Basic Issues in Start - Up - Start up issues, Entrepreneurship & Small Businesses | Entrepreneurship & Small Businesses - B Com PDF Download

Mobilizing Resources

The term “resource mobilization” is used routinely these days, but what does it really mean, and how does it relate to an organization’s sustainability?

What is resource mobilization?

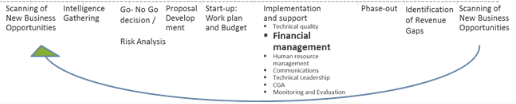

Resource mobilization refers to all activities involved in securing new and additional resources for your organization. It also involves making better use of, and maximizing, existing resources. Resource mobilization is often referred to as ‘New Business Development’. The figure below shows how New Business Opportunities – which are intended to mobilize resources – form part of an organization’s overall functioning.

Figure : Resource Mobilization and its Role in an Organization’s Functioning (MSH, 2010)

Why is resource mobilization so important?

Resource mobilization is critical to any organization for the following reasons:

-

Ensures the continuation of your organization’s service provision to clients

-

Supports organizational sustainability

-

Allows for improvement and scale-up of products and services the organization currently provides

-

Organizations, both in the public and private sector, must be in the business of generating new business to stay in business

What is meant by sustainability?

Although sustainability is often identified with having sufficient funds to cover an organization’s activities, it is actually a broader concept. There are three fundamental streams of sustainability: institutional, financial and programmatic. Each is vital to the survival of an organization. Below are the definitions of these three areas of sustainability:

Programmatic sustainability. The organization delivers products and services that respond to clients’ needs and anticipates new areas of need. Its success enables expansion of its client base.

Institutional sustainability. The organization has a strong, yet flexible structure and accountable, transparent governance practices. Its structure and good governance allows it to respond to the shifting priorities of its supporters and to new responsibilities toward its clients, while creating a positive work climate for its staff.

Financial sustainability. The organization draws on various sources of revenue, allowing it to support its ongoing efforts and to undertake new initiatives.

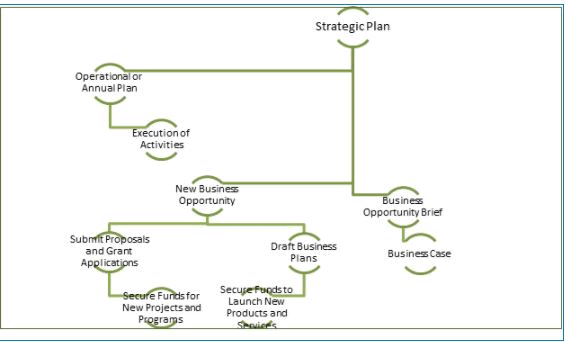

Figure 2 below shows how all of these streams of sustainability are exercised in an organization. The strategic plan is the anchor, in which an organization’s programs, structure and systems, as well as financials are reviewed and new business opportunities are identified. These new directions or new business opportunities are then pursued using a distinct resource mobilization strategy, such as writing proposals, submitting grant applications, or drafting business cases or business plans. All of these instruments are designed to showcase an organization’s programs, institutional structure, and financial health.

Figure 2: The Strategic Plan and Resource Mobilization

In signing off, I would like to share with you 10 truths about resource mobilization:

-

Organizations are not entitled to support; they must earn it.

-

Successful resource mobilization requires a lot of work and takes a lot of time.

-

If your organization needs additional revenue one year from now, start today!

-

Be ready, willing and able to sell your organization and the programs for which you are raising money.

-

Resource mobilization efforts should align with your organizational mission, objectives and strategic plan.

-

Resource mobilization is also about the needs of the (prospective) funder.

-

Understand the needs of your clients (target population/funders).

-

Be prepared to provide evidence-based results.

-

Your organizational performance today impacts your ability to generate resources tomorrow.

-

You must establish and maintain organizational credibility and reputation.

Accommodation and Utilities :

Accommodation and Utilities Required for Start-up: After planning about the resource mobilisation, an entrepreneur needs to have a clear picture of accommodation (space) and utilities of what business must have. Though, it is a tedious and time consuming task, but it essential and deserves high attention. For example, while many start-up mistakes can be rectified later on, a poor choice of location of business and office space is something impossible to repair.

Following points should be considered in selecting the location (accommodation) of business or office space:

- Style of operation (e.g. formal, casual, traditional retail store, kiosk, cart etc.)

- Consider who your customers are and how important their proximity to your location is.

- Monitor foot traffic

- Accessibility of parking

- Is your location/area business friendly?

- Is your area safe for business as well as for customers

- Proximity to other businesses and services

- Building infrastructure

- Utilities and their associated costs

- How close do you need to be your suppliers?

- Can you legally operate your business in this area?

- Possibilities of renovations or change in building (consider legal restrictions)

- Availability of labour, transport, fuel, power, raw material etc.

- Expansion possibilities

- Personal factors

Utilities:

Utilities (water, fuel, electricity etc.) are essential services that play a vital role in successful operation of any enterprises. What utilities your business requires will depend on the nature of business and size of operation. These utilities are required not only for smooth functioning of business, but also for health, safety and to improve efficiency at workplace.

Some common utilities which should be obtained/acquired or hold by the start-up are given below:

- Water

- Sewage

- Trash services

- Telecommunication (i.e. telephone, internet, FAX machine, word processing software etc.)

- Electricity

- Parking

- Canteen

- Furniture

- Toilets (for basic health, welfare, privacy and dignity)

- Conference style speaker phone

- Flipcharts

- LCD projectors

- Catering

- Photocopy

- Video conferencing facilities

- Waiting room/hall/area

- Change room

- Dining hall

- Personal storage

- Washing facilities for personal hygiene

- Lighting and temperature

- Shelter from respite from whether (e.g. heat, cold, rain, wind etc.)

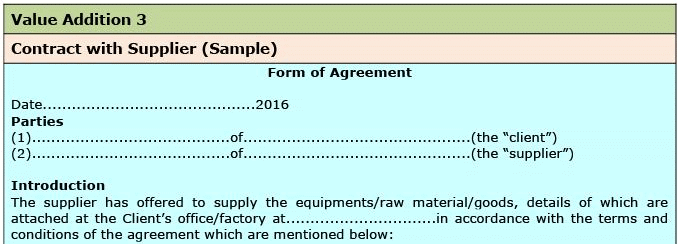

Preliminary Contracts :

For start-up enterprise, entrepreneur needs to sign some kind of contract in writing with various parties/stakeholders e.g. vendors, shareholders, suppliers, financial institutions/lenders/bankers and principal customers. These agreements allow the enterprises to define their legal relationship to the corporation, to each other and the start-up’s other participants. Added to this, written contracts also allow individuals and businesses with a legal document stating the expectations of both parties and how negative situations will be resolved. Contracts also are legally enforceable in a court of law. Contracts often represent a tool that companies use to safeguard their resources. For start up enterprises following points should be considered in the process of forming a contract with various parties i.e. vendor, suppliers, investors, customers or lenders.

1. The parties to the agreement (name of your business and name of the party whether the party is a customer, vendor, suppliers or lender.

2. Mention, how each party is going to be benefited from the agreement. In legal language it is referred as ‘consideration’. Consideration is base of every contract and law enforces only those promises which are made for consideration. Consideration may be related with past, present or future. It must be real, lawful and should be passed at the request of offeror. Consideration may in form of cash, kind or abstinence.

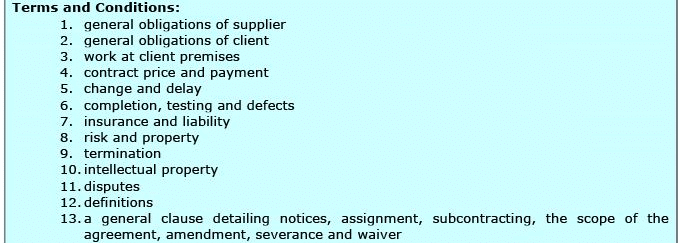

3. Define terms and conditions of contract. It includes what each party is promising to do. For example, in case of agreement with vendor following terms and conditions must be a part of the contract:

-

Bidding

-

Confidentiality agreement

-

Ownership

-

Invoice

-

Reporting

-

Communication

-

Review and acceptance

-

Timelines

-

Insurance verification

-

Attendance at meeting

-

Back-up

4. Additional terms and conditions should be well specified in the contract which generally includes conditions under which either party can terminate the contract, transfer or assign the contract to another company or person, how dispute arising from the contract may be mediated or arbitrated and payment of attorney’s fees if one party breach the contract.

5. Whenever, you need to share organisation’s proprietary information with other party, ask them to sing a non-disclosure agreement. Proprietary information can be anything from your business plan, marketing plan, resource planning, code or financial information as well as client and customer list.

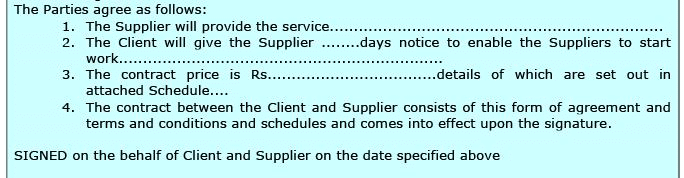

6. The contract shall take effect on the commencement date and shall expire automatically on the date specified in the specification, unless otherwise terminated in accordance with these conditions.

7. Nothing in the contract shall be construed as creating a partnership, a contract of employment or a relationship of principal and agent between the Client and the contractor.

8. Except as otherwise provided in the contract, no notice or communication from one party to the other shall be valid under the contract unless made in writing.

9. Prepare the sample contract and review it and substitute the terms and conditions that fit your project as negotiated with the party.

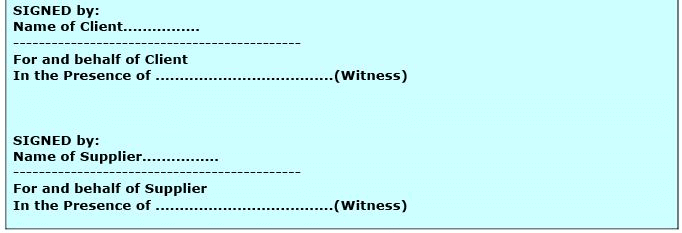

10. Present the final contract to the part for approval and make sure that both the parties sign the contract. Be sure that the person signing has the authority to sign.

11. Make sure that each party has a copy of signed agreement.

12. Have the contract amended and proofed and then sends it to legal department for approval.

Contract Management:

Contract management is a process or a system of managing the contracts made with various parties i.e. supplier, vendors, investors, partners, customers etc. It is also known as contract administration. Contract management not only deals with systematically and efficiently creation of contract but also their execution and analysis for maximum operational and financial performance, and minimising risks. For start-up enterprises contract management is very important because poor contract management can result in loss of sales, penalties and even lawsuits. Contract management is also helpful in minimising the risk arising from contract problem. In start up enterprises, contract problem can arise for a wide variety of reasons.

Some of the important are listed below:

- an issue

- conflict

- disagreements

- breach

- variation

- change

- unexpected events

- miscommunication

- misrepresentation

- failure

- unrealised expectations

To minimise the chance of a minor problem escalating into disputes, the issue need to be identified, discussed and resolved. This can be achieved through an effective contract management system.

Contract Problems of Start-up:

As mentioned above, contract problem may occur due to various reasons. However, the contract problems of start up enterprises are often not so simple. For example, start up owner does not know how to express family and friends that he wishes that they had a contract. Thus, a contract problem could exist for a number of unusual reasons. These could include the situations such as:

- Poor knowledge and understanding about contract formation/management

- Lack of legal advice

- Lack of experience in forming contracts

- The terms and conditions of contract are not clear or are open to misrepresentation.

- a contract, but not having a suitable process in place to support the management of contract.

- Communication problem.

- Not making the clear deal with co-founder or promoters.

- Not coming up with great standard form contract in favour of your enterprise.

- Not complying with securities law when issuing stocks to angels/family and friends.

- Not carefully considering protection of IP assets.

- Ignorance of tax issues

Making a Solid Business Contract: It is worthwhile noting that the contract is enforceable and successful if:

- It is written. Agreement should be in written even if law does not require it. A written agreement is less risky than oral.

- It is simple. Create clear and short sentences with simple, numbered paragraph headings that alert the reader to what is in the paragraph.

- There are no disputes and surprises.

- Identify each party correctly and deal with right person or authorised person.

- The supplier is cooperative and responsive.

- The organisation understands its obligations under the contract.

- Clearly specify terms and conditions and most important payment obligations.

- Specify circumstances under which agreement can be terminated.

- Specify how the disputes will be resolved through mediation, arbitration or through court.

- Each party keep promise that business information will be kept confidential.

- Encourage ongoing and open line of communications between the parties.

- Always seek advice, assistance or clarification when needed.

| Value Addition |

| Standard form of Contract |

|

1. Get sample contracts of what other people do in the industry. There is no need to re-invent a contract. 2. Make sure you have an experienced business lawyer doing the drafting, one that already has good forms to start with. 3. Make sure you make it look like a standard form pre-printed contract with typeface and font size. 4. Don’t make it so ridiculously long that the other side will throw up their hands when they see it. 5. Make sure you have clearly spelled out pricing, when payment is due, and what penalties or interest is owed if payment isn’t made. 6. Try and minimize or negate any representations and warranties about the product or service. 7. Include limitations on your liability if the product or service doesn’t meet expectations. 8. Include a “force majeure” clause relieving you from breach if unforeseen events occur. 9. Include a clause on how disputes will be resolved. Our preference is for confidential binding arbitration in front of one arbitrator. |

Funding Opportunities for Start-ups: No business can take off without monetary support. Finance is needed to fund purchase of land, plant and machinery, equipments, construction of factory, purchasing of technology or know-how, payment of wages, purchasing of raw material and consumables and other manufacturing and administrative expenses. Broadly, the need for finance in any enterprise can be classified into following types:

- Long and medium term financing

- Short term or working capital financing

- Seed capital or marginal money

- Bridge loans and

- Risk financing

Thus, infusion of money is needed in every stage of business and perhaps every activities of business. And that is why it is quite complicated to crack the problem of ‘raising finance’.

| Value Addition |

| Challenges in Raising Seed Capital |

|

At the same time, there are many creative options of financing available for starting a new business that you might not find when buying a car, home or other major consumer item. Basically, three source of financing are available for financing a new business:

1. Equity financing: Equity financing basically refers to the sale of an ownership interest to raise finance for business need. The investors shares in the profits of the business, as well as any deposition of its assets on a pro rata basis based on the percentage of the business owned. Popular equity financing options are:

1. Personal savings

2. Life Insurance policies

3. Home equity loans

4. Friends and relatives

5. Venture capital

6. Angel investors

7. Government grants

8. Equity offering

9. IPOs

10.Warrants

2. Debt financing: Debt financing involves borrowing funds from creditors (secured or unsecured) with the stipulation of repaying the borrowed funds plus interest at a specified future time (short term or long term. Popular debts financing options are:

1. Friends and Relatives

2. Banks and other commercial lenders ( a wide variety of financial institutions including development banks like IDBI, SIDBI, IFCI, IIBI and specialized financial institutions like IVCF, ICICI Venture Capital Funds Ltd., TFCI, etc. offer financial help.

3. Commercial Finance Companies

4. State financial corporation (there are 18 SFCs in the country. Each one offers its own scheme for potential entrepreneurs)

5. Bonds

6. Government Programs: Government of India has launched 10,000 start-up fund in Union Budget 2014-15 to improve the start-up ecosystem in India. Added to this, there are number of policies and programs to support start-up business in India.

Some of the notable are:

- Bank of Ideas and Innovation Programme

- Pradhan Mantri Micro Units Development and Refinance Agency Ltd. (MUDRA)

- Start Up India Action Plan

- The Credit Guarantee Fund Scheme

- Market Development Assistance Scheme for MSMEs

- National Equity Fund Scheme

- Micro Finance Programme

- Equipment Finance Scheme

- Mahila Udyan Nidhi (MUN)

- Single Window Scheme

| Value Addition 6 |

| A Typical Lending Criteria used in Debt Financing |

|

3. Lease financing: A lease is a method of obtaining the use of assets for the business without using debt or equity financing. It is a legal agreement between two parties that specifies the terms and conditions for the rental use of a tangible resource such as a building and equipment. Lease payments are often due annually. The agreement is usually between the company and a leasing or financing organization and not directly between the company and the organization providing the assets. When the lease ends, the asset is returned to the owner, the lease is renewed, or the asset is purchased.

Marketing Plan for Start-up: Most start up enterprises understands and realise the importance of a business plan, which basically outlines enterprise’s course of action to attain its objectives. One crucial element of that plan is marketing plan/strategy. Because the strategy is buried in the larger business plan, many start up owners may not give their time, efforts, research and attention it deserves, assuming that they know their customers and how to reach them. Therefore, marketing aspect of new business venture should be explored and analysed in a broader perspective to exploit market opportunities. At its most basics, marketing plan provides a holistic overview of enterprise’s marketing strategy. It can be defined as a process of determining a clear, compressive approach to the creation of customers (e.g. retaining existing customers as well as generating new customers). The following elements are critical for developing a marketing plan:

Figure : Elements of Marketing Plan

- Brief description of products or services offered by the new business

- Marketing goals and objectives

- Define target market

- Major strength and weakness

- Major opportunities and threats

- Positioning statements

- Market analysis

- Situation analysis

- Market segmentation

- Marketing strategies and tactics (Product, Price, Promotion and Place)

- Outside factors i.e. government policies, economic, technological, cultural and demographics.

- Legal changes i.e. tax rates, standards and governmental rates.

- Marketing budget and control centre

- Metrics and Adjust

|

49 videos|74 docs|22 tests

|

FAQs on Basic Issues in Start - Up - Start up issues, Entrepreneurship & Small Businesses - Entrepreneurship & Small Businesses - B Com

| 1. What are some common challenges faced by start-ups and small businesses? |  |

| 2. What is the importance of entrepreneurship in the growth of start-ups and small businesses? | |

| 3. How can start-ups and small businesses secure funding for their ventures? | |

| 4. What strategies can start-ups and small businesses employ to attract and retain customers? | |

| 5. How can start-ups and small businesses effectively manage their cash flow? | |

video lectures

,Sample Paper

,Free

,Exam

,Previous Year Questions with Solutions

,study material

,Entrepreneurship & Small Businesses | Entrepreneurship & Small Businesses - B Com

,shortcuts and tricks

,Viva Questions

,Semester Notes

,Basic Issues in Start - Up - Start up issues

,Basic Issues in Start - Up - Start up issues

,Objective type Questions

,MCQs

,Basic Issues in Start - Up - Start up issues

,ppt

,past year papers

,Entrepreneurship & Small Businesses | Entrepreneurship & Small Businesses - B Com

,Entrepreneurship & Small Businesses | Entrepreneurship & Small Businesses - B Com

,Extra Questions

,practice quizzes

,mock tests for examination

,Summary

,Important questions

;

Basic Issues in Start - Up - Start up issues, Entrepreneurship & Small Businesses Free PDF Download

Importance of Basic Issues in Start - Up - Start up issues, Entrepreneurship & Small Businesses

Basic Issues in Start - Up - Start up issues, Entrepreneurship & Small Businesses Notes

Basic Issues in Start - Up - Start up issues, Entrepreneurship & Small Businesses B Com Questions

Study Basic Issues in Start - Up - Start up issues, Entrepreneurship & Small Businesses on the App

|

© EduRev

|

Education Revolution

|

|