Introduction to Micro Economics Class 12 Economics

What is an Economy?

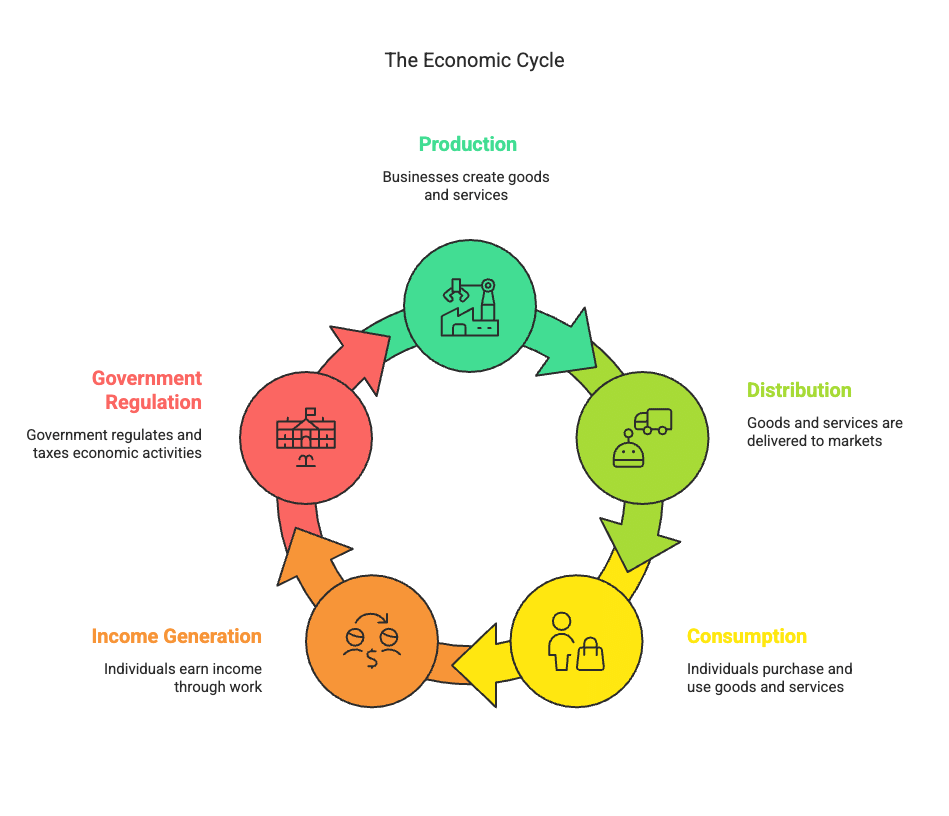

An economy is a system that includes the production, distribution, and consumption of goods and services within a particular region, such as a country. It is how a society decides what to make, how to make it, and how to share it among people.

This system includes many participants:

Individuals who work to earn income and spend it on goods and services

Businesses that produce goods or provide services in exchange for profits

The government, which plays a role in regulating economic activity, providing services, and collecting taxes

All these actors interact within markets—places (physical or virtual) where buying and selling happen. The goal of the economy is to allocate limited resources like land, labour, and capital efficiently so that the needs and wants of the population can be met.

Example: India’s economy includes farmers growing crops, factories manufacturing goods, banks offering financial services, people shopping in markets, and government programs like public healthcare or education.

What is Economics?

Economics is the study of how people, businesses, and governments make choices about how to use limited resources. It explores how we decide what to produce, how to produce it, and who gets to use the things that are made.

Since resources like money, time, raw materials, and labour are limited, economics helps us understand how to make the best possible choices.

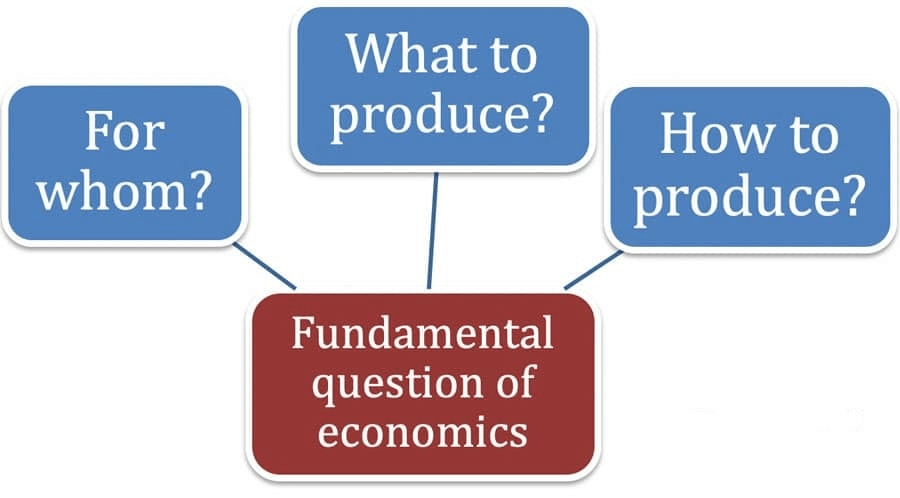

Economics answers three fundamental questions:

What to produce? (Should a country invest more in education or defence?)

How to produce? (Should a factory use more machines or more workers?)

For whom to produce? (Should basic goods be made available to all, or only to those who can afford them?)

By analysing these choices, economics helps us understand both individual behaviour and large-scale national and global trends.

Example: When petrol prices rise, people may choose to use public transport more often. This is a simple economic decision influenced by price and availability—a key focus in economics.

A Simple Economy

In a simple economy, people work, produce goods or services, earn money or other forms of income, and use it to satisfy their needs. However, this system faces a key challenge — the imbalance between unlimited needs and limited resources.

1. Needs are Unlimited

Every individual in a society has a long list of needs and wants. These include basic requirements like food, clothing, shelter, and transport, as well as other services such as education, healthcare, and entertainment.

For example:

A family may need nutritious food, a comfortable home, school education for children, and access to doctors.

They may also wish for new gadgets, vacation trips, or fashionable clothes.

There is no end to human desires — as soon as one need is fulfilled, another often takes its place.

2. Resources are Limited

While needs are unlimited, the resources to meet them — such as time, money, labour, land, and tools — are limited. People and economic units (like farmers, carpenters, or teachers) must make choices about how best to use their limited resources.

Examples:

A farmer can grow vegetables on his land and sell them in the market. He uses that income to buy clothes, tools, or pay school fees. However, he can only grow a limited amount based on the size of his land and the time he has.

A teacher offers teaching services in a school and earns a salary. With this income, the teacher buys food, pays rent, and saves for the future. But the teacher has only 24 hours in a day and a limited amount of energy — so only a certain number of teaching hours are possible.

Hence, resources — whether time, land, skill, or money — are never enough to meet every need.

3. Needs Exceed Resources

Because of this mismatch between wants and available means, individuals must prioritize — they choose some goods and services over others. This gives rise to the concept of opportunity cost — the value of what we give up when we choose something else.

For instance:

A person may choose to buy a mobile phone instead of going on a short trip, because they cannot afford both.

A weaver may decide to produce sarees instead of bedsheets, because sarees sell at a better price in the local market.

4. Matching Production with Needs

It is important for the entire society to align its production with the collective needs of its people. If too much of one good is produced and people don’t want it, it leads to wastage. If too little of an essential item is produced, it leads to shortages.

Examples:

If too many toys are produced and fewer food items, people may not have enough to eat.

If there is too much sugar but not enough medicine, the health of people may suffer.

Hence, a balance must be struck between what people want and what the economy produces.

5. The Core Economic Problem: Allocation and Distribution

Since resources are scarce, society faces the challenge of how to:

Allocate its limited resources (land, labour, capital) among different sectors — agriculture, industry, education, health, etc.

Distribute the final goods and services among people — who gets what and how much.

These are the fundamental economic problems that every society must solve — whether it is a simple rural economy or a modern industrial one.

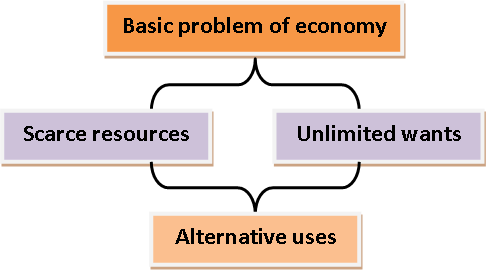

Central Problems of an Economy

‘Economic problem’ is the problem of choice involving the satisfaction of unlimited wants out of limited resources having alternative uses.

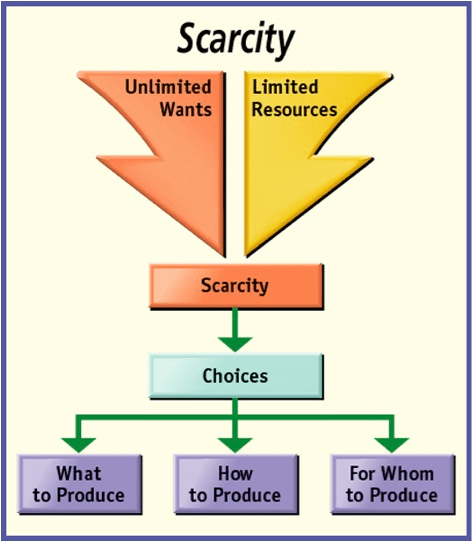

Scarcity

Scarcity is the fundamental economic problem that arises because resources are limited, but human wants are unlimited. This creates a situation where we must make choices — we cannot have everything we desire, so we prioritise and decide what to use our limited resources for.

1. Limited Resources vs Unlimited Wants

Resources such as money, time, land, labour, raw materials, and capital are finite. However, individuals continuously want more, better food, clothing, housing, gadgets, education, and experiences. Because we cannot fulfil all our desires at once, we must choose between alternatives.

Example:

A student has only three hours in the evening. If they need to study both Math and Science, they must divide their time, perhaps 2 hours for Math and 1 for Science. Spending more time on one subject means less time for the other. This is scarcity in action.

This situation of limited means and unlimited wants affects everyone —

Individuals must choose how to spend their time or money

Businesses must choose what goods to produce

Governments must choose how to use public funds

2. Alternative Uses of Resources

Scarcity leads to another key concept: alternative uses of resources.

Most resources can be used in more than one way, and choosing one use means giving up others. This leads to opportunity cost — the benefit of the next best alternative that we forgo.

Example:

A plot of land can be used to:

Grow wheat

Build houses

Open a factory

Create a public park

If the land is used for housing, it cannot be used for farming or industry at the same time.

The decision depends on needs, priorities, and long-term plans.

3. Scarcity Leads to Economic Problems

Because resources are scarce and have alternative uses, every economy must deal with three basic economic problems:

(i) What to Produce?

Should more food be grown, or more mobile phones be manufactured?

The economy must decide based on the needs and wants of its people.

(ii) How to Produce?

Should goods be produced using more labour (manual work) or more machines (technology)?

The choice depends on available resources and the aim of being efficient.

(iii) For Whom to Produce?

Who should receive the goods and services?

Should everyone get an equal share, or should it depend on income or work?

These questions must be answered carefully to ensure fairness and efficiency in the use of resources.

The central problems faced by an economy can be categorised under three heads:

1. What is produced and in what quantities?

This problem involves the selection of goods and services to be produced and the quantity to be produced of each selected commodity. It arises since resources are limited in an economy and can be put to alternative uses.

The problem of 'What to produce' has two aspects:

- What possible commodities to produce: An economy has to decide which consumer goods (rice, wheat, clothes, etc.) and which of the capital goods (machinery, equipment, etc.) are to be produced. In the same way, the economy has to choose between civil goods (bread, butter, etc.) and war goods (guns, tanks, etc.).

- How much to produce: After deciding the goods to be produced, the economy has to decide the quantity of each commodity that is selected. It means it involves a decision regarding the quantity to be produced, of consumer and capital goods, civil and war goods and so on. Guiding Principle: The guiding principle is to allocate resources in such a way that mthe aximum individuals in the economy are satisfied.

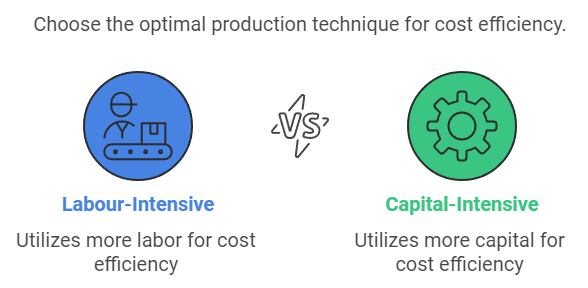

2. How are these goods produced?

This problem is concerned with the choice of technique of production to produce a given level of output.

For instance, a factory can choose between the following production techniques:

- The labour-intensive technique (where more labour is used than capital) or

- The capital-intensive technique (where more capital is used than labour) so that production is carried at minimum cost.

Example: Clothes can be produced with the help of handloom, which ensures greater employment (labour-intensive technique) or with the help of modern power looms, which ensure greater efficiency and productivity (capital-intensive techniques).

Sometimes, therefore, there can be a choice between choosing to employ more people and generating more income for society or choosing a capital-intensive method that is faster and more efficient.

3. For whom are these goods produced?

- This problem deals with the question of how an economy distributes its total production among different economic units (who gets how much to consume) and refers to the distribution of income and wealth in society.

Example: How much a computer engineer consumes is based on his earnings as compared to a doctor or a teacher. It has two aspects:

(a) Personal Distribution among different individuals and households. It is concerned with the problem of inequality in distribution.

(b) Functional Distribution among different factors of production (land, labour, capital, entrepreneur). It is not related to the problem of inequality.

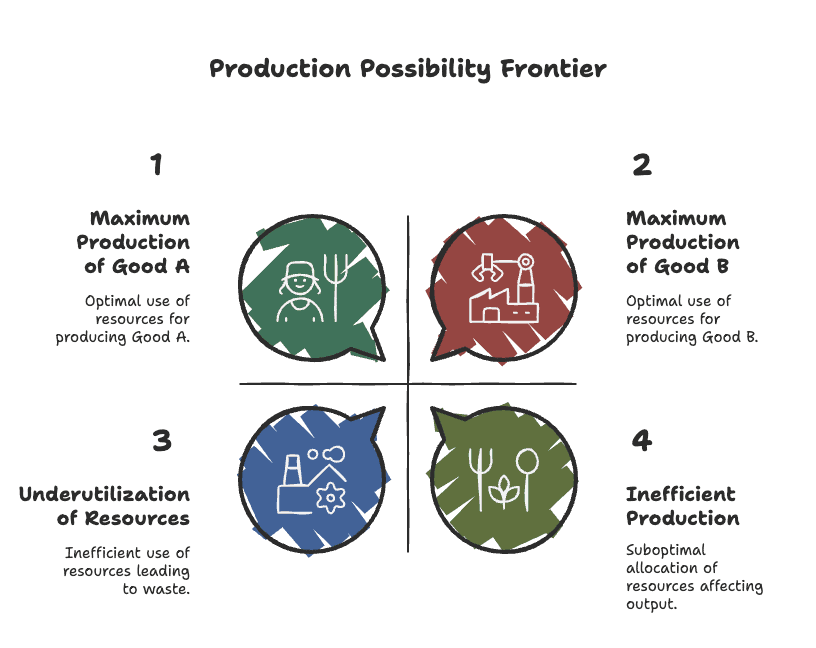

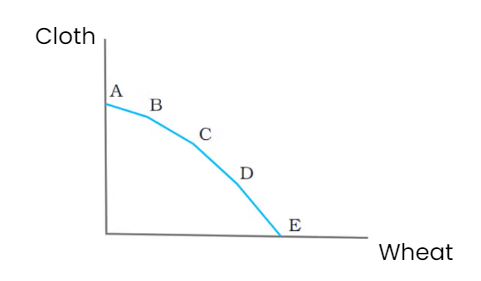

Production Possibility Frontier

Imagine an economy that produces only two goods — for example, rice and cloth. The PPF shows the maximum amount of rice and cloth that can be produced with the available land, labour, capital, and technology.

Key features:

Resources are limited

Choices must be made

Producing more of one good usually means producing less of another

Shape of the PPF: Concave Curve

The PPF is usually drawn as a concave curve (bowed outward). This shape represents the principle of increasing opportunity cost.

That means:

As we produce more of one good, we must give up more and more of the other. This happens because resources (like workers or machines) are not equally efficient in producing all goods.

Example:

Some land may be perfect for growing rice, but not for setting up cloth factories. If we shift that land to cloth production, it may not be very efficient. So, the cost of producing extra cloth increases as we produce more of it.

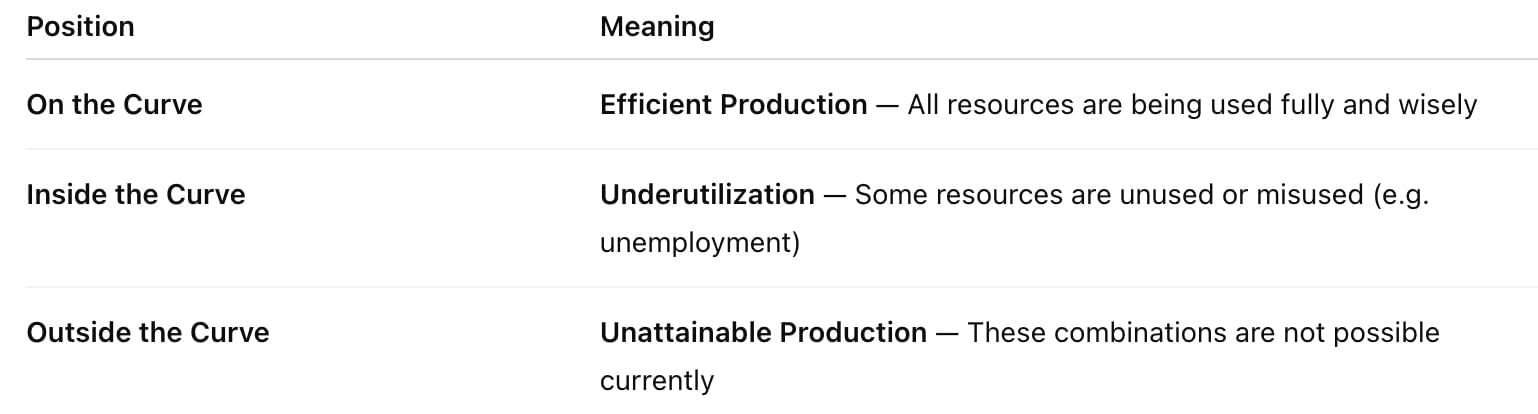

Understanding Points on, Inside, and Outside the PPF

Why is the PPF Important?

Helps us understand the concept of scarcity and choice

Shows the need for trade-offs and opportunity cost

Helps evaluate economic efficiency

Provides a visual way to understand how resource use affects production

Graphically:

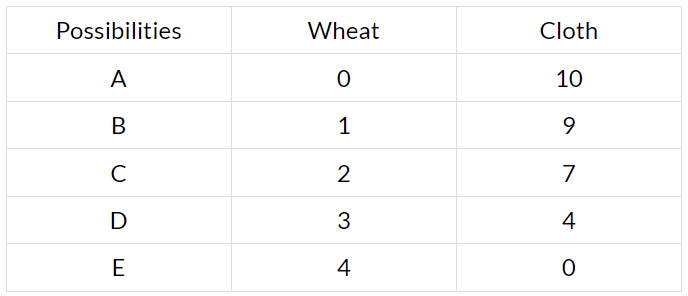

Suppose an economy decides to produce only two goods corn (representing agricultural goods) and cotton (representing industrial good).

- If 10 units of cotton are grown, then there is no space for corn to grow. This possibility is shown by point A.

- If 9 units of cotton is grown, then 1 unit of corn can be grown which is represented by B.

- Similarly, the other combinations are represented by points C, D and E.

Opportunity Cost:

Opportunity cost is the value of the next best alternative that you give up when you make a decision.

- If we use more of our limited resources to produce more of wheat, there will be fewer resources left for making cloth, and the same goes the other way.

- So, if we want to increase the amount of wheat we produce, we'll end up producing less cloth, and if we focus more on making cloth, we'll have less wheat.

- Understanding opportunity cost helps you make better choices by thinking about what you miss out on when you pick one option over another.

- Example: Suppose an economy has limited land, labour, and capital, which can be used to produce wheat or cloth. If the economy decides to use more of its resources to grow wheat, it will have to reduce the production of cloth because the same resources cannot be used for both at the same time. The cloth that is not produced becomes the opportunity cost of producing more wheat.

The same applies in reverse:

Producing more cloth means giving up some amount of wheat.

The more you produce of one good, the greater the opportunity cost in terms of the other good.

This is why the Production Possibility Frontier (PPF) is usually drawn as a concave curve—it shows that opportunity cost increases as you shift resources from one good to another.

Organisation of Economic Activities

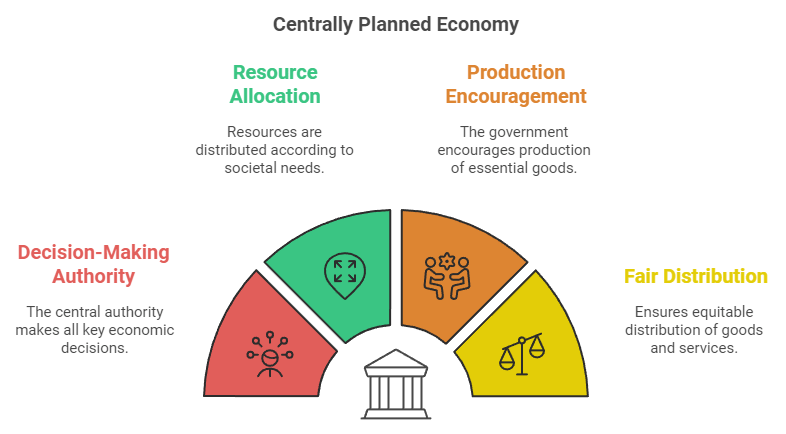

The Centrally Planned Economy

- In a centrally planned economy, the government or central authority makes all important decisions regarding the production, exchange, and consumption of goods and services.

- The central authority aims to achieve the desired allocation of resources and distribution of goods and services for the benefit of society as a whole.

Government Intervention for Social Welfare

If the economy lacks essential goods—like food, housing, or medicines—the government may:

Encourage production by providing subsidies or incentives

Directly produce those goods through public sector enterprises

Control prices to make the goods affordable for everyone

In situations where some people may not be able to access enough goods or services for survival, the government intervenes to ensure fair and equitable distribution. This is done through rationing, subsidies, or public distribution systems.

Example:

In the former Soviet Union, the government would set production targets for industries, control wages and prices, and decide how goods were distributed. If food was scarce in one region, resources were shifted to meet that need—even if it meant cutting back production elsewhere.

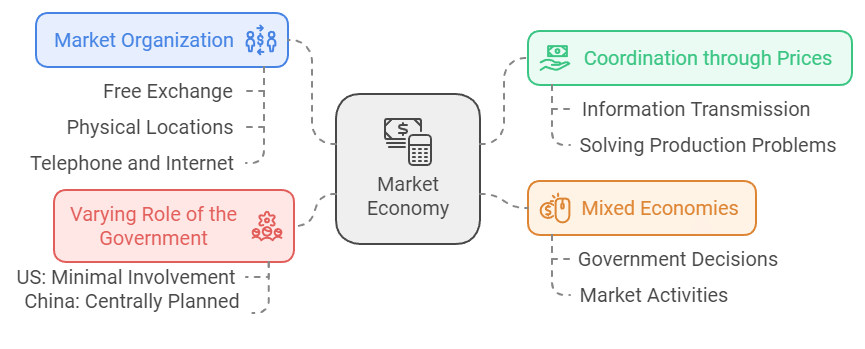

The Market Economy

The Market Economy

A market economy is a system where most economic decisions are made by buyers and sellers in the market—not by the government. People and businesses are free to decide what to make, how much to sell it for, and what to buy.

What is a Market?

In economics, a market is not just a shop or a marketplace. It means any place or way where people can buy and sell things. This could be:

A shop

A phone call

A website like Amazon

So, even ordering food online is part of a market!

How Do Markets Work?

In a market economy, prices play a very important role. They help people decide:

What to produce (If something is in demand and prices are high, businesses will produce more of it.)

How to produce (Businesses try to use the best and cheapest methods.)

For whom to produce (Goods are usually sold to people who are willing and able to pay.)

So, prices help solve the basic problems of the economy without direct government control.

Examples Around the World

Most countries today are not completely market-based or government-controlled. They use a mix of both systems:

In the United States, the government is less involved, and people have a lot of economic freedom.

In China, the government used to make most decisions, but now they allow more market-based choices.

Why Is It Important?

A market economy helps:

People make their own choices

Businesses compete, which improves quality

Resources get used more efficiently

But sometimes, markets don't work fairly for everyone. That’s why even in a market economy, the government still steps in to help with things like education, healthcare, and protecting the environment.

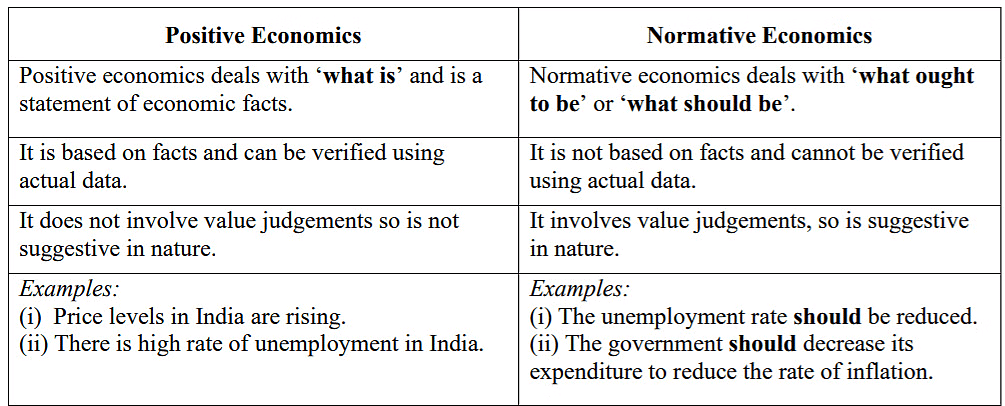

Positive and Normative Economics

- There are multiple ways to solve the central problems of an economy.

- These different mechanisms result in different allocations of resources and distributions of goods and services.

- It is important to determine which mechanism is more desirable for the economy as a whole.

- Economics analyzes and evaluates these mechanisms and their outcomes.

- Positive economic analysis studies how the mechanisms function, while normative economics evaluates how they should function.

- The distinction between positive and normative analysis is not strict, as both are closely related and understanding one requires understanding the other.

Positive Vs. Normative Economics

Positive Vs. Normative Economics

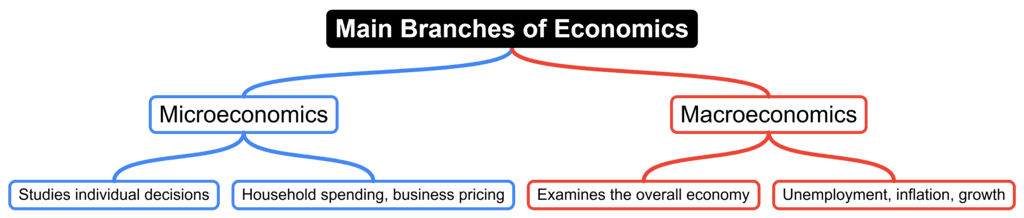

Microeconomics and Macroeconomics

- Economics is traditionally studied under two branches: Microeconomics and Macroeconomics.

- Microeconomics focuses on individual economic agents and their interactions in markets for goods and services.

- Macroeconomics looks at the economy as a whole, analyzing aggregate measures like total output, employment, and price level.

- Macroeconomics seeks to understand how these measures are determined and how they change over time.

- Questions in macroeconomics include determining total output, explaining its growth, and understanding resource unemployment and price increases.

- Unlike microeconomics, macroeconomics examines the behaviour of aggregate measures rather than individual markets.

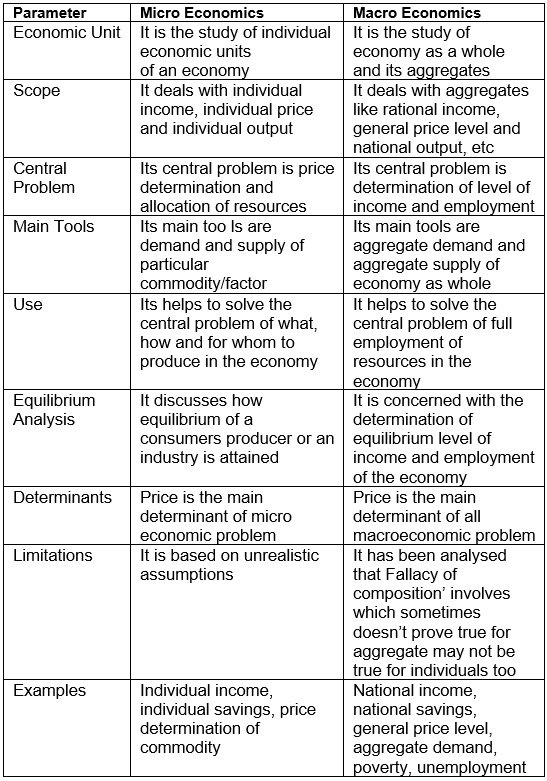

Difference between Micro and Macro Economics

Difference between Micro and Macro Economics

|

59 videos|274 docs|51 tests

|

FAQs on Introduction to Micro Economics Class 12 Economics

| 1. What are the central problems of an economy? |  |

| 2. What is the Production Possibility Frontier (PPF)? | |

| 3. How are economic activities organized in a simple economy? | |

| 4. What is the difference between positive and normative economics? | |

| 5. What is the difference between microeconomics and macroeconomics? | |

ppt

,Sample Paper

,Objective type Questions

,practice quizzes

,past year papers

,mock tests for examination

,Summary

,study material

,video lectures

,Exam

,shortcuts and tricks

,Semester Notes

,Important questions

,Previous Year Questions with Solutions

,Extra Questions

,Introduction to Micro Economics Class 12 Economics

,Introduction to Micro Economics Class 12 Economics

,Introduction to Micro Economics Class 12 Economics

,Viva Questions

,MCQs

,Free

;

Chapter Notes - Introduction to Microeconomics Free PDF Download

Importance of Chapter Notes - Introduction to Microeconomics

Chapter Notes - Introduction to Microeconomics

Chapter Notes - Introduction to Microeconomics Commerce Questions

Study Chapter Notes - Introduction to Microeconomics on the App

|

© EduRev

|

Education Revolution

|

|