Annuity | Quantitative Aptitude for CA Foundation PDF Download

| Table of contents |

|

| Definition |

|

| Types of Annuities |

|

| Ordinary Annuity Or Annuity Regular |

|

| Annuity immediate/Due |

|

Definition

An annuity is a series of payments, typically uniform in amount, disbursed at regular intervals. Examples include monthly rent, premiums for life insurance policies, deposits into a recurring bank account, consistent monthly payments received by a retired government servant as a pension, and installment payments for loans related to houses or automobiles.

Some terms related with annuities

- Periodic Payment: The individual payment size within an annuity is referred to as the periodic payment of the annuity.

- Annual Rent: The collective sum of all payments made in one year within an annuity is termed its annual rent.

- Payment Period/Interval: The time span between two consecutive payments of an annuity is known as the payment period (or payment interval) of the annuity.

- Term: The overall duration from the commencement of the first payment period to the conclusion of the last payment period is denoted as the term of the annuity.

- Amount of an Annuity: The comprehensive value of all payments at the maturity time of an annuity is defined as the amount (or future value) of the annuity.

- Present Value of an Annuity: The sum of the present values of all payments within an annuity is termed the present value or capital value of the annuity.

Types of Annuities

- Ordinary Annuity: An annuity in which payments are made at the end of the payment interval is referred to as an Ordinary Annuity or Regular Annuity.

- Annuity Due: An annuity in which payments are made at the beginning of the payment interval is known as an Annuity Due or Annuity Immediate.

- Perpetuity: A perpetuity is an annuity characterized by payments that continue indefinitely.

Note: In the upcoming discussion, it is assumed that the payment interval aligns with the interest period, unless stated otherwise.

Ordinary Annuity Or Annuity Regular

Definition: Annuity payments occur at the conclusion of the payment interval.

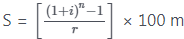

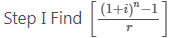

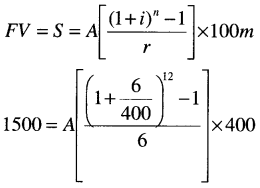

Type I

(TO Find Amount)

Where S = Amount of an Annuity

A = Value of each instalment

r = rate of interest

m = No. of conversion periods in a year

n = m.t = No. of instalments made in t yrs.

= Rate of interest of one conversion Period

= Rate of interest of one conversion Period

Calculator Trick

Step -1 Find (1 + i)n by calculator i.e. Type r ÷ 100 m + 1 Then push × button then push = button (n – 1) times.

Step-II Then – 1

Step – III ÷ r × 100m

Step – IV Then × A push = button (We get the required value of Amount)

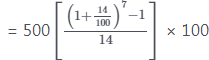

Example 1: Find the future value of an annuity of ₹ 500 is made annually for 7 years at interest rate of 14% compounded annually. [Given that (1.14)7 = 2.5023]

(a) ₹ 5365.25

(b) ₹ 5265.25

(c) ₹ 5465.25

(d) none

Ans: (a)

Calculator Trick = ₹ 5365.25

= ₹ 5365.25 = ₹ 5365.25

= ₹ 5365.25

As Type 14 ÷ 100 + 1 × Push = button 6 times.

Step – II Type – 1 ÷ 14 then × 100 (Because it is annually)

Step – III Then × 500 = (we get the result)

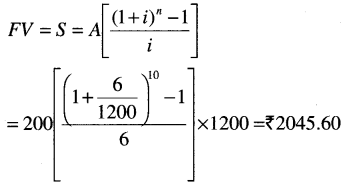

Example 2: ₹ 200 is invested at the end of each month in an account paying interest 6% per year compounded monthly. What is the future value of this annuity after 10th payment? Given that (1,005)10=1.0511

(a) ₹ 2544

(b) ₹ 2144

(c) ₹ 2544

(d) None

Ans: (a)

Here A = 200 ; r = 6% compounded monthly

n = 10 = No. of payments.

Calculator Trick

Step-1 Type 6 ÷ 1200 + 1 Then push × button then push = button 9 times.

Step-II Type – 1 Then ÷ 6 × 1200

Step-III Then Type × 200 = buttons we get the required amount.

Note: If (1 + i)n value is given in the question then use given value in the question otherwise answer may vary.

Type – II

To find the Value of Each Instalment

Example 3: If a bank pays 6% interest compounded quarterly what equal deposit have to be made at the end of the each quarter for 3 years if you want to have ₹ 1500 at the end of 3 years?

(a) ₹ 117.86

(b) ₹ 115.01

(c) ₹ 150.50

(d) None of these

Ans: (b)

A = ₹ 150.01

Calculator Trick

Step-I Type 6 ÷ 400 + 1 Then push × button then push = buttons 11 times

Step-II Then push – 1 ÷ 6 × 400 buttons

Step-III Then push M + button to save the typed value.

Step-IV Then type 1500 then ÷ button then push “MRC” button 2 times then push = button.

[we get the required result]

Type-III

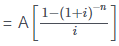

(To find Present Value for Ordinary Annuity)

PV = Present value =

Calculator Trick

Step-I Type (1 + i) value then push= button

Step-II Then push = buttons “n” times

Step-III Push GT button

Step-IV Then type × A (value) then push = button

we get the required result.

Example 4: Find the present value of an annuity which pays 200 at the end of each 3 months for 10 years assuming money to be worth 5% converted quarterly?

(a) ₹ 3473.86

(b) ₹ 3108.60

(c) ₹ 6265.38

(d) None of these

Ans: (c)

Here A = 200 ; m = 4 ; r = 5% 1/4 yrly.

t = 10 years ⇒ n = mt = 4 × 10 = 40 year PV=?

Calculator Trick

Step-I Type 5 + 400 + 1 then push + button

Step-II Then push = buttons 40 times

Step-III Then Push GT button

Step-IV Then typex 200 = buttons [We get the resulting value]

Type-IV

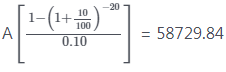

(To find instalment value if PV is given).

Example 5: Mr. A borrows 5,00,000 to buy a house.

If he pays equal instalments for 20 years and 10% interest on outstanding balance what will be the equal annual instalment?

(a) ₹ 58239.84

(b) ₹ 58729.84

(c) ₹ 68729.84

(d) None of these

Ans: (b)

Here PV = ₹ 5,00,000 ; r = 10% yrly.

t = 20 years

n = 20; A = ?

5,00,000 =

Calculator Trick

Step-I Type 10+ 100 + 1 then push + button

Step-II Push = buttons 20 times

Step-III Then Push GT button

Step-IV Then M+ buttons to save the result.

Step-V Type 5,00,000 then push + button then MRC button 2 time and then = button.

(We get the required result)

Annuity immediate/Due

Definition: An annuity due is an annuity the first payment of which is made at the beginning of the first payment interval

Type – V

(T0 find Amount)

Calculator Trick (work as ordinary annuity)

Step-I Type r ÷ 100 m + 1 then pushx button

Step-II Push = buttons n + 1 – 1 = n times then push -1 button then push button then push r value then push × 100m value buttons.

Step-III Push -1 button then × button and then type A value & then push = button (we get the required result)

|

116 videos|164 docs|98 tests

|

FAQs on Annuity - Quantitative Aptitude for CA Foundation

| 1. What is an ordinary annuity or annuity regular? |  |

| 2. What is an annuity immediate? | |

| 3. What is an annuity due? | |

| 4. What is the difference between an ordinary annuity and an annuity due? | |

| 5. How are annuities typically used? | |

|

4.90/5 Rating |

|

Dec 22, 2024 Last updated |

|

116 videos|164 docs|98 tests

|

|

Explore Courses for CA Foundation exam

|

|

Previous Year Questions with Solutions

,mock tests for examination

,Annuity | Quantitative Aptitude for CA Foundation

,Summary

,Objective type Questions

,practice quizzes

,Exam

,Free

,shortcuts and tricks

,video lectures

,MCQs

,past year papers

,Extra Questions

,Annuity | Quantitative Aptitude for CA Foundation

,Important questions

,Semester Notes

,Annuity | Quantitative Aptitude for CA Foundation

,Sample Paper

,study material

,ppt

,Viva Questions

;

Annuity Free PDF Download

Importance of Annuity

Annuity Notes

Annuity CA Foundation Questions

Study Annuity on the App

|

© EduRev

|

Education Revolution

|

|