Best Study Material for Commerce Exam

Commerce Exam > Commerce Notes > Accountancy Class 12 > Financial Statements of Not- for-Profit Organizations

Financial Statements of Not- for-Profit Organizations | Accountancy Class 12 - Commerce PDF Download

MEANING

It is an organization provides service to the society. The motive of these organizations is social welfare as a service provider, not for earning profit.

Following Statements are to be prepared by these organizations that are:

1. Receipts and Payment Account.

2. Income and Expenditure Account.

3. Opening and Closing Balance Sheet.

1. Receipts and Payment Account: It is prepared for recording the transactions related to cash. It is just like a cash book. All cash receipts recorded in debit side and all cash payments are recorded in credit side.

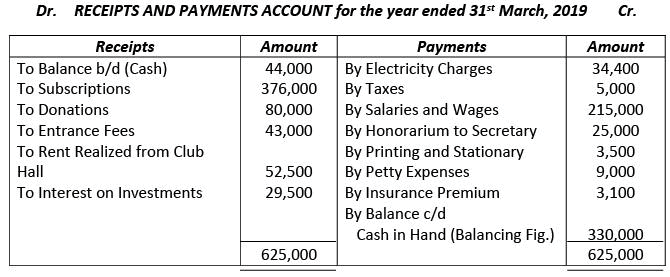

Example 1. From the following information given below, prepare Receipts and Payments Account of Friends Club, Delhi, for the year ended 31st March, 2019.

Cash Balance on 1st April, 2018 Rs. 44,000; Subscriptions Rs. 376,000; Donations Rs. 80,000; Entrance Fees Rs. 43,000; Rent Realized from Club Hall Rs. 52,500; Electricity Charges Rs. 34,400; Taxes Rs. 5,000; Salaries and Wages Rs. 215,000; Honorarium to Secretary Rs. 25,000; Interest Received on Investments Rs. 29,500; Printing and Stationary Rs. 3,500; Petty Expenses Rs. 9,000; Insurance Premium Paid Rs. 3,100.

Solution.

Friends Club, Delhi

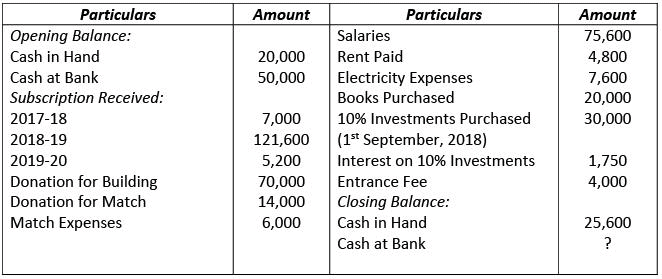

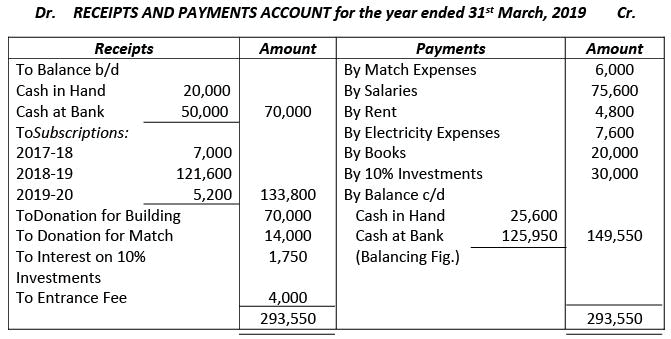

Example 2. From the information given below, prepare Receipts and Payments Account of Old men Recreation Club for the year ended 31st March, 2019. Solution.

Solution.

Oldmen Recreation Club, Delhi

2. Income and Expenditure Account: It is prepared to record the transactions that are incurred and generated in the same years. It means items are related to previous years or next year must be excluded. All expenses/losses are recorded in debit side and all incomes/profits are recorded in credit side.

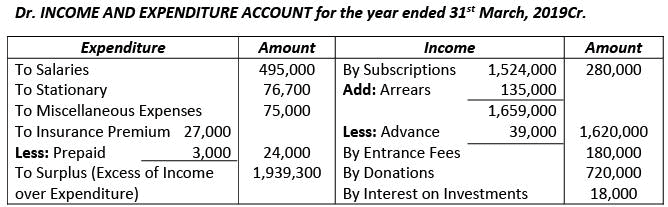

Example 3. From the following Receipts and Payments Account of Accountants Club Prepare Income and Expenditure Account for the year ended 31st March, 2019.

(i) Subscriptions in arrears for the year ended 31st March, 2019 – Rs. 135,000 and Subscriptions received in advance during the year ended 31st March, 2019 – Rs. 39,000.

(ii) Insurance Premium prepaid is Rs. 3,000.

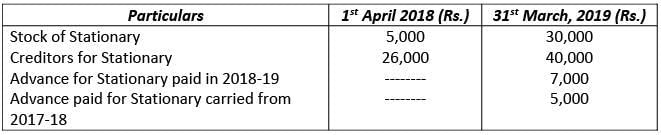

(iii) The details with respect to Stationary of Accountants Club is as follows: Solution.

Solution.

Accountants Club

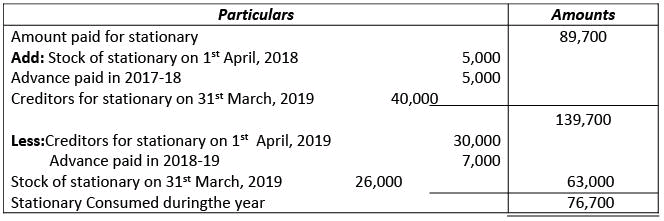

Working Note: Consumption of Stationary during the year:

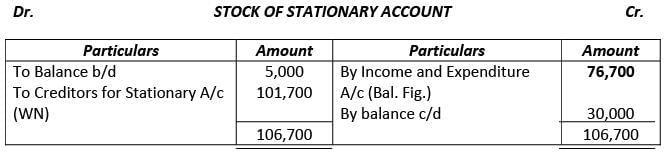

Working Note: Consumption of Stationary during the year: Alternatively: Consumption of Stationary may be calculated by preparing following two accounts:

Alternatively: Consumption of Stationary may be calculated by preparing following two accounts:

3. Opening Balance Sheet: It is prepared to find out the value of Capital Funds means opening capital.

4. Closing Balance Sheet: It is prepared to record the value of different types of Assets and Liabilities with adjusted value.

Before above three statements, you have to know the treatment of following items separately:

(a) Subscriptions.

(b) Fund based accounting like Match Fund.

(c) Consumable value of items likes Sports materials, Medicine, etc.

(d) Incomes like Entrance Fees, Locker Rent, etc.

(e) Expenses like Salary Paid, Rent Paid, etc.

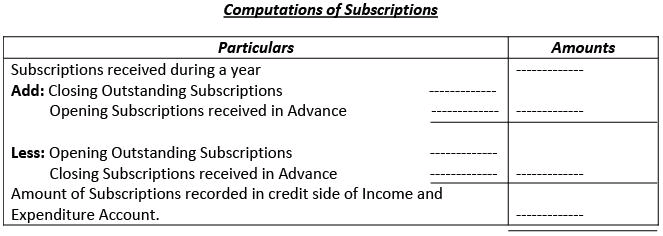

(a) Subscriptions: It is an amount paid by the members of Not-for-Profit Organizations for their membership. It is the main sources of revenue for NPO or we can say primary source of revenue.

(i) Outstanding Subscriptions: It means earned but not received. Opening Outstanding related to previous year and closing outstanding related to current year, treated as assets.

(ii) Subscriptions received in Advance: It means received but not earned. Opening received in advance related to current year and closing received in advance related to next year, treated as liabilities.

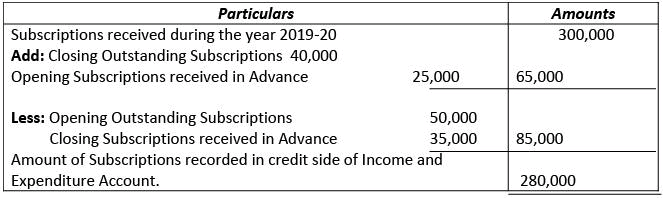

Examples 4. Calculate amount of Subscriptions which will be recorded in credit side of Income and Expenditure A/c for the year ended 31st March, 2020 from the following informations;

(a) Outstanding Subscriptions for the year 2018-19 was Rs. 50,000.

(b) Subscription received in advance for the year 2019-20 was Rs. 40,000.

(c) Subscription received during the year 2019-20 was Rs. 300,000.

(d) Outstanding Subscription for the year 2019-20 was Rs. 25,000.

(e) Subscription received in advance for the year 2020-21 was Rs.35, 000.

Solution.

INCOME AND EXPENDITURE ACCOUNT

Working Note:

Working Note:

Computations of Subscriptions

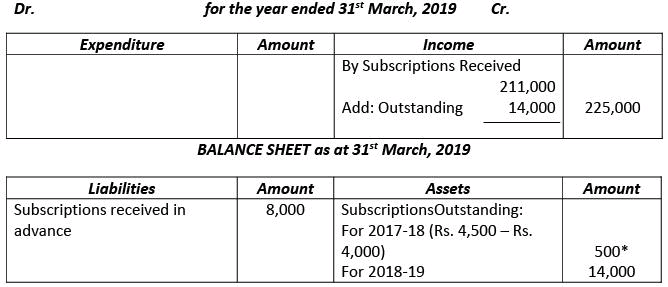

Example 5. Subscriptions received during the year ended 31st March, 2019 are:

| For the year ended 31st March, 2018 | Rs. 4,000 |

| For the year ended 31st March, 2019 | Rs. 211,000 |

| For the year ended 31st March, 2020 | Rs. 8,000 |

| Rs. 223,000 |

There are 450 members, each paying an annual subscription of Rs. 500. Rs 4,500 were in arrears for the year ended 31st March, 2018 in the beginning of the year ended 31st March, 2019. Calculate subscriptions to be shown in Income and Expenditure Account for the year ended 31st March, 2019 and also show treatment of subscriptions in the Income and Expenditure Account and Balance Sheet.

Solution.

Subscriptions receivable for the year ended 31st March, 2019

= Number of Members × Annual Subscription

= 450 × Rs. 500 = Rs. 225,000.

Subscriptions Outstanding = Total Subscriptions – Subscriptions received for the year ended 31st March, 2019

= Rs. 225,000 – Rs. 211,000 = Rs. 14,000.

INCOME AND EXPENDITURE ACCOUNT

*Subscriptions in arrears for the year ended 31st March, 2018 in the beginning of 2018-19 was Rs. 4,500, out of which Rs. 4,000 were received in the year ended 31st March, 2019.

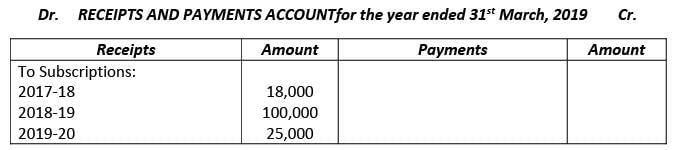

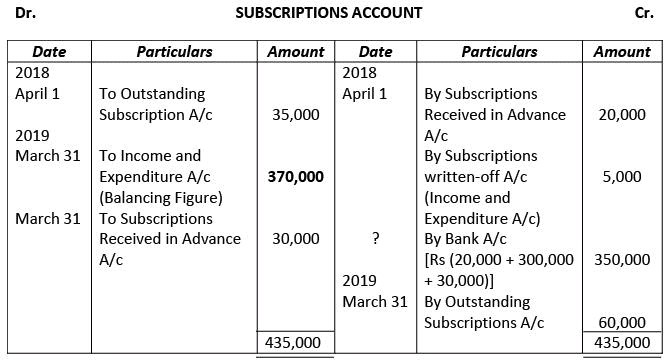

Example 6. From the following extract of the Receipts and Payments Account and the additional information, you are required to calculate Income from Subscriptions for the year ended 31st March, 2019 and show it in the Final Account of the Club.

Additional Information:

(i) Subscriptions outstanding as at 31st March, 2018: Rs. 20,000.

(ii) Subscriptions outstanding as at 31st March, 2019: Rs. 30,000.

(iii) Subscriptions received in advance as at 31st March, 2018: Rs. 20,000.

Solution.

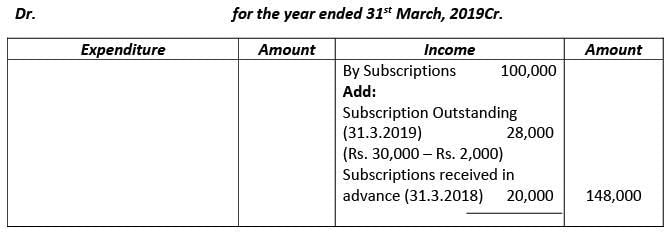

INCOME AND EXPENDITURE ACCOUNT

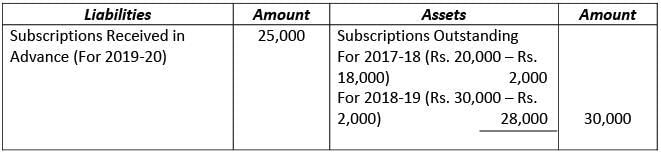

BALANCE SHEET as at 31st March, 2019

Note: Subscriptions outstanding as at 31st March, 2019 appearing on the asset side of the Balance Sheet is Rs. 30,000. It includes subscriptions outstanding for the year 2017-18 Rs. Rs. 2,000 [i.e., Rs. 20,000 – Rs. 18,000 (received during 2018-19)] and subscriptions outstanding for the year 2018-19, amounts to Rs. 28,000.

Note: Subscriptions outstanding as at 31st March, 2019 appearing on the asset side of the Balance Sheet is Rs. 30,000. It includes subscriptions outstanding for the year 2017-18 Rs. Rs. 2,000 [i.e., Rs. 20,000 – Rs. 18,000 (received during 2018-19)] and subscriptions outstanding for the year 2018-19, amounts to Rs. 28,000.

Example 7. From the following determine the amount of subscription that should be credited to Income and Expenditure Account for the year ended 31st March, 2019. Subscriptions received during the year were as follows:

For the year ended 31st March, 2018: Rs. 20,000

For the year ended 31st March, 2019: Rs. 300,000

For the year ended 31st March, 2020: Rs. 30,000

Subscription outstanding as at 31st March, 2018 was Rs. 35,000 out of which Rs. 5,000 was not recoverable. On that date, subscriptions received in advance for the year ended 31st March, 2019 were Rs. 20,000. Subscription still outstanding as at 31st March, 2019 amounted to Rs. 60,000.

Solution.

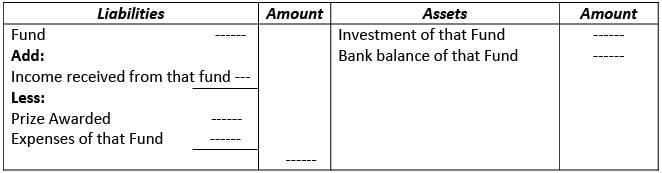

(b) Fund Based Accounting: It refers to an accounting system in which receipts and income related to that fund are credited (added) to that fund, not to Income and Expenditure A/c. Similarly, expenses related to that fund are charged to the fund (subtracted), not debited to Income and Expenditure A/c. Following are the examples of fund like Match Fund, Sports Fund, Prize Fund, Building Fund, etc.

Treatment of Fund

BALANCE SHEET as on 31st March, 20..

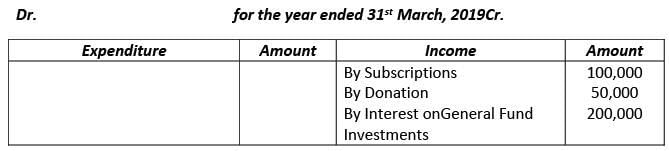

Example 8. The information given below relates to a sports club. Show them in the Income and Expenditure Account and the Balance Sheet of the club as at 31st March, 2019.

Sports Fund as at 1st April, 2018………......... Rs. 1,000,000

Sports Fund Investments………......... Rs. 1,000,000

Interest on Sports Fund Investments………......... Rs. 100,000 Donations for Sports Fund………......... Rs. 400,000 Subscription………......... Rs. 100,000

Donation………......... Rs. 50,000

Sports Prize Awarded……….........Rs. 300,000

Expenses on Sports Events………......... Rs. 100,000

General Fund………......... Rs. 2,000,000

General Fund Investments………......... Rs. 2,000,000

Interest on General Fund Investments………......... Rs. 200,000

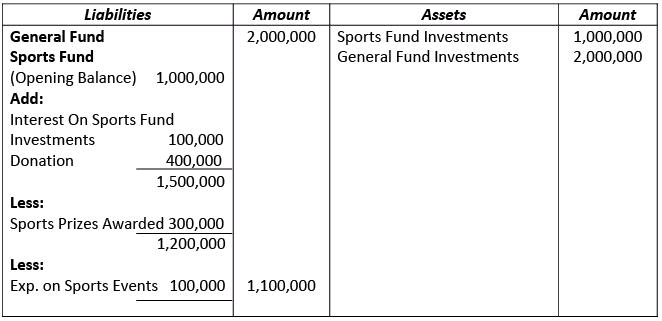

Solution.

INCOME AND EXPENDITURE ACCOUNT

BALANCE SHEET (Only Relevant Items) as at 31st March, 2019

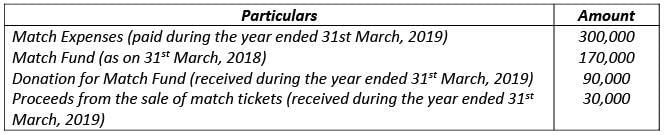

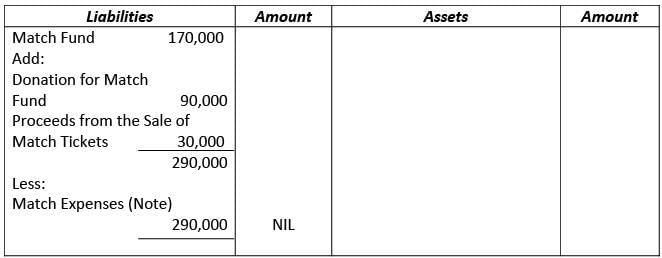

Example 9. From the following information of Indian Sports Club show the amounts of Match Expenses and Match Fund in the Financial Statement of the Club for the year ended on 31st March, 2018 and 31st March, 2019: Solution.

Solution.

BALANCE SHEET as at 31st March, 2018

BALANCE SHEET as at 31st March, 2029

INCOME AND EXPENDITURE ACCOUNT

INCOME AND EXPENDITURE ACCOUNT

Note: Match Expenses are Rs. 300,000 out of which Rs. 290,000 is met from Match Fund up to available fund and balance expenses of Rs. 10,000 are debited to Income and Expenditure Account. Thus, balances of Match Fund in nil in the Balance Sheet

Note: Match Expenses are Rs. 300,000 out of which Rs. 290,000 is met from Match Fund up to available fund and balance expenses of Rs. 10,000 are debited to Income and Expenditure Account. Thus, balances of Match Fund in nil in the Balance Sheet

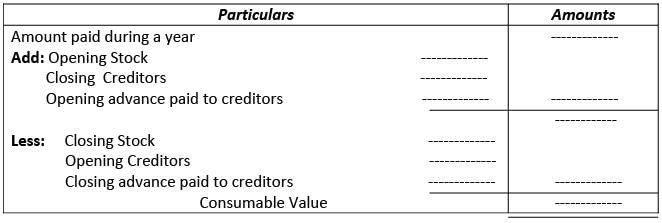

(c) Consumable Value of Items: Following items are not recorded in Income and Expenditure Account with all informations. Only consumable value of these items are recorded in debit side of Income and Expenditure Account and other informations like opening stock, closing stock, opening creditors, closing creditors, etc. are recorded in Opening and Closing Balance Sheet, These items are Medicine, Sports Materials, etc.

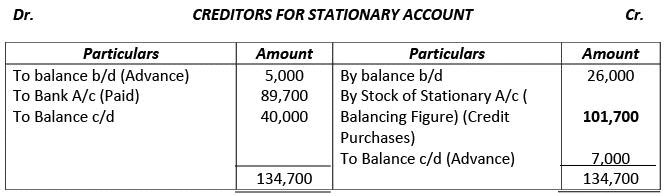

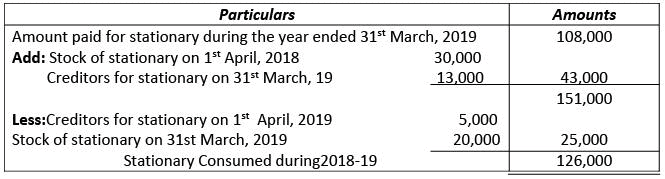

Example 10. From the following information, determine the amount to be debited to Stationary Account in Income and Expenditure Account for the year ended 31st March, 2019.

| Stock of stationary on 1st April, 2018 | Rs. 30,000 |

| Creditors for stationary on 1st April, 2018 | Rs. 20,000 |

| Amount paid for stationary during the year ended 31st March, 2019 | Rs. 108,000 |

| Stock of Stationary on 31st March, 2019 | Rs. 5,000 |

| Creditors for stationary on 31st March, 2019 | Rs. 13,000 |

Also, show the above items in the Income and Expenditure Account for the year ended 31st March, 2019 and in the Balance Sheet as at that date.

Solution.

Statement Showing Stationary Consumed during 2018-19

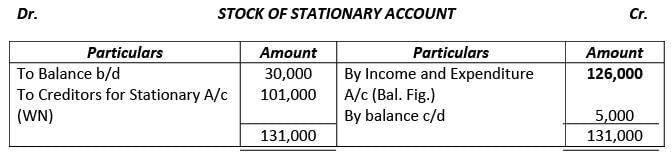

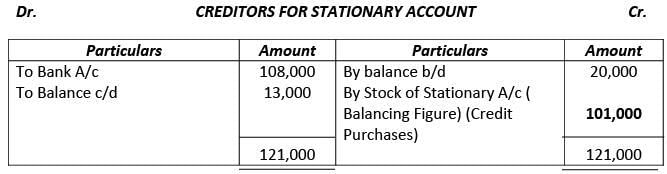

Alternative: Amount of Stationary consumed to be debited to Income and Expenditure Account can be also be computed by preparing Stock of Stationary Account as follows:

Alternative: Amount of Stationary consumed to be debited to Income and Expenditure Account can be also be computed by preparing Stock of Stationary Account as follows: Working Note: Calculation of Stationary purchased during the year:

Working Note: Calculation of Stationary purchased during the year:

Example 11. On the basis of the information given below, calculate the amount of stationary to be debited to Income and Expenditure Account of Good Health Sports Club for the year ended 31st March, 2019: Stationary purchased during the year ended 31st March, 2019 was Rs. 470,000.

Stationary purchased during the year ended 31st March, 2019 was Rs. 470,000.

Solution.

Good Health Sports Club

An Extract of INCOME AND EXPENDITURE ACCOUNT

Working Note:

Stationary Consumed (2018-19) = Opening Stock of Stationary + Purchases of Stationary – Closing Stock of Stationary

= Rs. 80,000 + Rs. 470,000 – Rs. 60,000 = Rs. 490,000.

Since stationary purchased during the year is given, creditors are already adjusted in it and, therefore, no treatment is given to creditors.

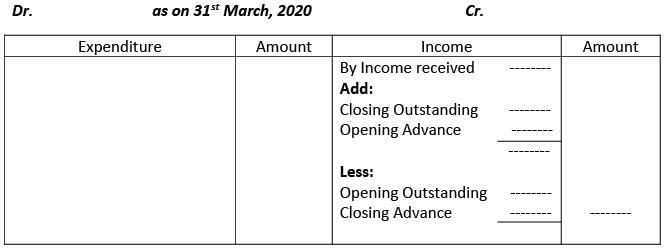

(d) Income Received: Income received by firm is recorded in credit side of Income and Expenditure Account. Only those incomes are recorded that are related to current year. If any amount related to previous year or next year are included in particular income that will be deducted. Same as, any amount related to current year is not received or received in advance in previous year are added. Examples of incomes are Entrance Fees, Rent, Locker Rent, etc.

INCOME AND EXPENDITURE ACCOUNT

Opening Balance Sheet

Closing Balance Sheet

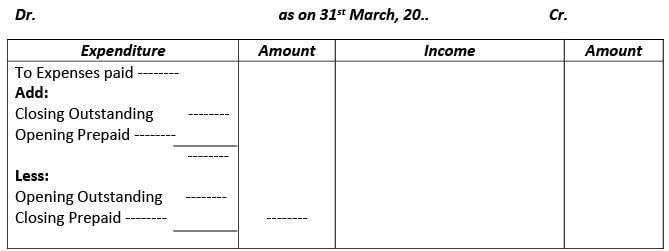

(e) Expenses Paid: An expense paid by a firm is recorded in debit side of Income and Expenditure Account. Only those expenses are recorded that are related to current year. If any amount related to previous year or next year are included in particular expenses that will be deducted. Same as, any amount related to current year is not paid or already paid in previous year are added. Examples of expenses are Salary, Rent, Wages, etc.

INCOME AND EXPENDITURE ACCOUNT

Opening Balance Sheet

Closing Balance Sheet

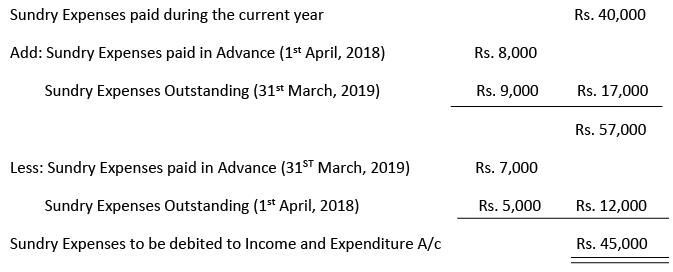

Example 12. How are the following items dealt in preparing Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date? Sundry Expenses paid during the year ended 31st March, 2019 Rs. 40,000.

Sundry Expenses paid during the year ended 31st March, 2019 Rs. 40,000.

Solution.

INCOME AND EXPENDITURE ACCOUNT (An Extract)

BALANCE SHEET(An Extract) as at 31st March, 2019

Working Note:

Working Note:

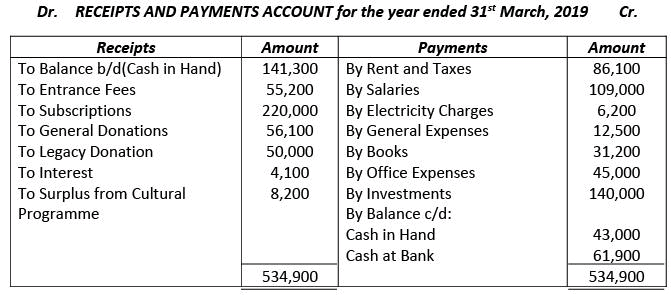

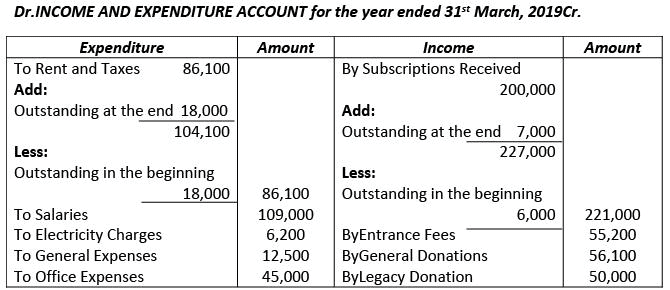

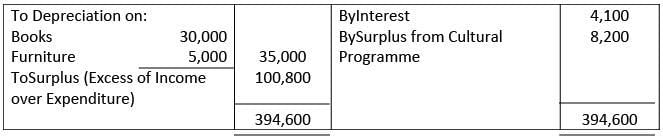

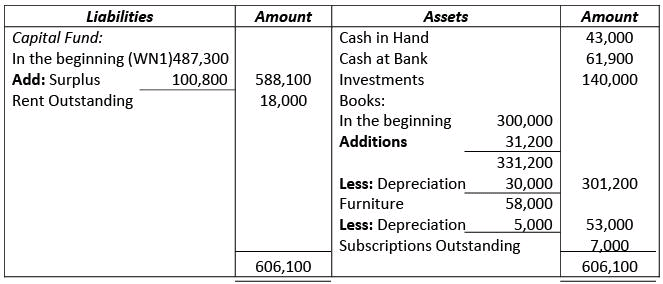

Example 13. From the following Receipts and Payments Account of Friends Club for the year ended 31st March, 2019, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date: Additional Informations:

Additional Informations:

(i) In the beginning of the year, the club had Books of Rs. 300,000 and Furniture of Rs. 58,000.

(ii) Subscriptions in Arrears on 1st April, 2018 were Rs. 6,000 and Rs. 7,000 on 31st March, 2019.

(iii) Rs. 18,000 was due by the way of Rent in the beginning as well as at the end of the year.

(iv) Write off Rs. 5,000 from Furniture and Rs. 30,000 from Books.

Solution.

Friends Club

BALANCE SHEET as at 31st March, 2019

Working Notes:

Working Notes:

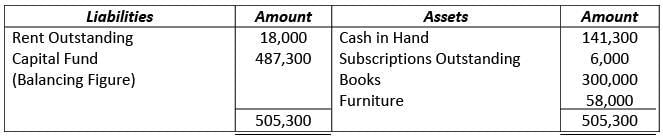

(i) Calculation of Opening Capital Fund:

BALANCE SHEET as at 31st March, 2018

(ii) Legacy Donation is credited to Income and Expenditure Account, it being not for specific purpose.

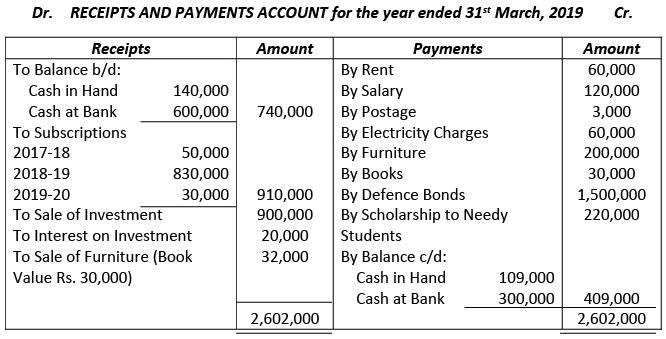

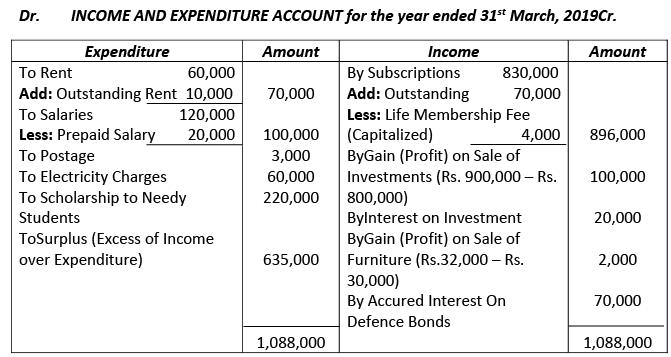

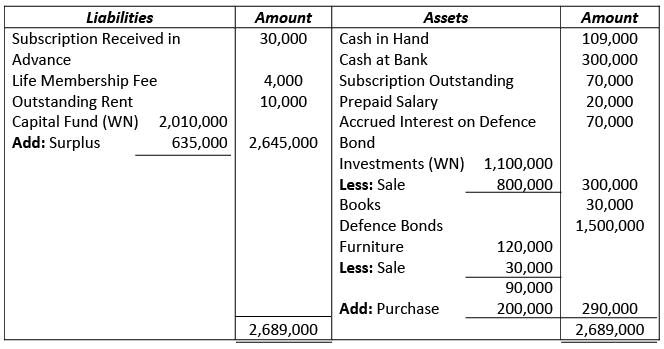

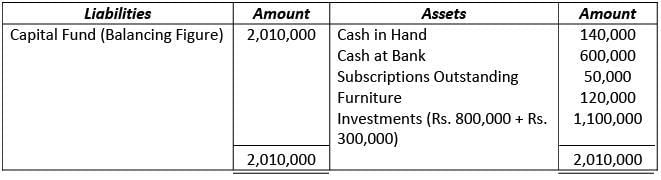

Example 14. Following is the Receipts and Payments Account of Rajdhani Charitable Trust: Prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as on that date after the following adjustments:

Prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as on that date after the following adjustments:

Subscription for the year ended 31st March, 2019 still due were Rs. 70,000. Interest due on Defence Bonds was Rs. 70,000. Rent Outstanding was Rs. 10,000. Book Value of Investment sold was Rs. 800,000, Rs. 300,000 of the investments were still in hand. Subscriptions received in the year ended 31st March, 2019 included Rs. 4,000 from a life member. Total Furniture on 1ST April, 2018 was worth Rs. 120,000. Salary paid for the year ended 31st March, 2020 is Rs. 20,000.

Solution.

Rajdhani Charitable Trust

BALANCE SHEET as at 31st March, 2019

Working Notes: Calculation of Capital Fund on 1st April, 2018:

BALANCE SHEET as at 31st March, 2018

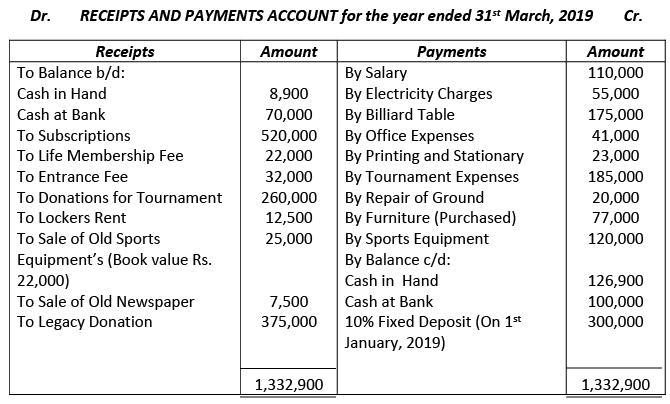

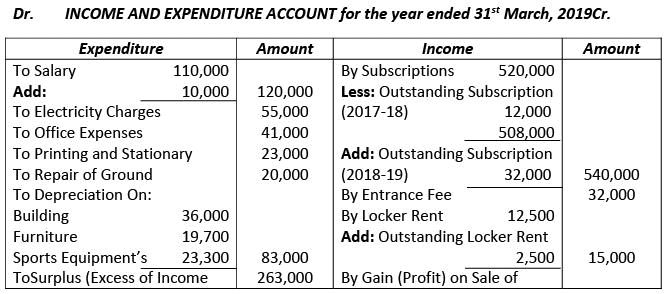

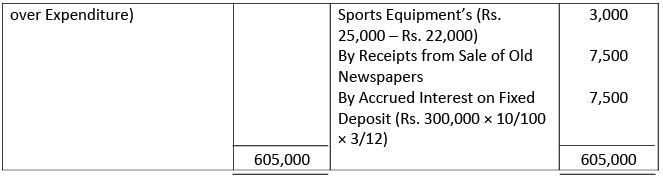

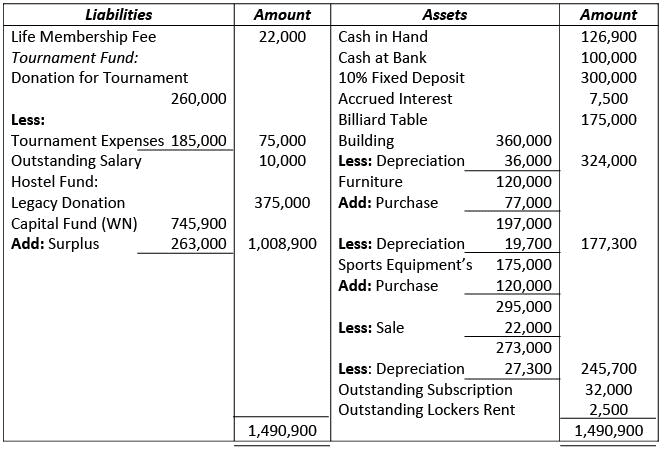

Example 15. Following is the Receipts and Payments Account of Indian Sports Club; prepare Income and Expenditure Account and Balance Sheet as on 31st March, 2019:

Other Information:

Subscription outstanding was on 31st March, 2018 Rs. 12,000 and Rs. 32,000 on 31st March, 2019. Lockers Rent outstanding on 31st March, 2019 Rs. 2,500. Salary outstanding on 31st March, 2019 Rs. 10,000.

On 1st April, 2018, club has building Rs. 360,000, furniture Rs. 120,000, Sports Equipment’s Rs. 175,000. Depreciation charged on these items @10% (including purchase).

Legacy Donation is for constructing hostel for sports persons.

Solution.

Indian Sports Club

BALANCE SHEET as at 31st March, 2019

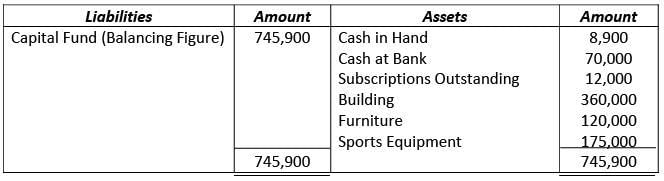

Working Notes: Calculation of Capital Fund on 1st April, 2018:

BALANCE SHEET as at 31st March, 2018

The document Financial Statements of Not- for-Profit Organizations | Accountancy Class 12 - Commerce is a part of the Commerce Course Accountancy Class 12.

All you need of Commerce at this link: Commerce

|

42 videos|168 docs|43 tests

|

FAQs on Financial Statements of Not- for-Profit Organizations - Accountancy Class 12 - Commerce

| 1. What are financial statements of not-for-profit organizations? |  |

| 2. What is the purpose of financial statements for not-for-profit organizations? | |

Ans. The purpose of financial statements for not-for-profit organizations is to provide transparency and accountability to stakeholders. These statements help donors, grantors, government agencies, and the public assess the financial health of the organization and how effectively it is using its resources to fulfill its mission. They also assist in decision-making, budgeting, and financial planning.

| 3. What are the key differences between financial statements of for-profit and not-for-profit organizations? | |

Ans. The key differences between financial statements of for-profit and not-for-profit organizations include the absence of an owner or shareholders in not-for-profit organizations. Instead of generating profits for distribution, not-for-profit organizations aim to reinvest their excess revenues into achieving their mission. Additionally, not-for-profit organizations often receive contributions and grants, which are accounted for differently from revenues in for-profit organizations.

| 4. How can financial statements of not-for-profit organizations be used for benchmarking and performance evaluation? | |

Ans. Financial statements of not-for-profit organizations can be used for benchmarking and performance evaluation by comparing their financial ratios and metrics with industry benchmarks or similar organizations. For example, comparing the organization's program expenses as a percentage of total expenses to industry standards can help assess its efficiency in delivering services. Similarly, analyzing liquidity ratios and fundraising efficiency metrics can provide insights into the organization's financial health and effectiveness.

| 5. What are the reporting requirements for financial statements of not-for-profit organizations? | |

Ans. Not-for-profit organizations are required to follow the reporting requirements set by accounting standards and regulatory bodies. In the United States, they are typically required to prepare financial statements in accordance with the Financial Accounting Standards Board's (FASB) Accounting Standards Codification (ASC) 958. These standards outline the presentation, recognition, and disclosure requirements for various financial statement elements and activities of not-for-profit organizations. Compliance with these reporting requirements ensures transparency and comparability among organizations in the sector.

Related Exams

About this Document

3.8K Views

4.80/5

Rating

Mar 28, 2025

Last updated

Document Description: Financial Statements of Not- for-Profit Organizations for Commerce 2025 is part of Accountancy Class 12 preparation.

The notes and questions for Financial Statements of Not- for-Profit Organizations have been prepared according to the Commerce exam syllabus. Information about Financial Statements of Not- for-Profit Organizations covers topics

like and Financial Statements of Not- for-Profit Organizations Example, for Commerce 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Financial Statements of Not- for-Profit Organizations.

Introduction of Financial Statements of Not- for-Profit Organizations in English is available as part of our Accountancy Class 12

for Commerce & Financial Statements of Not- for-Profit Organizations in Hindi for Accountancy Class 12 course.

Download more important topics related with notes, lectures and mock test series for Commerce

Exam by signing up for free. Commerce: Financial Statements of Not- for-Profit Organizations | Accountancy Class 12 - Commerce

Description

Full syllabus notes, lecture & questions for Financial Statements of Not- for-Profit Organizations | Accountancy Class 12 - Commerce - Commerce | Plus excerises question with solution to help you revise complete syllabus for Accountancy Class 12 | Best notes, free PDF download

Information about Financial Statements of Not- for-Profit Organizations

In this doc you can find the meaning of Financial Statements of Not- for-Profit Organizations defined & explained in the simplest way possible. Besides explaining types of

Financial Statements of Not- for-Profit Organizations theory, EduRev gives you an ample number of questions to practice Financial Statements of Not- for-Profit Organizations tests, examples and also practice Commerce

tests

Related Searches

practice quizzes

,ppt

,shortcuts and tricks

,Exam

,Objective type Questions

,Extra Questions

,Important questions

,Summary

,video lectures

,Previous Year Questions with Solutions

,Financial Statements of Not- for-Profit Organizations | Accountancy Class 12 - Commerce

,MCQs

,Sample Paper

,Free

,Financial Statements of Not- for-Profit Organizations | Accountancy Class 12 - Commerce

,study material

,Semester Notes

,past year papers

,Financial Statements of Not- for-Profit Organizations | Accountancy Class 12 - Commerce

,mock tests for examination

,Viva Questions

;

Additional Information about Financial Statements of Not- for-Profit Organizations for Commerce Preparation

Financial Statements of Not- for-Profit Organizations Free PDF Download

The Financial Statements of Not- for-Profit Organizations is an invaluable resource that delves deep into the core of the Commerce exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Financial Statements of Not- for-Profit Organizations now and kickstart your journey towards success in the Commerce exam.

Importance of Financial Statements of Not- for-Profit Organizations

The importance of Financial Statements of Not- for-Profit Organizations cannot be overstated, especially for Commerce aspirants.

This document holds the key to success in the Commerce exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Financial Statements of Not- for-Profit Organizations Notes

Financial Statements of Not- for-Profit Organizations Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Financial Statements of Not- for-Profit Organizations.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Financial Statements of Not- for-Profit Organizations Notes on EduRev are your ultimate resource for success.

Financial Statements of Not- for-Profit Organizations Commerce Questions

The "Financial Statements of Not- for-Profit Organizations Commerce Questions" guide is a valuable resource for all aspiring students preparing for the

Commerce exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Financial Statements of Not- for-Profit Organizations on the App

Students of Commerce can study Financial Statements of Not- for-Profit Organizations alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Financial Statements of Not- for-Profit Organizations,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Financial Statements of Not- for-Profit Organizations is prepared as per the latest Commerce syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up

within 7 days!

within 7 days!

Takes less than 10 seconds to signup