Allocation of Overheads and Steps in Implementation of ABC Costing | Crash Course for UGC NET Commerce PDF Download

| Table of contents |

|

| Allocation of Overheads under ABC |

|

| Steps to Develop ABC System |

|

| Characteristics of ABC |

|

| Six Critical Implementation Steps to ABC Costing |

|

| Implementation Steps |

|

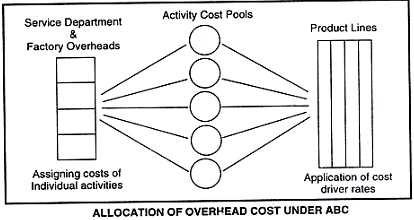

Allocation of Overheads under ABC

The short-term variable costs should be identified to products using volume related cost drivers such as direct labour hour, direct material cost, machine hours etc. Kalpan and Cooper claimed that volume related cost drivers are inappropriate for tracing long-term variable costs to products because they are driven by complexity and variety and not by volume and the key to understanding what causes (drivers) overhead costs in transactions undertaken by support departments costs and factory overheads to product lines under ABC system is shown in the following figure:

Steps to Develop ABC System

The steps required to develop an ABC system are as follows:

- Identify the main activities performed in the organization, such as manufacturing, assembly etc., as well as support activities, including purchasing, packing and dispatching.

- Identify the factors which influence the cost of each activity- the cost drivers.

- Collect accurate data on direct labour, material and overhead costs.

- Establishing the demands made by particular products on activities, using the cost drivers as a measure of demand.

- Trace the cost of activities to products according to a product’s demand for each activity.

Characteristics of ABC

Important characteristics of ABC are noted below:

- Simple traditional distinction made between fixed cost and variable cost is not enough guide to provide quality information to design a cost system.

- The more appropriate distinction between cost behaviour patterns are volume (scale) related, diversity (scope) related, events (decisions) related and time related.

- Cost drivers need to be identified. A cost driver is a structural determinant of cost related activity. The logic behind is that cost drivers dictate the cost behaviour pattern. In tracing overhead cost to product, a cost behaviour pattern must be understood so that appropriate cost driver could be identified.

Six Critical Implementation Steps to ABC Costing

ABC Costing is a supplemental method of cost accounting that provides the decision-making information absent from traditional costing methods. While ABC costing is not limited by business unit boundaries, it can not fully supplant traditional costing methods as it often fails to meet financial reporting requirements for businesses.

ABC Costing focuses on costs contributing to production of a product. It does not attribute other general costs that do not have at least an indirect relationship to the product. While traditional costing systems focus on direct costs and burden a product with other fixed costs, activity based costing increases accuracy of indirect cost assignment.

Implementation Steps

Step 1: Activity Identification

- First, activities must be identified and grouped together in activity pools. Activity pools are the supporting activities that tie in to a product line or service These pools or buckets may include fractionally assigned costs of supporting activities to individual products as appropriate during the second step.

Step 2: Activity Analysis

- ABC continues with activity analysis, clearly identifying the processes which support a product and avoiding some of the systemic inaccuracies of traditional costing. ABC costing requires activity analysis, similar to the process mapping found in lean manufacturing.

- This activity analysis identifies indirect cost relationships and allows assignment of some percentage of that activity to an end product directly.

Step 3: Assignment of Costs

- Based on the findings of step #1 and #2, costs are assigned to an activity pool. For example, human resources costs would be assigned to indirect administrative or indirect management costs. These pools will each have some contribution to object cost.

Step 4: Calculate Activity Rates

- Initial analysis may include direct labor hours, or indirect support labor. These activities must be assigned a value in real currency. All weightings must be added at this step. For instance, production labor hours should be in terms of a weighted labor rate including benefit costs.

Step 5: Assign Costs to Cost Objects

- Once activity costs, pools and rates are identified and clearly defined, the next step is to assign them to cost objects. Objects are generally defined as the results offered to a customer. In both manufacturing and non-manufacturing environments, this product should have some saleable value to compare to the assigned costs.

Step 6: Prepare and Distribute Management Reports

- Once ABC costing analysis is complete, that cost data should be placed in a concise and coherent manner for cost object and process owners. This communication of the costing analysis is critical to justify the cost of the analysis, as often this is not an inconsequential cost.

Conclusion

ABC costing does nothing for the organization if the information is collected but no action follows. The key to the value of this form of costing is that it is actionable. This analysis allows companies to make decisions about product lines, where to direct sales efforts, and to validate the true value provided by capital equipment.

|

237 videos|236 docs|166 tests

|

FAQs on Allocation of Overheads and Steps in Implementation of ABC Costing - Crash Course for UGC NET Commerce

| 1. How can a company allocate overheads using Activity-Based Costing (ABC)? |  |

| 2. What are the steps involved in developing an ABC system? | |

| 3. What are the characteristics of Activity-Based Costing (ABC)? | |

| 4. What are the six critical implementation steps to ABC costing? | |

| 5. How can ABC costing help a company improve cost management and decision-making? | |

Viva Questions

,Free

,Extra Questions

,Sample Paper

,Allocation of Overheads and Steps in Implementation of ABC Costing | Crash Course for UGC NET Commerce

,ppt

,Objective type Questions

,Important questions

,Allocation of Overheads and Steps in Implementation of ABC Costing | Crash Course for UGC NET Commerce

,Exam

,Summary

,practice quizzes

,study material

,shortcuts and tricks

,past year papers

,Semester Notes

,Previous Year Questions with Solutions

,mock tests for examination

,MCQs

,Allocation of Overheads and Steps in Implementation of ABC Costing | Crash Course for UGC NET Commerce

,video lectures

;

Allocation of Overheads and Steps in Implementation of ABC Costing Free PDF Download

Importance of Allocation of Overheads and Steps in Implementation of ABC Costing

Allocation of Overheads and Steps in Implementation of ABC Costing Notes

Allocation of Overheads and Steps in Implementation of ABC Costing UGC NET Questions

Study Allocation of Overheads and Steps in Implementation of ABC Costing on the App

|

© EduRev

|

Education Revolution

|

|