Unit 5: Redemption of Preference Shares Chapter Notes | Accounting for CA Foundation PDF Download

Unit Overview

Introduction

- Redemption refers to the act of repaying an obligation at prearranged amounts and timings. In the context of preference shares, it is a contract that specifies the obligation to redeem these shares within or at the end of a given time period at an agreed price.

- Preference shares are issued with the understanding that shareholders will be repaid the amount they invested in the company at a future date, along with regular payments of a specified dividend during the tenure of the shares.

- The redemption date, also known as the maturity date, is the specified date when repayment is scheduled to occur, and it is usually indicated on the preference share certificate.

- Through redemption, a company can also adjust its financial structure. For instance, it can eliminate preference shares and replace them with other securities if such a change becomes advantageous for future growth.

Purpose of Issuing Redeemable Preference Shares

- Raising Finance in a Dull Market: Redeemable preference shares offer a viable option for raising funds when the primary market is sluggish.

- Attracting Investors: Companies whose shares are not listed on the stock exchange may struggle to attract investors. Redeemable preference shares provide an assurance to potential investors by guaranteeing redemption, making the investment more appealing.

- Utilizing Surplus Capital: Companies can redeem preference shares when they have surplus capital that cannot be effectively utilized for profitable business activities. This flexibility helps in managing excess funds.

- Dividend Flexibility: Unlike debentures or loans where interest is payable regardless of profit, preference dividends are only paid when there are profits. This makes redeemable preference shares a more flexible option during periods of loss.

In India, the issuance and redemption of preference shares are regulated by Section 55 of the Companies Act, 2013.

Provisions of the Companies Act (Section 55)

A company limited by shares may issue preference shares that are redeemable at the company’s option, within a period not exceeding 20 years from the date of issue, if authorized by its Articles.Key Points to Note:

- Redemption Sources: Shares can only be redeemed out of divisible or distributable profits (profits available for dividend) or from the proceeds of a fresh issue of shares specifically for redemption purposes.

- Full Payment Requirement: Preference shares cannot be redeemed unless they are fully paid.

- Premium on Redemption:

(i) For prescribed classes of companies complying with accounting standards under Section 133, any premium on redemption must be provided out of profits before redemption.

(ii) For other companies, the premium, if any, must be provided out of profits or the company’s securities premium account before redemption. - Capital Redemption Reserve Account: When redeeming shares out of profits, a sum equal to the nominal amount of shares redeemed must be transferred to the Capital Redemption Reserve Account (CRR) out of divisible profits. (i) The CRR Account is treated as paid-up share capital, and its utilization is restricted to issuing fully paid-up bonus shares.

- Security for Creditors: The redemption process aims to ensure that the security for creditors and bankers is not diminished.

- Partial Redemption: It is possible to redeem part of the preference share capital out of accumulated divisible profits and the balance out of a fresh issue of shares.

Methods of Redemption of Fully Paid-Up Shares

Redemption of preference shares refers to the repayment by a company of its obligation concerning shares that have been issued. Under the Companies Act, 2013, preference shares issued by a company must be redeemed within a maximum period, typically 20 years. This means that companies cannot issue irredeemable preference shares.- Section 55 of the Companies Act, 2013, governs the redemption of preference shares. It aims to ensure that the redemption does not lead to a reduction in shareholders’ funds, thereby protecting the interests of outsiders. To achieve this, the Act requires either a fresh issue of shares or the retention of distributable profits, which are then transferred to the Capital Redemption Reserve Account.

- The rationale behind these provisions is to safeguard the interests of outsiders who are entitled to be paid before the redemption of preference share capital. By substituting the nominal value of the capital redeemed, the same amount of shareholders’ funds is maintained, ensuring protection for outsiders.

Methods for Filling Gap in Capital:

When redeeming redeemable preference shares, the gap created in the company’s capital must be filled by:

- Proceeds from a fresh issue of shares.

- Capitalisation of undistributed profits by creating a Capital Redemption Reserve.

- A combination of both (a) and (b).

A. Redemption of Preference Shares by Fresh Issue of Shares

1. Overview

- Redemption of preference shares can be done using the proceeds from a fresh issue of shares, either equity or preference shares.

- Proceeds from the issue of debentures cannot be used for this purpose.

2. Securities Premium Consideration

- When making a fresh issue for the redemption of preference shares at a premium, a question arises about including the securities premium in the proceeds.

- According to Section 52 of the Companies Act, 2013, the securities premium account can be applied for certain purposes, including:

- (a) Issue of unissued shares as fully paid bonus securities.

- (b) Writing off preliminary expenses.

- (c) Writing off expenses, commission, or discount on securities or debentures.

- (d) Providing for premium on redemption of redeemable preference shares or debentures.

- (e) Purchase of own shares or other securities.

3. Restrictions on Utilization

- Certain companies complying with Accounting Standards cannot apply the securities premium account for purposes (b) and (d) mentioned above.

- Utilization of the securities premium account for purposes not prescribed is considered a contravention of law.

4. Conclusion

- Proceeds from a fresh issue of shares for the redemption of preference shares do not include the securities premium amount.

B. Reasons for Issuing New Equity Shares

- Permanent Capital Requirement: Companies may realize that they need capital on a permanent basis and prefer to issue equity shares instead of redeemable preference shares, which have a fixed dividend rate.

- Insufficient Profit Balance: When the balance of profit available for dividend is insufficient, companies may opt for issuing equity shares.

- Poor Liquidity Position: Companies with a weak liquidity position may find it more advantageous to issue equity shares.

C. Advantages of Redemption through Fresh Equity Shares

- No Immediate Cash Outflow: There is no cash outflow now or in the future.

- Potential for Premium Valuation: New equity shares may be valued at a premium.

- Retention of Equity Interest: Existing shareholders retain their equity interest.

D. Disadvantages of Redemption through Fresh Equity Shares

- Dilution of Future Earnings: Future earnings may be diluted due to the issuance of new equity shares.

- Change in Shareholding: If new shares are issued to outsiders, shareholding in the company changes. This can be mitigated if the fresh issue is made to existing shareholders in proportion to their shareholding (rights issue).

Accounting Entries for Share Transactions

1. When New Shares are Issued at Par:

Bank Account Dr.

To Share Capital Account

(Being the issue of ……. shares of ₹…… each for the purpose of redemption of preference shares, as per Board’s Resolution No… dated…. )

2. When New Shares are Issued at a Premium:

Bank Account Dr.

To Share Capital Account

To Securities Premium Account

(Being the issue of …….. shares of ₹…… each at a premium of ₹…… each for the purpose of redemption of preference shares as per Board’s Resolution No….. dated……)

3. When Preference Shares are Redeemed at Par:

Redeemable Preference Share Capital Account Dr.

To Preference Shareholders Account

4. When Preference Shares are Redeemed at a Premium:

Redeemable Preference Share Capital Account Dr.

To Preference Shareholders Account

To Premium on Redemption of Preference Shares Account

5. When Payment is Made to Preference Shareholders:

Preference Shareholders Account Dr.

To Bank Account

For adjustment of premium on redemption

6. For Adjustment of Premium on Redemption:

Profit and Loss Account Dr.

To Premium on Redemption of Preference Shares Account

ILLUSTRATION 1

Hinduja Company Ltd. had 5,000, 8% Redeemable Preference Shares of ₹ 100 each, fully paid up. The company decided to redeem these preference shares at par by the issue of sufficient number of equity shares of ` 10 each fully paid up at par. You are required to pass necessary Journal Entries including cash transactions in the books of the company.

SOLUTION

ILLUSTRATION 2

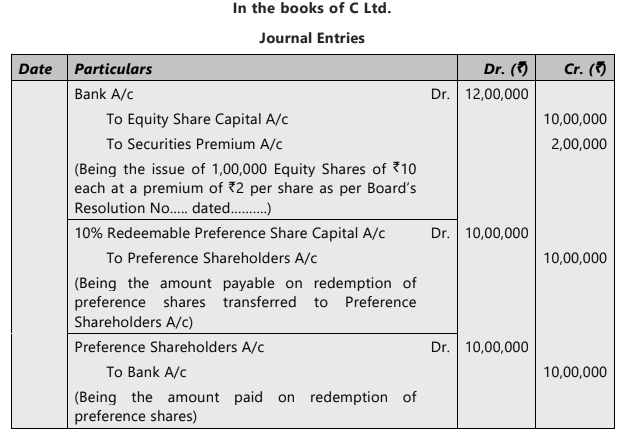

C Ltd. had 10,000, 10% Redeemable Preference Shares of ₹ 100 each, fully paid up. The company decided to redeem these preference shares at par, by issue of sufficient number of equity shares of ₹ 10 each at a premium of ₹ 2 per share as fully paid up. You are required to pass necessary Journal Entries including cash transactions in the books of the company.

SOLUTION

Note: Amount required for redemption is ` 10,00,000. Therefore, face value of equity shares to be issued for this purpose must be equal to ` 10,00,000. Premium received on new issue cannot be used to finance the redemption.

ILLUSTRATION 3

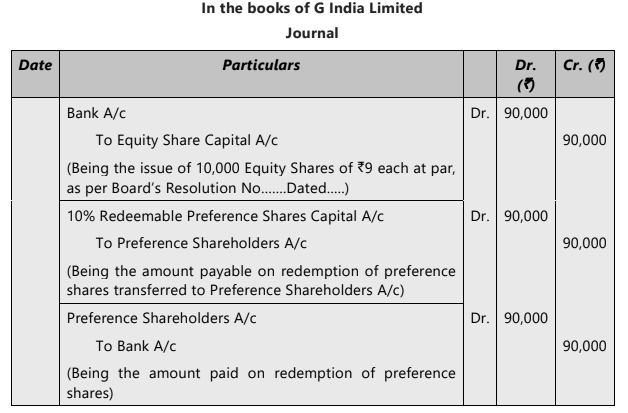

G India Ltd. had 9,000 10% redeemable Preference Shares of ₹ 10 each, fully paid up. The company decided to redeem these preference shares at par by the issue of sufficient number of equity shares of ₹ 9 each fully paid up.

You are required to pass necessary Journal Entries including cash transactions in the books of the company.

SOLUTION

Calculation of Minimum Fresh Issue of Shares

1. Determine Maximum Reserves and Surplus: Assess the maximum amount of reserves and surplus available for redemption. This involves looking at the balances in the balance sheet before redemption and considering any additional information provided in the problem. For instance, if the general reserve balance is ₹1,00,000 and the Board of Directors has decided that it should not fall below ₹40,000, the maximum amount available for redemption would be ₹60,000.

2. Calculate Minimum Proceeds of Fresh Issue: Subtract the maximum amount of reserves and surplus available for redemption from the nominal value of the preference shares to be redeemed. This calculation helps determine the minimum proceeds required from a fresh issue of shares. Section 55 allows redemption either from fresh issue proceeds or from divisible profits.

3. Determine Minimum Number of Shares: Divide the minimum proceeds calculated in the previous step by the proceeds of one share. The proceeds of one share refer to its par value, whether issued at par or at a premium. If shares are issued at a discount, it refers to the discounted value. The formula is: Minimum Number of Shares = Minimum Proceeds / Face Value of One Share

4. Adjust Minimum Number of Shares: Make necessary adjustments to the minimum number of shares calculated. If the result includes a fraction, round it up to the next whole number to comply with Section 55. Additionally, if the problem specifies that the proceeds or number of shares should be a multiple of a certain number (e.g., 10, 50, 100), round up to the next higher multiple.

ILLUSTRATION 4

The Board of Directors of a Company decided to issue minimum number of equity shares of ₹ 9 to redeem ₹ 5,00,000 preference shares. The maximum amount of divisible profits available for redemption is ₹ 3,00,000. Calculate the number of shares to be issued by the company to ensure that the provisions of Section 55 are not violated. Also determine the number of shares if the company decides to issue shares in multiples of 50 only.

SOLUTION

Nominal value of preference shares ₹ 5,00,000

Maximum possible redemption out of profits ₹3,00,000

Minimum proceeds of fresh issue ₹ 5,00,000 – 3,00,000 = ₹ 2,00,000

Proceed of one share = ₹9

Minimum number of shares = 2,00,000 / 9 = 22,222.22 shares

As fractional shares are not permitted, the minimum number of shares to be issued is 22,223 shares.

If shares are to be issued in multiples of 50, then the next higher figure which is a multiple of 50 is 22,250. Hence, minimum number of shares to be issued in such a case is 22,250 shares.

Fresh Issue at a Premium and Minimum Fresh Issue

Fresh Issue at a Premium: When calculating the minimum number of shares for a fresh issue at a premium, it is crucial to handle the figures with care. The minimum fresh issue cannot be determined without knowing the profits available for replacing preference shares. However, the profits available for replacement can only be figured out if we know how much profit is needed for redemption to cover the premium on redemption.

- To simplify this process, we can make an assumption: suppose the profits available for redemption are not needed to cover the premium on redemption of preference shares. This means that the securities premium, including the premium on the fresh issue, is greater than the premium on redemption.

- If this assumption is valid, we can easily calculate the minimum number of shares without using complex equations. However, if this condition does not hold, we would need to use an equation to determine the minimum number of shares required.

Minimum Fresh Issue to Provide Funds for Redemption

- In addition to complying with Section 55, the fresh issue of shares is aimed at generating funds to make payments to preference shareholders. To calculate the minimum number of fresh shares that need to be issued for this purpose, we compare the amount payable to preference shareholders with the funds available for redemption.

- The difference between these amounts indicates the additional funds that need to be raised through the fresh issue of shares. To determine the minimum number of shares to be issued, we divide this amount by the issue price of a share, which includes any premium on the fresh issue. This calculation helps ensure that sufficient funds are raised to meet the obligations towards preference shareholders.

ILLUSTRATION 5

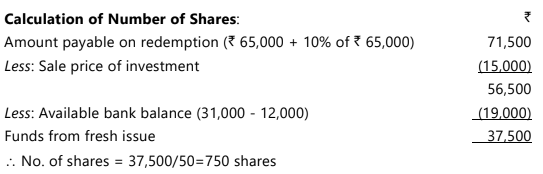

X Ltd. gives you the following information as at 31st March, 2023:

The share capital of the company consists of ₹ 50 each equity shares of ₹ 2,25,000 and ₹ 100 each Preference shares of ` 65,000(issued on 1.4.2021). Reserves and Surplus comprises Profit and Loss Account only.

In order to facilitate the redemption of preference shares at a premium of 10%, the Company decided:

(a) to sell all the investments for ₹ 15,000.

(b) to finance part of redemption from company funds, subject to, leaving a bank balance of ₹ 12,000.

(c) to issue minimum equity share of ₹ 50 each share to raise the balance of funds required. You are required to pass the necessary Journal Entries to record the above transactions.

SOLUTION

Working Note:

Redemption of Preference Shares by Capitalisation of Undistributed Divisible Profits

Another method for redeeming preference shares, as per the Companies Act, involves using distributable profits instead of issuing new shares. When shares are redeemed using distributable profits, an amount equal to the face value of the redeemed shares is transferred to the Capital Redemption Reserve Account by debiting the distributable profit. This means that a portion of the distributable profits is set aside to ensure it can never be distributed to shareholders as dividends.Distributable profit refers to the profit or a portion of profit that can legally be distributed as dividends to shareholders.

Provisions of the Companies Act

According to the Companies Act, when preference shares are redeemed using distributable profits, a sum equal to the nominal amount of the shares redeemed must be transferred to the Capital Redemption Reserve Account from profits that would otherwise be available for dividend. This ensures that the redeemed shares are properly accounted for and that the company's financial stability is maintained.

- Only divisible profits can be used to create the Capital Redemption Reserve. Non-divisible profits cannot be used for this purpose.

Advantages of Redemption of Preference Shares by Capitalisation of Undistributed Divisible Profits

- No Change in Equity Shareholding Percentage: The redemption process does not alter the percentage of equity shareholding in the company.

- Utilisation of Surplus Funds: Surplus funds can be effectively utilized for the redemption process.

Disadvantages of Redemption of Preference Shares by Capitalisation of Undistributed Divisible Profits

- Reduction in Liquidity: There will be a reduction in liquidity, which may necessitate the sale of assets such as investments.

Accounting Entries

1. For transferring nominal amount of shares redeemed to Capital Redemption Reserve Account

2. When shares are redeemed at par

3. When shares are redeemed at a premium

4. When payment is made to preference shareholders

4. When payment is made to preference shareholders

5. For adjustment of premium of redemption

ILLUSTRATION 6

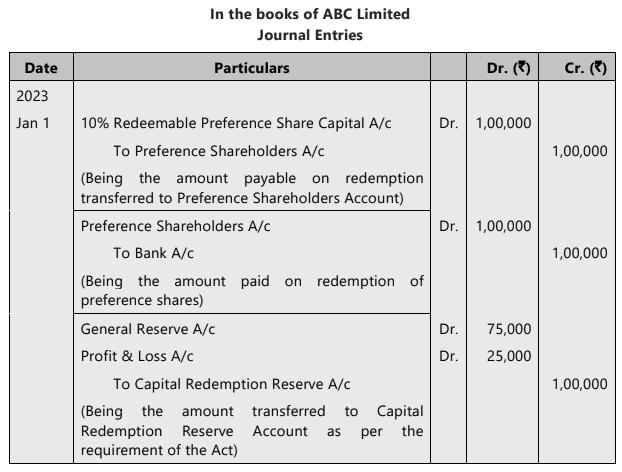

The following are the extracts from the Balance Sheet of ABC Ltd. as on 31st December, 2022.

Share capital: 40,000 Equity shares of ₹ 10 each fully paid – ₹ 4,00,000; 1,000 10% Redeemable preference shares of ₹ 100 each fully paid – ₹ 1,00,000.

Reserve & Surplus: Capital reserve – ₹ 50,000; Securities premium – ₹ 50,000; General reserve – ₹ 75,000; Profit and Loss Account – ₹ 35,000

On 1st January 2023, the Board of Directors decided to redeem the preference shares at par by utilisation of reserve.

You are required to pass necessary Journal Entries including cash transactions in the books of the company.

SOLUTION

Note: Securities premium and capital reserve (not being distributable profits) cannot be utilised for transfer to Capital Redemption Reserve.

Redemption of Preference Shares by combination of Fresh Issue and Capitalisation of Undistributed divisible Profits

A company can redeem the preference shares partly from the proceeds from new issue and partly out of profits. In order to fill in the ‘gap’ between the face value of shares redeemed and the proceeds of new issue, a transfer should be made from distributable profits (Profit & Loss Account, General Reserve and other Free Reserves) to Capital Redemption Reserve Account.Formula:

The phrase ‘proceeds from fresh/new issue’ can be understood in different ways depending on how the shares are issued:

(a) Issue at Par: When shares are issued at par value, the entire amount is credited to Share Capital. For example, if a share has a par value of ₹10 and is issued at ₹10, the full ₹10 is credited to Share Capital.

(b) Issue at Premium: When shares are issued at a premium, the amount credited to Share Capital is only the par value, while the premium is credited to the Securities Premium Account. The premium is not considered 'proceeds' because if it were, the transfer of distributable profits to the Capital Redemption Reserve would be reduced by the amount of the premium received. For instance, if a share with a par value of ₹10 is issued at ₹15, ₹10 is credited to Share Capital and ₹5 is credited to the Securities Premium Account.

(c) Issue at Discount: When shares are issued at a discount, the amount received is debited to Cash/Bank. For example, if a share with a par value of ₹10 is issued at ₹8, the ₹8 received is debited to Cash/Bank.

Note: Section 53 of the Companies Act, 2013 prohibits issue of shares at a discount, except in case of issue of Sweat Equity Shares as outlined in Section 54.

ILLUSTRATION 7

C Limited had 3,000, 12% Redeemable Preference Shares of ₹ 100 each, fully paid up. The company had to redeem these shares at a premium of 10%.

It was decided by the company to issue the following:

(i) 25,000 Equity Shares of ₹ 10 each at par,

(ii) 1,000 14% Debentures of ₹ 100 each.

The issue was fully subscribed and all amounts were received in full. The payment was duly made. The company had sufficient profits. Show Journal Entries in the books of the company.

SOLUTION

Working Note:

Amount to be transferred to Capital Redemption Reserve Account

Face value of shares to be redeemed - 3,00,000

Less: Proceeds from new issue - (2,50,000)

Total Balance - 50,000

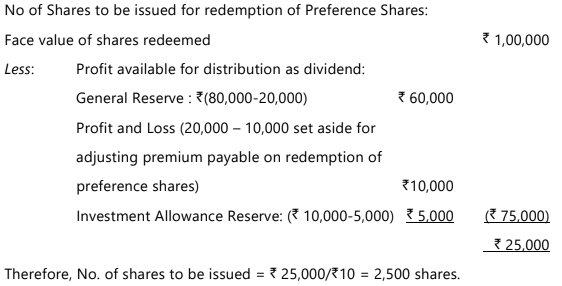

ILLUSTRATION 8

The capital structure of a company consists of 20,000 Equity Shares of ₹ 10 each fully paid up and 1,000 8% Redeemable Preference Shares of ₹ 100 each fully paid up (issued on 1.4.2021).

Undistributed reserve and surplus stood as: General Reserve ₹ 80,000; Profit and Loss Account ₹ 20,000; Investment Allowance Reserve out of which ₹ 5,000, (not free for distribution as dividend) ₹ 10,000; Securities Premium ₹ 2,000, Cash at bank amounted to ₹ 98,000. Preference shares are to be redeemed at a Premium of 10% and for the purpose of redemption, the directors are empowered to make fresh issue of Equity Shares at par after utilising the undistributed reserve and surplus, subject to the conditions that a sum of ₹ 20,000 shall be retained in general reserve and which should not be utilised.

Pass Journal Entries to give effect to the above arrangements.

SOLUTION

Working Note:

Sale of Investments to Provide Sufficient Funds for Redemption: Companies may have sufficient investments, which can be sold, in the market to arrange funds for redemption of preference shares.

Redemption of Partly Called-Up Preference Shares

When redeeming preference shares, it's important to note that only fully paid-up shares can be redeemed by a company. Here are some key points regarding the redemption of partly called-up preference shares:- Redemption of Partly Called-Up Shares: If the situation involves redeeming preference shares that are partly called-up, it is assumed that the final call on these shares has been demanded and received before proceeding with their redemption.

- Distinction Between Fully Paid and Partly Paid Shares: If information is provided about both fully paid and partly paid preference shares, it is presumed that only fully paid shares are eligible for redemption, while the partly paid shares remain intact.

- Forfeiture of Shares: The company has the right to forfeit shares if the call money is not received, despite giving the shareholder an opportunity to pay it through reminders.

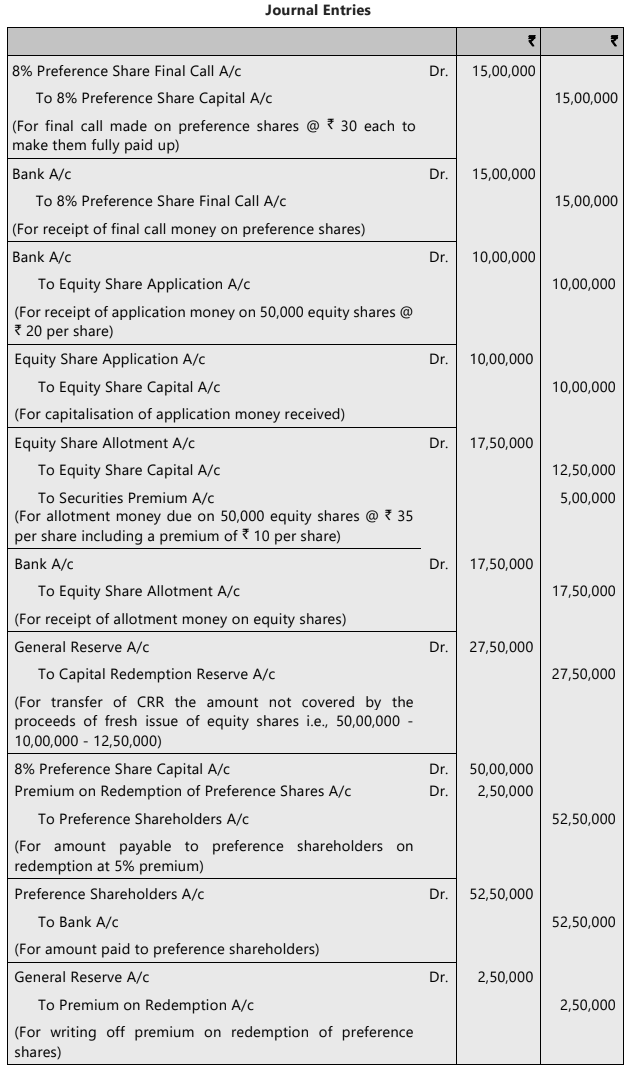

ILLUSTRATION 9

The Balance Sheet of XYZ Ltd. as at 31st March, 2021 inter alia includes the following information:

Under the terms of their issue, the preference shares are redeemable on 31st March, 2022 at 5% premium. In order to finance the redemption, the company makes a rights issue of 50,000 equity shares of ₹ 100 each at ₹ 110 per share, ₹ 20 being payable on application, ₹ 35 (including premium) on allotment and the balance on 1st January, 2023. The issue was fully subscribed and allotment made on 1st March, 2022. The money due on allotment were duly received by 31st March, 2022. The preference shares were redeemed after fulfilling the necessary conditions of Section 55 of the Companies Act, 2013.

You are asked to pass the necessary Journal Entries. (Ignore date column)

SOLUTION

Note: On the redemption of redeemable preference shares out of accumulated divisible profits, it will be necessary to transfer to the Capital Redemption Reserve Account an amount equal to the amount repaid on the redemption of preference shares on account of face value less proceeds of a fresh issue of shares made for the purpose of redemption.

Redemption of Fully Called but Partly Paid-Up Preference Shares

The issue of unpaid calls on fully called-up shares can be examined under the following categories:1. When Calls-in-Arrears are Received by the Company

- If the company receives the amount of unpaid calls before redemption, the following accounting entry is made:

After receiving the calls in arrears, the shares become fully paid up, and the company can proceed with redemption in the normal course.

2. In the Case of Forfeited Shares

- If shareholders fail to pay the unpaid calls despite receiving a proper notice from the company, the Board of Directors may decide to forfeit the shares.

- This is done when the redemption of these shares is due immediately or in the near future.

- The journal entry for forfeiture in this case is as follows:

Note: In this situation, the number of shares to be redeemed will be reduced by the number of shares forfeited.

Since the preference shares are being redeemed, the forfeited shares will not be reissued.

Therefore, the balance in the Shares Forfeited Account should be transferred to Capital Reserve by passing the following journal entry:

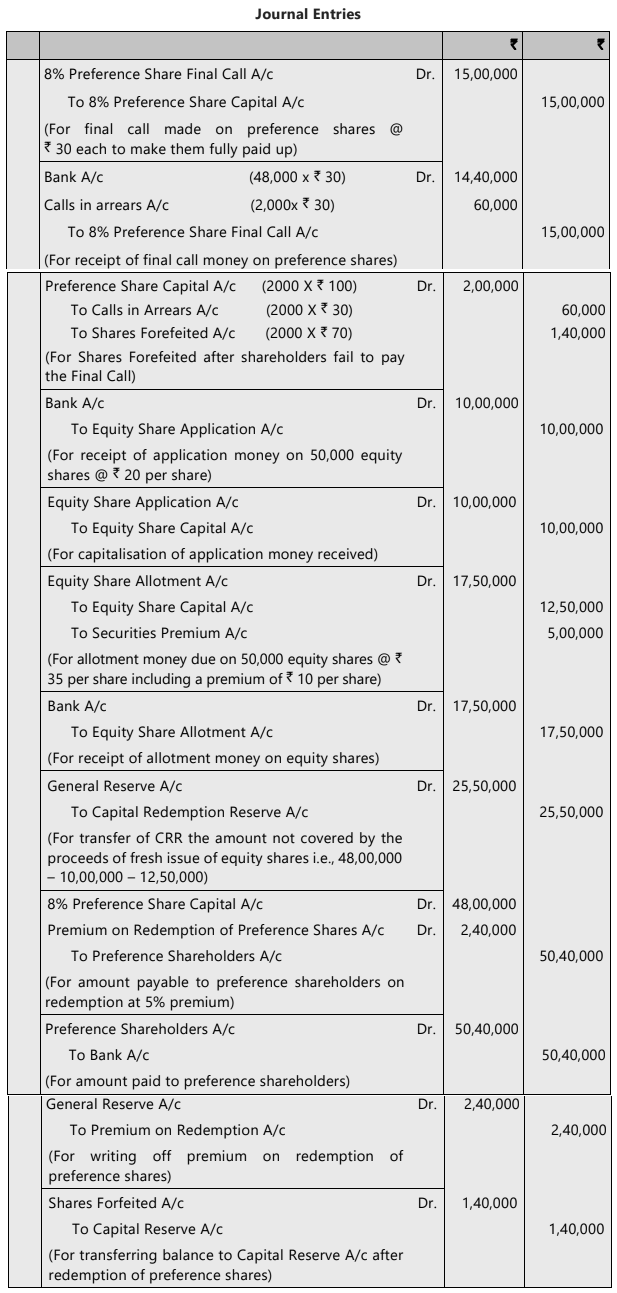

ILLUSTRATION 10

With the help of the details in Illustration 9 above and further assuming that the Preference Shareholders holding 2,000 shares fail to make the payment for the Final Call made under Section 55, you are asked to pass the necessary Journal Entries and show the relevant extracts from the balance sheet as on 31st March, 2022 with the corresponding figures as on 31st December, 2021 assuming that the shares in default are forfeited after giving proper notices. (Ignore date column)

SOLUTION

Note: Amount received (excluding premium) on fresh issue of shares till the date of redemption should be considered for calculation of proceeds of fresh issue of shares. Thus, proceeds of fresh issue of shares ` 22,50,000 (`10,00,000 application money plus ` 12,50,000 received on allotment towards share capital) will be considered.

|

68 videos|160 docs|83 tests

|

FAQs on Unit 5: Redemption of Preference Shares Chapter Notes - Accounting for CA Foundation

| 1. What are redeemable preference shares and why are they issued? |  |

| 2. What does Section 55 of the Companies Act entail regarding redeemable preference shares? | |

| 3. What are the methods for redeeming fully paid-up preference shares? | |

| 4. Can preference shares be redeemed using undistributed divisible profits? | |

| 5. How does the redemption of partly called-up preference shares work? | |

|

4.63/5 Rating |

|

Dec 22, 2024 Last updated |

|

Explore Courses for CA Foundation exam

|

|

Sample Paper

,Summary

,Free

,Exam

,Unit 5: Redemption of Preference Shares Chapter Notes | Accounting for CA Foundation

,Important questions

,Viva Questions

,Unit 5: Redemption of Preference Shares Chapter Notes | Accounting for CA Foundation

,Objective type Questions

,MCQs

,practice quizzes

,ppt

,Extra Questions

,Previous Year Questions with Solutions

,video lectures

,study material

,Semester Notes

,past year papers

,Unit 5: Redemption of Preference Shares Chapter Notes | Accounting for CA Foundation

,shortcuts and tricks

,mock tests for examination

;

Chapter Notes- Unit 5: Redemption of Preference Shares Free PDF Download

Importance of Chapter Notes- Unit 5: Redemption of Preference Shares

Chapter Notes- Unit 5: Redemption of Preference Shares

Chapter Notes- Unit 5: Redemption of Preference Shares CA Foundation Questions

Study Chapter Notes- Unit 5: Redemption of Preference Shares on the App

|

© EduRev

|

Education Revolution

|

|