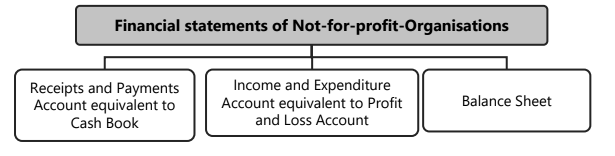

Financial Statements of Not-for-Profit Organizations Chapter Notes | Accounting for CA Foundation PDF Download

Chapter Overview

Introduction

- A non-profit organization is a legal entity that operates for the benefit of society as a whole, rather than for the profit of a sole proprietor, partners, or shareholders. The primary goal of a non-profit organization is to provide services to society or its members.

- The final accounts of non-profit organizations differ from those of profit-making entities. The sources of receipts and payments also vary based on the nature of the activities carried out by the organization.

- Non-profit organizations such as public hospitals, educational institutions, clubs, temples, and churches prepare Receipts and Payments Accounts, Income and Expenditure Accounts, and Balance Sheets as part of their final accounts to show periodic performance (surplus or deficit) and financial position at the end of the period.

- The Income and Expenditure Account for non-profit organizations is similar to the Profit and Loss Account for profit-making organizations, but the terminology differs. Profit is referred to as surplus (excess of income over expenditure) and deficit (excess of expenditure over income).

- Non-profit organizations highlight total cash receipts and payments through the Receipts and Payments Account.

Nature of Receipts and Payments Account

- A Receipts and Payments Account is a summary of the cash book without the date column.

- It is a basic form of accounting commonly used by not-for-profit organizations such as hospitals, clubs, societies, temples, and churches to present their receipts and payments periodically, along with cash balances at the beginning and end of the period.

- Receipts are recorded on the left-hand side, and payments on the right-hand side, just like in the Cash Book.

- The key point to note is that the Receipts and Payments Account is not based on the accrual system of bookkeeping.

- It records all receipts and payments, whether capital or revenue, related to the current, previous, or future periods.

Features of Receipts and Payments Account

- It is a summary of cash and bank transactions, similar to a cash book. All receipts, whether capital or revenue, are debited, and all expenditures, whether capital or revenue, are credited.

- The account starts with opening cash and bank balances and ends with closing balances. It is usually not part of the double-entry system, as it includes all cash and bank receipts and payments, regardless of the period they relate to.

- Surplus or deficit for an accounting period cannot be determined from this account, as it only shows the cash and bank position and excludes non-cash items.

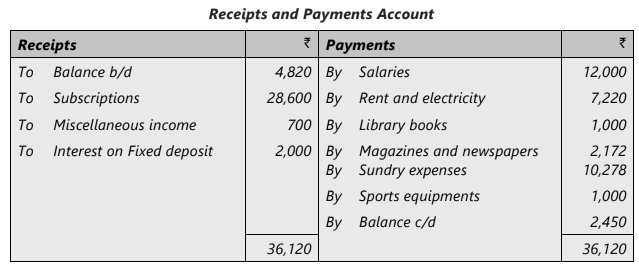

ILLUSTRATION 1

The receipts and payments for the Swaraj Club for the year ended March 31, 2022 were: Entrance fees ₹ 300; Membership Fees ₹ 3,000; Donation for Club Pavilion ₹ 10,000, Foodstuff sales ₹ 1,200; Salaries and Wages ₹ 1,200 Purchase of Foodstuff ₹ 800; Construction of Club Pavilion ₹11,000; General Expenses ₹ 600; Rent and Taxes ₹ 400; Bank Charges ₹ 160.

Cash in hand–April. 1st ₹ 200, March. 31st ₹ 350

Cash in Bank–April. 1st ₹ 400; March. 31st ₹ 590

You are required to prepare Receipts and Payment Account.

SOLUTION

Limitations of Receipts and Payments Account

- Misleading Cash Position: The increase in cash and bank balances shown at the end of the year does not accurately reflect the surplus. This is because it overlooks crucial transactions like the excess cost of pavilion construction over donations received, outstanding subscriptions, and subscriptions collected in advance.

- Inclusion of Irrelevant Items: The Receipts and Payments Account includes items from all periods and of all types, whether capital or revenue. To determine if the organization has a surplus or deficit, an account needs to be constructed that considers only relevant revenue transactions for the current period.

- Inadequate for Complex Organizations: Since the Receipts and Payments Account does not account for important factors, its preparation is not recommended for organizations with complex activities. It is only suitable for simple and modest organizations with no carryover from one period to the next, no assets except cash balance, and no liabilities.

Income and Expenditure Account

The Income and Expenditure Account is similar to the Profit and Loss Account used by profit-making businesses. Nonprofit organizations commonly use this account, which is prepared following the accrual principle. Only revenue items relevant to the current accounting period are included. Preparing this account requires adjustments for outstanding and advance items of income and expenditure. The key difference is in terminology: "profit" is called "surplus" (excess of income over expenditure), while "loss" is termed "deficit" (excess of expenditure over income).Non-profit organizations registered under section 8 of the Companies Act, 2013, must prepare their Income and Expenditure Account and Balance Sheet according to Schedule III of the Act.

Features of Income and Expenditure Account

- Purpose: Prepared to determine the surplus or deficit for the accounting period by matching expenses against revenue.

- Inclusion of Items: Both cash and non-cash items, such as depreciation, are considered. However, capital expenditures and incomes are excluded.

- Timing: Only current year's income and expenses are included.

- Surplus/Deficit: The surplus or deficit is carried forward to the balance sheet, affecting the capital fund.

Surplus and Deficit

Surplus and Deficit are important terms used in the Income and Expenditure Account of non-profit organizations.

- Surplus refers to the situation when the income of the organization exceeds its expenditure during a specific period. This indicates that the organization has made a profit and is in a healthy financial position. Surplus is a positive outcome and reflects the efficiency and effectiveness of the organization in managing its resources.

- Deficit, on the other hand, occurs when the expenditure of the organization surpasses its income within the same period. This indicates a loss and suggests that the organization is facing financial challenges. Deficit is a negative outcome and raises concerns about the sustainability and financial stability of the organization.

In the context of the Income and Expenditure Account, surplus or deficit is calculated by subtracting total expenditure from total income. If the result is positive, it signifies a surplus, while a negative result indicates a deficit.

The surplus or deficit figure is crucial as it is carried forward to the balance sheet and impacts the capital fund of the organization. A surplus is added to the capital fund, enhancing the organization's financial position, while a deficit is deducted, indicating a decline in financial strength.

Main Sources of Income

The sources of income for a not-for-profit organization vary depending on the nature of its activities. Here are some common sources of income for different types of organizations:

- Charitable Hospitals: Income may come from donations, grants, and fees for medical services.

- Sports Clubs: Income can be generated from membership fees, donations, and grants.

- Drama Clubs: Income may be sourced from ticket sales, donations, and grants.

- Educational Societies: Income can come from tuition fees, donations, and grants.

- Library Societies: Income may be generated from membership fees, donations, and grants.

Fund Accounting:

Fund accounting is a method used by non-profit organizations to track and manage funds raised for specific purposes. This system ensures transparency and accountability in the use of donations and grants.

- When a non-profit organization receives a donation or grant for a specific purpose, such as a "Building Fund," the amount is credited to a separate fund account rather than being treated as general income. This allows the organization to monitor how the funds are used for the designated purpose.

- If a fixed asset, like a building, is sold, the capital profit or loss from the sale is recorded in the Income and Expenditure Account. This ensures that the financial statements reflect the true financial position of the organization.

- Fund accounting provides a clear picture of how funds are allocated and spent, helping non-profits demonstrate their commitment to using donations and grants for the intended purposes.

Distinction between Receipts and Payments Account and Income and Expenditure Account

Not-for-profit organizations, such as public hospitals, educational institutions, clubs, temples, and churches, prepare both the Receipts and Payments Account and the Income and Expenditure Account to show their financial performance over a specific period. Here are the key differences between these two accounts:

- Nature of Accounts: The Receipts and Payments Account is a basic account that summarizes cash receipts and payments over a period, while the Income and Expenditure Account is more detailed and resembles a Profit and Loss Account of profit-making organizations.

- Inclusion of Items: The Receipts and Payments Account includes all receipts and payments, whether of revenue or capital nature, and items pertaining to current, previous, or future periods. In contrast, the Income and Expenditure Account only contains items relevant to the current accounting period, excluding capital receipts, prepayments of income, and capital expenditures.

- Opening Balance: The Income and Expenditure Account does not start with any opening balance, whereas the Receipts and Payments Account includes cash balances at the beginning and end of the period.

- Balancing Figure: The balancing figure in the Income and Expenditure Account represents the difference between income and expenditure, indicating surplus or deficit. In the Receipts and Payments Account, the balance at the end of the period reflects the difference between cash received and paid, and is always in debit.

Preparation of Income and Expenditure Account from Receipts and Payments Account

Steps to Prepare Income and Expenditure Account from Receipts and Payments Account:

- Compute Opening Balance: Determine the opening balance of the Accumulated Fund or Capital Fund by preparing an opening balance sheet. This represents the excess of total assets over liabilities at the beginning of the period.

- Open Ledger Accounts: Create ledger accounts for various income and expenditure items where accruals or outstanding amounts need adjustment. Enter accruals or outstanding amounts for the period, as well as amounts related to earlier or future periods. The balance in these accounts will represent the income or expenditure for the period, which should be transferred to the Income and Expenditure Account.

- Post from Receipts & Payments Account: Transfer items of income from the Receipts and Payments Account to the Income and Expenditure Account where accruals and outstanding amounts need adjustment. Post items of expenses without adjustments directly to the Income and Expenditure Account.

- Transfer Balance: Transfer the balance of the Income and Expenditure Account to the Accumulated Fund or Capital Fund Account.

- Post Capital Receipts and Payments: Post capital receipts and payments from the Receipts and Payments Account to the appropriate asset or liability accounts for inclusion in the Balance Sheet. If an asset is sold, any capital profit or loss is credited or debited to the Income and Expenditure Account. The balance of the Income and Expenditure Account is transferred to the Accumulated Fund or Capital Fund Account.

- Prepare Balance Sheet: Create a Balance Sheet including all balances remaining after transfers to the Income and Expenditure Account.

ILLUSTRATION 2

During 2022, subscription received in cash is ₹ 42,000. It includes ₹ 1,600 for 2021 and ₹ 600 for 2023. Also ₹ 3,000 has still to be received for 2022.

Required

Calculate the amount to be credited to Income and Expenditure Account in respect of subscription.

SOLUTION

The various accounts will appear as under:

Subscription outstanding ₹ 3,000 and Subscription received in advance ₹ 600 will be shown in the balance sheet on the assets and liabilities side respectively.

ILLUSTRATION 3

Suppose salaries paid during 2022 were ` 23,000. The following further information is available:

Required

Calculate the amount to be debited to Income and expenditure account in respect of salaries and also show necessary ledger accounts.

SOLUTION

Balance Sheet of a Not-for-Profit Organization

A Balance Sheet provides a snapshot of the assets and liabilities of an accounting unit on a specific date. It is typically prepared at the end of an accounting period, following the preparation of the Income and Expenditure Account. The Balance Sheet is a classified summary of the ledger balances that remain after all revenue items have been closed and transferred to the Income and Expenditure Account.

- In not-for-profit organizations, the difference between total assets and total outside liabilities is referred to as the Capital Fund. This fund represents contributions from members, including legacies, special donations, entrance fees, and accumulated surpluses over the years. If members have not contributed any funds, the balance will be termed as the "Accumulated Fund" instead of the Capital Fund.

- The surplus or deficit from the current year's operations, as indicated by the Income and Expenditure Account, is either added to or deducted from the Capital or Accumulated Fund brought forward from the previous period.

Format of Balance Sheet of a Not-for-Profit Organization

Liabilities

- Capital Fund: Represents the difference between total assets and total outside liabilities, including contributions from members and accumulated surpluses.

- Accumulated Fund: Used when members have not contributed any funds, representing the accumulated surplus or deficit.

- Surplus/Deficit: The surplus or deficit from the current year’s operations, added to or deducted from the Capital or Accumulated Fund.

Assets

- Total Assets: All assets owned by the organization, including property, equipment, and other tangible and intangible assets.

- Current Assets: Any assets that are expected to be converted into cash or used up within one year, such as cash, accounts receivable, and inventory.

Accounting Treatment of Some Special Items

Donations- Donations can be for either revenue or capital expenditure.

- Donations for revenue expenditure are credited directly to the Income and Expenditure Account.

- Donations for capital expenditure are credited based on the donor's intention:

- If specified by the donor, credited to a special fund account.

- If not specified, credited to the Capital Fund Account.

- When investments or assets are purchased from a special fund, they must be disclosed separately.

- Income from such investments or donations for a specific purpose should be credited to an account indicating the purpose.

- Corresponding expenditure should be debited to the same account.

- These expenses should not be charged to the Income and Expenditure Account.

- The term "Fund" is used for amounts collected for a special purpose when these are invested, e.g., Scholarship Fund, Prize Fund etc.

- The term "Account" is used when amounts collected are not invested in securities or assets distinguishable from those belonging to the institution, e.g., Building Account, Tournament Account etc.

- If a donor gives a security or another readily realizable asset instead of cash, the value of the asset must be credited to the fund for which the donation was intended.

Entrance and Admission Fees:

- Entrance and admission fees paid by members upon joining a club or society are typically considered capital receipts and are credited to the Capital Fund.

- This is because these fees do not create any special obligation towards the member, who receives the same privileges as those who have paid only their annual subscription.

- However, if the fee is small, intended to cover admission-related expenses, or if the society's rules allow such fees to be treated as income, they may be included in the Income and Expenditure Account.

- The treatment of these fees depends on the specific requirements of the question.

- If the question does not specify, it is safer to treat the fee as a capital receipt.

Subscription:

- Subscriptions, being a form of income, should be allocated over the period in which they are earned.

- To test candidates' understanding of this accounting principle, examination questions often provide figures for subscriptions collected during the year, as well as those outstanding at the beginning and end of the year.

- If subscriptions have been received in advance, their amounts are also indicated.

- In such cases, it is advisable to set up a Subscription Account to determine the amount of subscriptions pertaining to the period for which accounts are being prepared.

For instance, if a society collected subscriptions amounting to ₹ 1,850 during the year 2022, out of which ` 200 represented subscriptions for the year 2021 and ₹ 100 were subscriptions for the year 2023, it is important to allocate these amounts correctly to reflect the income for the period. Collected in advance for the year 2023, and subscriptions amounting to ₹ 500 were outstanding for recovery at the end of 2022, the adjusting journal entries and the Subscription Account should be set up as follows:

The amount of outstanding subscription is adjusted in the Subscription Account by debit to Outstanding Subscription Account and that balance is shown as an asset in Balance Sheet. The Subscription Account is closed off by transferring its balance at the end of the year to the Income and Expenditure Account.

Life Membership Fee

- Fees collected for life membership are considered a capital receipt because they are non-recurring in nature. These fees are directly added to the capital fund or general fund.

- To adjust the lump sum subscription collected from life members, one of the following methods can be used:

- (1) Special Account Method: The entire amount may be carried forward in a special account until the member passes away. After the member's death, the remaining amount can be transferred to the credit of the Accumulated Fund.

- (2) Annual Transfer Method: An amount equal to the normal annual subscription may be transferred every year to the Income and Expenditure Account, with the balance carried forward until it is exhausted. If the life member dies before the entire amount has been transferred, the remaining balance should be transferred to the Accumulated Fund on the date of death.

- (3) Annual Transfer Based on Age: An amount, calculated based on the age and average life expectancy of the member, may be transferred annually to the credit of the Income and Expenditure Account.

Other Concepts in Not-For-Profit Organizations

Treatment of Important Items

1. Donation:. donation is a gift given in cash or kind from an individual. There are two types of donations:

- (a) Specific Donation: This type of donation is received for a specific purpose, such as building a facility or donating library books. Specific donations should be capitalized and shown on the liabilities side of the balance sheet.

- (b) General Donation:. general donation is not received for any specific purpose and should be shown on the credit side of the Income and Expenditure Account.

2. Entrance Fees: Also known as admission fees, entrance fees should be capitalized and added to the capital fund for all organizations. If the question provides specific treatment for entrance fees, that should be followed.

3. Legacy:. legacy is an amount received by an organization as per the will of a deceased person. It should be capitalized and shown on the liabilities side of the balance sheet by adding it to the Capital Fund.

4. Life Membership Fees: Life membership fees should be capitalized and shown on the liabilities side of the balance sheet. If the question provides specific treatment for life membership fees, that should be followed.

5. Endowment Fund Donation: This type of donation is received with the condition that only the income generated from the donation will be used for a specific purpose. In such cases, the income related to special funds should be added to these funds on the liabilities side of the balance sheet. All expenses related to these funds should be deducted from the fund on the liabilities side of the balance sheet.

6. Treatment of Sale of Old Newspaper and Periodicals: The income received from the sale of old newspapers and periodicals is shown as income on the credit side of the Income and Expenditure Account.

7. Sale of Old Fixed Assets: The sale proceeds of old fixed assets are treated as capital receipts. The profit or loss on the sale of fixed assets is shown in the Income and Expenditure Account.

8. Honorarium: An honorarium is paid to individuals who are not employees of the not-for-profit organization for services rendered.

Preparation of Balance Sheet

- Opening Balance Sheet and Surplus Calculation: If the capital fund or accumulated surplus at the beginning of the year is not provided, it is calculated by deducting liabilities from assets at the beginning of the year. While calculating the opening capital fund, prepaid expenses and accrued incomes should be included as assets, while outstanding expenses and advance incomes should be treated as liabilities. Any surplus earned during the year is added to the opening capital fund, and any deficit is deducted from it.

- Cash and Bank Balance: The closing cash and bank balance, as disclosed in the Receipt and Payment Account, is shown on the assets side of the balance sheet. In case of a bank overdraft, it should be displayed on the liabilities side of the balance sheet.

- Fixed Assets: The opening balances of fixed assets such as furniture, buildings, equipment, etc., are adjusted by adding the amount of purchases, deducting sales, and accounting for depreciation.

- Liabilities: The opening balances of liabilities should be modified to reflect any increases or decreases in the same.

Note: The illustrations presented in this chapter pertain to clubs not registered under the Companies Act, 2013. Therefore, the Income & Expenditure Account and Balance Sheet are prepared in accordance with the applicable guidelines and not as per Schedule III of the Companies Act, 2013.

ILLUSTRATION 4

Following is the Receipts and Payments Account of New bird Forty Club for the year ended 31st March, 2022:

Additional information :

(a) Outstanding subscriptions for the year ended 31st March, 2022 – ₹ 55,000.

(b) Outstanding salaries and wages –₹ 40,000 for the year ended on 31st March 2022.

(c) Depreciate sports equipment by 25% for the year ended on 31st March 2022.

(d) Capitalize 50% of the entrance fees.

Prepare Income and Expenditure Account of the club from the above particulars for the year ended on 31st March 2022.

SOLUTION

ILLUSTRATION 5

From the following information of a club show the amounts of match expenses and match fund in the appropriate Financial Statements of the club for the year ended on 31st March, 2022:

SOLUTION

Note: Since the expenses incurred are more than the Match fund available ₹ 1,05,000 we are limiting the expenses to ₹ 1,05,000. The remaining expenses of ₹ 5000 (1,10,000-1,05,000) will be debited to the Income and expenditure account.

ILLUSTRATION 6

During the year ended 31st March, 2022, the subscriptions received by the Jaipur Literary Society were₹ 4,50,000. These subscriptions include₹ 20,000 received for the year ended 31st March, 2021. On 31st March, 2022, subscriptions due but not received were₹ 15,000. Advance subscription received for the year ending 31st March 2022 but pertaining to year 2023 amounted to ₹ 26,000. The Subscriptions received in advance for the year ending 31st March, 2021 includes ₹ 18,000 pertaining to year 2021-22. Show the subscription account in book of the society?

SOLUTION

ILLUSTRATION 7

From the following information, calculate amount of subscriptions outstanding for the year ended 31st March, 2022.

A club has 350 members each paying an annual subscription of ₹ 1,050. The Receipts and Payments Account for the year showed a sum of ₹ 4,10,000 received as subscriptions. The following additional information is provided:

Subscriptions Outstanding on 31st March, 2021 – ₹ 45,000

Subscriptions Received in Advance on 31st March, 2022 – ₹ 62,000

Subscriptions Received in Advance on 31st March, 2021 – ₹ 30,000

SOLUTION

ILLUSTRATION 8

The following was the Receipts and Payments Account of Exe Club for the year ended March. 31, 2022

You are given the following additional information:

For the year ended March 31, 2022, the honorarium to the Secretary and Treasurer are to be increased by a total of ₹ 200. Prepare the Income and Expenditure Account and Balance Sheet for period ending 31st March, 2022.

SOLUTION

ILLUSTRATION 9

The Sportwriters Club gives the following Receipts and Payments Account for the year ended March 31, 2022:

Figures of other assets and liabilities are furnished as follows:

The closing values of furniture and sports equipments are to be determined after charging depreciation at 10% and 20% p.a. respectively inclusive of the additions, if any, during the year. The Club's library books are revalued at the end of every year and the value at the end of March 31, 2022 was ` 5,250.

Required

From the above information you are required to prepare:

(a) The Club's Balance Sheet as at March 31, 2021;

(b) The Club's Income and Expenditure Account for the year ended March 31, 2022.

(c) The Club's Closing Balance Sheet as at March 31, 2022.

SOLUTION

Working Notes:

ILLUSTRATION 10

The Income and Expenditure Account of the Youth Club for the Year 2022 is as follows:

This account had been prepared after the following adjustments:

Salaries Outstanding at the beginning and the end of 2022 were respectively ₹ 400 and ₹ 450. General Expenses include insurance prepaid to the extent of ₹ 60. Audit fee for 2022 is as yet unpaid. During 2022 audit fee for 2021 was paid amounting to ₹ 200.

The Club owned a freehold ground valued at ₹ 10,000. The club had sports equipment on 1st January, 2022 valued at ₹ 2,600. At the end of the year, after depreciation, this equipment amounted to ₹ 2,700. In 2021, the Club has raised a bank loan of ₹ 2,000. This was outstanding throughout 2022. On 31st December, 2022 cash in hand amounted to ₹ 1,600.

Required

Prepare the Receipts and Payments Account for 2022 and Balance Sheet as at the end of the year.

SOLUTION

ILLUSTRATION 11

Smith Library Society showed the following position on 31st March, 2021:

The receipts and payment account for the year ended on 31st March, 2022 is given below:

You are required to prepare income and expenditure account for the year ended 31st March, 2022 and a balance sheet as at 31s , March, 2022 after making the following adjustments:

Membership subscription included ₹ 10,000 received in advance and 75% of the entrance fees is to be capitalized.

Rent for ₹ 4,000 and salaries for ₹ 3,000 are outstanding.

Books are to be depreciated @ 10% including additions. Electrical fittings and furniture are also to be depreciated at the same rate.

Interest on securities is to be calculated @ 5% p.a. including purchases made on 1.10.2021 for ₹ 40,000.

SOLUTION

Working Notes:

ILLUSTRATION 12

From the following Income and Expenditure Account and the Balance Sheet of a club, prepare its Receipts and Payments Account and Subscription Account for the year ended 31st March, 2022:

The following adjustments have been made in the above accounts:

(1) Upkeep of ground ` 600 and Printing ` 240 relating to 2020-2021 were paid in 2021-22.

(2) One-half of entrance fee has been capitalised by transfer to General Fund.

(3) Subscription outstanding in 2020-21 was ` 800 and for 2021-22 ` 700.

(4) Subscription received in advance in 2020-21 was ` 200 and in 2021-22 for 2022-23 ` 100.

SOLUTION

Note: In order to arrive at the payments under Upkeep of ground and printing, even the payment for 2020-21 has been considered, as receipts and payments A/c shows all the period payments

Educational Institutions

Registration- Most educational institutions in India are registered as Societies under the Indian Societies Registration Act of 1860.

- In some states where Public Trust Acts exist, societies registered under the Indian Act must also register under the Trust Act. For example, in Maharashtra, societies are registered under both the Indian Act and the Bombay Public Trust Act of 1950.

Organizational Pattern

- Trust Societies are autonomous with office bearers including a President, Secretary, Treasurer, and Executive Committee Members.

- The General Body comprises all Society Members. For Societies/Trusts managing multiple colleges and schools, each institution has its own governing body.

- The Governing Body, which includes the Principal or Head of the Unit, oversees the functioning of the individual school or college.

Salient Features

- Educational institutions are expected to cover part of their expenses through funds raised from donations or charities.

- State Governments provide assistance to educational institutions through grant-in-aid codes, but there is no uniformity in this assistance.

- All educational institutions follow the financial year as their accounting year.

Sources of Finance for Running the Educational Institution

Educational institutions typically rely on three main sources for funding:- Donations from the Public

- Fees (including annual tuition fees, term fees, admission fees, laboratory fees, etc.)

- Government Grants

Government Grants

These are further categorized into four types:

- Maintenance Grant

- Equipment Grant

- Building Grant

- Other Grants as sanctioned by the Government from time to time

Specific Items of Funding

1. Donation from Public

- Donations can be for recurring or non-recurring purposes and may be received in cash or kind.

- In-kind donations might include land, buildings, shares, securities, and other assets, often with the intent to honor a distinguished family member.

2. Capitation Fees or Admission Fees

- Collected from parents or guardians seeking admission for their children, usually by the Parent Body running the institution.

- These fees have faced criticism and legal restrictions in recent times.

3. Laboratory and Library Deposit

- Typically collected by schools and colleges and held until the student leaves the institution.

4. Use of Term Fees

- A separate account for receipts and expenditures should be maintained, with surpluses carried over to the next year.

Term fees can be used for various purposes, including:

- Medical Inspection

- School Magazine (manuscript and/or printing)

- Examination expenses (printing question papers and supplying answer books)

- Contributions to athletic and cultural associations related to school activities

- School functions and festivals

- Inter-class and Inter-school tournaments

- Sports and Games (major and minor)

- Newspapers and magazines

- Extra-curricular excursions and visits

- School competitions (e.g., elocution competitions)

- Scouting and Guiding

- School Band

- Social and Cultural activities and associated equipment

- Vocational Guidance

- Prizes for Co-curricular activities

- Maintenance of playgrounds

- Purchase of books for Pupils Library

- Drawing and Craft material

- Audio-Visual Education

- Curricular visits and excursions

- Equipment for Physical Education

5. Recurring Grants

- Recurring grants, such as Maintenance Grants, are received in installments throughout the year.

6. Use of Grant-in-Aid

- The School Code outlines admissible items for grant-in-aid, including:

- Staff salaries and allowances

- Leave Allowance, Bad Climate Allowance, Water Allowance, Leave Salary

- Expenditure on teacher training, Pension and Gratuity, Librarian appointment

- Rent, Taxes, Insurance, and Other Contingencies (printing, stationery, conveyance, etc.)

- Current repairs, Miscellaneous Expenses (e.g., School Garden, Physical Education)

- Prizes, Expenditure on co-operative stores, Registration fee for Board recognition

- Maintenance of Tiffin Rooms, Teacher Bonus, Electrical and Telephone Charges

- Expenditure on Conferences, Subscription to educational Associations, Medical Charges

- Audit fees, Sales-tax and General tax on purchases, Merit scholarships

ILLUSTRATION 13

From the following balances and particulars of Republic College, prepare Income & Expenditure Account for the year ended March, 2022 and a Balance Sheet as on the date :

Adjustments:

SOLUTION

Working Notes:

Note: Expense related to income earned like consultancy charges, conference expenses are shown as net of income.

|

68 videos|160 docs|83 tests

|

|

Dec 22, 2024 Last updated |

|

Explore Courses for CA Foundation exam

|

|

past year papers

,Free

,Financial Statements of Not-for-Profit Organizations Chapter Notes | Accounting for CA Foundation

,MCQs

,video lectures

,shortcuts and tricks

,Financial Statements of Not-for-Profit Organizations Chapter Notes | Accounting for CA Foundation

,practice quizzes

,Exam

,study material

,Financial Statements of Not-for-Profit Organizations Chapter Notes | Accounting for CA Foundation

,Important questions

,Sample Paper

,Summary

,Semester Notes

,Objective type Questions

,Viva Questions

,Previous Year Questions with Solutions

,ppt

,mock tests for examination

,Extra Questions

;

Chapter Notes: Financial Statements of Not-for-Profit Organizations Free PDF Download

Importance of Chapter Notes: Financial Statements of Not-for-Profit Organizations

Chapter Notes: Financial Statements of Not-for-Profit Organizations

Chapter Notes: Financial Statements of Not-for-Profit Organizations CA Foundation Questions

Study Chapter Notes: Financial Statements of Not-for-Profit Organizations on the App

|

© EduRev

|

Education Revolution

|

|