a partnership balance sheet? | |

| 5. What is a statement of appropriation of profit or loss in partnership accounting? | |

Semester Notes

,Objective type Questions

,Accounting for Partnership Firms-Fundamentals (Part - 4) | Accountancy Class 12 - Commerce

,mock tests for examination

,ppt

,Accounting for Partnership Firms-Fundamentals (Part - 4) | Accountancy Class 12 - Commerce

,Previous Year Questions with Solutions

,Viva Questions

,Sample Paper

,Free

,video lectures

,Accounting for Partnership Firms-Fundamentals (Part - 4) | Accountancy Class 12 - Commerce

,shortcuts and tricks

,Summary

,study material

,past year papers

,MCQs

,Important questions

,practice quizzes

,Exam

,Extra Questions

;

Accounting for Partnership Firms-Fundamentals (Part - 4) Free PDF Download

Importance of Accounting for Partnership Firms-Fundamentals (Part - 4)

Accounting for Partnership Firms-Fundamentals (Part - 4) Notes

Accounting for Partnership Firms-Fundamentals (Part - 4) Commerce Questions

Study Accounting for Partnership Firms-Fundamentals (Part - 4) on the App

|

© EduRev

|

Education Revolution

|

|